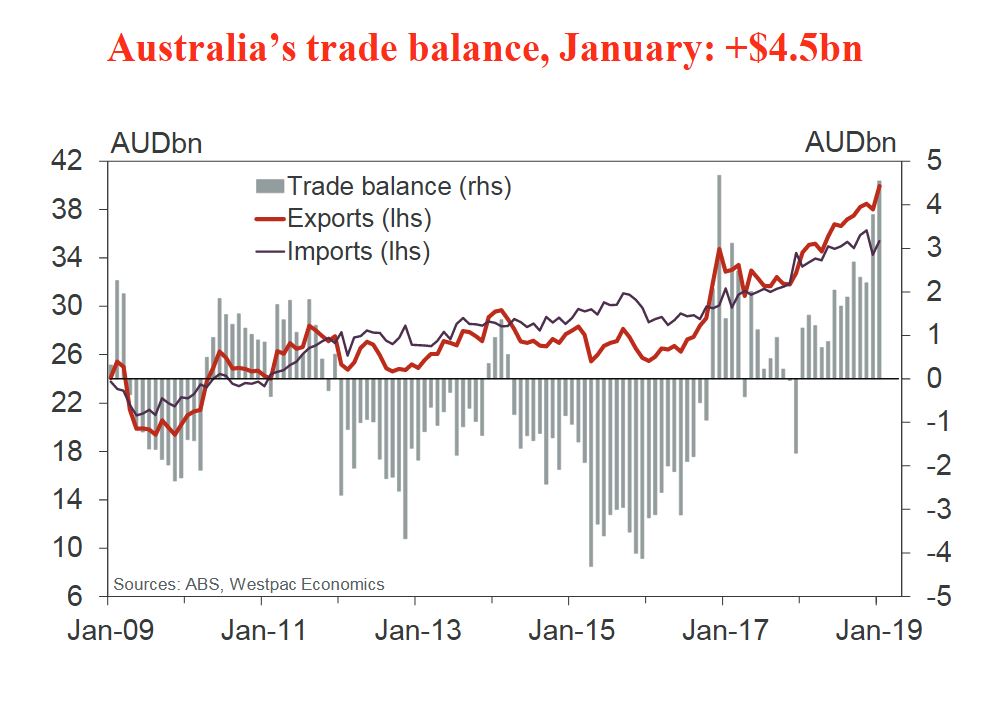

The ABS released the latest trade data to end January 2019. The surplus jumped to $4.5bn which is the second highest on record. The largest was $4.7bn surplus in December 2016.

Westpac highlighted that the January outcome was a $0.8bn improvement on December and exceeded expectations (market median $2.75bn and Westpac $3.1bn).

Imports did rebound in the month, +3.3%, following a 5.5% fall last month (vs a forecast +4%).

Exports were much stronger than anticipated, increasing by 5.0%, up $1.9bn (vs a forecast +2.2%).

Export strength was largely centred on a sharp rebound in gold off a low base, up 174% (Westpac expected a 75% rebound).

In dollar terms, gold accounted for $1.4bn of the $1.9bn increase in total exports in the month.

Coal exports rose 6%, following a couple of softer months, and metal ores increased by 3.4%, boosted by the higher iron ore price. But rural exports have been more resilient over the past couple of months – however the drought in NSW and surrounds remains a considerable headwind.

Metal ores and coal both advanced in January, up a combined $0.6bn.

The trade surplus widened in 2018 and in to 2019 on higher export earnings, boosted by rising commodity prices.

Notably, commodity prices have surprised to the high side in part due to supply disruptions having an amplified impact in a market where supply and demand are in relatively tight balance.

The $4.5bn surplus for January compares with a Q4 monthly average of $2.8bn.

The surplus for Q1 as a whole is expected to be a material improvement on that in Q4, with export volumes forecast to rise (following a disappointing second half of 2018) and on a likely further increase in the terms of trade.

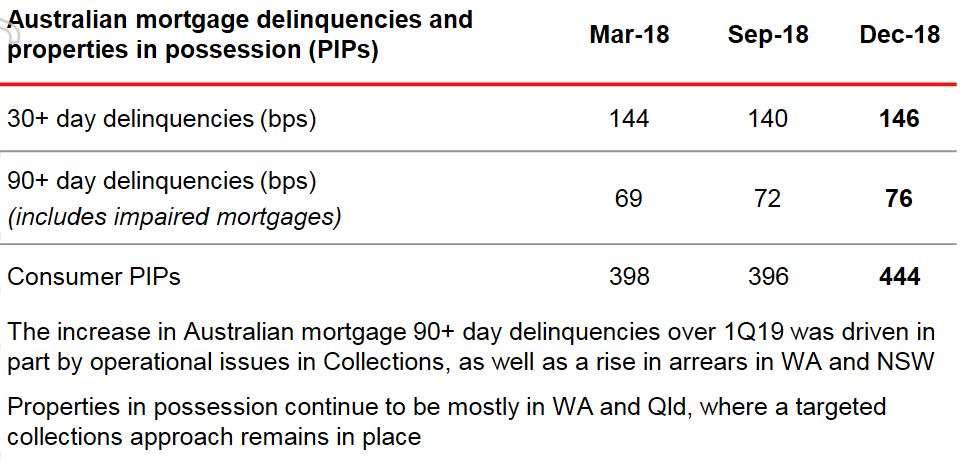

Westpac released their Pillar 3 report for December 2018, plus data on asset quality funding and capital. Of most interest to me was their mortgage data, which shows loan volume growth slowing, and rising delinquencies. The number of properties in possession rose from 396 to 444 in a quarter!

They said their audited statutory net profit for 1Q19 was $1.95 billion, comparable to 2H18.

They reported net interest margins excluding treasury was higher following repricing last year. There was a weaker contribution from treasury.

Provisions were $4,066 million compared with Sep 18’s $3,053.

On 1 October 2018 Westpac adopted AASB 9 and AASB 15. The models for implementation of these standards are still to be finalised and so current changes associated with implementation are preliminary and may change. These will be finalised with Westpac’s First Half 2019 results.

Some transitional impacts from the adoption of AASB 9 have included: i) an increase in collectively assessed provisions of $974 million; ii) a reduction in retained earnings and an increase in deferred tax assets; iii) a $3.9 billion reduction in risk weighted assets; iv) a rise in reported stressed assets; and• v) a 2 basis point increase in the CET1 capital ratio.

Impairment charge was $204 million. $30m pre-tax in insurance claims for Sydney hailstorms are expected.

Westpac showed the slowing in mortgage lending we are seeing across the majors.

Mortgage Interest only lending was 32% of portfolio at 31 Dec 2018 (down from 35% at 30 Sep 2018). Investor lending growth, using APRA extended definition, 0.8% pa

They have a portfolio of IO loans, some at 10 years plus. 16% expire this year.

Australian mortgage delinquencies were 4 basis points higher over the quarter while Australian unsecured delinquencies were also higher, up 10 basis points. The number of properties in possession rose from 396 to 444 in a quarter!

