Australian businesses have never had it better, according to the latest National Australia Business (NAB) survey released today.

The survey’s conditions index — a composite indicator that measures trading activity, profitability and employment — surged by a massive 7 points to +21, leaving it at the highest level since the survey began in 1997.

On this measure, Australian businesses have not had it this good in at least two decades.

As the chart below shows, there were enormous increases recorded in trading and profitability, suggesting that demand was rampant during October.

Source: NAB

But are business conditions as strong as the NAB survey suggests?

While no one doubts that things have improved over the past year — strong growth in employment, for one, suggests they have — but the strength in the NAB survey is significantly greater than in other alternate business indicators such as the Ai Group’s measures on manufacturing, services and construction activity levels.

Like the NAB survey, they too have been around for years, and they paint a very different picture on the current momentum in the business sector.

In October, respondents in those surveys reported that activity levels improved at a slower pace than September, and well below the levels seen just a few months ago.

Services fell to 51.4, manufacturing to 51.1 and construction to 53.2, remembering that a reading over 50 indicates that perceived activity levels improved from one month earlier.

So activity levels improved according to those surveys, but at a marginal pace.

While they are constructed differently, they both look at perceived business conditions in Australia.

And while the Ai Group respondents did report an improvement in activity levels, one has to ask whether that would lead to the boom in profitability and trading conditions reported by respondents in the NAB survey?

Given the divergence, caution is understandably warranted.

That’s something that Alan Oster, Chief Economist at the NAB, stressed following the release of October report, noting that a sharp improvement in manufacturing conditions contributed to the outsized move.

“This is an extremely strong result and of itself would suggest a better than expected performance for the economy,” he said.

“However, it is unclear just how long conditions can remain at these record levels given that the result was driven by a surprise jump in manufacturing.”

Adding to the need for caution, Oster said the surveys lead indicators also softened over the month, which, along with an unchanged reading on business confidence, raised questions as to whether the bounce in the conditions index can be sustained.

“Some of the leading indicators such as forward orders — which have been giving a more accurate read on the strength of the economy — have actually softened a little in recent months,” he said.

“Less upbeat readings on business confidence may also be telling, with firms previously indicating that uncertainty around the outlook for their business is holding confidence back.”

Given softer internals in the NAB report, along with the slowdown in other business indicators, it will be interesting to see whether the NAB’s conditions index will retrace its October surge next month.

Things are undoubtedly looking better for Australian business, but it’s probably best to keep the champagne on ice, says Tom Kennedy, Economist at JP Morgan.

“Although firms’ operating conditions have obviously improved, the sectoral momentum in the survey [from] manufacturing and mining makes us think that the magnitude of the improvement is overdone and the implications for economic growth and monetary policy need to be faded,” he says.

George Tharenou, Economist at UBS, agrees with Kennedy’s assessment.

“The conditions [index] is now giving an incredibly bullish signal on the economy with a spike to a record high,” he says.

“However, it has been average or above for most of the last three years and has just not translated through to the hard data like GDP, CPI or wages.”

Tag: NAB

600 Technology Specialists to Join NAB

As part of its recently released updated strategy, NAB will immediately hire 600 technology specialists in the areas of software engineering, data, architecture and security.

The national and global recruitment drive is part of NAB’s plan to reshape the workforce and create up to 2,000 new jobs by 2020 to meet the changing needs of customers.

Chief Technology and Operations Officer Patrick Wright said NAB is looking for the best talent in Australia and the world to come and join its technology and digital teams.

“We want the top talent in the industry to come and join us, as we change dramatically to become the very best bank we can be and give our customers the products and services they demand and deserve,” Mr Wright said.

“We know this is an ambitious target and acknowledge the war for talent is intense, but these are the essential skills and roles we need in order to deliver our plan.“This builds on three years of innovation at NAB, including the establishment of our innovation incubator, NAB Labs, and our innovation fund, NAB Ventures, the launch of Quickbiz which provides our business customers with lending decisions in seconds, and the continued roll-out of Customer Journeys, which is dramatically changing how we deliver improved products and services to our customers.”

The move also aims to rebalance the shift from outsourced suppliers based in Australia and overseas, to bring talent back inside the bank in NAB’s Australian offices to increase competitive advantage.

“We’re looking at the skills needed inside and outside our business to make sure that we can run our systems and service our customers as best as possible,” Mr Wright said.

NAB recently announced a record $4.5 billion investment into the bank over the next three years – with much of that funding directed to technology and digital priorities.

“This significant investment will help change the way we provision technology services, which is critical to delivering more effectively to balance innovation with resilience, and speed with security.

“Our people are integral to the success of NAB, and this investment ensures they are enabled and backed to deliver their very best.

“We understand what the fintechs across the world are doing, and we think we can do better, but we need to move now, invest in the right systems and people, and change dramatically,” Mr Wright said.

To kick start the recruitment drive, NAB has announced the appointment of leading global technology talent of two new roles; Executive General Manager Business Enabling Technology, Yuri Misnik and Executive General Manager leading our Program Management Office Kyle McNamara. The roles will report to Mr Wright.

Mr Misnik will have responsibility for all NAB’s business-facing technology teams including Digital technology and Corporate functions.

Mr McNamara will be focused on NAB’s change activities across the franchise and delivery of the significant investment slate announced last week.

The Robots Are Coming to a Bank Near You

The NAB results yesterday included one of the clearest signals yet of the digital disruption which is hitting the finance sector (and other customer facing businesses too).

