NAB has launched a digital assistant that helps MLC members engage with their superannuation.

Available on Google Home devices, Talk to MLC answers 15 common questions members ask: such as how to open an MLC account, find lost super and change investment options.

MLC customer experience specialist Peter Forster said the super fund expects most members to access superannuation in a way that’s convenient and personalised without the need for passwords.

He said millennials and older Australians will likely be the first to embrace Talk to MLC.

“The technology took us six weeks to develop and deploy, and we’re in the process of developing other technology at a similar speed that will help to reduce asymmetry of information and further benefit our customers,” Forster said.

He added in the near future MLC will be able to provide personalised tips to help members boost their super; project where their super balance will be at retirement time; and advise how best to invest their money in super.

NAB executive general manager of digital and innovation Jonathan Davey said the proliferation of voice-activated, hands-free devices such as Siri and Google Home and Amazon’s Alexa in the Australian market is reshaping consumer behaviour and expectations.

“We live in a world that wants instant gratification. We want quick answers and problems that are solved immediately – we don’t want to be left waiting. Our lives are busier than ever before,” Davey said.

Early this year, CBA launched Ceba, a chatbot that recognises about 60,000 consumer banking questions.

Ceba’s point of difference, according to CBA executive general manager digital Pete Steel, is that it can actually carry out tasks for customers, rather than providing instructions on how they can be done.

ANZ is also deploying chatbots with the help of Progress’ NativeChat, to enable customers to converse and transact with chatbots naturally. NASDAQ-listed Progress helps develop industry-specific and self-learning chatbots for organisations.

In 2018, the way customers are banking in the Riverina and the surrounding areas has changed. Today, in response, NAB confirms changes to some of its branches in the area.

NAB invests $1.6M to improve branches in the Riverina and surrounding areas in 2017 and 2018.

Following consultation with local teams, NAB can confirm Ardlethan, Lockhart, Grenfell, Culcairn, Boort, Barham and Euroa branches will close in June.

Customers in these towns can continue to do their banking at Australia Post offices, including making deposits up to $10,000 cash or withdrawals up to $2,000 per day.

NAB continues to back the Riverina through its other NAB branches across the region, sponsorships, including NAB AFL Auskick, and by funding and advocating for infrastructure so regional areas can grow.

Our business and agri bankers will continue to service the areas.

Locally, NAB is investing more than $1.6M into improving branches in Cowra, Seymour and Kerang, completed last year, and Tatura, Alexandra and Griffith, scheduled to be completed by September 2018, including installing and upgrading 32 ATMs in the area. Many of these ATMs are ‘Smart ATMs’, where customers can make deposits, check balances, and withdraw cash so customers can bank at their convenience.

As improvements are made to some branches, other branches in the area will be closing. Between 80-90% of NAB customers in Ardlethan, Lockhart, Grenfell and Culcairn are using other branches in the area such as Temora, Wagga Wagga, Young and Holbrook. Similarly approximately 85% of customers using Euroa, Boort and Barham are using other branches .

NAB General Manager, Retail, Paul Juergens, explained the decision was a difficult one to make and was only made after careful consideration.

“While our branches continue to be an important part of what we do at NAB, the way our customers are banking has changed dramatically in recent years,” Mr Juergens said.

“Increasingly we find that our customers are banking at other branches, or prefer to do their banking online, on the phone, or through our mobile app.

“In the locations we are closing, more than 80% of our customers are also using our other NAB branches in the area.

“Importantly, we are continuing to support the Riverina and surrounding areas, including a $1.6M investment into other branches in the area as well as through local sponsorships.”

Mr Juergens emphasised that NAB wants to continue to help our customers with their banking.

“Over the coming weeks, we’ll be spending time with our customers explaining the different banking options available to them, including online banking and banking through Australia Post.

“We know that some NAB customers still like to bank in person, which is why we have a strong relationship with Australia Post offices, which offer banking services on NAB’s behalf.

“At Australia Post, NAB customers can do banking like check account balances, pay bills and make deposits up to $10,000 cash or withdrawals up to $2,000 per day.”

