The results from the 2017 Article IV consultation with China have been published. The IMF acknowledged that China’s continued strong growth has provided critical support to global demand and they commended the authorities’ ongoing progress in re-balancing the Chinese economy toward services and consumption.

They noted that economic activity had recently firmed and saw this as an opportunity for the authorities to accelerate needed reforms and focus more on the quality and sustainability of growth. They supported the importance of reducing national savings to help prevent domestic and external imbalances and emphasized the need for greater social spending and making the tax system more progressive. Stronger domestic demand helped further reduce China’s external imbalance, though it remains moderately stronger compared to the level consistent with medium-term fundamentals

They noted that economic activity had recently firmed and saw this as an opportunity for the authorities to accelerate needed reforms and focus more on the quality and sustainability of growth. They supported the importance of reducing national savings to help prevent domestic and external imbalances and emphasized the need for greater social spending and making the tax system more progressive. Stronger domestic demand helped further reduce China’s external imbalance, though it remains moderately stronger compared to the level consistent with medium-term fundamentals

Amid strong growth, the authorities have pivoted toward tightening measures, reflecting a greater focus on containing financial sector risks.

Amid strong growth, the authorities have pivoted toward tightening measures, reflecting a greater focus on containing financial sector risks.

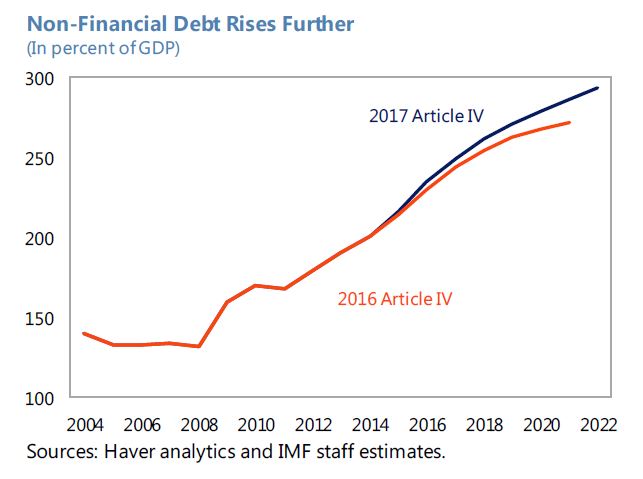

Debt is now expected to continue to grow as the IMF now assumes that the authorities will broadly maintain current levels of public investment over the medium term and not substantially consolidate the “augmented” deficit, reaching 92 percent of GDP in 2022 on a rising path. Private sector credit is projected to continue increasing over the medium term. Thus, total non-financial sector debt reached about 235 percent of GDP in 2016 and is projected to rise further to over 290 percent of GDP by 2022.

Debt is now expected to continue to grow as the IMF now assumes that the authorities will broadly maintain current levels of public investment over the medium term and not substantially consolidate the “augmented” deficit, reaching 92 percent of GDP in 2022 on a rising path. Private sector credit is projected to continue increasing over the medium term. Thus, total non-financial sector debt reached about 235 percent of GDP in 2016 and is projected to rise further to over 290 percent of GDP by 2022.

They say downside risks around the baseline have increased. A key consequence of the new baseline is that it envisions China using up valuable fiscal space to support a growth path with slower rebalancing and a higher probability of a sharp adjustment. Thus, if a sharp adjustment were to materialize, China would have lower buffers with which to respond. Such a potential adjustment could be triggered by several risks, including:

They say downside risks around the baseline have increased. A key consequence of the new baseline is that it envisions China using up valuable fiscal space to support a growth path with slower rebalancing and a higher probability of a sharp adjustment. Thus, if a sharp adjustment were to materialize, China would have lower buffers with which to respond. Such a potential adjustment could be triggered by several risks, including:

- Funding. A funding shock could come from at least two (related) pressure points. The first is the mostly short-term, “interbank” wholesale market (which includes banks’ claims on each other and on NBFIs). The second is a loss of confidence in short-term asset management products issued by NBFIs, or a run on the WMPs which fund them.

- Retreat from Cross-Border Integration. Should higher trade barriers be imposed by trading partners, the impact would depend on their coverage and magnitude, how exchange rates respond, and whether China retaliates. For example, an illustrative simulation in the IMF’s Global Integrated Monetary and Fiscal Model suggests that if the U.S. puts a 10-percent tariff on Chinese exports and China allowed its real exchange rate to adjust, real GDP in China would fall by about 1 percentage point in the first year. If China retaliated with similar tariffs on U.S. imports, its GDP would contract further. However, given the complexity of global trade relationships and uncertainty regarding how exchange rates would adjust, the effect could be larger and more disruptive.

