Australians are embracing digital payments according to the latest Milestones Report released by the payments industry self-regulatory body Australian Payments Network (previously Australian Payments Clearing Association). As a result, cash and cheques are in decline. Australia’s digital economy underpins what can increasingly be characterised as a less-cash society.

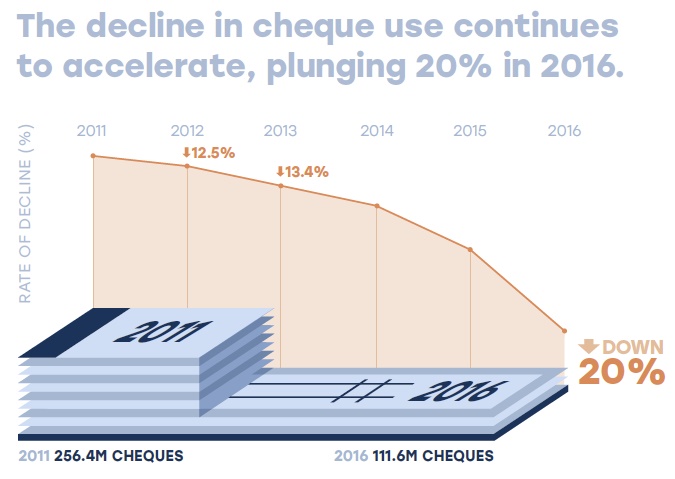

Cheque use plunged 20% to 111.6 million – the largest drop ever-recorded. The value of cheques dropped by 6% over the same period, after remaining flat in 2015 and dropping by less than 1% in 2014. Over the last five years, cheque use has dropped 56%.

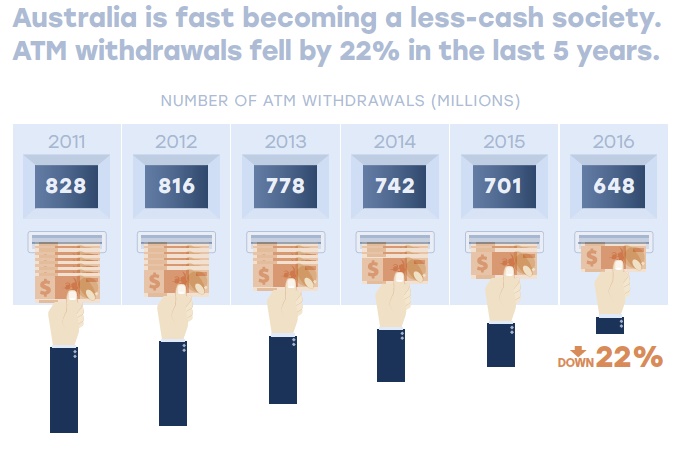

The number of ATM withdrawals dropped 7.5% to 648.5 million in 2016 following a 5.5% drop in 2015 and a 4.7% drop in 2014. Since 2011, ATM withdrawals have dropped by 22%.

CEO of the Australian Payments Network, Dr Leila Fourie said “Looking at the payment choices that Australians make, it’s clear that the vast majority of us are moving away from cash and cheques faster than ever before. This is happening because of widespread use of new technology combined with a strong preference for faster and more convenient payment options.”

CEO of the Australian Payments Network, Dr Leila Fourie said “Looking at the payment choices that Australians make, it’s clear that the vast majority of us are moving away from cash and cheques faster than ever before. This is happening because of widespread use of new technology combined with a strong preference for faster and more convenient payment options.”