NAB is working with our local branch employees to discuss their next steps.

“When we make changes to our branches, we make every effort to find opportunities for our local teams at other branches in our network, and often this is possible. If we can’t find opportunities, we help our employees through The Bridge, our industry leading program where employees are provided up to six months of career coaching as they decide what’s next for them – whether that be retirement, pursuing a new career or starting a small business.”

The Australian Banking Association welcomes today’s ACCC interim report into residential mortgages, which clearly shows very high levels of discounting in the Australian home loan market. It’s clear that competition is delivering better deals for customers, shopping around works and Australians should continue to do so to get the best discounts on the advertised rate.

The report itself states that “an overwhelming majority of borrowers with variable rate residential mortgages at the Inquiry Banks were paying interest rates significantly lower than the relevant headline rate” (the advertised rate). Discounts on home loans ranged between .78% and 1.39% below the relevant headline interest rate.

The advertised variable discount rate for home buyers today is 4.5%, close to the lowest ever recorded.

Data from APRA(1) and Canstar further illustrates there is strong competition in the home loan market, with over 140 providers, offering over 4,000 home loan products. Truly a vast and competitive market for Australians to choose a home loan.

Other evidence shows that Australians are taking advantage of this competitive market and are shopping around. Research by Galaxy shows that:

3 million people had switched banks over the last three years.

Of those who had switched banks over the last three years, two-thirds (68 per cent) found that switching was an easy process.

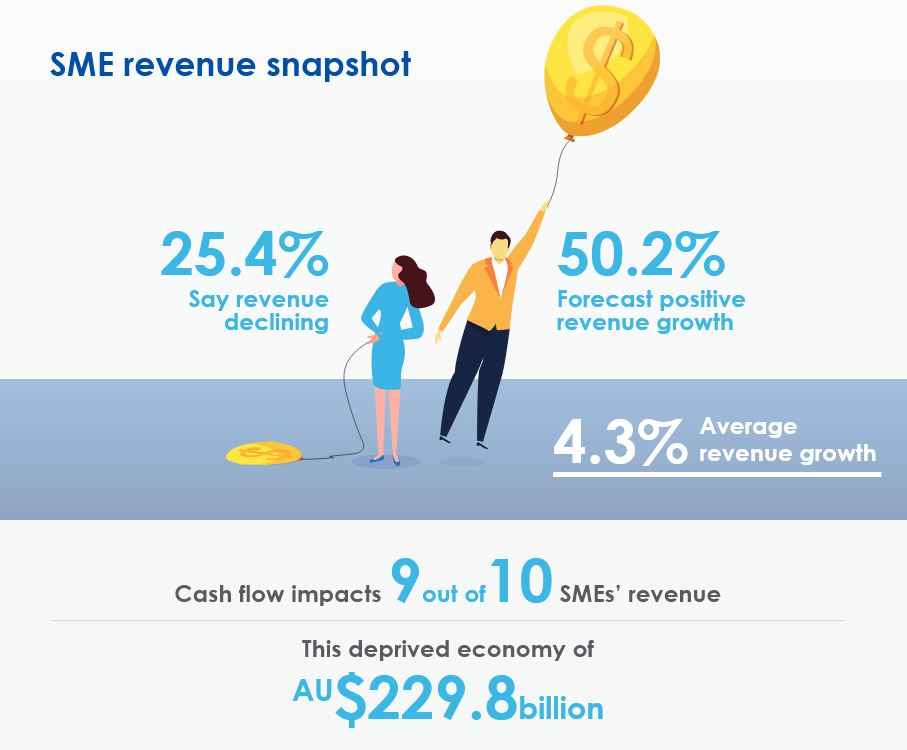

The latest edition of the Scottish Pacific SME Growth Index has been released. It gives an interesting snapshot on the critically important SME sector in Australia. Once again, as in our own SME surveys, cash-flow is king. 90% of SME owners said they faced cash-flow related issues. That said, the non-bank sector, including Fintechs need to do more to raise awareness of the solutions they offer.