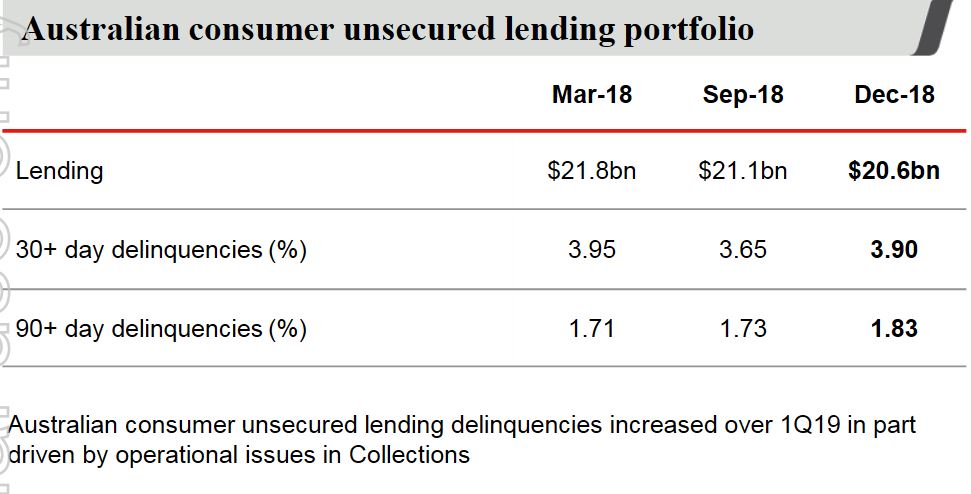

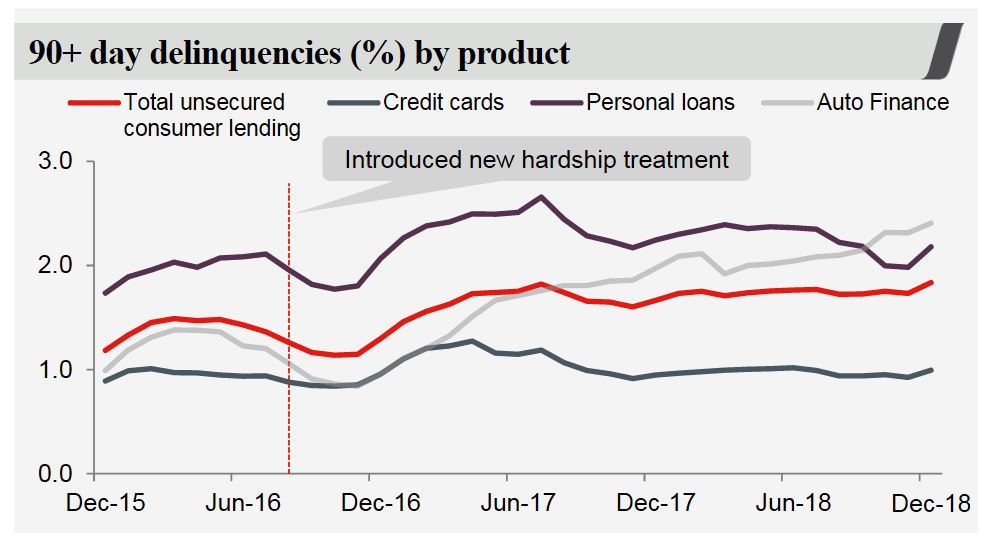

Australian unsecured 90+ day delinquencies increased to 1.83% (up 10bps over the quarter)

The Group’s common equity Tier 1 (CET1) capital ratio was 10.4% at 31 December 2018. The ratio was lower than the 10.6% reported for September 2018 after payment of Westpac’s final dividend (net of DRP), which reduced the CET1 capital ratio by 69 bps. Excluding the dividend payment, the CET1 capital ratio increased 49 basis points.

Liquidity coverage ratio (LCR) 128%, net stable funding ratio (NSFR) 112%

$16bn of term funding was raised during 4 months to 31 January 2019

Finally, a warning about capital.

Australia’s big banks may struggle to raise the amount of extra capital they require under new rules proposed by the country’s banking regulator, a senior executive at Westpac Banking Corporation said in an interview published on Monday.

The

mooted requirements, which the country’s four largest lenders said

would mean they need to raise between A$67 billion and A$83 billion over

four years ($48 billion to $60 billion) are sound in principle but

tough to achieve, Westpac treasurer Curt Zuber told the Australian

Financial Review newspaper.

“As we go through cycles, it is

potentially problematic for the banks to get the volumes they need in an

economic way for the system which allows for the balance we want to

achieve,” he said.

ASIC is appealing last year’s landmark Federal Court decision, determinedto prove two Westpac subsidiaries provided personal financial advice despite not being licensed to do so, via Financial Standard.

In

December 2018, Justice Jacqueline Gleeson determined Westpac Securities

Administration Limited (WSAL) and BT Funds Management (BTFM) had

breached the Corporations Act in 2014, during two telephone campaigns in

which staff recommended the rollover of superannuation accounts to

Westpac/BT super products.

However,

the judge said ASIC failed to prove the phone calls constituted

personal financial advice. Under their respective AFSLs, WSAL and BTFM

are only licensed to provide general advice.

ASIC has now filed an

appeal of the decision, seeking greater clarity and certainty as to the

difference between general and personal advice for consumers and

financial services providers.

“The

dividing line between personal and general advice is one of the most

important provisions within the financial services laws. It directly

impacts the standard of advice received by consumers,” ASIC deputy chair

Daniel Crennan said.

“This is why ASIC brought this test case and

ASIC believes further consideration by the full court of the Federal

Court is necessary to better inform consumers and industry.”

The

case concerned 15 phone calls which the judge determined to be general

advice “because the callers did not consider one or more of the

objectives, financial situation and needs of the customers to whom the

advice was given.”

However, in 14 of the 15 calls, the law was

breached by the implication that the rollover of super funds into a BT

account was recommended. While not dishonest, the product advice was not

provided efficiently, honestly and fairly, the judge deemed.

Westpac incurred a first strike against its remuneration report at its annual general meeting this week, where chairman Lindsay Maxsted said the ruling would send a strong message to the board; via InvestorDaily.

CEO Brian Hartzer along with Mr Maxsted also addressed the royal

commission, the bank’s financial performance for the past year and the

executives’ remuneration in the company’s AGM.

Peter Hawkins, non-executive director, retired following the AGM,

after 10 years of being on the board. Westpac will be electing two new

non-executive directors in the first half of calendar 2019.

While the poll on the remuneration report among shareholders had not

been completed at the time of the chairman’s address, more than half of

the votes already received were against the resolved salaries.

“Feedback from shareholders has varied, but the key point from those

voting against the remuneration report has been that although the board

took events over the year into account, many have questioned whether we

went far enough, particularly in reducing short-term variable reward

paid to the CEO and other executives,” Mr Maxsted said.

The short-term variable reward for the Westpac CEO and group

executives in Australia were on average, 25 per cent lower than last

year.

No long-term variable reward was vested in 2018. Around one-third of

the board’s potential remuneration forfeited, which Mr Maxsted said was

equivalent to about $18 million.

The CEO saw his short-term variable reward outcome cut by 30 per cent, or $900,000 over the past year.

The largest individual year on year reduction was 50 per cent, although Westpac did not disclose who it was, or for what reason.

“This is entirely consistent with the relatively weak performance of

shares in the banking sector, including Westpac, over the last few

years, including the 2018 financial year,” Mr Maxsted said.

