CBA has joined the lenders cutting the buffers rate to 1% for certain borrowers, despite the Council of Financial Regulators saying 3% was appropriate. More extend and pretend.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you.

Buying property, is both challenging and adversarial. The vendor has a professional on their side.

Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make.

Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest.

Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.

CBA has joined the lender cutting the buffers rate to 1% for certain borrowers, despite the Council of Financial Regulators saying 3% was appropriate. More extend and pretend.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you.

Buying property, is both challenging and adversarial. The vendor has a professional on their side.

Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make.

Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest.

Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.

Lenders are selectively lower the hurdles to make mortgage loans and refinance existing borrowing. According to an AFR article, some are tweaking the serviceability buffers. So we look at the implications, given rates are expected to continue to rise.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Rising interest rates are already putting more pressure on households and now banks are reducing their ability to lend at high multiples with an effective reduction of “Borrowing Power” of up to 20%. Combined, this will put more stress on property owners and renovators.

APRA has written to the banks stressing the importance of sound mortgage lending. Better late than never!

WA may well see some of the biggest changes.

Go to the Walk The World Universe at https://walktheworld.com.au/

The use and regard to expenditure benchmarks is “an area that is ripe for further guidance from ASIC”, and will be a focus of the updated RG 209 guidance next month, the financial services regulator has suggested. Via The Adviser.

Speaking at the parliamentary joint

committee on corporations and financial services hearing on its

oversight of the Australian Securities and Investments Commission (ASIC)

and the Takeovers Panel on Tuesday (19 November), chairman James

Shipton and commissioner Sean Hughes revealed some of the specific

issues that will be addressed in its upcoming revised guidance on responsible lending.

The chair told the parliamentary

joint committee that there was a need for “more contemporaneous”

guidance around responsible lending, particularly given the increasing

number of online lenders, the upcoming open banking scheme and increased

data, the evolution of business practices, updates to technology, and

automatisation of systems.

Commissioner Hughes elaborated that

the “greater use of technology and technological tools to verify borrow

information in real time” and have it “fully verified using technology

solutions within 58 minutes” was an advancement that was not available

when the National Consumer Credit Protection Act(NCCP) was written 10 years ago.

Another area that required updating was around expense benchmarks used to verify borrower expenses – such

as the Household Expenditure Measure (HEM) – particularly given the

fact that some categories of expenses are not included in HEM, such as

certain medical costs, superannuation contributions and mortgage

repayments.

Commissioner Hughes said: “We are not

requiring lenders to scrutinise how many cups of coffee you are having,

whether you are going to an expensive gym and all those things. That is

not what our guidance requires.

“What our guidance is suggesting (and I emphasize suggesting)

is that lenders could have regard to unusual patterns and expenditure,

which take a borrower outside normal patterns for that person.”

He continued: “There are some

categories of expense that require a lender to go above and beyond the

standardised benchmark. So, this is something we’ve recognised through

the consultation process that we have undertaken. It’s been something

that all the submissions have commented on, and we think it’s an area

that is ripe for further guidance from ASIC.”

Mr Hughes later told the committee that another area ASIC will be “zeroing in on” will be the level of enquiries needed for refinances, among other activities.

He said: “[W]hat we do want to

preserve, as part of our guidance in the next version, is the concept of

scalability. And this is something that other submitters [to the

consultation] have commented on as well.

“So for instance, if I use the

example of a borrower who is seeking to refinance an existing loan that

retains the same overall credit headroom – perhaps swapping out another

security, taking advantage of lower interest rates – we would say that,

if all other things haven’t changed and the borrower’s

capacity to repay the loan remains the same and their income seem

stable, that would not require a lender to do the forensic detailed

examination of how many cups of coffee, or gym memberships, etc., they

have that might be required in other instances.”

Other areas that the new guidance

will reportedly clarify include detailing situations where the

responsible lending guidance does not apply (such as small-business

lending) as well as when the guidance does apply outside of mortgages

(such as for credit cards and unsecured personal loans).

However, Mr Shipton emphasised that ASIC’s

new guidance will be “principles-based” rather than dogmatic, and

“provide discretion by financial institutions and lenders, to be able to

exercise their good professional discretion in determining these

areas”, given that there is “always going to nuance” and “unique

situations” in providing finance.

He continued: “There will never be able to be a set of rules or guidance written which will be able to precisely convey and allow for every precise circumstance. That’s why principles-based guidance is important. That’s what we’re going to, that’s what we’re going to be aiming to do.”

The latest UBS study, the fifth in their series looking at lending standards, and based on a survey of around 900 home loan applicants reveals that (perhaps surprisingly) there was a rise in “porkys” being told as part of the mortgage application, despite the Banking Royal Commission.

As a result, more than a third of Australian home loans could have ‘liar loans’ based on inaccurate information.

