In past years we have been highlighting the misaligned policy settings which have allowed home prices to balloon, household debt to soar, interest rates to slide and investors to gain more than a third of the market, higher than UK or USA. As banks have continued to lend and inflate their balance sheets and bolster their profitability, despite some tightening of standards; households are massively exposed.

The high debt means households have less disposable income and banks choosing to lend for housing rather than for productive business investment; both growth killing. The current capital rules have also encouraged more home lending and despite some recent tweaks, are still very generous.

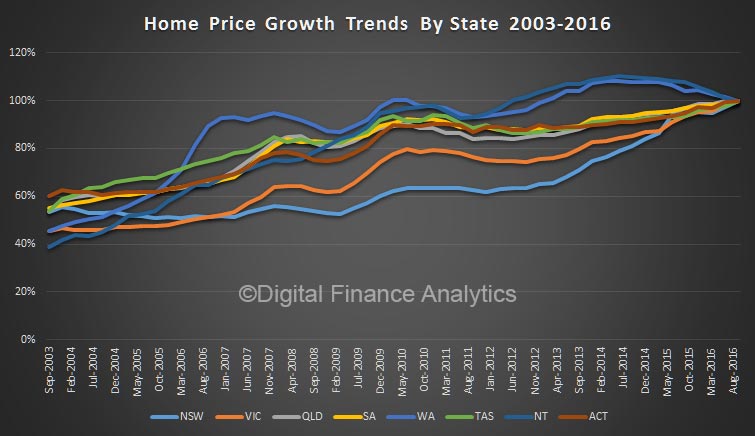

Here is a tracker of home price growth, working back from today’s prices. The problem is not just the Sydney and Melbourne markets. Its just that Sydney and Melbourne came later to the party.

Here is a tracker of home price growth, working back from today’s prices. The problem is not just the Sydney and Melbourne markets. Its just that Sydney and Melbourne came later to the party.

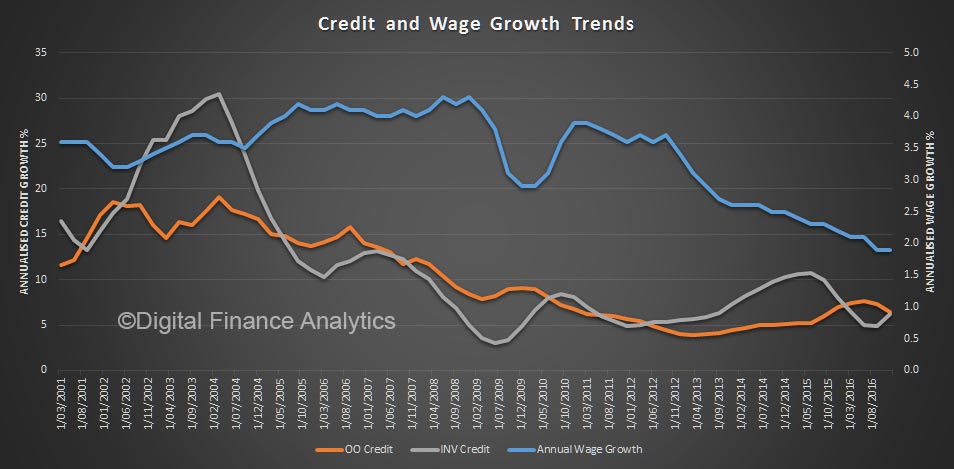

Wage growth is still slowing whilst debt continues to lift. This is a real problem.

Had the settings been adjusted several years ago, this was then a manageable problem, but I am not sure it is now.

Had the settings been adjusted several years ago, this was then a manageable problem, but I am not sure it is now.

If the RBA cuts the cash rate it will stimulate housing further, whilst if it lifts rates, then mortgage rates will rise (beyond the recent and continuing out of cycle uplifts) and move the ~22% of households in mortgage stress higher. Some will default. The international rate cycle is on the way up, not down.

If more homes come on the market they will continue to be snapped up by cashed up investors (often levering the capital in their existing property) and overseas buys, which account for perhaps 10% of transactions.

If first time buyers are offered incentives, be they stamp duty relief, money from parents, cash payments/grants or cannibalising their super, the net effect will be simply to drive prices higher, it being a zero sum game. We know there are more than 1 million households who “Want to Buy”. Plus more arriving thanks to migration.

Investors still want property, thanks to the tax breaks and years of sustained growth, despite crushed rental yields. If lending standards are tightened, and a lower speed limit put on investor lending, we will see more investors going to the smaller lenders and the non-bank sector. Also, some who already bought will be unable to refinance as they would now fall out of revised tighter requirements – about 9% of buyers fall into this category.

Switching away from stamp duty to a property tax may make more people trade, but that will just change the demand/supply curve, and perhaps drive prices even higher (as an artificial barrier is removed).

In fact, even joined up thinking which collectively attempts to cool the market whilst encouraging first owners into the market, is unlikely to succeed. Given the current political environment, this is even more unlikely.

Beneath all this is the financialisation of property, where it is seen as an investment class, not a source of shelter. This was called out recently in a UN paper, and is a global problem.

So, it looks to me as though we need a circuit breaker to kick-in, and that circuit breaker has to be a property correction, or even a crash.

A correction would scare off many investors, drop home prices to allow new entrants to purchase, and whilst many households would see paper profits falling, it was always funny money anyway. Banks would take a hit, but then they have the capital buffers in place, and the RBA backstop.

In parallel, we still will need tighter rules of lending – especially for investment purposes, and the removal of the tax breaks which underpin the sector. I think we need lending growth to track wage growth.

From here if we are careful, we can perhaps manage the settings such that such an explosion in prices wont happen again in the future.

But I wonder if we NEED a property crash. We certainly seem unable to manage under the current conditions.

2 thoughts on “Think The Unthinkable – The Property Crash We Have To Have?”