“Putting this another way, for the CEO, his total variable reward outcome was 36 per cent of his total target variable reward.”

The chairman said the key failings from Westpac in light of the royal

commission were not fully appreciating the underlying risks in the

financial planning business, employee remuneration contributing to poor

behaviour and inadequacy in dealing with complaints.

“Better training and supervision, changes to the way financial

planners were remunerated, and better documentation of advice was

required,” Mr Maxsted said.

“As we have seen across the industry, where we get it wrong, the remediation is costly,” Mr Hartzer said.

“What has been clear is that we have not always embedded strong

enough controls and record-keeping around ensuring that customers

received the advice they had signed up for.”

Mr Maxsted also cited Westpac’s slowness in focusing on non-financial risks.

“In 2018, our financial performance was mixed; we have further built

on the balance sheet and financial strengths that are a hallmark for

Westpac but our annual profit was relatively flat over the year,” Mr

Maxsted said.

Cash earnings for the year ended 30 September was $8 billion, $3

million up on the year before. Reported profit reached $8.1 million,

increasing by 1 per cent from the prior corresponding period.

Business Bank grew profits by 8 per cent and New Zealand was up 5 per

cent. Excluding the cost of remediation provisions, BT’s profit was

down 1 per cent.

Institutional Banking saw its profit go down by 6 per cent, which Mr

Hartzer said largely represents a slowdown in financial markets

activity.

The bank also saw a slowdown in housing lending, with credit growing

5.2 per cent in the past 12 months, when it was 6.6 per cent in 2017.

“The group began the year solidly with good growth and well-managed

margins in the first half. Conditions in the second-half, however, were

more difficult with higher funding costs, lower mortgage spreads, and a

reduced markets and treasury contribution,” Mr Maxsted said.

“In addition, we needed to lift provisions associated with customer

refunds and regulatory/litigation costs as we address some of the legacy

issues alluded to earlier.”

The board determined a final dividend of 94 cents per share,

unchanged over the prior half and consistent with the final dividend for

2017. The full year dividend comes to 188 cents per share, unchanged

from the year before.

Mr Maxsted also noted Westpac removing grandfathered commission

payments in the past year, saying it was the first in the market to do

so.

“With revenue growth continuing to be a challenge, we have re-doubled

our efforts to reduce costs by simplifying our products, automating

process and modernising our technology platform,” Mr Hartzer said.

“Over recent years, we have delivered productivity savings of around

$250-300 million per year. In 2019, we aim to lift that to more than

$400 million – almost one third higher than 2018.”

Mr Maxsted also mentioned the bank’s development of its new Customer

Service Hub, the group’s multibrand operating system. The system is now

in pilot and will go live with new Westpac mortgages in 2019.

In terms of outlook, Mr Hartzer said that while it seemed positive as

a whole for the Australian economy, for banks, it looked more

challenging.

“Although credit quality is likely to remain a positive, low interest

rates, slowing credit growth, and a fall in consumer and business

confidence – especially about house prices – puts pressure on bank

earnings growth,” he said.

In commercial litigation, as in most litigation, there is an emphasis on trying to settle matters early before they are heard in court.

In criminal law matters the prosecutions encourage early guilty pleas in exchange for lower penalties.

The Australian Securities and Investments Commission (ASIC) has been increasingly resorting to early settlements as a means of achieving cheaper and quicker outcomes.

The quick win for ASIC is an enforceable undertaking and a media release. The quick win for the other party is avoiding a drawn-out court case and being able to get on with its business.

Courts usually rubber-stamp them

Where the alleged breach of the law is serious, necessitating a large penalty, a judge has to formally approve the settlement, in a hearing until now regarded as something of a rubber-stamping exercise.

He rejected the joint application for settlement between ASIC and Westpac Banking Corporation for a penalty of A$35 million.

The problem, as he pointed out was that it was not clear from the agreed facts what actual contraventions of the National Consumer Credit Protection Act 2009 Westpac had been accused of.

He asked ASIC and the Westpac to redraft the agreed settlement and return to court by 27 November 2018.

To establish the law and what happened

The case matters because the Financial Services Royal Commission has been examining the use of computer programs to determine the ability of borrowers to repay loans.

It is possible that many Westpac loans were approved to customers who would have been found to be unable to meet the repayments had their individual circumstances been examined, and it is possible that is in breach of the law.

But without a clear judgment or a clear statement of facts for the court to examine, or a clear judgment from the court, it is impossible to tell.

That’s why Justice Perram said no, to establish what the law requires and what Westpac did.

Author: Michael Adams Professor of Corporate Law & Governance, School of Law, Western Sydney University

The use of HEM may well be back in play, following the latest from the Westpac ASIC case. Given that at some banks HEM is still being used for around half of applications, and the Royal Commission commented specifically in the use of HEM, perhaps the law needs to be changed.

The core of the argument is whether the loans were unsuitable, and that it seems would depend of the ultimate progress of the loan subsequently. In other words, it cannot be proved to be unsuitable until it falls over. ASIC would need to prove the loan was unsuitable!

Actually we think the law says lenders have to verify expenses, and in other cases, for example in pay day lending specific inquiries are required as part of the assessment.

But its a clear as mud at the moment! When is unsuitable lending to be demonstrated. This will have a significant impact on any potential class actions. Expect bank share prices to rise!

A federal court has rejected a $35million fine for Westpac after it admitted breaking responsible lending laws, via MPA.

Last year the Australian Securities and Investments Commission (ASIC) began proceedings against Westpac in relation to its use of the Household Expenditure Measure (HEM) when assessing home loans.

ASIC argued the bank failed to conduct proper assessments to ascertain whether borrowers could afford to repay their loans.

The $35m penalty was a negotiated settlement between the two parties after it admitted to using the HEM to assess borrowers’ living costs.

ASIC alleged the bank approved around 50,000 home loans based on a HEM benchmark, even though expenses were presumably higher.

Among the explanations of the reasons behind the decision to refuse the penalty, Justice Nye Perram said the court had been asked to determine whether Westpac was in contravention of Section 128 of the National Consumer Credit Protection Act 2009.

Justice Perram said this section merely prohibits the making of a credit contract where an assessment has not been carried out. Regardless of the bank using the HEM benchmark, an assessment was in fact carried out.

Justice Perram also said that although both parties had agreed on the sum, “the theoretical maximum penalty is therefore either $1.1 million or $1.7 million per contravention” depending on the dates of contravention.

Justice Perram said because the parties could not agree on what contravened the section, it was difficult to “judge the appropriateness” of the $35m figure.

ASIC says the Federal Court of Australia today ordered Westpac Banking Corporation (Westpac) pay a pecuniary penalty of $3.3 million for contravening s12CC of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act) through its involvement in setting BBSW in 2010.

In reasons for making the pecuniary penalty order, Justice Beach noted the legislative constraint he had in imposing the order,

‘If I had been permitted to do so I would have imposed a penalty of at least one order of magnitude above $3.3 million in order to discharge [the objectives of specific and general deterrence]. But I am not free do so.‘

Justice Beach concluded in his reasons,

‘Westpac’s misconduct was serious and unacceptable…Westpac has not shown the contrition of the other banks. Moreover, imposing the maximum penalty is the only step available to me to achieve specific and general deterrence. The message that should be sent is that if you manipulate or attempt to manipulate key benchmark rates you are likely to have the maximum penalty imposed, whatever that is from time to time.‘

The Court also ordered that an independent expert agreed between ASIC and Westpac be appointed to review whether Westpac’s current systems, policies and procedures are appropriate, and to report back to ASIC within 9 months.