SME business confidence is on the rise finds small business owners forecasting revenue to improve during the first half of 2018.

There appears to be a splitting of the pack in SME fortunes, with a greater number of previously “unchanged” growth SMEs moving into positive or negative growth.

For most SMEs cash flow has improved compared to 12 months ago, however one in 10 say they are worse off now. The number of SMEs reporting significantly better cash flow (27%) and better cash flow (42%) will hopefully act as a major driver of new capital expenditure and business investment demand.

Despite this reported rise in cash flow, nine out of 10 SMEs say they had cash flow issues in 2017 and nine out of 10 say these issues impacted on revenue. On average, small businesses say that better cash flow would have increased their 2017 revenue by 5-10%.

For SMEs with plans to invest in expansion over the next 6 months, 24% of them report they will fund that growth by borrowing from their main relationship bank – continuing a downward trend, and well short of the high of 38% who nominated this option to fund growth in the first round of the Index in September 2014.

21.7% of SMEs say they plan to use non-bank lenders to fund upcoming growth (with 90.8% planning to use their own funds). Non-bank lending intentions have trended upwards since the first Index, closing the gap between bank and non-bank lending intentions. Despite these intentions, more than 91% of SMEs responded in H1 2018 that in the previous 12 months they had not accessed any non-bank lending options to provide working capital for their business.

So while SMEs seem unsatisfied with traditional banks, they are not yet fully accessing opportunities available to them in the non-banking sector.

Results show that growth SMEs are five times more likely to use alternative lending options than declining growth SMEs, with debtor finance the most popular option. The growth potential for the non-bank lending sector is significant, given that 48% of SMEs who didn’t use non-bank lending in 2017 are considering it for 2018.

With SME owners revealing a solid reliance on personal credit cards to give their business the working capital required for day to day operations, those with better business solutions must find a way to reach these small business people.

Businesses implementing appropriate working capital solutions to get on top of cash flow impediments are well placed to realise their growth ambitions.

An excellent summary of the ACCC’s report, which we discussed yesterday, from MPA’s Otiena Ellwand. It confirms the banks were well aware of the opportunity to capture substantial economic benefit of hundreds of millions of dollars in additional revenue, and a quest to meet financial targets.

The ACCC’s interim report into residential mortgage pricing reveals the “lack of transparency” around how the ‘inquiry banks’ – ANZ, CBA, Macquarie, NAB and Westpac— make these decisions.

The regulator found a “lack of vigorous price competition” between the big four banks in particular, with negative public reaction being a major concern.

The ACCC examined thousands of internal documents for this report. This is what they reveal:

1. Banks raised rates to reach internal performance targets:

The ACCC found that achieving profit and/or revenue-related performance targets affected the banks’ decisions on interest rates.

For example, concern about a shortfall relative to target was a key factor in two inquiry banks increasing headline variable interest rates in March 2017.

Tweaking the headline variable interest rates may be in the banks’ favour because it affects both new and existing borrowers, so even small increases can have a significant impact on revenue, the report found. And the majority of existing borrowers would likely not be aware of small changes in rates and would therefore be unlikely to switch.

2. A shared interest in avoiding disruption:

The banks’ pricing behaviour “appears consistent with ‘accommodating’ a shared interest in avoiding disruption of mutually beneficial pricing outcomes”, the ACCC found.

Instead of trying to increase market share by offering the lowest interest rates, the big four banks were mainly preoccupied and concerned with each other when making pricing decisions.

In fact, in late 2016 and early 2017, two of the big four banks each adopted pricing strategies aimed at reducing discounting in the market even though this was potentially costly for them if the other majors didn’t follow suit.

3. Reputation is everything:

The banks are particularly attentive to when and how they explain interest rate decisions to the public, and strong public reaction can even put pricing decisions on hold.

One inquiry bank decided to defer a rate rise due to the reputational impact.

Another bank’s internal document noted that changing the headline variable interest rate without an easily understood reason or trigger event could have the “potential to attract a lot more attention and focus” from the public.

In an email discussion among a group of bank executives, one leader noted that it had not made the case for repricing its back book.