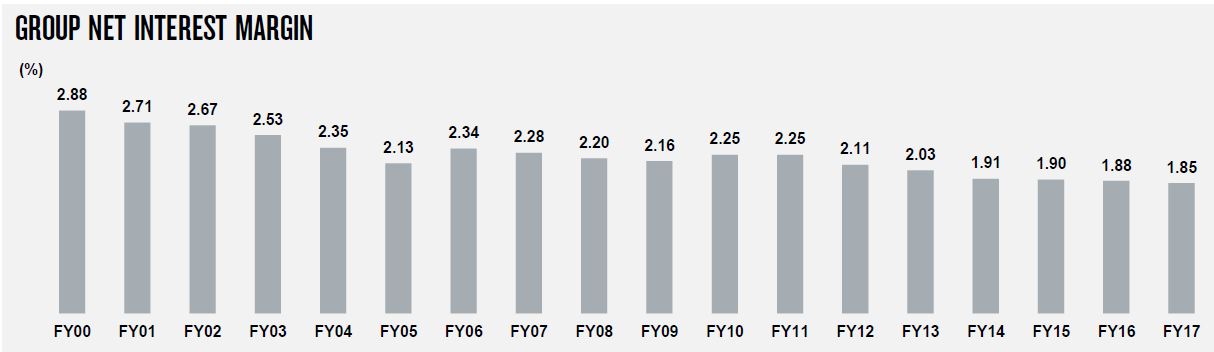

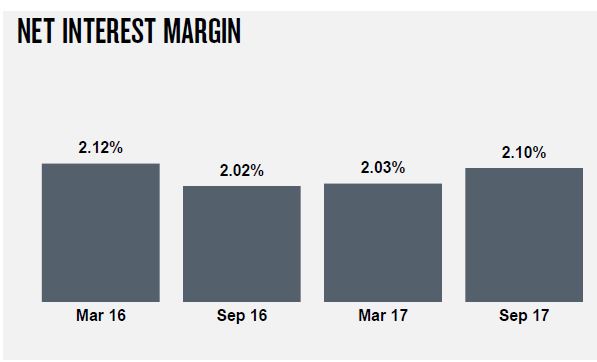

Worth also reflecting on the fact that since the turn of the century NAB’s net interest margins have fallen 100 basis points, to below 2% today. They have to find a different economic model for the business. Just pulling back to Australia and New Zealand and flogging more mortgages will not solve their problem. The biggest expense by far is the people they employ.

Worth also reflecting on the fact that since the turn of the century NAB’s net interest margins have fallen 100 basis points, to below 2% today. They have to find a different economic model for the business. Just pulling back to Australia and New Zealand and flogging more mortgages will not solve their problem. The biggest expense by far is the people they employ.

They will shed 6,000 banking jobs and replace them with 2,000 people holding digital skills, from analytics through to software engineers. The future of banking is indeed digital.

This is because banking is a very “bittable” business, and just like newspapers do not need to sell physical documents to distribute news, banks do not need branches, or people on the customer service or sales lines. If they get the digital design right.

In fact, when we completed our last “Quiet Revolution Survey” which looked at customers and their banking channel preferences, we concluded:

The Quiet Revolution highlights that existing players need to be thinking about how they will deploy appropriate services through digital channels, as their customers are rapidly migrating there. We see this migration to digital more advanced amongst higher income households but momentum continues to spread. So players which are slow to catch the wave will be left with potentially less valuable customers longer term. Players need to adapt more quickly to the digital world. We are way past an omni-channel (let them choose a channel) strategy. We need to adopt a “mobile-first” strategy. Such digital migration needs to become central strategy because the winners will be those with the technical capability, customer sense and flexibility to reinvent banking in the digital age. The bank branch has limited life expectancy. Banks should be planning accordingly.

Many households and small businesses were critical of the slow pace at which banks were moving to service digital, and the lack of innovation available via mobile banking applications. And not just younger “digital migrants”.

So the task in hand for NAB and other other industry players, is to manage down the traditional branch and ATM infrastructure, while building compelling digital alternatives, whether it be payments, core banking or wealth management. And keep the business afloat during the transition. Think changing the propellers on an airplane for jet engines while in flight!

It is quite feasible to use robo-banking technologies to replace mortgage brokers, and financial advisers. It is completely possible to apply for a mortgage end-to-end on line, and deliver a quicker and more compelling customer fulfillment experience. Electronic payments can now replace cash. The mobile device will contain an electronic wallet and payment capability and rewards programmes and much more. Physical plastic credit cards are a thing of the past. Every electronic transaction produces data which is now the new life-blood of banking. Use that data to guide customers to new solutions.

The barriers to change have been the culture (especially in the middle management ranks) within banking organisations, so defaulting to a “let the customer choose” channel approach. But this was always a cop-out. Plus the complexity of the ancient “back-end systems” many of which are tens of years old, have to be tackled or replaced (as the CBA has done).

But now, banks have to be re-engineered and migrated to digital, harnessing the power of algorithms, robotics and user experience experts. A whole new world. We may need banking services, but do we need a bank?

Then there will be consequences for society. First, banks of the future will have many fewer staff, and those who remain will need different skills. Almost none will be customer facing. Just as robots replaced workers on the assembly line, robots are now becoming bankers.

Second, the minority of customers who a Digital Luddites will need to be handled appropriately. The current branch infrastructure is just too expensive. How will banks meet their implicit service obligation? Or will they try to trade it away, as they did with the ATM network?

But third, and this is the rub. What we are discussing here is also happening across other industries, and as the digital revolution gains pace, the risk is that more people find themselves without employment.

This is the worry-some aspect of digital transformation. Digital efficiency will mean fewer jobs. What happens to those without?

We are just 10% along the digital journey. It is unstoppable, and business models, careers and whole chunks of the banking system will be shaken to pieces. Just ask the Fintechs! But the social implications should certainly be considered too.

NAB FY17 Result Cash Earnings $6,642 million

National Australia Bank reported its FY17 results today. Cash earnings were up 2.5% to $6,642 million, which was below expectation, and the statutory profit was $5,285m. The cash return on equity was 14%, down 30 basis points on last year. CET1 Capital was 10.1%, up 29 basis points.

NAB now has its main footprint in Australia, (and New Zealand). NIM improved, although the long term trend is down. Wealth performance was soft, and expenses were higher than expected, but lending, both mortgages and to businesses, supported the results. They made a provision for potential risks in the retail and the mortgage portfolio, with a BDD charge of 15 basis points but new at risk assets were down significantly this last half.

Ahead, they flagged considerable investment in driving digital, and major cost savings later into FY20.

Of the $565.1 billion in loans, 58% of the business is mortgages, 40% business loans and 2% personal loans. 84% of gross loans are in Australia, and 13% in New Zealand. 10.9% of gross loans, or $61.9bn are commercial real estate loans, mainly in Australia.

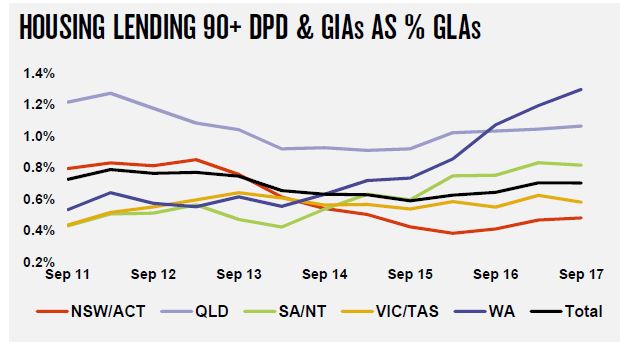

So, the key risk, or opportunity, depending on your point of view, is the property sector. Currently portfolio losses are low at 2 basis points but WA past 90-day mortgages were up. If property prices start to fall away seriously, new mortgage flows taper down, or households get into more difficulty (especially if rates rise), NAB will find it hard to sustain its current levels of business performance.

