We have updated our analysis of assistance first time buyers are getting from their families in a desperate effort to get into the housing market at a time when the entry barriers in terms of price and affordability are as high as ever they have been. In addition, high loan-to-value loans are less available, so first time buyers need a larger deposit, and first owner grants are harder to access. Savings interest rates are also very low.

We released analysis a few months back, which caused quite a stir as it highlighted the inter-generational issues in play. We have now updated the quarterly analysis with data to December 2016.

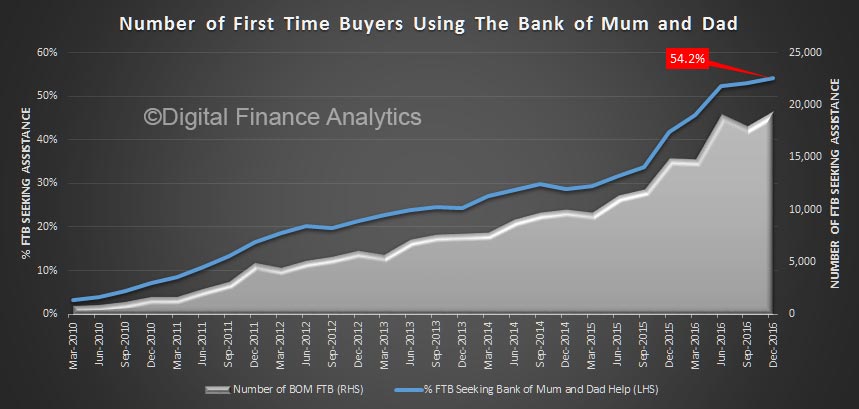

First, more first time buyers are getting help from parents – up to 54% in the past quarter. This help varies from a loan for a deposit, a cash present, help with transaction expenses, or ongoing assistance with mortgage repayments or other household expenses. Parental guarantees are falling out of favour.

Parents are able to assist, thanks to the wealth effect created by home price appreciation, which is still occurring in the eastern states, though more patchily elsewhere.

Parents are able to assist, thanks to the wealth effect created by home price appreciation, which is still occurring in the eastern states, though more patchily elsewhere.

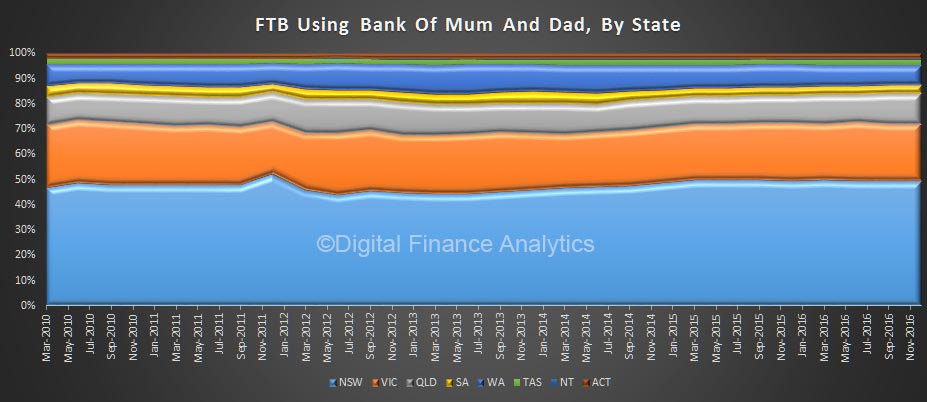

Just under half the assistance is going towards first time buyers in NSW (mainly Greater Sydney), where the affordability issues are most difficult, and home prices the highest. But other states are also, to some extent, also in the game. Ignoring the volume growth, the percentage mix has been relatively stable.

