The prospective sale of Firstmac underscores the dilemma for Non-Banks operating in the current environment. Pre-GFC, most were able to work a very effective Residential Mortgage Backed Securitisation (RMBS) model where bundles of loans were packaged up and sold to investors, many of whom were offshore. Then the GFC hit. As a result the securisation markets froze and funding all but stopped. It has hardly recovered.

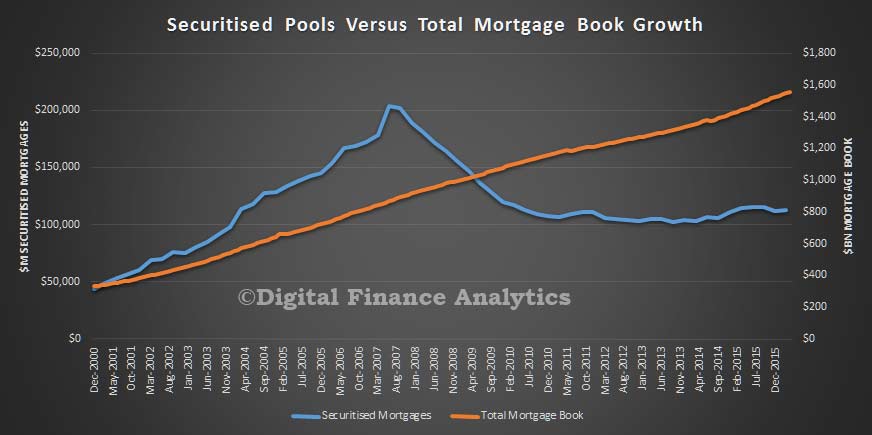

In this chart we compared the assets of securitised pools with the total mortgage loan growth in Australia, and it starkly shows the changes post the GFC. We used data from RBA and ABS to generate the data. As a result, the share of mortgages written by banks have lifted from 70% to well above 90%. Banks also have looked at other funding routes, (for example Bendigo Bank have moved from 20% to 6% RMBS, and this has created a capital headwind, so they will most likely focus on senior funding), because costs of securitising is still higher than before the GFC, when the Non-Banks had a significant funding advantage. Banks also are now subject to tighter capital rules for securitised pools.

In this chart we compared the assets of securitised pools with the total mortgage loan growth in Australia, and it starkly shows the changes post the GFC. We used data from RBA and ABS to generate the data. As a result, the share of mortgages written by banks have lifted from 70% to well above 90%. Banks also have looked at other funding routes, (for example Bendigo Bank have moved from 20% to 6% RMBS, and this has created a capital headwind, so they will most likely focus on senior funding), because costs of securitising is still higher than before the GFC, when the Non-Banks had a significant funding advantage. Banks also are now subject to tighter capital rules for securitised pools.

Here is the latest data on issuance from Macquarie.

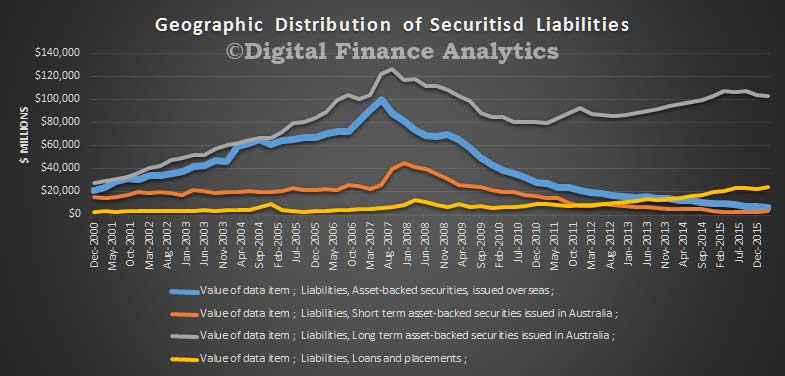

In addition, most deals which are done are in Australia, as the global demand for securitised paper is still well down as shown by this chart. Most deals now done to institutional investors in Australia, in long term instruments. We also see a rise in direct placements.

In addition, most deals which are done are in Australia, as the global demand for securitised paper is still well down as shown by this chart. Most deals now done to institutional investors in Australia, in long term instruments. We also see a rise in direct placements.

So, Non-Banks need alternative models to make their business work. Those who survive do so on the back of funding from investors, (which include some of the major banks, as well as retail super funds and sophisticated individuals). They also find it hard to compete in the current low interest rate environment making “meat and potato” loans, because the margins are compressed. As a result they will be looking for niche markets, such a low documentation loans, jumbo loans, investment loans, and credit impaired loans. Here they have an advantage as they are not under the APRA 10% speed limit for investment loans, and do not have to hold capital against these loans under the Basel III arrangements. They are merely answerable to ASIC.

So, Non-Banks need alternative models to make their business work. Those who survive do so on the back of funding from investors, (which include some of the major banks, as well as retail super funds and sophisticated individuals). They also find it hard to compete in the current low interest rate environment making “meat and potato” loans, because the margins are compressed. As a result they will be looking for niche markets, such a low documentation loans, jumbo loans, investment loans, and credit impaired loans. Here they have an advantage as they are not under the APRA 10% speed limit for investment loans, and do not have to hold capital against these loans under the Basel III arrangements. They are merely answerable to ASIC.

So we expect Non-Banks to operate in niche markets, funding their business from investors. We also expect to see more sales and consolidation.

One thought on “The Changing Face of the Non-Bank Sector”