The latest World Economic Outlook includes country specific observations. Of note is their view of the Australian housing market. “Domestically, the unwinding of housing-market tensions to date may presage dramatic and destabilising developments, rather than herald a soft landing”.

We think the risks are centred on the high-rise apartment sectors, especially in the east coast urban centres. In our worst case scenario, prices may fall up to 38%, in Melbourne but not immediately.

They also echo the latest GDP scenario, as reported, GDP was up thanks to LNG exports, but of course household income growth continues to languish.

Output growth will gradually strengthen towards 3% in 2017. Adjustment to declining resource-sector investment will continue. Growth in the non-resource sector will pick up, aided by dollar depreciation and a steady increase in household consumption. Further falls in the rate of unemployment are not expected to generate strong inflationary pressures and will help reduce inequality.

With receding risks from the housing boom, there is leeway for further monetary policy easing in the event of a new downturn. Close vigilance on housing-market developments is still required. Fiscal consolidation should be back-loaded in light of economic uncertainties. Tax reform should be a core element of structural policy.

Boosting productivity in Australia requires a focus on innovation. Targeted R&D policy, university-business linkages and effectiveness and efficiency of financial support for research are important. Ensuring strong competition, regulation that accommodates new internet-platform-based businesses, sound ICT infrastructure and continuing education reform are also key for productivity performance. In addition, education reform will boost inclusiveness through stronger low-end skills and better ICT infrastructure can reduce gaps in economic opportunity by improving access in rural areas.