It was also ordered that Westpac pay ASIC’s costs of and incidental to the penalty hearing as agreed and assessed.

Today’s court orders follow Justice Beach’s judgment, delivered on 24 May 2018, which found that Westpac on 4 dates in 2010 traded with a dominant purpose of influencing yields of traded Prime Bank Bills and where BBSW set in a way that was favourable to its rate set exposure. His Honour held that this was unconscionable conduct in contravention of s12CC of the ASIC Act.

His Honour also found in his 24 May 2018 judgment that Westpac had inadequate procedures and training and contravened its financial services licensee obligations under s912A(1)(a), (c), (ca) and (f) of the Corporations Act 2001 (Cth).

ASIC Commissioner Cathie Armour welcomed today’s decision and noted that ‘ASIC brought this litigation to hold the major banks to account for their unacceptable conduct, and to test the scope of the law in combating benchmark manipulation. ASIC actions have led to these successful court outcomes, and also contributed to new benchmark manipulation offences being enacted by Parliament, and the calculation method and administration of the BBSW being radically overhauled.’

On 5 April 2016 ASIC commenced civil penalty proceedings in the Federal Court against Westpac, alleging in the period between 6 April 2010 and 6 June 2012 (inclusive) it traded in a manner that was unconscionable and created an artificial price and a false appearance with respect to the market for certain financial products that were priced or valued off BBSW.

This mirrored proceedings brought in the Federal Court against the Australia and New Zealand Banking Group (ANZ) on 4 March 2016 (refer: 16-060MR), against National Australia Bank (NAB) on 7 June 2016 (refer: 16-183MR) and Commonwealth Bank of Australia (CBA) on 30 January 2018 (refer:18-024MR).

On 10 November 2017, the Federal Court made declarations that each of ANZ and NAB had attempted to engage in unconscionable conduct in attempting to seek to change where the BBSW set on certain dates and that each bank failed to do all things necessary to ensure that they provided financial services honestly and fairly. The Federal Court imposed pecuniary penalties of $10 million on each bank.

On 20 November 2017, ASIC accepted enforceable undertakings from ANZ and NAB which provides for both banks to take certain steps and to pay $20 million to be applied to the benefit of the community, and that each will pay $20 million towards ASIC’s investigation and other costs (refer: 17-393MR).

On 21 June 2018, the Federal Court in Melbourne imposed pecuniary penalties totalling $5 million on CBA for attempting to engage in unconscionable conduct in relation to BBSW. CBA admitted to attempting to seek to change where BBSW set on five occasions in the period 31 January 2012 to 15 June 2012.

On 11 July 2018 ASIC accepted a court enforceable undertaking to address its BBSW conduct which provides for CBA will pay $15 million to be applied to the benefit of the community and $5 million towards ASIC’s investigation and legal costs (refer: 18-210MR).

In July 2015, ASIC published Report 440, which addresses the potential manipulation of financial benchmarks and related conduct issues.

The Government has recently introduced legislation to implement financial benchmark regulatory reform and ASIC has consulted on proposed financial benchmark rules.

On 21 May 2018, the new BBSW methodology commenced (refer: 18-144MR). The new BBSW methodology calculates the benchmark directly from market transactions during a longer rate-set window and involves a larger number of participants. This means that the benchmark is anchored to real transactions at traded prices.