“I am also very conscious that we suspect that many first home buyers, unable to afford owner occupier homes, have instead have [sic] bought [an] investment property to take advantage of the low interest rates, tax break and keep a foot on the housing market. I don’t think that this would play well from a customer or community stand point,” the executive wrote.

4. Not just about APRA:

In July 2015, all of the big four banks attributed interest rate increases to APRA’s limits on investor lending.

However, one inquiry bank said in an internal memo that the “substantial economic benefit” of hundreds of millions of dollars in additional revenue was a consideration in its decision.

Where does this ACCC report come from?

Back in June 2017, the banks indicated that rate increases were primarily due to APRA’s regulatory requirements, but once under further scrutiny they admitted that other factors contributed to the decision, including profitability.

In December, the ACCC was called on by the House of Representatives Standing Committee on Economics to examine the banks’ decisions to increase rates for existing customers despite APRA’s speed limit only targeting new borrowers.

The investigation falls under the ACCC’s present enquiry into residential mortgage products, which was established to monitor price decisions following the introduction of the bank levy.

Interesting speech from Guy Debelle, RBA Deputy Governor “Risk and Return in a Low Rate Environment“. He explores the consequences of low rates, on asset prices, and asks what happens when rates rise. He suggests that we need to be alert for the effect the rise in the interest rate structure has on financial market functioning.

The recent spike in volatility is one example of this. This was a small example of what could happen following a larger and more sustained shift upwards in the rate structure. The recent episode was primarily confined to the retail market. The large institutional positions that are predicated on a continuation of the low volatility regime remain in place. He has expected that volatility would move higher structurally in the past and this has turned out to be wrong. But He thinks there is a higher probability of being proven correct this time.

In other words, rising rates will reduce asset prices, and the question is have investors and other holders of assets – including property – been lulled into a false sense of security?

Here is the speech:

Low Interest Rates

I am going to use the rate structure in the US, and particularly the yield on a US 10-year Treasury bond to illustrate the shift in the rate structure (Graph 1).

Graph 1

As you are all aware, in the wake of the financial crisis and the sharp decline in global growth and inflation, monetary policy rates round the world were reduced to historically low levels. In a number of countries (Australia being one notable exception), the policy rate was lowered to its effective lower bound, which in some cases was even in negative territory.

In part reflecting the low level of policy rates and the slow nominal growth post crisis, long-term bond yields also declined to historically low levels. 10-year government bond yields in some countries, including Germany, Japan and Switzerland have been negative at various times in recent years. In 2015, over US$14 trillion of sovereign paper had negative yields.

For the past decade, the yield structure in the US has been lower than at any time previously. Let me put in context the current excitement about the 10-year yield in the US reaching 3 per cent. In the three decades prior to 2007, the low point for the yield was 3.11 per cent.

All this goes to say that we have been living in a period of unusually low nominal bond yields. How long will this period last?

One way to think about this question is to ask whether what we are seeing is the realisation of a tail event in the historical distribution of interest rates. While this tail event has now lasted quite a long time, if you thought it was a tail event, then you would expect yields to revert back to their historical mean at some point. You also wouldn’t change your assessment of the distribution of future realisation of interest rates.

On the other hand, it might be the case that the yield structure has shifted to a permanently lower level because of (say) secular stagnation resulting in structurally lower growth rates for the major economies for the foreseeable future. If this were the case, you would change your assessment of future interest rate outcomes.

I don’t know the answer to this question, but it has material implications for asset pricing.

As I said earlier, the prices of many assets could be broadly validated if you believe the low rate structure is here to stay. This is because the lower rate structure means that the rate with which you discount expected future returns on your asset is lower and hence the asset price is higher for any given flow of future earnings.

The current constellation of asset prices seems to be based on the view that the global economy can grow strongly, with associated earnings growth, but that strong growth will not lead to any material increase in inflationary pressure.

You might want to question how long such a benign conjuncture could last. Current asset pricing suggests that the (average) expectation of market participants is that it will last for quite a while yet.