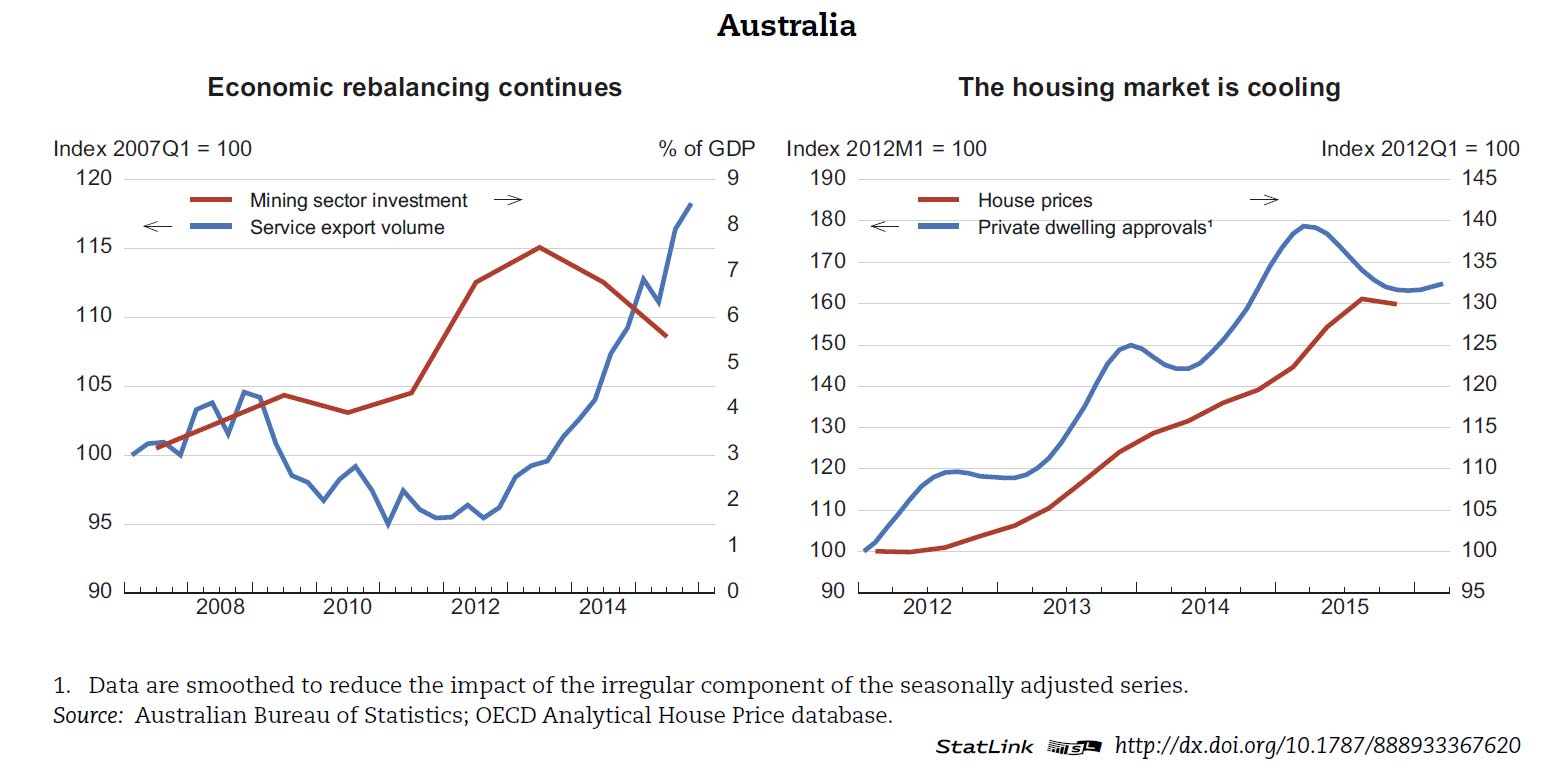

Rebalancing away from resource sectors continues

Resource-sector investment and employment face ongoing decline and commodity prices remain low, although new liquefied-natural-gas (LNG) production is boosting exports. Non-resource activity continues to pick up, especially in services exports, in part reflecting past depreciation of the currency. Non-resource activity is now driving employment growth. In addition, house-price and mortgage-credit growth are slowing, assisted by macro-prudential tightening. Consumer price inflation remains low. Also, uncertainty about global economic prospects is impacting Australia’s stock market and business sentiment.

Continued policy support for economic adjustment and productivity growth is required

The Reserve Bank reduced the policy rate by 25 basis points in May to 1.75%, the first rate change in 12 months, prompting a depreciation of the exchange rate. The projection envisages no further easing and assumes that policy-rate increases begin in 2017. Nevertheless, room for further rate cuts remains in the event of below-par growth. Fiscal policy needs to let the automatic stabilisers operate while keeping a medium-term objective of reducing the public-debt burden.

In structural policy, the OECD has long emphasised the scope for improving Australia’s tax system, in particular through greater use of efficient tax bases, such as the Goods and Services Tax and land tax, and reforms in specific areas, such as the taxation of pensions (“superannuation”). Reform to the latter could lower inequality by narrowing differences across households and between women and men among older cohorts. Strengthening of consumer-protection regulation in banking would also benefit households. Australia’s greenhouse-gas reduction policy relies principally on the Emission Reduction Fund, which provides financial incentives for businesses to reduce emissions and as of July 2016 it will backed by a safeguard mechanism that discourages offsetting emissions.

Boosting productivity requires strengthening capacities for generating and absorbing innovation. Research collaboration between the university and business sectors remains a point of weakness. Also, ensuring value-for-money in financial incentives, such as R&D tax breaks, remains a challenge. Policy responses to “disruptive” internet-platform innovations have generally been positive. Australian product and labour market regulation is broadly conducive to resource re-allocation, thus helping innovation via “creative destruction”. However, ICT infrastructure and services require ongoing policy attention and there is scope for greater innovation in public services.

The pick-up in growth will be gradual, but risks and uncertainties remain sizeable

Output growth is projected to be just under 3% in 2017. Negative effects from shrinking mining investment are set to ease and new LNG production will boost exports. Exchange rate depreciation and supportive macroeconomic policy have helped rebalance activity towards non-mining sectors. Employment growth will drive a further decline in the rate of unemployment. Household consumption is expected to remain solid, helped by further erosion of the household savings ratio.The pick-up in activity will not generate significant inflationary pressure, due to remaining economic slack.

Australia’s exposure to commodity-market developments, particularly those linked to the Chinese economy remains an important source of uncertainty and risk. Domestically, the unwinding of housing-market tensions to date may presage dramatic and destabilising developments, rather than herald a soft landing. Uncertainties on future economic policy ahead of the Federal election, which is scheduled for 2nd July, are also adding a degree of risk.