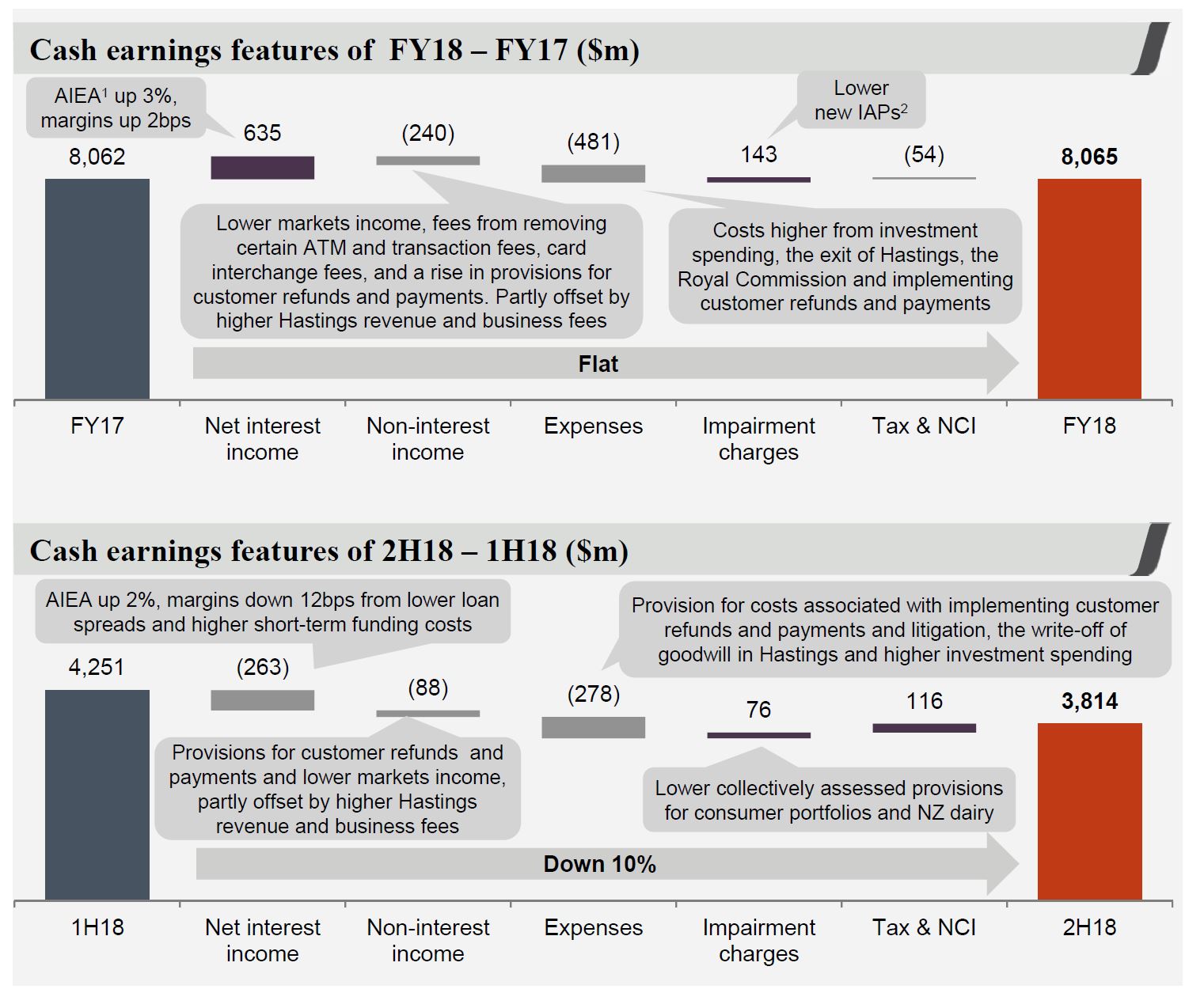

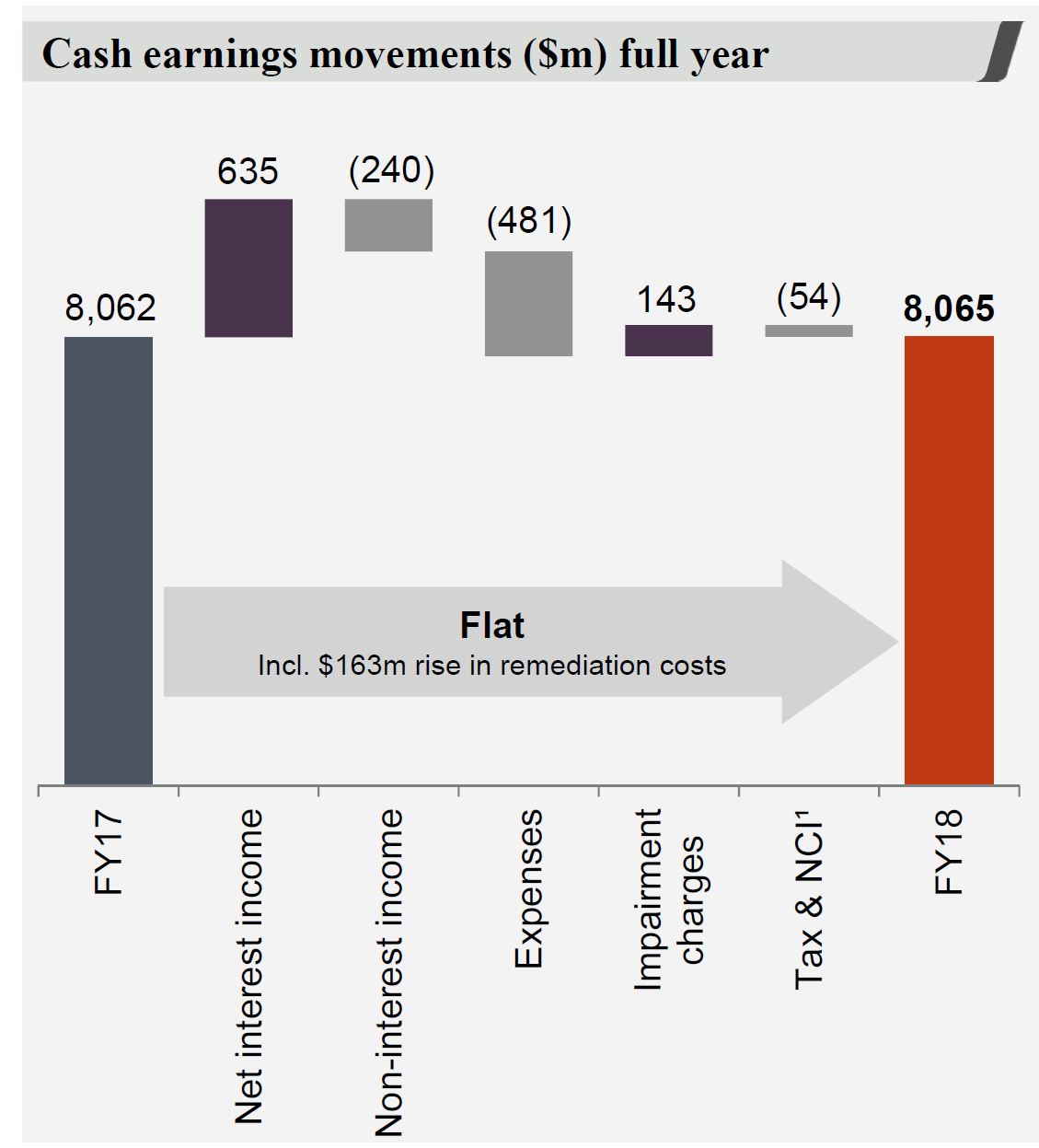

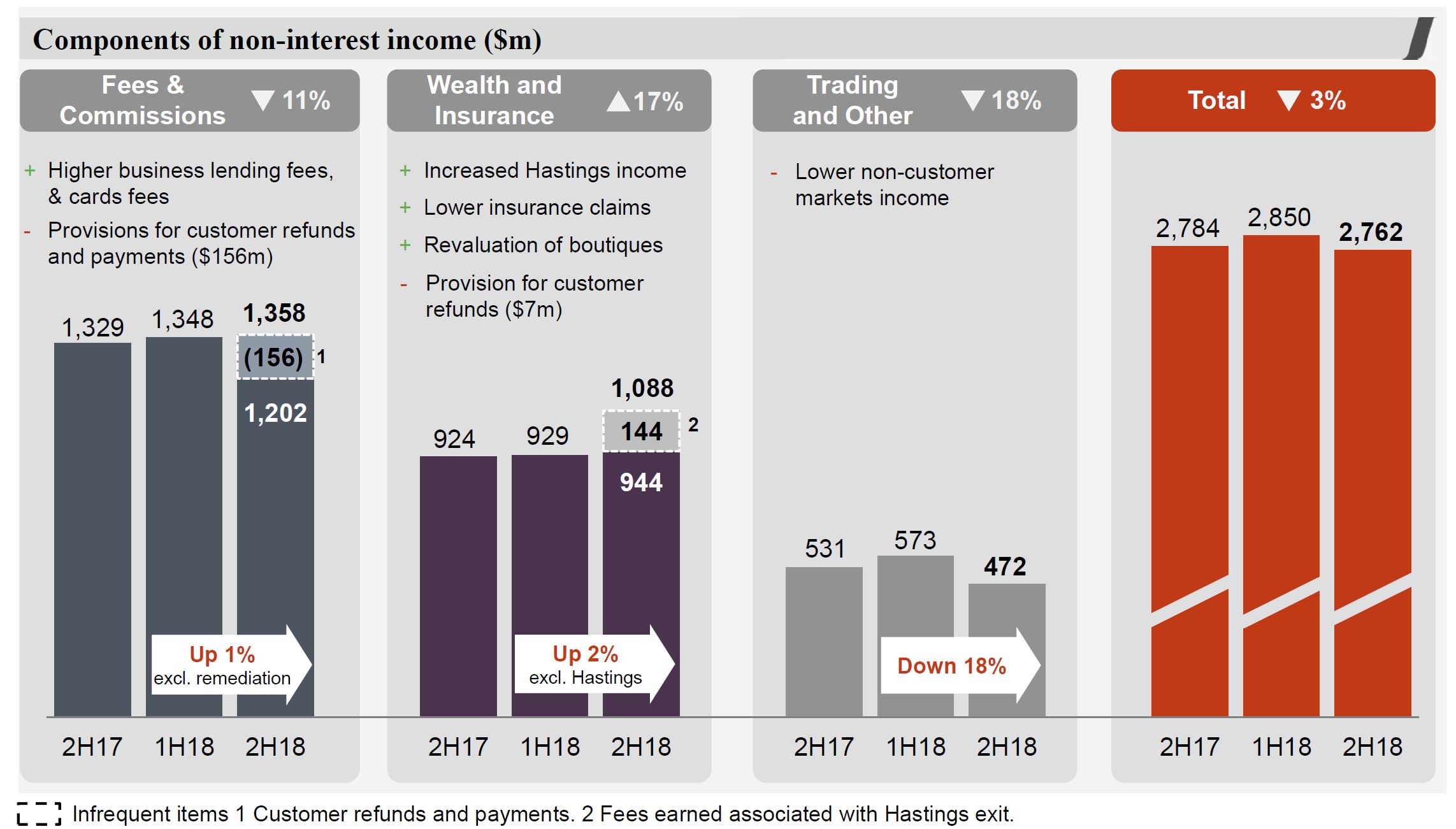

Westpac has released their 2018 full year results. They had already signalled customer remediation costs, and its impact on profitability, but their net interest margin was significantly lower in the second half, and 90+ mortgage delinquency continued to rise in Australia. Total provisions were lower. Capital ratio though are in good shape. The proportion of IO loans is falling, and they expect more home price easing.