It is also worth pointing out that it is possible that a move higher in interest rates occurs alongside higher expected (nominal) dividends because of even higher real growth. If this were to occur it would not necessarily imply that asset prices have to adjust. It would depend upon the relative movements in earnings expectations and interest rates; that is, the numerator and denominator in the asset price calculation.

How might we know whether the distribution of interest rates has shifted? One can think of the interest rate distribution as being anchored by the neutral rate of interest. I talked about this in the Australian context last year. As I said then, empirically the neutral rate of interest is difficult to estimate. It is even harder to forecast. The factors which affect it are often slow moving. But sometimes they aren’t, most notably around the time of the onset of the financial crisis in 2007-08, when estimates of the neutral rate declined rapidly and significantly. Currently, there is a debate in the US as to whether the neutral rate of interest has bottomed and is shifting up. This raises the question as to the degree and speed with which such a movement in the neutral rate in the US might translate globally.

All of these questions highlight to me the inherent uncertainty about the future evolution of interest rates. One might decide that interest rates are going to continue to remain lower for longer, but I struggle to see how one can hold that view with any great certainty. Yet there appears to me to be very little, if any, compensation for this uncertainty in fixed income markets. Most estimates of the term premium in the 10-year US Treasuries are around zero, or are even negative (Graph 2). Investors are not receiving any additional compensation for holding an asset with duration.

Graph 2

That is, one can have different views about the longevity of the current rate structure. But, in part reflecting these different views about longevity as well as the unusual nature of the current environment, there is a significant degree of uncertainty about the future. Yet many financial prices do not obviously offer any compensation for that uncertainty.

Low Volatility

It’s not only in the term structure of interest rates where compensation for uncertainty is low. Measures of implied volatility indicate that compensation for uncertainty about the path of many other financial prices is also low, and has been low for some time. This has been true across short and long time horizons, across countries, including Australia, across asset classes, and across individual sectors within markets (Graph 3 and 4). I will discuss some of the possible explanations for this, drawing on material published in the RBA’s February Statement on Monetary Policy, and also discuss the recent short-lived spike in volatility in equity markets.

Graph 3

Graph 4

Implied volatility is derived from prices of financial options. Just as the term premium measures compensation for uncertainty about the future path of interest rates, implied volatility reflects uncertainty about the future price of the asset(s) underlying a financial option. The more certain an investor is of the future value of the underlying asset, or the higher their risk tolerance, the lower the volatility implicit in the option’s price will be.

Thus, one interpretation of the recent low level of volatility is that market participants have been more confident in their estimates of future outcomes. This is consistent with the observed reduction in the variability of many macroeconomic indicators, such as GDP and inflation, and a decline in the frequency and magnitude of the revisions that analysts have made to their forecasts of such variables (Graph 5). Given the importance of these variables as inputs into the pricing of financial assets, it’s no surprise that greater investor certainty about their future values has in turn given investors more certainty about the future value of asset prices.

Graph 5

As you can see from all three graphs, a similar degree of certainty about the future was present in the mid 2000s, when there was a high degree of confidence that the ‘Great Moderation’ was going to deliver robust growth and low inflation for a number of years to come.

Monetary policy is also an important input into the pricing of financial assets, so a reduction in the perceived uncertainty around central bank policy settings may also have contributed to low financial market volatility. Monetary policy settings have been relatively stable in recent years, and where central banks have adjusted interest rates or their purchases of assets, these changes have tended to be gradual and clearly signalled in advance. Central banks have also made greater use of forward guidance as a policy tool to attempt to provide more certainty about the path of monetary policy.

But while central banks might act gradually and provide this guidance, the market doesn’t have to believe the guidance will come to pass. There are any number of instances in the past where central bank forward guidance didn’t come to pass. In my view, it is more important for the market to have a clear understanding about the central bank’s reaction function. That is, how the central bank is likely to adjust the stance of policy as the macroeconomic conjuncture evolves. If that is sufficiently clear, then forward guidance does not obviously have any large additional benefit, and runs the risk of just adding noise or sowing confusion.