UBS Analyst Jonathan Mott said:

While asking detailed questions appears to be prudent, it does not appear to be effective as many factually inaccurate mortgages are still working their way through the process.

Of the borrowers who said their application was not completely factual in the past year, 20 per cent overstated their income, 23 per cent understated debts, 34 per cent understated their living costs, and 23 per cent misstated multiple categories.

Now, this is consistent with the DFA surveys where true incomes and costs are often higher than might be expected. And the extra granularity now required by the banks (many categories of costs, more detail on incomes etc) can create a false sense of accuracy – especially when many households are making best guesses to provide information to support their applications.

And financial intermediaries still appear to be part of the story, with a higher percentage of borrowers who misstated information on applications through a mortgage broker (40 per cent) than through the banks (27 per cent).

UBS said that a “large number” of survey respondents indicated their mortgage consultant advised them to misrepresent elements of their application.

At a time when the mortgage growth stops are being pulled, and lower rates are expected in a highly competitive market, this will simply create a bigger bust later.

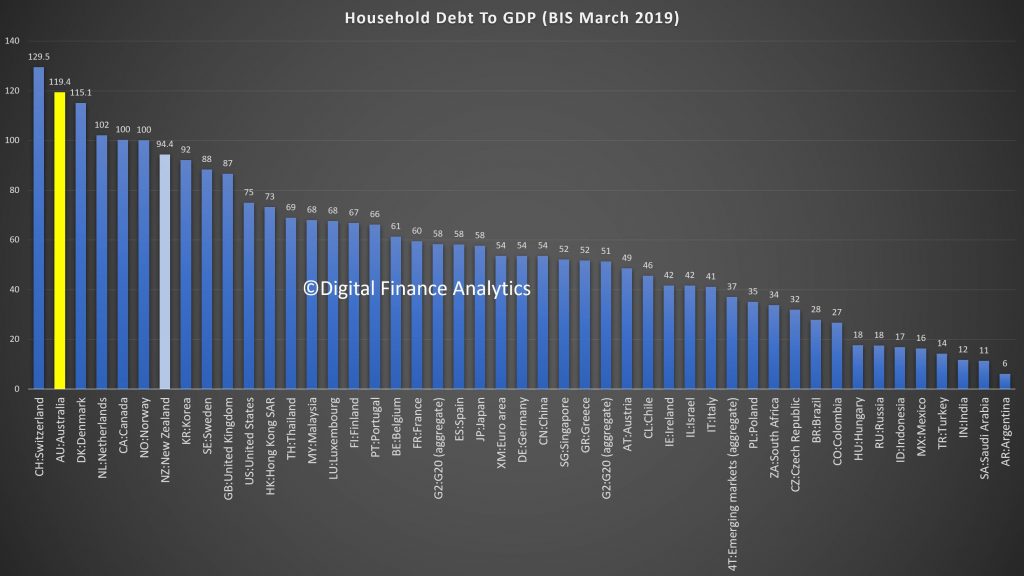

And remember that on an international basis, we are right at the top of the international benchmarks in terms of household debt.

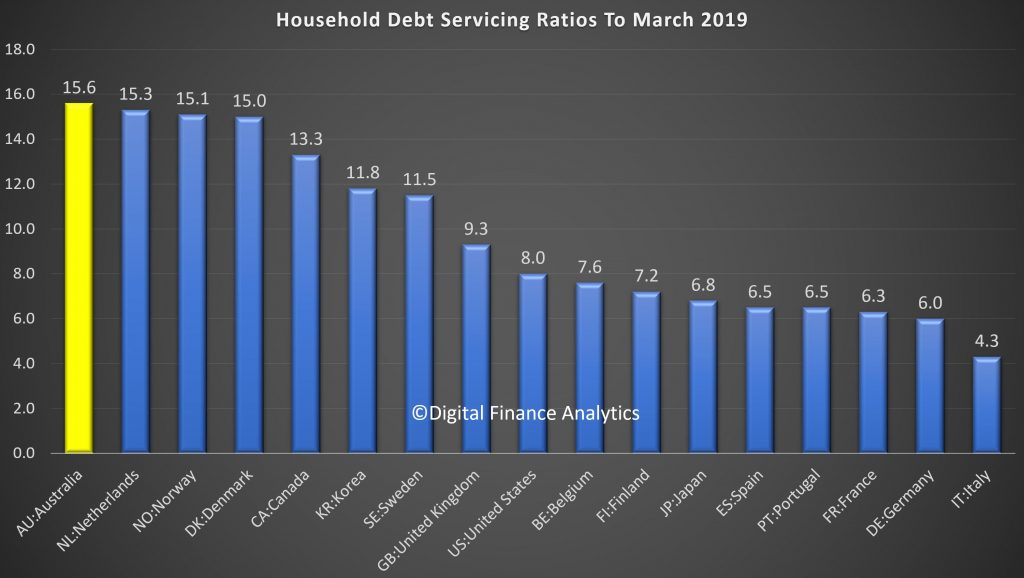

In fact according to the latest BIS data we lead in terms of debt servicing ratios.