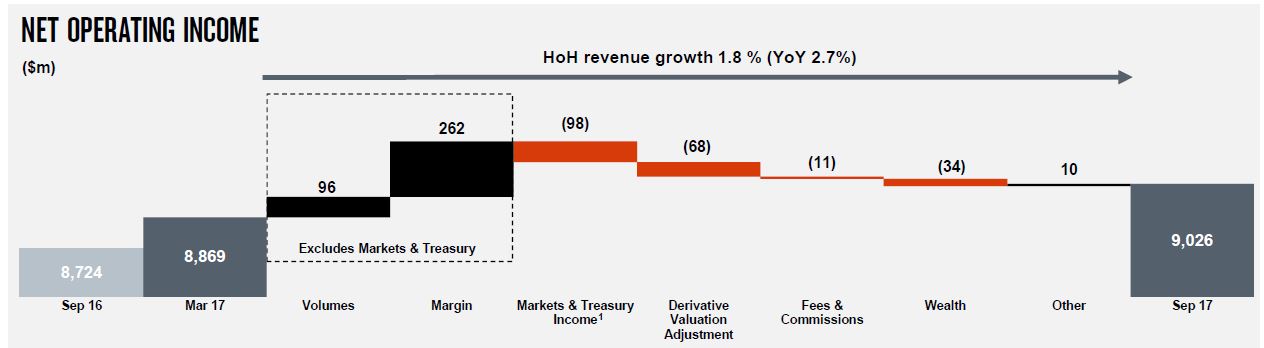

Looking in more detail, Group Net operating income was 2.7% higher YOY and 1.8% higher in the second half.

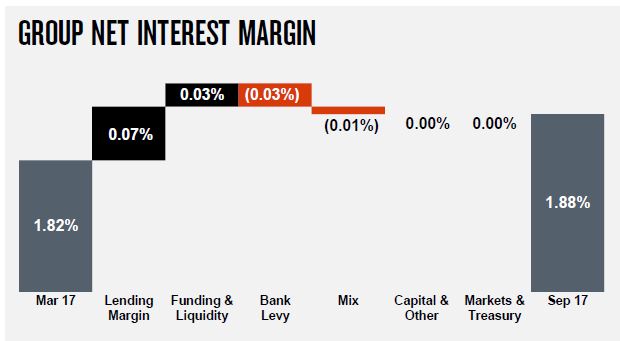

Group net interest margin was 1.88%, up from 1.82% in 1H. They improved their lending margin by 7 basis points. The bank levy cost 3 basis points.

Group net interest margin was 1.88%, up from 1.82% in 1H. They improved their lending margin by 7 basis points. The bank levy cost 3 basis points.

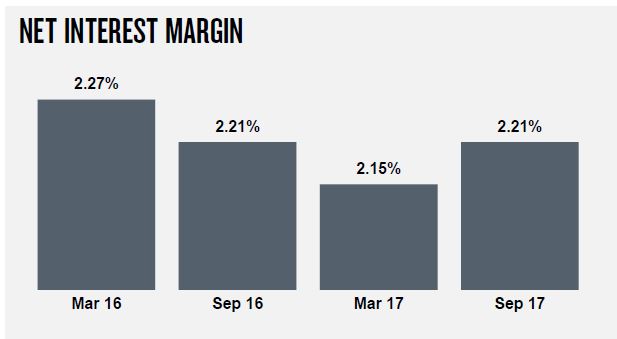

But long term NIM trends are lower.

But long term NIM trends are lower.