Hence an explanation for the low volatility could be the assumption of a stable macro environment together with an understanding of central bank reaction function, rather than the effect of forward guidance per se.

The low level of implied volatility could also reflect greater investor willingness to take on financial market risk. This is consistent with measures that suggest demand for derivatives which protect against uncertainty has declined. It is also consistent with other indicators of increased investor appetite for financial risks, such as the narrowing of credit spreads. This increased risk appetite may in part reflect the low yield environment of recent years; protection against uncertainty is not costless, and so detracts from already low returns.

There has also been an increased interest in the selling of volatility-linked derivatives by investors to generate additional returns in the low yield environment in recent years. Effectively, some market participants were selling insurance against volatility. They earned the premium income from those buying the insurance whilever volatility remains lower than expected, but they have to pay out when volatility rises. In recent years, there was a steady stream of premium income to be had. (This is even more so if I were a risk neutral seller of insurance to a risk-averse buyer, in which case, the expected value of the insurance should be positive.) But the payout, when it came, was large. I will come back to this shortly in discussing recent developments.

This reduced demand for volatility insurance combined with increased supply saw the price fall.

Graph 6

Such an extended period of low volatility is not unprecedented, although the recent episode was among the longest in several decades (Graph 6). Prolonged periods of low volatility have sometimes been followed by sudden increases in volatility – although generally not to especially high levels – and a repricing of financial assets. A rise in volatility could be associated with a reassessment of economic conditions and expected policy settings, in which case, one might not expect the rise to last that long. In contrast, a structural shift higher in volatility requires an increase in uncertainty about future outcomes, rather than simply a reassessment of them. But just as I find it puzzling that term premia in fixed income markets have been so low for so long, I similarly find it puzzling that measures of volatility do not seem to embody much uncertainty either.

The recent spike in volatility in early February is interesting in terms of the market dynamics, coming as it did after a prolonged period of low volatility.

From around September 2017, there had been a rise in bond yields, most notably in the US, as confidence about the outlook for the US and global economy continued to improve. This rise in yields accelerated in January 2018, again most notably in the US, in large part in response to the passage of the fiscal stimulus there. As Graph 7 shows, the rise in Treasury yields in the first part of this year reflected both a rise in real yields and compensation for inflation. This reassessment of the macroeconomic outlook was also reflected in a reassessment (albeit relatively small) of the future path of monetary policy in the US. It is also worth noting that the real yield can incorporate any risk premium on the underlying asset. So the recent rise may also be a result of a change in the assessment of investors about the riskiness of US Treasuries.

Graph 7

In light of the reassessment of the macro environment it was somewhat surprising that through the month of January, equity prices in the US rose as strongly as they did. As I discussed at the outset of this speech, I would expect that a shift upwards in the structure of interest rates would result in a repricing of asset prices more generally. In late January, this indeed is what happened: equity prices declined, again most sharply in the US. There was a sharp rise in volatility. The initial rise in volatility was exacerbated by the unwinding of a number of products that allowed retail investors (and others) to sell volatility insurance, and the hedging by the institutions that had offered those products to their retail customers. Indeed, unwinding is a euphemism as, in some cases, the retail investor lost all of their capital investment. Having seen the legendary Ed Kuepper and the Aints again last Friday, it’s worth remembering to “Know Your Product”, otherwise it will be “No, Your Product”.

What is particularly noteworthy about this episode is how much the rise in volatility, and the large movements in prices, was confined to equity markets. While volatility rose in other asset classes, it did not increase to particularly noteworthy levels. For example, there was relatively little spillover to emerging markets. This is in stark contrast to similar episodes in the past. The fact that these products were particularly associated with volatility in US equity prices appears to have contributed to the limited contagion. Also noteworthy is how short-lived the rise in volatility has been (to date). In discussions with market participants, one possible cause of this is that the unwinding of volatility positions has been largely confined to the retail market, which was relatively small in size. There does not seem to have been much adjustment in the volatility exposures of large institutional market participants to date.

That said, it is conceivable that this episode gives a foretaste of the sort of market dynamics that might occur if there were to be a further rise in yields as the market reassesses the outlook for output and, particularly, inflation.