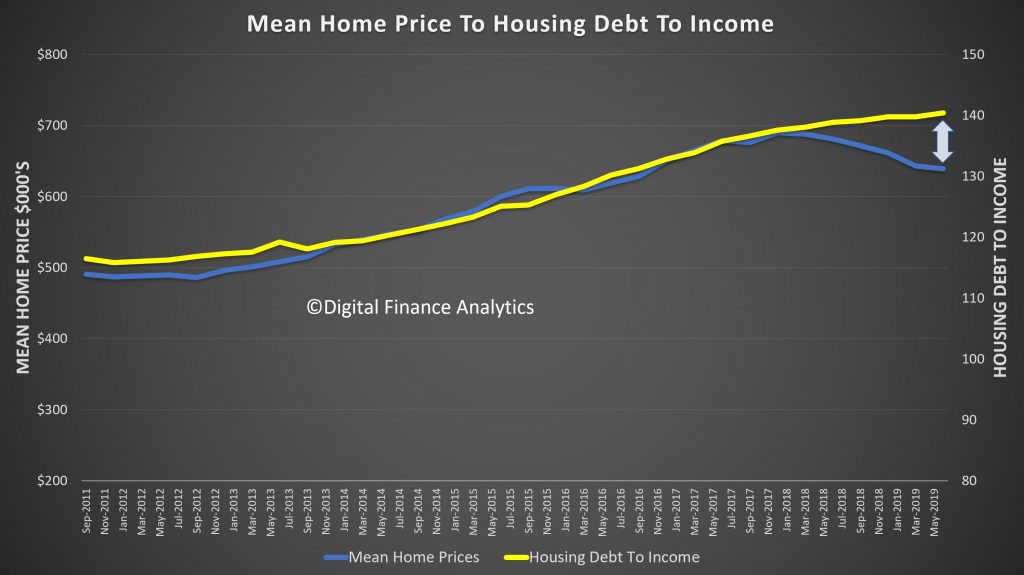

And the falls in prices have created a significant gap which highlights the risks in the system.

You can watch our recent show where we look at household debt in more detail including the data above.

Westpac will decrease its floor rate from 5.75% to 5.35%, effective 30 September.

The same change will go into effect at its subsidiaries: St. George, BankSA and Bank of Melbourne.

After the initial round of floor reductions across lenders of all sizes, Westpac matched CBA with the higher floor rate of the big four banks at 5.75%, while ANZ and NAB each amended theirs to 5.50%.

Smaller lenders followed suit, the majority also updating their rates to either the 5.50% or 5.75% figure.

While some went even lower, ME Bank amending its rate down to 5.25% and Macquarie to 5.30%, Westpac has taken a step away from the other majors with its newest update.

With July marking the strongest demand for new mortgages in five years and further RBA rate cuts expected in the near future, the floor reduction seems well timed to capitalise on the strong market activity forecasted to continue into the coming

This is a race to the bottom, and is bad news for financial stability. When will APRA wake up? It will also jack some home prices higher, in selected areas and types.

Following its Tuesday victory against ASIC, with the court dismissing the regulator’s allegations of irresponsible lending, Westpac has announced a spectrum of changes to its home lending policies. From Australian Broker.

The updated guidelines are set to go into effect on 20 August, at not

only the major, but its associated brands: St. George, Bank of

Melbourne, and Bank SA.

Perhaps most notably, Westpac is to update and add new expense

categories to its household expenditure measure “to reflect industry

guidelines on the HEM values we use as our customer expense benchmarks” –

bringing the total number of categories from 13 to 18.

Further, the bank will apply income-based HEM bands based on total gross unshaded income, including gross rental income.

Particularly relevant in light of the recently dismissed court case, in instances when total liability is seven times or more higher than total gross income, the loan applications will be reviewed by a credit assessment officer rather than run through the automated system.

ASIC’s case against the bank had hinged on the allegation Westpac

breached the National Consumer Credit Protection Act 2009 through

assessing loans via its automated system which solely considers the

benchmark HEM rather than customers’ declared living expenses.

Westpac additionally addressed the changes being made to tax debt through changing its approach to margin loans. They will now be assessed on the higher of 1% of the balance or the customer’s monthly declared commitment.

Further, Westpac will require a more comprehensive understanding of

payment plans businesses have made with the ATO and decline to lend to

customers with an overdue amount payable to the ATO for the previous

year’s tax without a formal payment plan in place.

The policy changes will impact all new and re-submitted applications

made from Tuesday, requiring brokers to utilise the expanded 18

categories for expenses, as well as heed the new seven times

debt-to-income ratio.

Westpac also announced that changes to the commercial, SME and private wealth broking channels will be made later this year.

Blog")