- Capital Outflows. Pressure on the exchange rate could resume because of a faster-than-expected normalization of U.S. interest rates, much weaker growth in China, or some other shock to confidence. In an extreme scenario, the pressure could lead to renewed large reserve loss and eventually a potential disruptive exchange rate depreciation. However, this risk is likely small in the short run due to the stronger enforcement of CFMs, the prominence of state-owned banks in the foreign exchange market, and ample foreign exchange reserves.

While agreeing on the growth outlook, the authorities disagreed about the associated risks. The authorities agreed that 2017 growth was likely to exceed marginally the 6.5 percent full year target. This implied some deceleration during the course of the year and would result in inflationary pressure remaining contained and a broadly unchanged current account. For the medium term, though the authorities shared the view that their 2020 target of doubling 2010 real GDP would likely be reached, they viewed the debt build-up thus far as manageable and likely to slow further as their reforms take effect. They also explained that their “projected growth targets” were anticipatory and not binding. They underscored that reaching the desired quality of growth was a greater priority than the quantity of growth. The authorities viewed domestic concerns, such as high financial sector leverage, as manageable considering ongoing reforms and Chinese-specific strengths, such as high domestic savings. They saw the external environment as facing many uncertainties, such as an unexpected fall in global demand or a retreat from globalization.

The IMF conclude that:

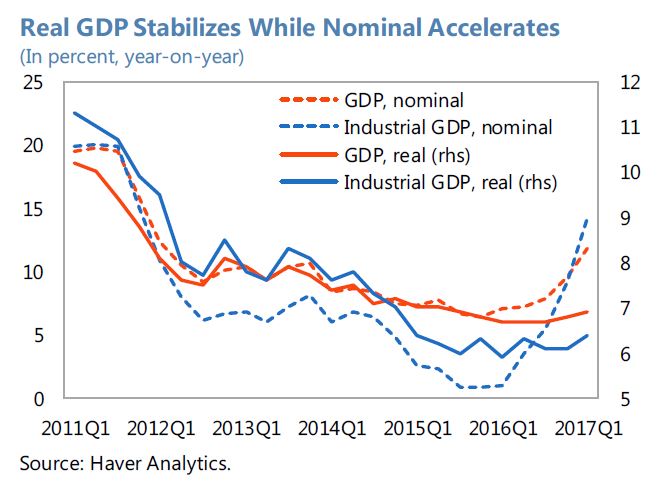

China continues to transition to a more sustainable growth path and reforms have advanced across a wide domain. Growth slowed to 6.7 percent in 2016 and is projected to remain robust at 6.7 percent this year owing to the momentum from last year’s policy support, strengthening external demand, and progress in domestic reforms. Inflation rose to 2 percent in 2016 and is expected to remain stable at 2 percent in 2017. Important supervisory and regulatory action is being taken against financial sector risks, and corporate debt is growing more slowly, reflecting restructuring initiatives and overcapacity reduction.

Fiscal policy remained expansionary and credit growth remained strong in 2016. Growth momentum will likely decline over the course of the year reflecting recent regulatory measures which have tightened financial conditions and contributed to a declining credit impulse.

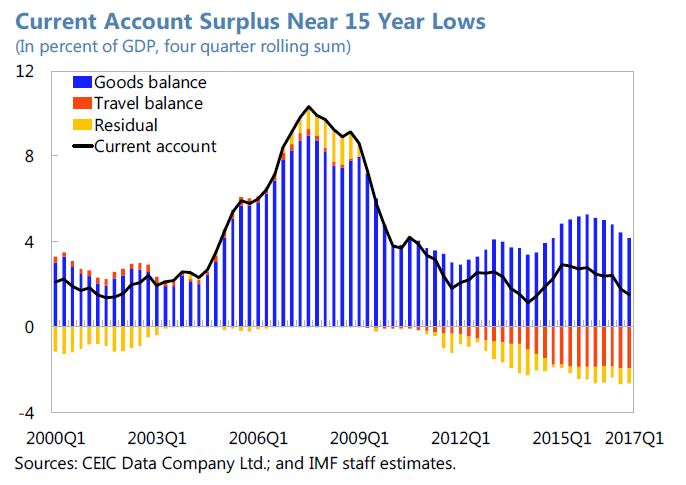

The current account surplus fell to 1.7 percent of GDP in 2016, driven by a sharp recovery in goods imports and continued strength in tourism outflows. It is projected to further narrow to 1.4 percent of GDP this year, due primarily to robust domestic demand and a deterioration in terms of trade. Capital outflows have moderated amid tighter enforcement of capital flow management measures and more stable exchange rate expectations. After depreciating 5 percent in real effective terms in 2016, the renminbi has depreciated some 2¾ percent since then and remains broadly in line with fundamentals.