CEO Harzter said ““We expect house prices to cool further, and investor demand to remain weak. On the other hand, demand from first home buyers is holding up. These dynamics are likely to lead to housing credit growth easing to 4% next year, with total credit growth of 3.5%. With around 70% of Australian customers ahead on their repayments and delinquencies low, credit risks in the housing market currently remain low”.

However, their disclosed stress tests suggest in a severe downturn cumulative total losses could be $3.9bn over three years.

Cash earnings were $8,065 million, little changed on last year. Cash earnings per share, 236.2 cents, down 1% and the cash return on equity (ROE) was 13.0%, at the lower end of the range Westpac is seeking to achieve. The final, fully franked dividend was unchanged, of 94 cents per share (cps), so the full year, fully franked dividend of 188 cps. Statutory net profit was $8,095 million, up 1%.

The cash earnings included $163 million in remediation charges, and a fall of $240 million in non-interest income, a a reduction in impairment charges.

There was a fall of $263 million in the second half in net interest income. and a 10% reduction in earnings, with remediation costs of $430 million.

Income was down 3% over the half, thanks to margin decline and customer remediation.

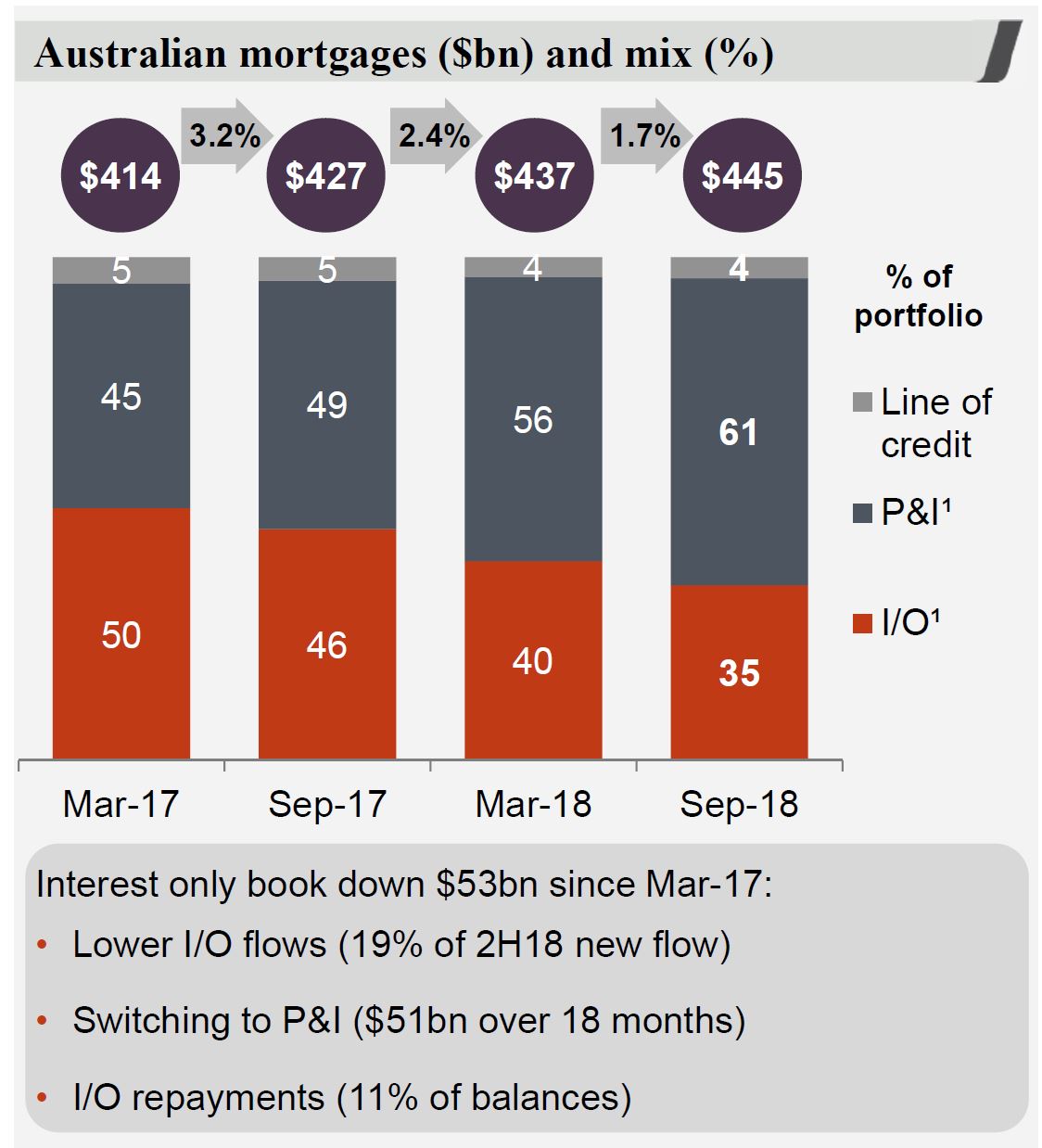

They highlight that Australian mortgage growth is moderating and interest only loans are down $53 billion since March 2017.