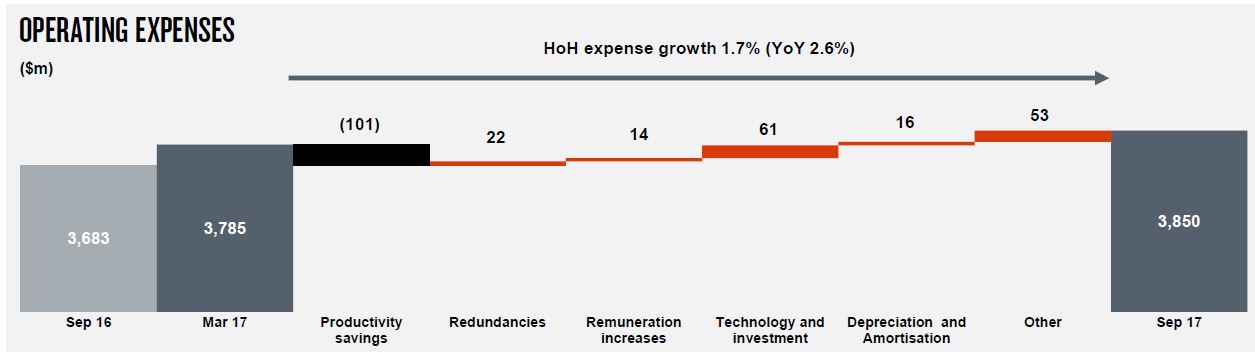

Operating expenses rose 2.6% YOY

Operating expenses rose 2.6% YOY

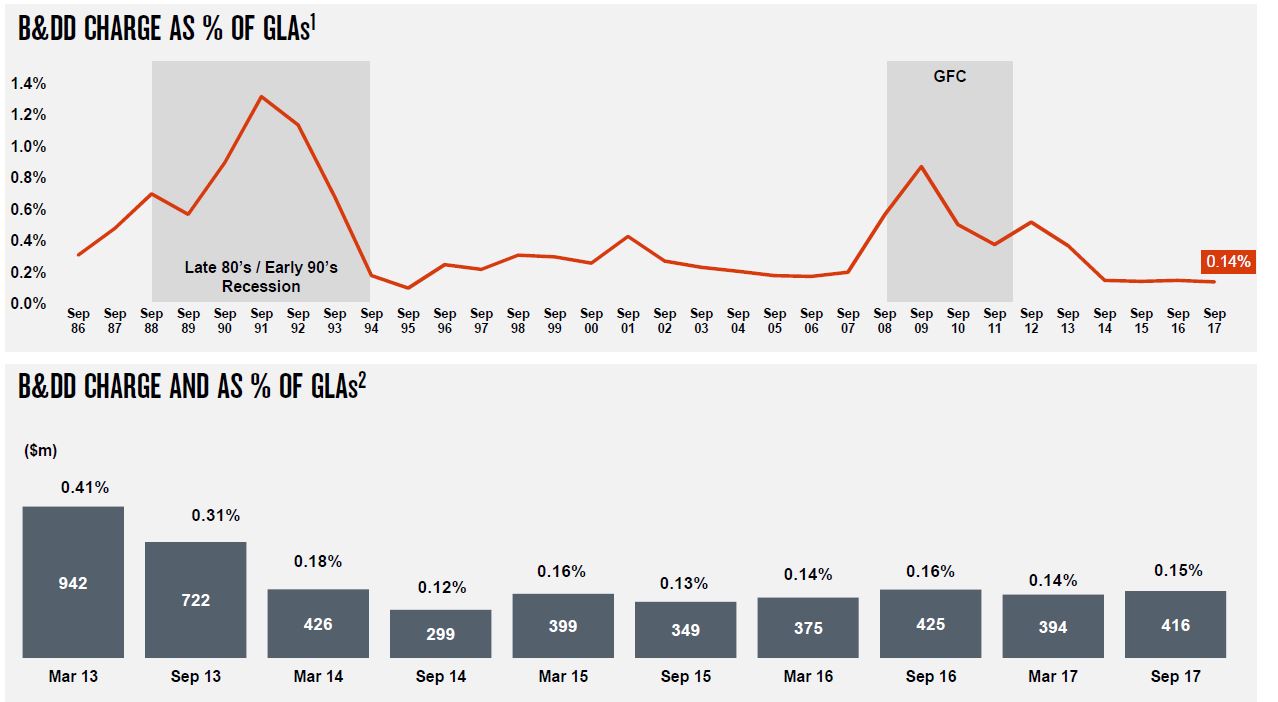

B&DD Charges rose to $416m, and was 0.15% of GLAs.

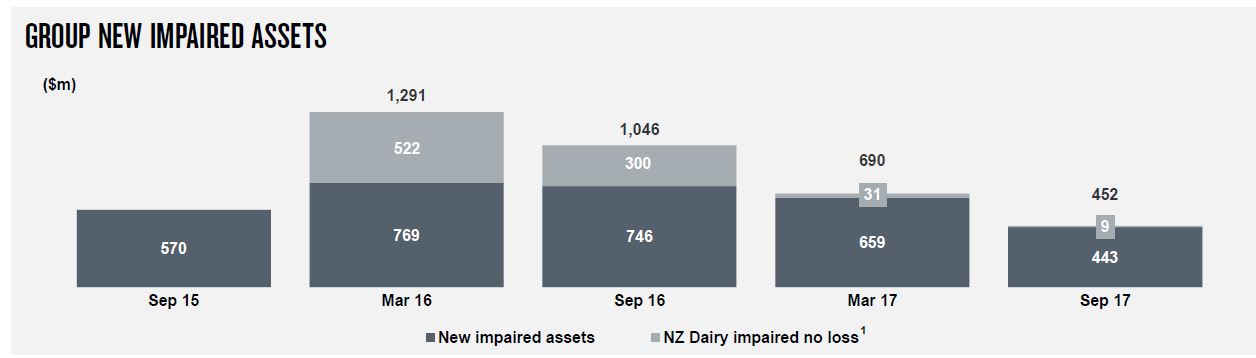

New impairments were $452m Sep 17, down from $690m in Mar 17.

New impairments were $452m Sep 17, down from $690m in Mar 17.

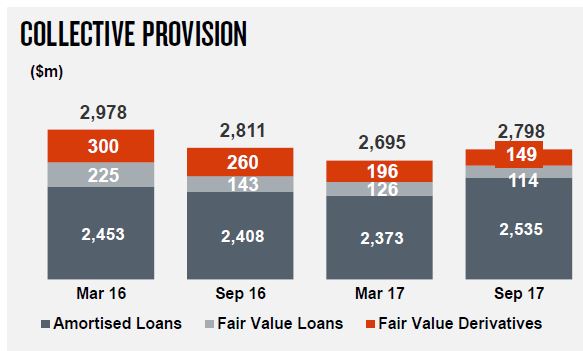

The collective provisions were up, $2,798m in Sep 17.

The collective provisions were up, $2,798m in Sep 17.

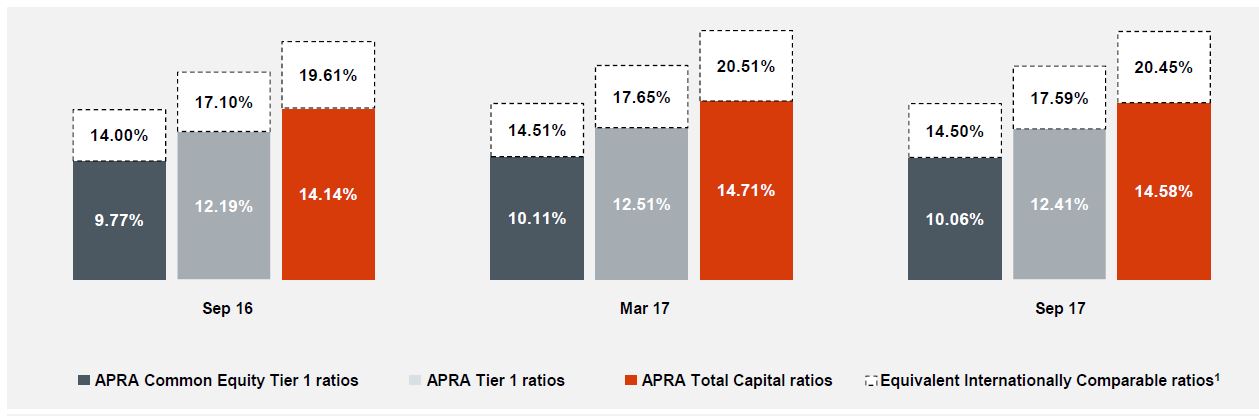

NAB CET1 ratio is 10.1% under APRA, but 14.5% under their claimed Internationally Comparable CET1 ratio. It was hit by the move to higher mortgage risk weights in 2H. This added around 17 basis points.

NAB CET1 ratio is 10.1% under APRA, but 14.5% under their claimed Internationally Comparable CET1 ratio. It was hit by the move to higher mortgage risk weights in 2H. This added around 17 basis points.