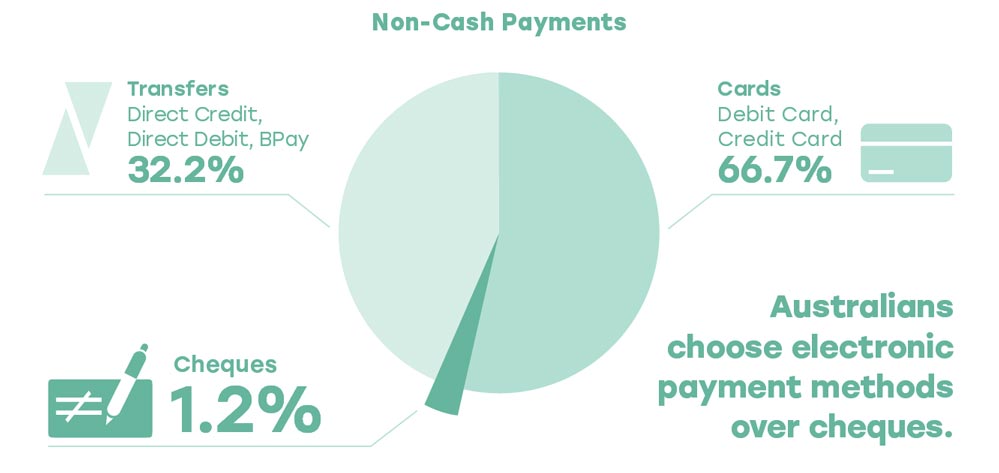

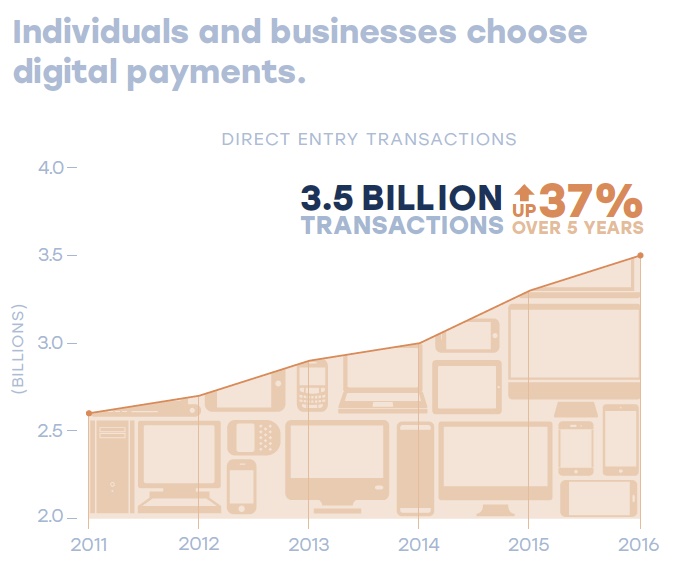

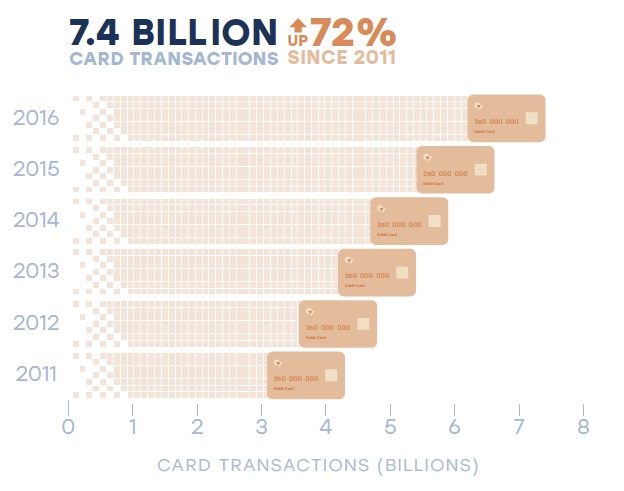

Consumers’ preference for digital payments is reflected in the strong year-on-year growth in card and direct entry transactions:

Consumers’ preference for digital payments is reflected in the strong year-on-year growth in card and direct entry transactions:

- Australians used their cards 12.3% more in 2016, making 7.4 billion transactions.

- Direct entry transactions (direct debit and direct credit) increased by 8.6% to 3.5 billion.

Over the last five years, card transactions grew by 72% and direct entry by 36%.

Increased smartphone penetration, which reached 84% in 2016, up from 76% in 2014, is an important contributing factor.

Increased smartphone penetration, which reached 84% in 2016, up from 76% in 2014, is an important contributing factor.

Australia’s online retail spend was estimated at $21.6 billion in 2016 and encouragingly from a digital inclusion perspective, this spend is not restricted to digital natives. Older Australians are using online shopping platforms more, with domestic online spending growing by 8.7% for those in the 55-64 age group, and 7.5% for 65+.

The Report also tracks progress on initiatives supporting Australia’s transition to the digital economy including the industry’s New Payments Platform and Australian Payments Plan.