In the December 2014 edition of the RBA Bulletin, there is an important article on the emerging fast retail payment systems. Here are some of the most salient points:

In December 2014, a group of Australian financial institutions announced that funding had been secured for the next phase of the New Payments Platform (NPP), which will provide the capability for Australian consumers and businesses to make and receive payments in near to real time. The NPP is one example of a fast retail payment system, a number of which have been implemented in other countries in recent years.

Advances in technology – in particular improved telecommunications, faster processing speeds and wide penetration of internet connectivity – mean that real-time payments can be extended to the high-volume, low-value payments used by consumers and businesses (‘retail payments’). Systems implemented in a number of countries allow businesses and consumers to make and receive payments in near to real time, with close-to-immediate funds availability to the recipient. Fast retail payment systems can benefit end users of payments systems, and also payment providers themselves – for example, by replacing the use of relatively costly cheque payments with real-time transfers using a payment application on a mobile device.

Fast retail payments can be thought of as payments that are available for use by the recipient a short time after the payment has been initiated by the sender – within minutes, or indeed seconds. This contrasts with many established retail payment systems that rely on batch processing where funds are made available on the next business day, or even several days later – particularly in the case of cheques. There are three steps within the payment process relevant for achieving fast payments – clearing, posting and settlement. First, following the initiation of a payment by the customer (payer), the exchange of payment instructions and the calculation of payment obligations between financial institutions (referred to collectively as ‘clearing’) need to be performed in real time. Many retail payment systems have tended to clear payments infrequently in batches, making timely receipt of funds by the payee impossible. Second, the recipient’s financial institution must act on the payment instructions it receives in the clearing process to make funds available to the recipient (‘posting’) in near to real time. Finally, the payer’s financial institution needs to ‘settle’ the funds owing to the receiver’s financial institution for the payment. This typically occurs by transferring funds between accounts held by financial institutions at the central bank (Exchange Settlement Accounts in Australia’s case). Clearing and posting need to occur quickly for a system to be, in effect, a ‘fast’ system. However, settlement between financial institutions need not be completed before funds are made available to the recipient customer. There is therefore freedom for settlement to occur in a number of ways and indeed the fast retail payment systems implemented to date have taken varying approaches. While there have been significant developments in recent years, the concept of fast retail payments is not new. For example, Japan’s Zengin Data Telecommunication System (Zengin System) was established in 1973. The development of fast payment systems has generally occurred in one of two ways: through the extension of existing infrastructures (such as high-value systems or real-time ATM infrastructure) to accommodate high-volume, fast retail payments, or through new purpose-built infrastructure. In most cases, new specialised infrastructure has been adopted for retail payments, but there are examples of hybrid systems processing both high-value and retail payments. For example, Japan’s Zengin System clears both high-value and low-value funds transfers in near to real time, but settlement arrangements vary with transaction size. Switzerland’s Swiss Interbank Clearing (SIC) provides for near to real time clearing and settlement of high-value payments and some retail funds transfers. A range of other countries have introduced fast retail payment systems either as hybrid systems or as dedicated low-value systems since 2000. Australia’s NPP system will rely on newly developed clearing infrastructure, with settlement occurring in real time through a new component of the Reserve Bank’s high-value settlement system, the Reserve Bank Information and Transfer System (RITS).

The use of mobile phones as an access channel for fast payment services is a focus for a number of fast payment systems, including in the United Kingdom, Sweden and Singapore. This dovetails particularly well with some services for easier addressing of payments. For instance, the Paym service recently introduced in the United Kingdom enables mobile phone numbers to be used as payment addresses for person-to-person payments (Payments Council 2014). Users register their mobile phone number and link it to their bank account number. They can then send and receive real-time payments to other registered users using their mobile phone numbers through their bank’s internet portal.