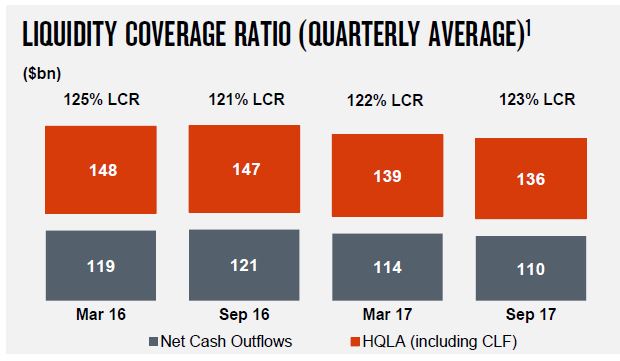

51% of funding is from stable customer deposits. The Liquidity Coverage Ratio was 123%.

51% of funding is from stable customer deposits. The Liquidity Coverage Ratio was 123%.

The net stable funding ratio was 108% at Sep 17.

The net stable funding ratio was 108% at Sep 17.

Looking in more detail at the segments:

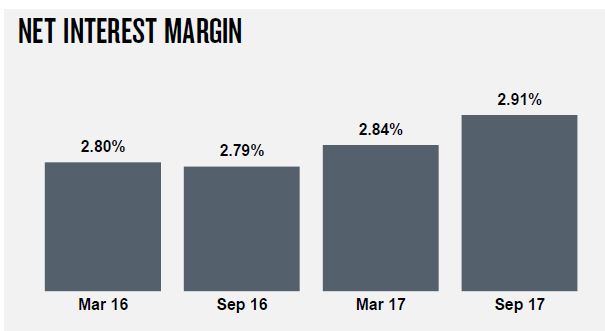

The net interest margins for Consumer Banking and Wealth is 2.10%.

NIM for Business and Private Banking was higher.

NIM for Business and Private Banking was higher.

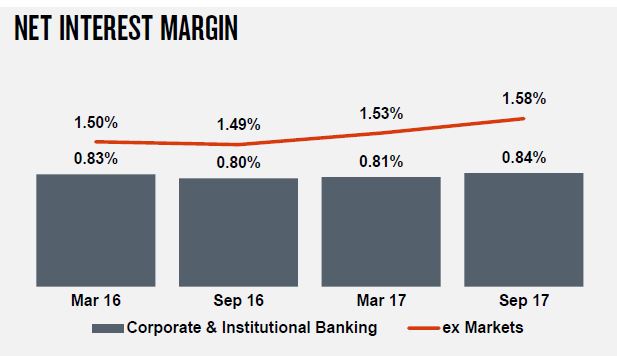

Corporate and Institutional Banking NIM also improved.

Corporate and Institutional Banking NIM also improved.

NIM in the NZ business was also higher in 2H17.

NIM in the NZ business was also higher in 2H17.

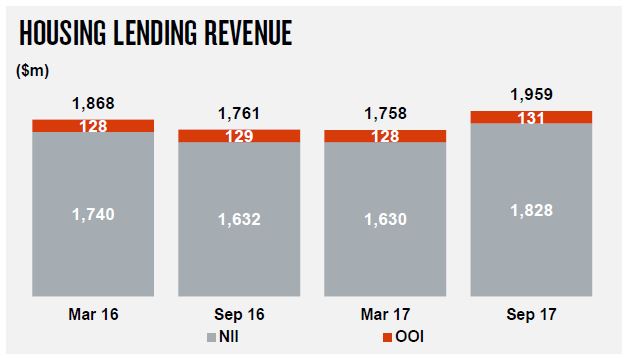

Turning to the critical Australian Mortgage portfolio we see that housing revenue grew..

Turning to the critical Australian Mortgage portfolio we see that housing revenue grew..

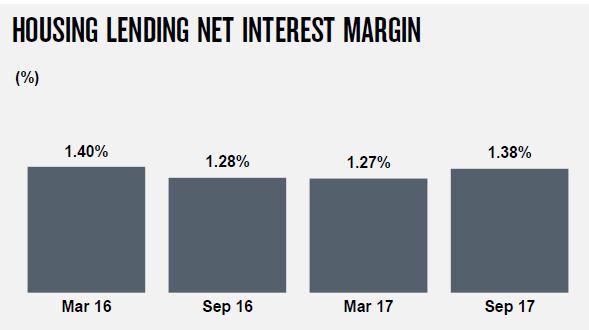

.. and NIM improved in 2H17.

.. and NIM improved in 2H17.

They highlight prudent customer behaviour – on average customers are 30 monthly payments in advance; 73% of all customers are at least 1 month in advance but this includes offset accounts.

They highlight prudent customer behaviour – on average customers are 30 monthly payments in advance; 73% of all customers are at least 1 month in advance but this includes offset accounts.

They said the average LVR at origination was 69% and the dynamic LVR is 43%

NAB uses interest rate buffers and applies a floor rate (7.25%) or buffer (2.25%) to new and existing debt, plus granular expense evaluation across 12 customer expense criteria using the greater of customer expense capture or scaled Household Expenditure Measures.

The strongest growth came from their Broker and Advantedge channels, with 4,637 brokers under NAB owned aggregators. 42% of draw-downs were attributed to brokers in Sep 17. One third of the portfolio is broker originated.

The strongest growth came from their Broker and Advantedge channels, with 4,637 brokers under NAB owned aggregators. 42% of draw-downs were attributed to brokers in Sep 17. One third of the portfolio is broker originated.

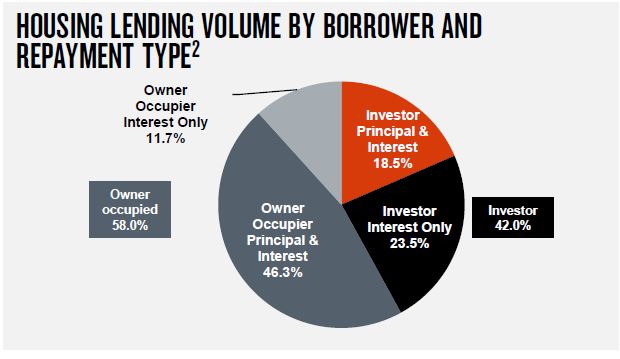

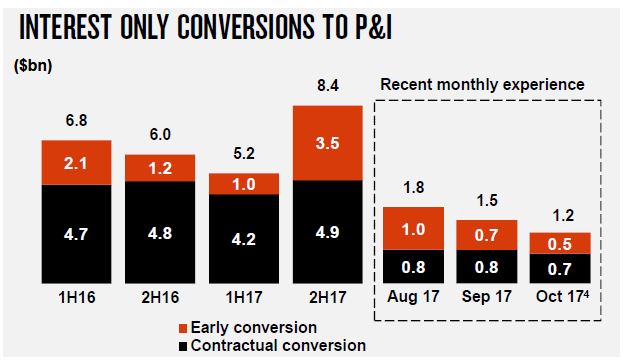

They reported some switching from interest only loans to principal and interest loans, including contractual conversion.

