Despite the rumors yesterday, the imposition of the liability levy in the budget last night was something of a surprise. It will hit the big four, and one other, only at this stage. They need liabilities of more than $100 billion to be captured.

On one hand you could argue that it is a simple, if rather lazy revenue raising measure, which plays to the gallery in terms of banks universally being poorly perceived and is a vote of no confidence in the bank driven processes of cultural reform.

Or you can argue it is an appropriate response to the recent aggressive repricing of the mortgage books and growing profits, despite margin compression.

The Government conveniently linked it to the FSI “unquestionably strong” mantra, which is clever, but it is not necessarily directly connected.

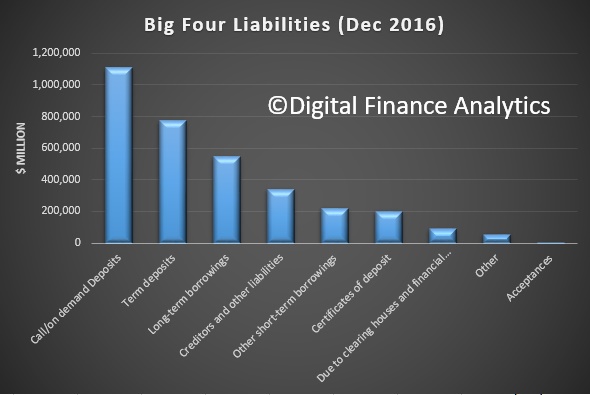

Which ever way you run the argument, it is worth looking in more detail at the numbers involved and how the banks may react. First, the budget papers said the big four banks had liabilities of $3.3 trillion, more than the national GDP. This is true. This number comes from the APRA Banks Performance data for December 2016.

Within the mix, more than $1 billion are on call deposits, and another $700m on term deposits.

Within the mix, more than $1 billion are on call deposits, and another $700m on term deposits.

Now, liabilities within the $250k consumer deposit protection scheme are excluded, as are those related specifically to capital ratios. It is not easy to separate this out from public data.

“Ordinary bank deposits and other deposits protected by the Financial Claims Scheme – including those held by everyday Australians – will be excluded from the levy base. It will not be levied on mortgages”.

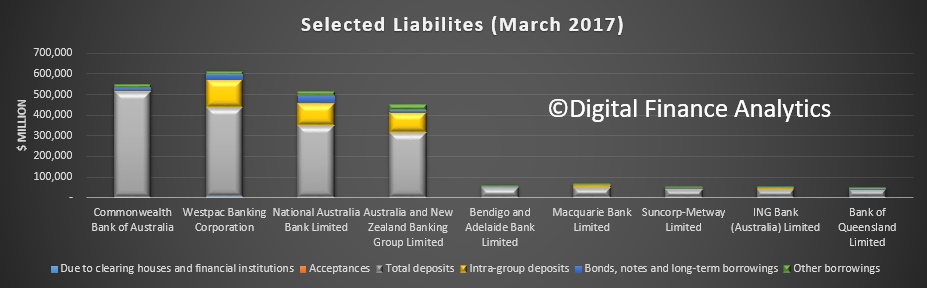

Individual banks have different liability structures. Looking at APRA data to March 2017, by bank, we see CBA has the largest volume of call deposits. This has been the case for many years, and reflects the heritage of the bank. Banks have been powering their deposits higher, especially term deposits, as part of the required net stable funding ratio, which is a mechanism to reduce their reliance on more risky overseas funding (the big banks still rely partly on US commercial paper to fund some of their book).

Presumably the fifth bank is Macquarie, as the other bank using the IRB capital approach. Other regionals are pursuing this route, which in theory should reduce their costs of capital, but in practice, as the Basel rules morph, the gap between standard and IRB is reducing (and perhaps to the point where there is little benefit in switching?). If they were to get bigger they might fall in the levy zone.

Presumably the fifth bank is Macquarie, as the other bank using the IRB capital approach. Other regionals are pursuing this route, which in theory should reduce their costs of capital, but in practice, as the Basel rules morph, the gap between standard and IRB is reducing (and perhaps to the point where there is little benefit in switching?). If they were to get bigger they might fall in the levy zone.

The measure is 6 basis points on the net liabilities, and is expected to yield about $1.5 billion each year. So, the assumption is 70-80% of liabilities may be captured. This would equate to 4-5% of annual profit of the big four, but may not be equally distributed.

In addition, banks have the option of switching their funding from bonds and other financial instruments to retail deposits below 250k to avoid the charge. So we would expect even greater competition for consumer deposits in the months ahead. A change in treasury mix will take some time, but may improve financial stability down the road.

Banks in Australia are still relatively inefficient (no world class cost income ratios here), so in theory they could drive out costs harder. But this is hard.

They can also adjust their deposit pricing for larger deposits, to cover the costs, or lift their lending rates to cover the costs of the levy. Whilst the ACCC has been charged with looking at mortgage rates and how they move, given the many moving parts between changes to capital ratios, repricing to adjust volume flow (especially in investor and interest only loans), and competitive issues, it will be hard to unscramble the egg to identify repricing connected to the levy within the bank treasury function. The upcoming APRA discussion on revised capital ratios will just add to the confusion.

Banks could also reduce their payouts to shareholders a little, and there are a number of reasons why future returns may be lower, perhaps coming back to an average of circa 12-13%. This is more to do with the slowing residential mortgage sector, which has the main growth engine for the industry for years. The recent round of results showed that, trading income apart, home lending drove the results, despite lower net interest margins.

The impact on smaller banks will be interesting, as they are at a pricing disadvantage of 10-15 basis points, or more. So even if the full weight of the levy was applied to the mortgage book of the majors, regionals will still find it hard to compete. Indeed the pressure for deposits may become more intense adding extra margin pressure.

With so many moving parts, the true impact will be hard to track, but I think you can assume that consumers will end up paying, either with higher mortgage rates, lower deposit rates, or via lower dividends. The ABA has already said as much. So really this is not so much a levy on the banks as a second order tax on consumers and small business.

Might be smart politics, but the impost on the community may well get lost in translation!

One thought on “What The Liability Levy May Mean”