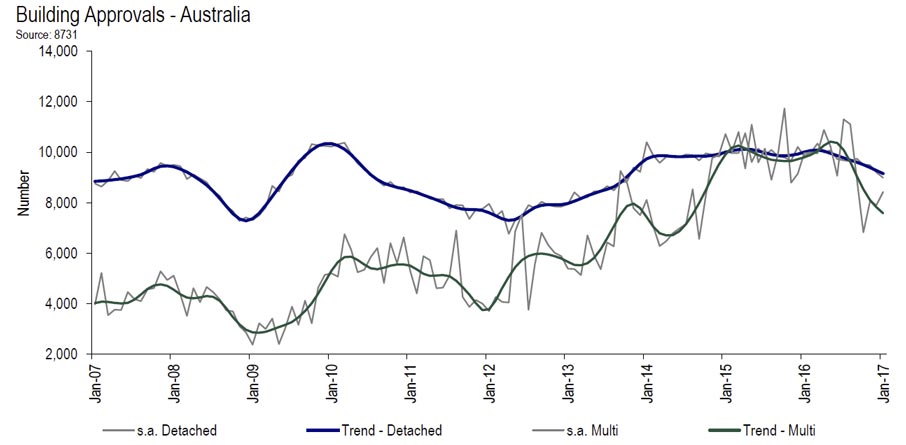

According to the Housing Industry Association, during the year ended September 2016, there were over 229,000 dwellings that commenced construction. While this is still an exceptionally high level of activity based on historical experience, the annualised level of commencements has eased since peaking at over 231,000 in the year ending in the March 2016 quarter. This is supportive of HIA’s view that the current new residential building cycle is likely to have peaked in 2016.

Detached houses

Despite the decline in the total number of commencements, the detached house segment of the market has proven resilient.

There were 29,634 detached houses commenced during the September 2016 quarter, which makes a total of 115,953 commencements in the year up to this point.

There were 29,634 detached houses commenced during the September 2016 quarter, which makes a total of 115,953 commencements in the year up to this point.

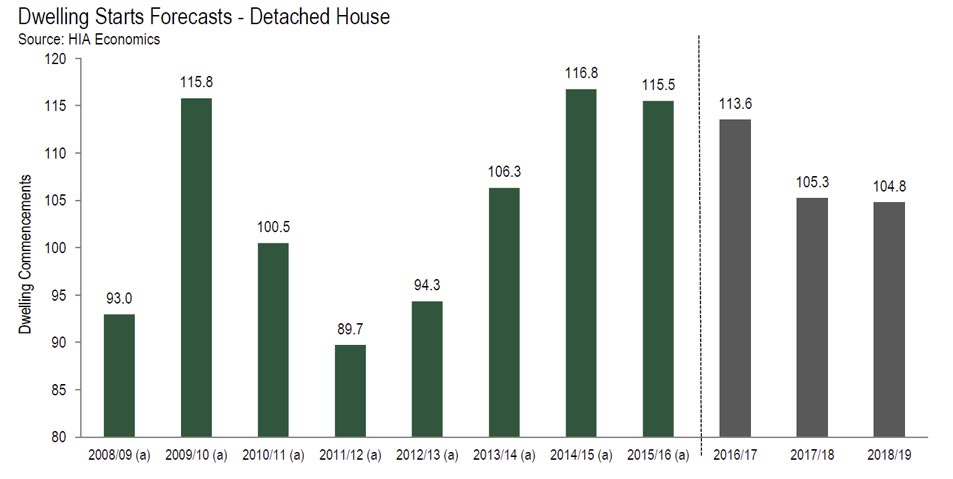

The prevailing dynamics in the detached house market during 2015/16 were a marked contraction in the level of activity in Western Australia counter balancing the ongoing resurgence in the Victorian and New South Wales markets. While there were variations in other state and territory markets, when we take a national perspective these two factors eclipsed the rest. However, we are now well into 2016/17 and approaching a new phase of the cycle which will have a fresh dynamic. The headwinds afflicting WA may soon subside and Sydney and Melbourne’s time in the sun may be drawing to a close.

From a national perspective, detached house commencements are forecast to ease by 1.7 per cent in 2016/17 ahead of a further decline of 7.3 per cent in 2017/18. After falling to a low of 104,800 starts in the 2018/19 year, the level of detached house building is forecast to gradually improve across the out years of the forecast horizon.

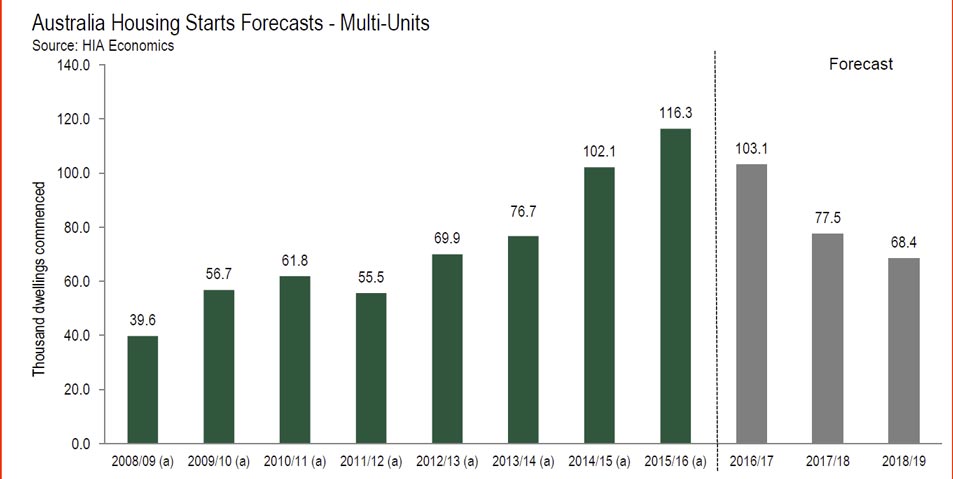

Multi-unit dwellings

The ‘multi-unit’ market has weakened overall. After a very strong result in the March 2016 quarter, the number of multi-unit commencements fell away quite sharply throughout the middle of the year.

However, there are markedly different trajectories for the semi-detached market (including townhouses, row and terrace type dwellings) and the market for apartments in buildings of four or more storeys.

However, there are markedly different trajectories for the semi-detached market (including townhouses, row and terrace type dwellings) and the market for apartments in buildings of four or more storeys.

The number of commencements for semi-detached dwellings continued to grow throughout the year. In contrast, the number of commencements for apartments in high-rise developments slowed as activity in Victoria and Queensland eased. The flow of new apartment projects getting underway in New South Wales has remained more buoyant and there is a record level of apartments in developments awaiting commencement.

In aggregate, there were a total of 25,202 multi-unit dwellings commenced in the September 2016 quarter, which is equivalent to 113,383 across the full year. HIA is forecasting that multi-unit dwelling commencements will remain at quite a high level in the 2016/17 financial year, albeit with an annual decline of 11.3 per cent. Looking beyond 2016/17 is when we anticipate commencements will post more significant declines. Multi-unit commencements are forecast to decline by around 25 per cent in 2017/18, and then by a further 12 per cent in 2018/19. The 2018/19 year is projected to be the low point of the cycle for multi-unit commencements, when 68,400 starts are forecast to occur.