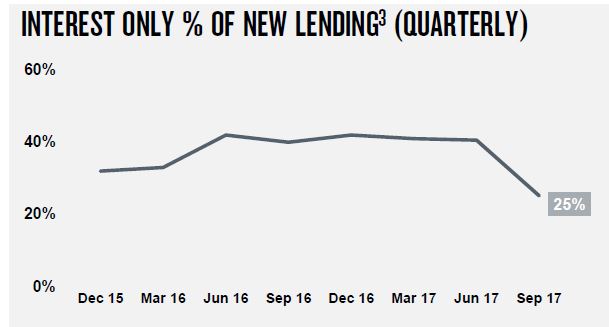

The proportion of new interest only lending is falling. The 30% Interest Only flow cap includes all new IO loans and net limit increases on existing IO loans. The cap excludes line of credit and internal refinances unless the internal refinance results in an increased credit limit (only the increase is included in the cap).

The proportion of new interest only lending is falling. The 30% Interest Only flow cap includes all new IO loans and net limit increases on existing IO loans. The cap excludes line of credit and internal refinances unless the internal refinance results in an increased credit limit (only the increase is included in the cap).

90-Day past due date are sitting at ~0.6%, but WA is 1.2% (similar to other lenders, WA is were higher risks reside at the moment). QLD is around 1.0%. 9% of loans are in WA, 17% in QLD. Current loss rates are 2 basis points (12 month rolling Net Write-offs / Spot Drawn Balances).

90-Day past due date are sitting at ~0.6%, but WA is 1.2% (similar to other lenders, WA is were higher risks reside at the moment). QLD is around 1.0%. 9% of loans are in WA, 17% in QLD. Current loss rates are 2 basis points (12 month rolling Net Write-offs / Spot Drawn Balances).

Looking ahead, the bank is targetting more than $1bn in cost savings by FY20 by driving simplification and automation, with a flatter organisational structure, and savings from procurement and third party costs. However, FY18 expenses are expected to increase by 5-8% due to higher investment spend, then targeting broadly flat expenses to FY20.

Looking ahead, the bank is targetting more than $1bn in cost savings by FY20 by driving simplification and automation, with a flatter organisational structure, and savings from procurement and third party costs. However, FY18 expenses are expected to increase by 5-8% due to higher investment spend, then targeting broadly flat expenses to FY20.

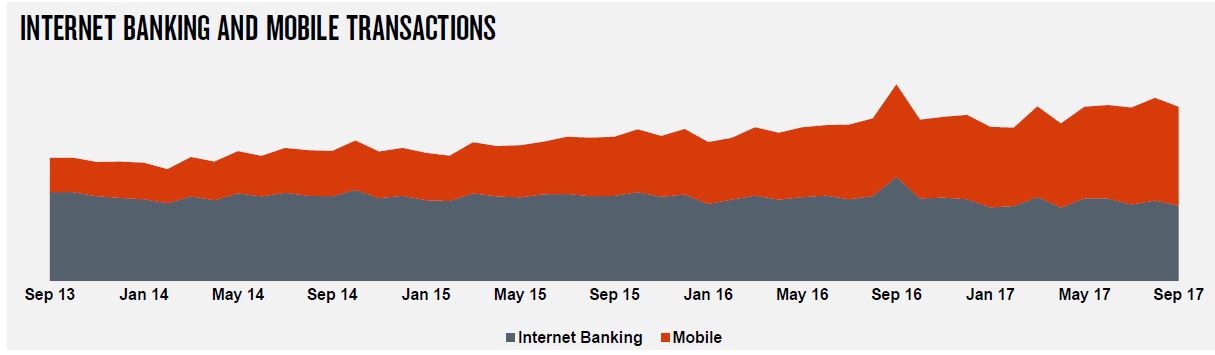

They highlight the transition to mobile, with more transactions now via mobile than internet banking.

Further investments will be made here. 6,000 jobs will go in the next 3 years, while 2,000 new digital jobs will be created.

Further investments will be made here. 6,000 jobs will go in the next 3 years, while 2,000 new digital jobs will be created.

The Next Round In The Payments Wars

The Commonwealth Bank, Westpac, and National Australia Bank are working together to build the next generation of mobile payments and wallets in Australia. These banks are not offering the Apple Pay solution, unlike ANZ. They sought unsuccessfully to negotiate collectively with Apple in order to gain access to the iPhone’s near-field communications (NFC) chip which would allow their own apps to make contactless payments.

The first initiative of the new joint venture will be the development of a payment app that will enable instant payments for all Australians, including small businesses, regardless of who they bank with.

Beem will be a simple and convenient free app enabling anyone to make an instant payment using their smartphone, and request payment from someone who owes them money or to split a bill. The hope is that it will become an industry-wide payment solution, and is open to interest from other banks, industry, and retail players.

Beem will work on both iOS and Android smartphones, and will be compatible across devices and different banks – users won’t need to be customers of CBA or Westpac or NAB.

Commonwealth Bank Group Executive of Retail Banking Services, Matt Comyn, said Beem will give Australians a simpler way to pay and request payments, a pain point for both consumers and small businesses.

“Two thirds of small businesses say they are owed money for completed work, with around $7,300 owed to small traders. Beem will give small businesses a cost effective and easy way to collect payments instantly and on the go for their goods and services, without having to take the larger leap into using merchant credit facilities, or issuing invoices to be paid later,” Mr Comyn said.

Beem will benefit from bank level security and encrypted user account information. Every transaction will be authenticated and subject to real-time fraud monitoring.

Westpac Chief Executive, Consumer Bank, George Frazis, said Beem expands payment choices for customers, and is the latest offering in Australia’s long history of innovative payment solutions, including EFTPOS, Pin@POS, chip, tap and pay, and wearable payment devices.

“We are committed to giving our customers more choice by supporting a range of convenient ways for them to pay and transfer their money. Customers will soon be able to ‘Beem’ free payments instantly using any smartphone, regardless of who they bank with and without the need to add account details.