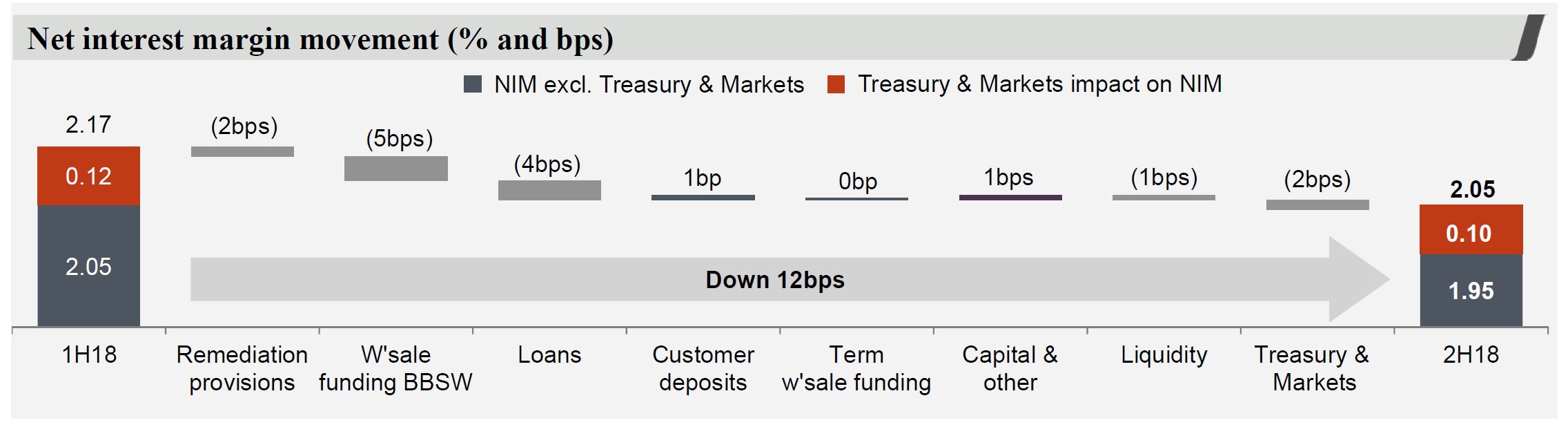

Margins in the second half were down from 2.05 to 1.95, or 10 basis points in the main banks, and from 0.12 to 0.10 in the Treasury and Markets. 5 basis points related to wholesale funding, and 4 basis points loans, offset by 1 basis point from deposits.

Non interest income fell and included provisions for customer refunds of $156 million and lower trading income, which was down 18% in the second half.

Expenses were higher thanks to regulation and compliance, remediation and platform investments.

FTE were down by around 700 from the first half.

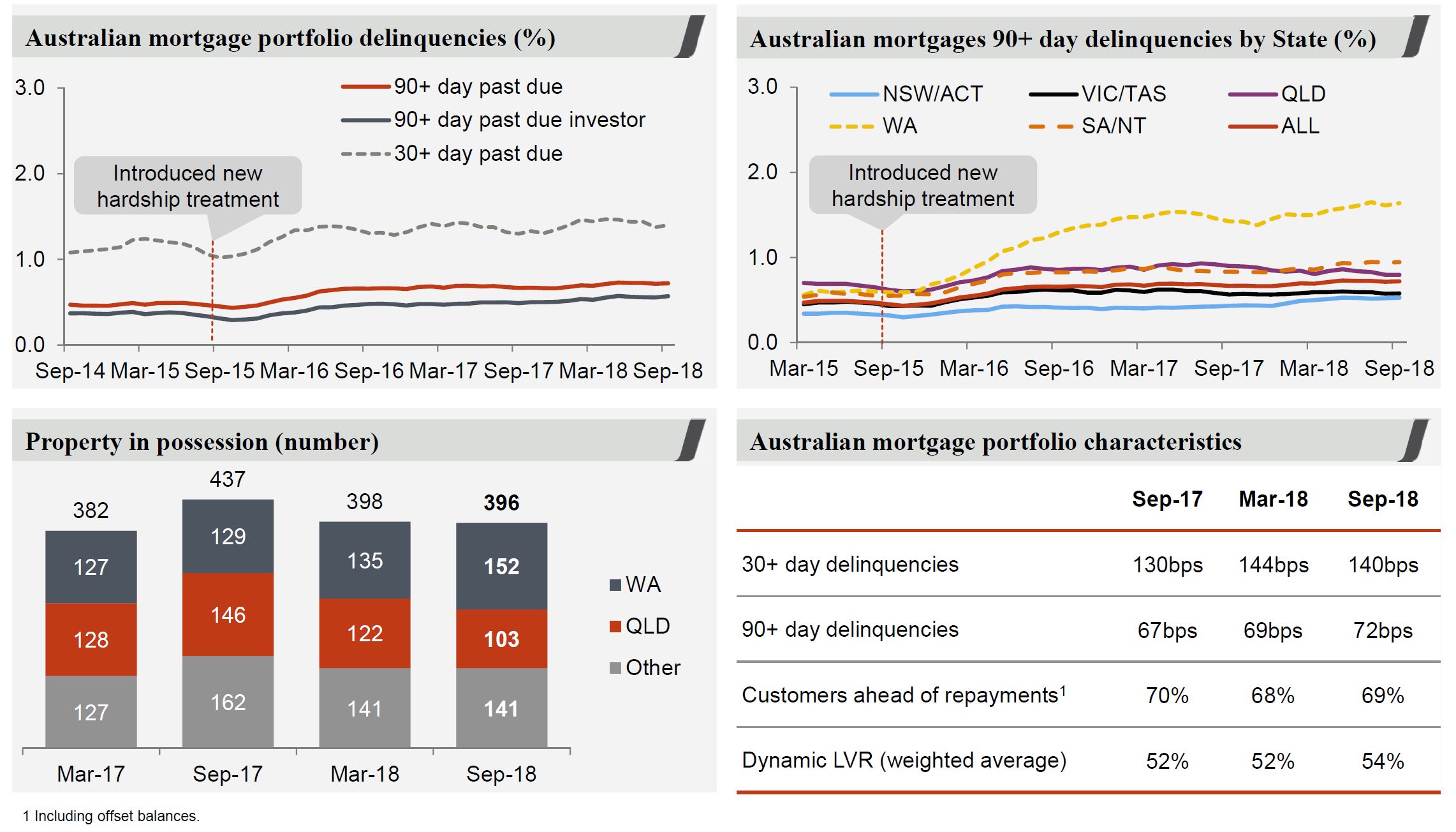

Stressed assets as proportion of total committed exposure (TCE) was lower, despite a rise in 90 days+ past due. Australian 90 day + mortgage delinquencies rose from 69 to 72 basis points in the second half.

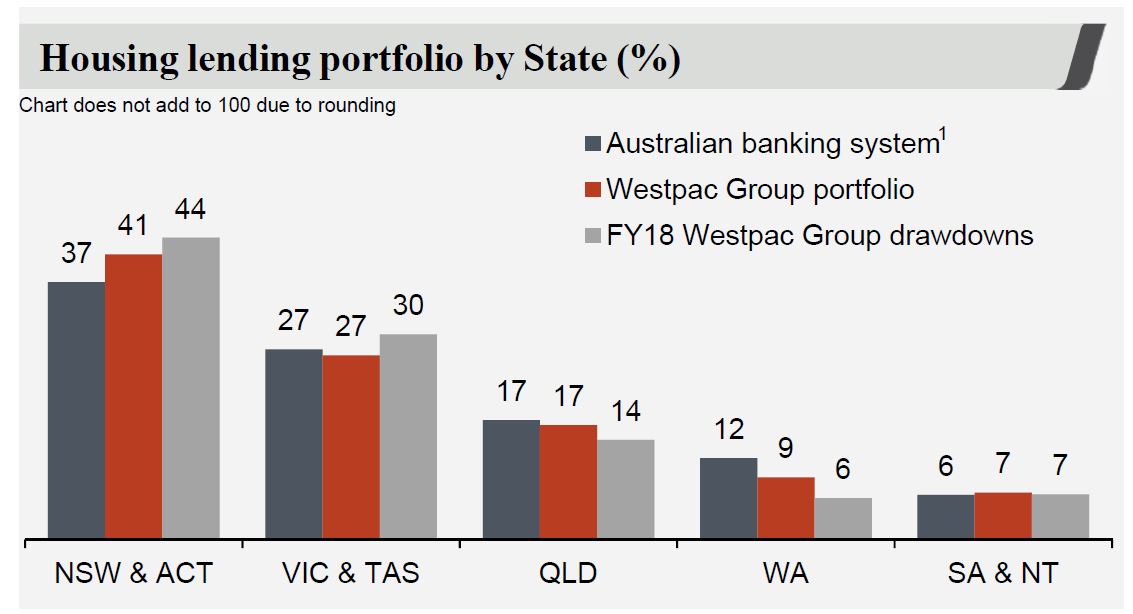

Westpac is writing more mortgage loans from NSW and VIC, relative to system and 51.6% of new flows came from propitiatory channels. 8.2% of new loans were from first time buyers. Borrowers applying for a mortgage must be able to service the higher of either: 7.25% minimum assessment rate; or product rate plus 2.25% buffer. Actual mortgage losses are 2 basis points.

