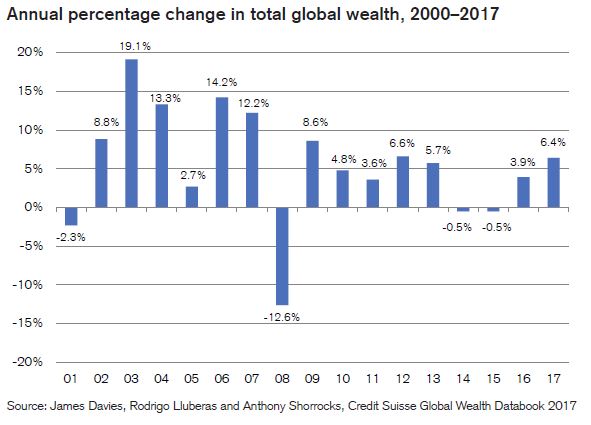

According to the eighth edition of the Credit Suisse Research Institute’s Global Wealth Report, in the year to mid-2017, total global wealth rose at a rate of 6.4%, the fastest pace since 2012 and reached USD 280 trillion. This reflected widespread gains in equity markets matched by similar rises in non-financial assets (home prices), which moved above the pre-crisis year 2007’s level for the first time this year.

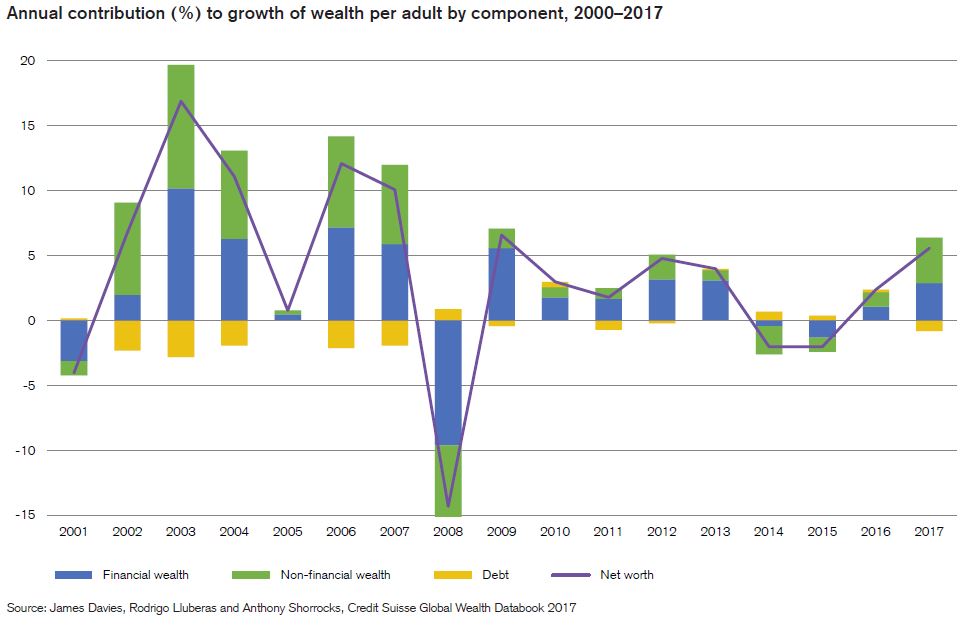

Wealth growth also outpaced population growth, so that global mean wealth per adult grew by 4.9% and reached a new record high of USD 56,540 per adult.

Wealth growth also outpaced population growth, so that global mean wealth per adult grew by 4.9% and reached a new record high of USD 56,540 per adult.

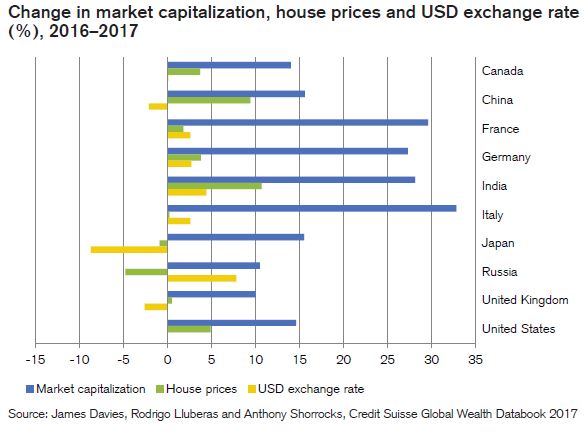

House price movements are a rough proxy for the non-financial component of household assets, and here most countries experienced a rise in values last year, although Japan (–1%) and Russia(–5%) were among the exceptions.

House price movements are a rough proxy for the non-financial component of household assets, and here most countries experienced a rise in values last year, although Japan (–1%) and Russia(–5%) were among the exceptions.

This year, the report includes a focus on Millennials’ wealth position and provides a comparison with earlier generations. They are not faring well, “Millennials are not only likely to experience greater challenges in building their wealth over time, but also greater wealth inequality than previous generations.”

This year, the report includes a focus on Millennials’ wealth position and provides a comparison with earlier generations. They are not faring well, “Millennials are not only likely to experience greater challenges in building their wealth over time, but also greater wealth inequality than previous generations.”

Australia

Household wealth in Australia grew at a fast pace between 2000 and 2012 in US dollar terms, except for a short interruption in 2008. The average annual growth rate of wealth per adult was 12%, with about half the rise due to exchange-rate appreciation against the US dollar. The exchange rate effect went into reverse for three years after 2012 and, like other resource-rich countries, Australia was badly hit by sagging commodity prices. Despite that slowdown, Australia’s wealth per adult in 2017 is USD 402,600, the second highest in the world after Switzerland.