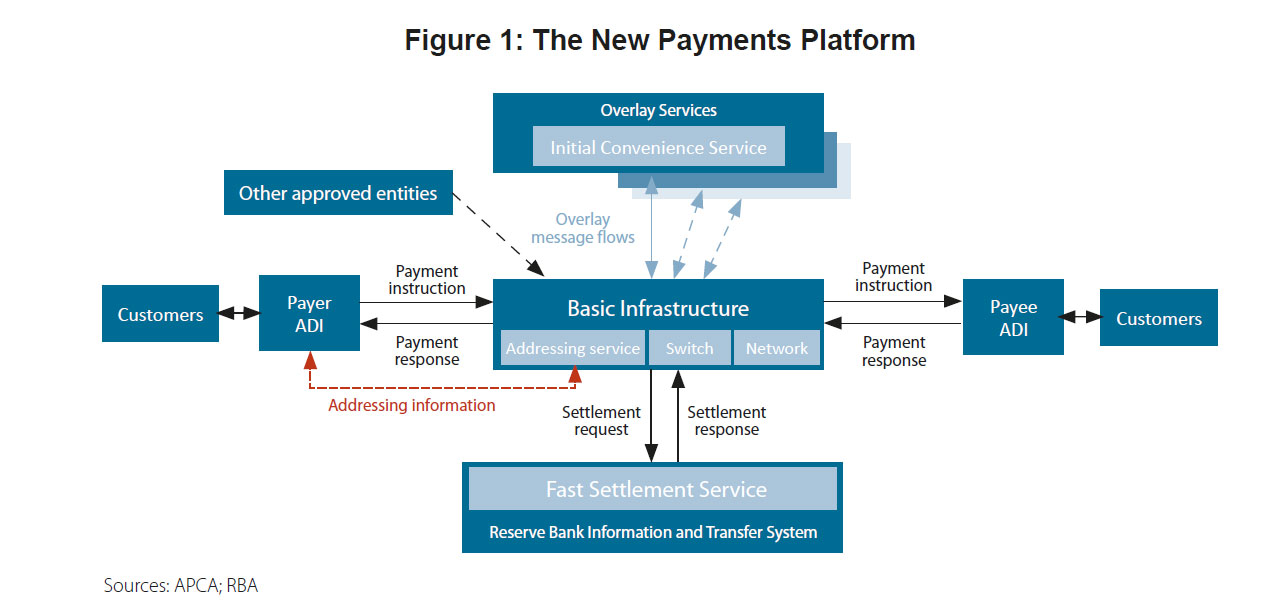

The broad approach to providing infrastructure that would support fast retail payments in Australia was established by the industry Real-Time Payments Committee (RTPC) and published in February 2013 (APCA 2013). The RTPC proposed the establishment of a mutual collaborative clearing utility to provide the payments infrastructure to which authorised deposit-taking institutions would be connected for real-time clearing of payments. This utility, known as the Basic Infrastructure (BI), will not be commercial in nature and will provide a platform through which a variety of payment services can be offered. While financial institutions will be able to offer basic payment services to their customers using only the BI, the model proposed by the RTPC anticipates that a variety of ‘overlay services’ will be able to use the BI to offer commercially oriented services, for instance through a commercial scheme. Participation by financial institutions in any particular commercial overlay would be voluntary. This model was chosen with the view that it would provide the greatest scope for innovation and competition between financial institutions and payment providers in the services that can be offered to end users. The RTPC also proposed that an agreed overlay service, referred to as the ‘Initial Convenience Service’ (ICS), would be built at the same time as the BI, to help establish a compelling proposition for use of the NPP from the outset. While the ICS will be the first overlay to give payments system users access to fast retail payments, it is intended to be the first of a number of overlay services that could be developed over time. The BI and the ICS comprise two of the three main components of the NPP. In addition, the Reserve Bank is developing a Fast Settlement Service (FSS) that will provide line-by-line real-time settlement of transactions processed through the NPP. This model will enable real-time clearing and settlement for retail payments, with the recipient’s financial institution able to provide fast access to funds without incurring interbank settlement risk. The interaction of these three components – BI, ICS and FSS – is illustrated below (Figure 1). Consistent with the approach taken in recently developed fast retail payment systems, the NPP will operate 24 hours a day, 7 days a week and will incorporate ISO 20022 messaging standards to facilitate the inclusion of richer remittance information with transactions. The NPP model also includes an addressing solution, enabling users to receive payments without having to supply BSB and account numbers to the payer. This combination – of real-time capability, 24/7 operations, richer messaging functionality and easier addressing – addresses the key gaps in the payments system identified by the Strategic Review. The capacity for new overlay services to utilise the system should also be a vehicle for innovation and competition.