The schedule of IO loan expiry reaches out over the next 10 years!

The Australian mortgage book shows a rise in delinquencies, a small fall in those paying ahead, and a rise in dynamic LVR (in response to falling prices). Dynamic LVR is the loan-to-value ratio taking into account the current loan balance, estimated changes in security value, offset account balances and other loan adjustments. WA and SA/NT are most exposed.

Westpac reported their mortgage stress tests which assumes a severe

recession in which significant reductions in consumer spending and business investment lead to six consecutive quarters of negative GDP growth. This results in a material increase in unemployment and nationwide falls in property and other asset prices. They say that estimated Australian housing portfolio losses under these stressed conditions are manageable and within the Group’s risk appetite and capital base.

Cumulative total losses of $3.9bn over three years for the uninsured portfolio (1H18: $3.5bn).

Cumulative claims on LMI, both WLMI and external insurers, of $911m over the three years (1H18: $911m).

Peak loss rate in year 2 has increased to 52bps (1H18: 48bps) due to recent

declines in house prices which leads to a higher dynamic LVR starting point for the portfolio. In addition, the unemployment rate for September of 5.0%

creates a bigger peak to trough change compared to 1H18.

WLMI separately conducts stress testing to test the sufficiency of its capital

position to cover mortgage claims arising from a stressed mortgage

environment.

Total impairments were down to $3,053 million (44% of impaired assets).

The CET1 ratio was 10.63%, up 13 basis points from March 2018.

Westpac Group has announced that it will introduce new changes to the way brokers are remunerated as part of a move to “enhance transparency and customer outcomes”, via The Adviser.

Effective 1 January 2019, Westpac and its subsidiaries, St.George, Bank of Melbourne, and BankSA, will link upfront commission payments for standard home loans to net debt utilisation and inclusive of loan offset arrangements, rather than the approved loan limit.

The group noted that the amount of upfront commission paid for most home loans will now be calculated as a percentage of the amount drawn down and used by the customer at settlement, excluding any amount which remains in an offset account.

Westpac general manager, home ownership, Will Ranken, said: “We know many of our customers value the independent service and advice mortgage brokers provide.

“Westpac Group continues to be an active participant in the Combined Industry Forum and supportive of its work to ensure better customer outcomes.

“We believe the changes we are introducing will be the start of delivering a more transparent commission model that better meets the needs of consumers and industry.

“We remain committed to supporting mortgage brokers to ensure we are providing the right home loan solutions for our customers.”

Westpac also stated that the new commission structure for standard home loans will also allow for a subsequent upfront commission for when brokers arrange loans for customers with funds held in offset accounts for a short term future purpose like renovations.

The bank said that the changes will mean if a customer takes out a $400,000 home loan and purchases a property for $350,000 and puts $50,000 of that loan into an offset account, the broker will be paid an upfront commission based on the $350,000 amount. Westpac added that if the customer then draws down the $50,000 in the offset account in the twelve months following settlement, the broker will receive a subsequent upfront commission calculated on the $50,000.

In addition, Westpac Group noted that it will implement improvements to increase the transparency of customer disclosure of the commissions mortgage brokers receive, including providing details of how the commission paid to mortgage brokers will be calculated.

According to Westpac, the new changes will also provide brokers with access to priority service arrangements for their clients if they “consistently meet quality loan application measures”.

The group added that there will be no requirement for brokers to meet any dollar volume business threshold to access these new arrangements.

Westpac Group said that the measures are part of its commitment to implement reforms recommended by the Combined Industry Forum (CIF) to “ensure better consumer outcomes”, which it said includes preserving and promoting competition and consumer choice, and improving standards of conduct and culture in mortgage broking.

Westpac also stated that The changes to commission calculations do not apply to Construction Loans, Equity Access Loans or Portfolio Loans as the commissions for these products remain unchanged in-line with the Combined Industry Forum recommendations, and said that changes to the commission model and service model will take effect by 1 January 2019.

Changes to make commission payments more transparent to Westpac Group customers will start being made in February 2019.

Westpac’s move follows similar broker remuneration changes announced by NAB in September.

Westpac CEO Brian Hartzer faced the firing line of a parliamentary committee where he was asked to explain why branch staff are still required to meet sales targets; via InvestorDaily.

Most of the questions directed at Brian Hartzer by the House of Representatives standing committee on Thursday were about the royal commission.

Labor MP Matt Thistlewaite read from the witness statement of Carol Separovich, Westpac’s head of performance & rewards, who appeared before the Hayne inquiry in May.

“She said there is still a variable reward and an opportunity for employees to gain financial advantage from elements that are at risk and related to certain targets,” Mr Thistlewaite said. “What proportion of frontline staff salary is at risk?”

Mr Hartzer confirmed that for Westpac personal bankers it’s about 10 to 15 per cent.

“If you’ve got someone who is in a very focused sales role like a home finance manager, it’s probably around 20 per cent,” he added.

Mr Thistlewaite moved on to Westpac’s key performance indicators (KPIs), as outlined in Ms Separovich’s witness statement.

“For personal bankers, this includes things like total branch first-party net home loan and deposits growth, total net growth percentage of branch customers, referrals to specialist business partners such as wealth business premiums,” he said “Those referral opportunities and growth KPIs are still there.”

“In terms of credit card products, one KPI is cards systems growth. It appears to me that you’ve done a bit of window dressing but there is still that notion within branches, within banks that an element of your job is to push these products onto customers and if you do it and do it well you’ll be rewarded for it.”

Mr Hartzer rejected this characterisation of the bank.

“I certainly wouldn’t characterise it as window dressing. We are a commercial organisation. We want to grow. The strategy here is around encouraging people to consolidate their business with us.

“We are trying to get that balance of rewarding people who do a great job and look after customers and allow them to benefit from that success. But at the same time not create perverse incentives that cause them to push a product onto someone who doesn’t need it. We have changed the structures so that people are agnostic about the products they are talking to customers about.”

Commissioner Hayne’s interim report, released last month, questioned the role of incentive remuneration and bonus cultures within financial services: “If customer facing staff should not be paid incentives, why should their managers, or those who manage the managers? Why will altering the remuneration of front-line staff effect a change in culture if more senior employees are rewarded for sales or revenue and profit?

The chief executives of ANZ and NAB will appear before the inquiry on Friday, 12 October and Friday, 19 October, respectively.