Innovations such as Beem and wearables are leading the way in payment solutions because they’re convenient, easy to use, and fit in with people’s lifestyles – we firmly believe in going to where our customers are and providing them with greater choice,” Mr Frazis said.

NAB Chief Operating Officer, Antony Cahill, said the bank is continually looking for opportunities to make banking easier, simpler, and more convenient for its customers, both consumers and businesses.

“Think about all the times you’ve gone out for dinner and split the bill – this app will make it easy for Australians to pay their family and friends instantly. Or, when you go to the local market and need to pay the butcher – this means instant payment through your phone. This is the industry working together to deliver an innovative payments solution, no matter who you bank with,” Mr Cahill said.

Commonwealth Bank is currently conducting user testing of a Beem prototype, with the app to be available for download on iOS and Android smartphones later this year.

Beem will initially have a sending limit of $200 a day ($6,000 per month), with a monthly receiving limit of $10,000 as an initial risk control measure.

Beem will be available to all bank customers and small businesses that hold a global scheme debit card issued by an Australian Authorised Deposit-taking Institution (ADI).

The joint venture will be independently run, with a mandate to actively seek new participants to join the initial three participants. Future product initiatives beyond the payments facility are being planned, including digital wallet features and capabilities.

NAB settles BBSW court case for $50m

In an announcement made late on Friday, NAB admitted that on 12 occasions between 2010 and 2011 its employees “attempted to engage in unconscionable conduct in breach of the ASIC Act”.

The settlement will see NAB fork out a $10 million penalty, cover ASIC’s costs of $20 million and donate $20 million to an ASIC-nominated financial consumer protection fund – all of which will be reflected in its 2017 financial year results.

NAB is the second of three major banks to settle with ASIC following claims of rigging the bank bill swap rate (BBSW). ANZ has already settled, leaving Westpac as the last bank remaining defending the court case.

Commenting on the settlement, NAB group chief executive Andrew Thorburn said the way BBSW was calculated “had changed since that time”.

“We accept we did not meet the high standards of professional conduct that ASIC, the community and NAB expects of itself, in that market during that period,” Mr Thorburn said.

“The ASX is now responsible for the administration of BBSW and NAB fully supports the reforms that are being introduced by the ASX to enhance trust and transparency in the BBSW market.

‘No formula’ for mortgage repricing, says NAB CEO

NAB chief executive Andrew Thorburn told a parliamentary committee on Friday (20 October) that if the bank wanted to maximise profits, it would not have reduced principal and interest rates by 8 basis points for 500,000 customers.

“We are trying to do a whole lot of very delicate things in a very dynamic market,” Mr Thorburn said.

“APRA required 30 per cent. We then have to make a judgement of what the number should be to get to that. That’s an estimate we make in very fast-moving competitive, dynamic environment.

“There is no base number to work off. You have to estimate what you think it takes with the price to reduce your demand in a market where there are dozens of players doing the same thing.”

Committee chair David Coleman MP was eager to find a correlation between NAB’s 35 basis point hike on all interest-only loans and APRA’s direction for banks to cap new interest-only lending at 30 per cent.

Mr Coleman questioned whether the Australian Competition and Consumer Commission (ACCC), which is currently investigating banks’ mortgage pricing decisions, will find the cost of the change as materially less than what NAB charged its customers.

“I don’t think we will ever know,” Mr Thorburn said. “The ACCC [has] all the documents. There is no formula that tells you what the number should be.”

Also appearing in Canberra on Friday was NAB’s chief operating officer, Antony Cahill, who confirmed that the major bank has reduced its interest-only portfolio from 41 per cent to 37.7 per cent of the total book.

He explained that price was just one of the many levers the bank pulled to meet regulatory requirements and lend responsibly. Others include LVR caps, ceasing lending to non-resident borrowers and introducing an LTI ratio.

Mr Cahill also highlighted that the lender introduced “highly competitive fixed rates” that have driven a surge in volumes.

“Our fixed rate lending has more than doubled in the last three months,” the NAB COO said. “We have gone from $500 million to $1.3 billion of customers with fixed rates.”

NAB trialling IBM blockchain technology

National Australia Bank is one of a number of global banks that are trialling a cross-border payments solution powered by IBM Blockchain.

IBM has rolled out a new blockchain banking solution designed to reduce settlement times for cross-border payments.

NAB is the only Australian bank involved in the trial so far, along with institutions from Argentina, Indonesia, Thailand and the Philippines, among others.

According to a statement by IBM, the solution uses a blockchain distributed ledger to allow all parties to have access and insight into clearing and settlement of payments.

“It is designed to augment financial flows worldwide, for all payment types and values, and allows financial institutions to choose the settlement network of their choice for the exchange of central bank-issued digital assets,” said the statement.

The IBM solution, which has been created in collaboration with open source blockchain network Stellar.org and KlickEx Group, is already processing live transactions in 12 currency “corridors” across the Pacific islands and Australia, said IBM.

“For example, in the future, the new IBM network could make it possible for a farmer in Samoa to enter into a trade contract with a buyer in Indonesia.

“The blockchain would be used to record the terms of the contract, manage trade documentation, allow the farmer to put up collateral, obtain letters of credit, and finalise transaction terms with immediate payment, conducting global trade with transparency and relative ease.”

The solutions is run from IBM’s open source Blockchain Platform on Hyperledger Fabric.