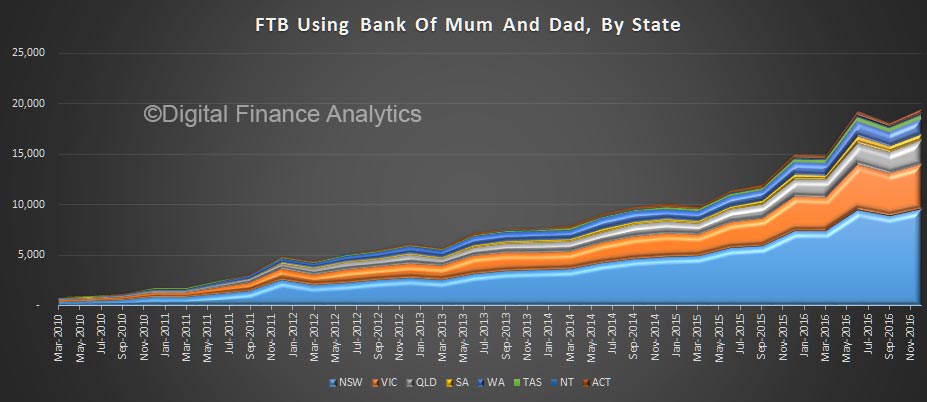

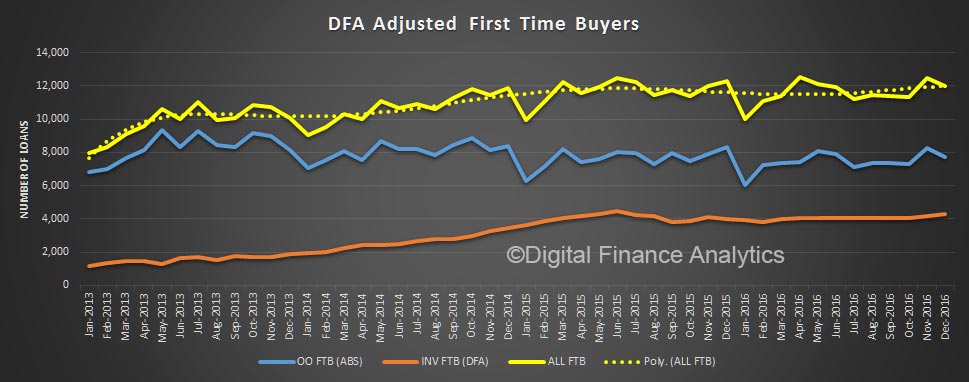

But here is the volume picture, which shows the relative number across states (note the small counts in some states are less statistically robust), but the trends are clear.

But here is the volume picture, which shows the relative number across states (note the small counts in some states are less statistically robust), but the trends are clear.

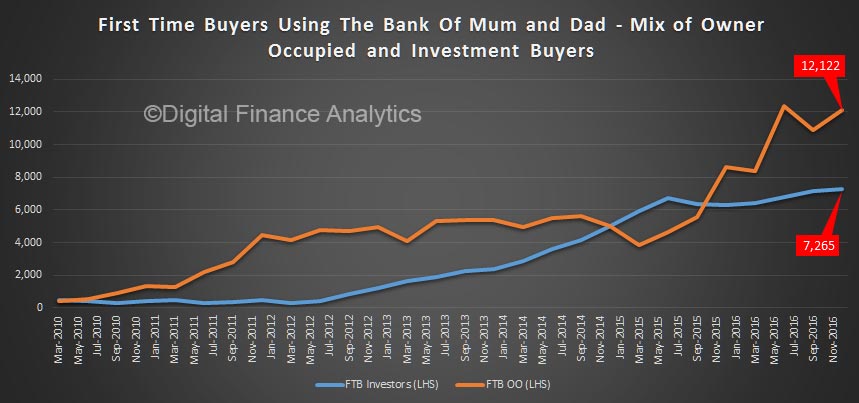

Another cut on the data is looking at the type of property being purchased. In 2015, more investment property was is the mix, but now the growth is among owner occupied purchasers.

Another cut on the data is looking at the type of property being purchased. In 2015, more investment property was is the mix, but now the growth is among owner occupied purchasers.

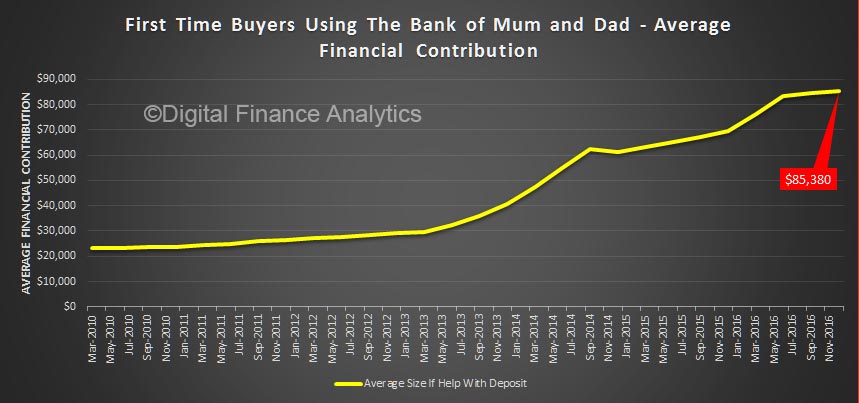

In terms of the value of the financial contribution, it varies. But for those making a loan or payment direct to assist in a purchase by way of a deposit, the average amount is now north of $85,000.

In terms of the value of the financial contribution, it varies. But for those making a loan or payment direct to assist in a purchase by way of a deposit, the average amount is now north of $85,000.

If parents bring forward payments to assist their offspring, it is worth asking whether this act of kindness may have unintended consequences.

If parents bring forward payments to assist their offspring, it is worth asking whether this act of kindness may have unintended consequences.

- First, are parents giving away some of their future financial security?

- If it is a loan, is the basis of repayment clear, and documented?

- When a bank assesses a mortgage application do they consider the source of the deposit – receiving a “seagull” lump sum is not the same as demonstrating a history of saving, and the risk profiles down the track are different.

It also raises complex questions around equity between siblings, and a whole raft of questions relating to inter-generational finance.

It is also worth remembering that more first time buyers are going to the investment sector before purchasing their own home for owner occupation, as our first time buyer tracker shows.

3 thoughts on “More First Time Buyers Open An Account At “The Bank of Mum and Dad””