The composition of household wealth in Australia is heavily skewed towards non financial assets, which average USD 303,200, and form 60% of gross assets. The high level of real assets partly reflects a large endowment of land and natural resources relative to population, but also results from high property prices in the largest cities.

Wealth inequality is relatively low in Australia, as reflected in a Gini coefficient of just 65% for wealth. Only 5% of Australians have net worth below USD 10,000. This compares to 19% in the UK and 29% in the USA. Average debt amounts to 20% of gross assets. The proportion of those with wealth above USD 100,000, at 68%, is the fourth highest of any country, and almost eight times the world average. With 1,728,000 people in the top 1% of global wealth holders, Australia accounts for 3.5% of this top slice, despite being home to just 0.4% of the world’s adult population.

Global Summary

Global Summary

We further saw an increase of 2.3 million US-dollar-millionaires, almost half of whom reside in the United States. Partially due to a 3% rise in the value of euro against the US dollar, we also note 620,000 new dollar-millionaires in the main Eurozone countries Germany, France, Italy and Spain. Another 200,000 joined in Australia and about the same number appeared in China and India together. We have seen a decline in millionaire numbers in very few countries, mostly associated with depreciating currencies: the United Kingdom lost 34,000 and Japan lost over 300,000.

Our home market Switzerland has seen wealth per adult increase by 130% to USD 537,600 since the turn of the century and continues to lead the global rankings. Again, we note that a large part of the rise is associated with the appreciation of the Swiss franc against the US dollar between 2001 and 2013. Nonetheless, measured in Swiss francs, domestic household wealth rose by 35% since 2000, which corresponds to an average annual rate of 1.8%. Switzerland today accounts for 1.7% of the top 1% of global wealth holders and over two-thirds of Swiss adults have assets above USD 100,000. 8.8% of Swiss are US-dollar millionaires and an estimated 2,780 individuals are in the ultra-high net worth bracket, with wealth over USD 50 million.

Financial assets continue to make up 54% of gross wealth in Switzerland, which is less than in Japan or the United States and debts average USD 140,500 per adult, which is one of the highest absolute levels in the world, although we continue to believe that the debt ratio reflects the country’s high level of financial development, rather than excessive borrowing.

On the worrying end, among the ten countries for which long series of wealth distribution are available, Switzerland is alone in having seen no significant reduction in wealth inequality over the past century.

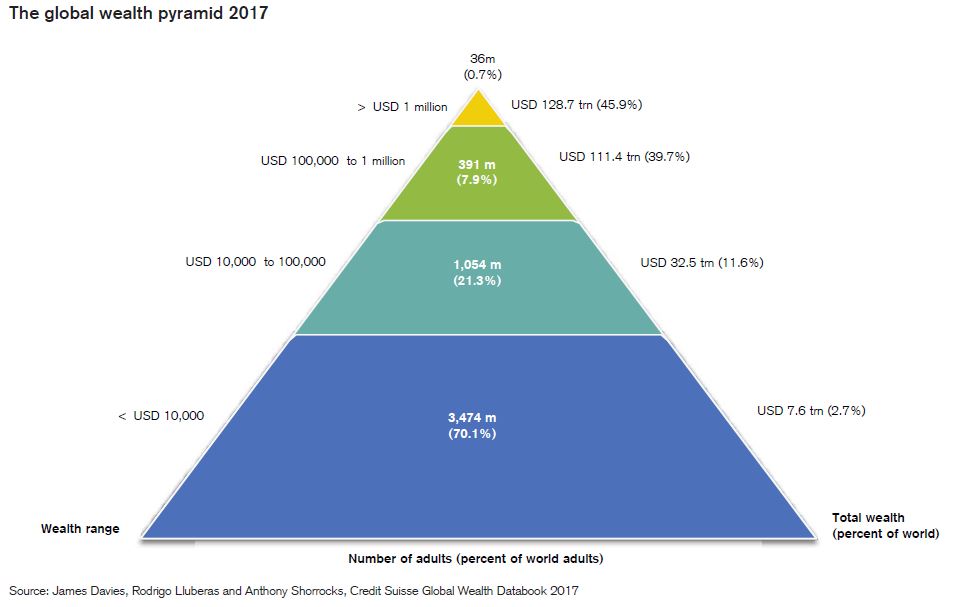

Looking at the bottom of the wealth distribution, 3.5 billion people – corresponding to 70% of all adults in the world – own less than USD 10,000.

Those with low wealth tend to be disproportionately found among the younger age groups, who have had little chance to accumulate assets, but we find that Millennials face particularly challenging circumstances compared to other generations.

Although relatively less severe in some emerging markets, capital losses during 2008–2009, high unemployment, tighter mortgage rules, growing house prices, increased income inequality, less access to pensions and lower income mobility have dealt serious blows to young workers and savers and hold back wealth accumulation by the Millennials in many countries. With the baby boomers occupying most of the top jobs and much of the housing, Millennials are doing less well than their parents at the same age, especially in relation to income, home ownership and other dimensions of wellbeing assessed in this report. While Millennials are more educated than preceding generations (we see an increase of more than 20% in tertiary education across OECD countries), we expect only a minority of high achievers and those in high-demand sectors such as technology of finance to effectively overcome the “millennial disadvantage.”

We also note that entrepreneurship, as measured by the fraction of self-employed workers, has been declining across OECD countries since the turn of the century, including Millennials who are generally touted as a generation of entrepreneurs.

One thought on “Global Wealth Higher, But More Uneven”