Ratesetter, a Peer To Peer Lender, has just launched in Australia.

“Redefining savings and loans in Australia. RateSetter connects lenders with creditworthy borrowers who want a simple, competitive personal loan. We are excited to be the first and only company in Australia to provide peer-to-peer lending to retail savers and investors. RateSetter is not a bank. RateSetter is part of a new generation of modern businesses, using technology to replace traditional middlemen and reduce the costs of providing financial services. We provide a transparent marketplace where lenders and borrowers, empowered by technology, can transact directly and share the benefits.

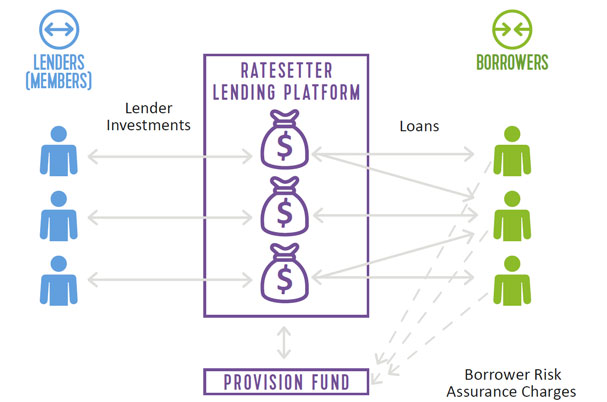

A peer-to-peer pioneer The RateSetter group in the United Kingdom was the first peer-to-peer lender globally to introduce the concept of a provision fund to help protect lenders from late borrower payments or default. This innovation represents a significant evolution in peer-to-peer lending. The money in the Provision Fund in Australia comes from borrowers, and is held on trust by an external trustee. Whilst the Provision Fund is not a guarantee or an insurance product, RateSetter Australia may make a claim on the Provision Fund on behalf of a lender in the event of a late borrower payment or default.

Regulated by ASIC RateSetter holds an Australian financial service licence and an Australian credit licence.”

RateSetter was founded in the United Kingdom in 2010 by ex-Lazard investment banker Rhydian Lewis and former Ashurst lawyer and RBS banker Peter Behrens. RateSetter has since attracted over 500,000 customer registrations and facilitated over $700 million in loans. RateSetter in the United Kingdom has been backed since the start of the company by private investors who have invested £8m of equity capital into the business. RateSetter in Australia is backed by RateSetter in the United Kingdom and other private investors. The launch of the Sydney office was kick-started with a $3.1m investment from local and international investors. RateSetter does not fund borrower loans. Rather, it is lenders who fund loans.

According to their product disclosure document RateSetter Australia is not a bank and your investment is not a deposit and does not benefit from depositor protector laws as if would if it were an amount deposited with an Australian ADI. All loans made to borrowers are subject to the provisions of the National Consumer Credit Protection Act 2009 (NCCP) and its related regulation. Your investment may be impacted if a borrower to whom your funds are on loan exercises certain rights under the NCCP, including requesting a variation to loan payments due to hardship, the effect of which is that the term of your investment may be impacted. An investor can lend in four different lending markets, with indicative terms of 1 month, 1 year, 3 years and 5 years. If you lend in the 1 Month or 1 Year lending markets, your funds may need to remain on loan to a borrower beyond the indicative term, although in such circumstances you should continue to receive borrower payments. You choose how much you wish to invest, in which lending markets, and at what rates. Their peer-to-peer information technology systems automatically match your funds to the loans of borrowers that have met our loan underwriting requirements. Whilst they perform comprehensive borrower risk assessment and lend only to creditworthy Australia-resident borrowers, there may be differences in the creditworthiness of borrowers to whom your funds are matched to. They only approve loan applications from creditworthy Australia-resident individuals aged 24 or over. They do not lend to businesses.

Loans to borrowers are between $2,001 and $35,000, for terms from six months to five years. Borrowers have a legal obligation to repay their loan in broadly equal payments each month over the term of the loan, with payments comprising both interest and principal. All loans to borrowers are governed by a standard form loan contract. Loans are unsecured. If a borrower defaults on a loan, they or a nominated third party may undertake a number of actions to pursue payments, which may include appointing an external collections agency or taking recourse to available legal remedies, including where appropriate, court action.

When you make an order to lend money in a lending market, your order may be matched to a single loan or multiple loans. This will depend on the amount of your order, the time your order was made relative to other orders in that lending market and the number and amount of loans available to be funded in that lending market.

Each borrower’s loan is governed by a single loan contract. The parties to the loan are the borrower and the Custodian. You as lender (and also other lenders, to the extent the loan is funded by more than on lender) do not have a contract with the borrower. Rather, when your funds are on loan, your RateSetter Account is updated to reflect that you have an interest in the relevant loan, and your rights in respect of that loan are governed primarily by the Constitution and this PDS. Importantly, when your funds are matched to a loan, you have a direct economic interest in that loan, and your interest in that loan is not directly impacted by the performance of other loans. Ratesetter believe that this is an important feature of any peer-to-peer lending investment structure.

The Provision Fund is a pool of money funded by borrowers and held on trust by an external trustee. RateSetter Australia may make a claim on the Provision Fund in the event of a borrower late payment or default on a loan. Any amount paid from the Provision Fund is credited to the lenders who funded the loan, in proportion to the amount funded by each lender.

As we predicted P2P lending is emerging in Australia. How well it develops will be determined by performance and demand. Demand exists certainly, according to our recent surveys.