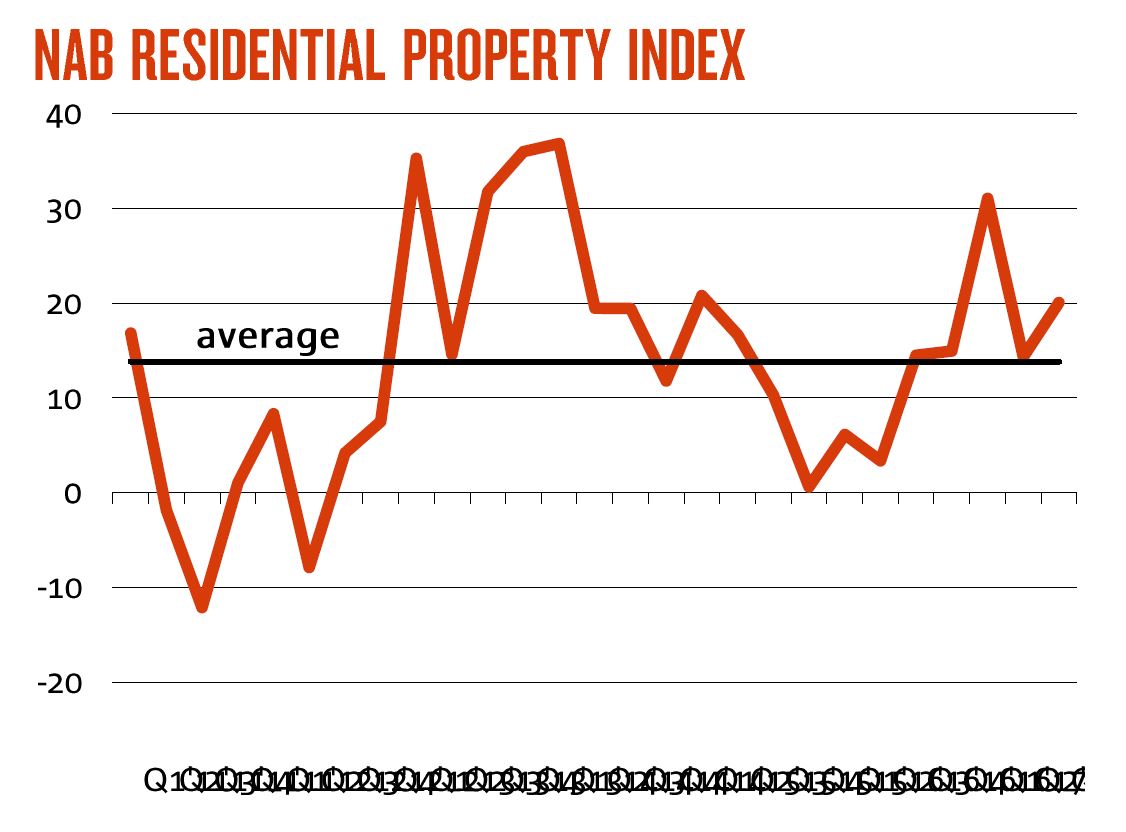

NAB expects prices to slow in 2018-19, but not a severe adjustment.

The latest NAB Residential Property Index is out, and it rose 6 points to +20 in Q3, with sentiment (based on current prices and rents) improving in all states except NSW (which edged down). Sentiment rose sharply in Victoria (up 27 to +63) and in Queensland (up 4 to +16). Whilst sentiment rises and confidence lifts among property experts in Q3, NAB expects prices to slow in 2018-19, but not a severe adjustment.

Australian housing market sentiment lifted over the third quarter of 2017, supported mainly by a large increase in the number of property experts reporting positive rental growth in the quarter and continued house price growth in most states.

“The NAB Residential Property Survey shows an improvement in market sentiment across most states last quarter, but we continue to see market conditions that vary across different locations. The momentum is clearly with Victoria, while NSW is experiencing something of a slowdown,” NAB Chief Economist Alan Oster said.

Confidence (based on forward expectations for prices and rents) lifted in all states, led by Victoria, and with WA the big improver. Despite weakening price growth in NSW, higher confidence is being supported by predictions for higher rents.

First home buyers continue emerging as key buyers in both new and established housing markets, accounting for over 36% of all sales in new housing markets and around 29% in established markets.

During Q3, the overall market share of foreign buyers in new property markets fell to a 5-year low of 9.5%, potentially due to lending restrictions on foreign buyers. Low foreign buying activity in new property markets was led by Victoria, where the share of sales to foreign buyers fell to 14.4% (20.8% in Q2).

For the first time, tight credit was identified as the biggest constraint on new developments in all states, while access to credit was the biggest barrier for buyers of established property. Price levels were the biggest concern in both Victoria and NSW. In WA and SA/NT, property experts said that employment security was the biggest barrier to buying an established home.

They also highlighted lower foreign buying activity in new property markets, with VIC saw the share fall to 14.4% (from 20.8% in Q2) and NSW down to 7.8% from 12% in Q2. In contrast, QLD saw a rise to 11.4%, up from 8.6% last quarter.

NAB’s forecasts on residential prices

NAB Group Economics has revised its national house price forecasts, predicting an increase of 3.4% in 2018 (previously 4.3%) and easing to 2.5% in 2019. Unit prices are forecast to rise 0.5% in 2018 (-0.3% previously), with a modest fall expected in 2019.

“More moderate market conditions reflect a combination of factors which vary across markets, including deteriorating affordability, rising supply of apartments, tighter credit conditions and rising interest rates in the second half of 2018” said Mr Oster.

“But still relatively low mortgage rates, a favourable housing supply-demand balance and strong population growth population growth should continue to provide support for prices going forward.”

“By capital city, house price growth is forecast to be moderate outside of Perth – where prices are flattening out – consistent with good business conditions and better employment growth.”

“Melbourne and Hobart are currently experiencing solid growth in prices; Sydney is cooling and we expect Brisbane and Adelaide will cool. Finally, we expect 2018 to mark the beginning of a gradual turnaround for Perth.”

About 300 property professionals participated in the Q3 2017 survey.

NAB announces start to Comprehensive Credit Reporting

NAB has announced it will commence its roll out of Comprehensive Credit Reporting in February 2018. Read our earlier post “Comprehensive Credit Reporting, Friend or Foe?”

Comprehensive Credit Reporting will provide a more complete picture of a customer’s situation, and mean that lenders like NAB are better able to match the provision of credit to a customer’s individual needs.

“Most Australians have a credit report, and with Comprehensive Credit Reporting, these reports will represent a more balanced reflection of their credit history,” NAB Chief Operating Officer, Antony Cahill, said.

“NAB has championed Comprehensive Credit Reporting from the start because we believe it’s the right thing to do for customers.”

“Comprehensive Credit Reporting will help ensure customers get the right product and credit that’s suitable for their needs, and it will drive more competition in the industry,” Mr Cahill said.

Currently, an Australian’s credit report contains only ‘negative’ information such as payment defaults, credit enquiries, bankruptcies, and court orders and judgements. Under Comprehensive Credit Reporting, positive credit information will be added – including accounts that have been opened, credit limits on those accounts, and details of monthly payments made.

“By having a more complete picture, we can have better discussions with customers and make the right products and credit limits available to them,” Mr Cahill said.

NAB is phasing its roll out of Comprehensive Credit Reporting, commencing with personal loans, credit cards and overdrafts, to ensure it is a smooth transition for customers.

“A number of smaller players have already started participating in Comprehensive Credit Reporting, and we look forward to seeing it roll out across the industry,” Mr Cahill said.

Comprehensive Credit Reporting has been supported by the Federal Government, and will bring Australia in line with many other countries including New Zealand, the USA, and the United Kingdom.