Demand and Supply Dynamics

Another consideration in thinking about future developments in the yield structure is the balance of demand and supply in the sovereign debt market. It is often difficult to assess the degree of influence that demand and supply dynamics have on the market. But there are some noteworthy developments occurring at the moment that are worth highlighting.

Graph 8 shows the net new debt issuance by the governments of the US, the euro area and Japan, and the net purchases of sovereign debt by their respective central banks. It shows that the peak net purchases by the official sector occurred in 2016. This happens to coincide with the low point in sovereign bond yields, but I would not attribute full causation to that. The central bank purchases are a reaction to the macroeconomic conjuncture at the time which itself has a direct influence on the yield structure. That said, one of the main aims of the central bank asset purchases was to reduce the term premium.

Graph 8

But in 2018, there is going to be a net supply of sovereign debt to the market from the G3 economies for the first time since 2014. This reflects a few different developments. The Federal Reserve started the process of reducing the size of its balance sheet last year by not fully replacing maturing securities with new purchases. While this is a very gradual process, it is a different dynamic from the previous eight years. At the same time, the US Treasury will issue considerably more debt than in recent years to finance the US budget deficit, which has grown from 2 per cent of GDP in 2015 to over 5 per cent in 2019 as the Trump administration implements its sizeable fiscal stimulus.

In Europe, the fiscal position is gradually improving, but the ECB has started the process of scaling back its purchases of sovereign debt, with some expectation these might cease entirely at the end of the year. In Japan, the Bank of Japan is still undertaking very large purchases of Japanese Government debt, which are larger even than the sizeable net issuance to fund Japan’s fiscal deficit.

Meanwhile, there is no expectation of significant reserve accumulation by central banks or sovereign asset managers, which can often take the form of sovereign debt purchases. And financial institutions, which have been significant accumulators of sovereign bonds in recent years as they sought to build their liquidity buffers, are not expected to accrue liquid assets to the same extent again in the foreseeable future.

So the net of all of this is that some of the demand/supply dynamics in sovereign bond markets will be different this year from previous years. For a number of years, central banks purchased duration from the market, but that is in the process of reversing. In that regard, an issue worth thinking about is that the central banks don’t manage their duration risk in their bond holdings at all. Nor do they rebalance their portfolios in response to price changes, unlike most other investors whose actions to rebalance their portfolios back to their benchmarks act as a stabilising influence.

An additional issue worth thinking about is that, through its purchases of mortgage-backed securities, the US Federal Reserve removed much of the uncertainty associated with the early prepayment of mortgages by homeowners by absorbing the impact of prepayments on the maturity profile of its bond portfolio. Private investors typically hedge this risk, and their hedging activity contributes to volatility in interest rates. As the Fed winds down its balance sheet, it is putting this negative convexity risk back in the hands of private investors, and the associated interest rate volatility will return to the market.

Issuance in a Low Rate Environment

To date I have been discussing developments in the rate structure from the perspective of the investor. But it is also interesting to examine how issuers have responded to the historically low rate structure.

Graph 9 shows that many issuers have responded to the low rate structure, and particularly the absence of any material term premium, by lengthening the maturity of their debt, aka “terming out”. Moreover, lower interest rates on their new issuance have resulted in the average duration of their debt rising by even more.

Graph 9

The first two panels show that is true of most sovereigns. The Australian governments, Commonwealth and State, have proceeded along this path. The Australian Office of Financial Management (AOFM) has significantly extended the curve in Australia, by issuing out to a 30-year bond. A number of bonds have been issued well beyond the 10-year maturity, which was the standard end of the yield curve for a number of years. This has also helped state governments to increase the maturity of their issuance.

One interesting exception to the general tendency to term out their debt is the US Treasury, which is undertaking a sizeable amount of issuance at the short end of the curve.

Corporates have also termed out their debt. Some corporates have issued debt with maturities as long as 50 years, which is interesting for at least two reasons. Firstly, a 50-year bond starts to take on more equity-like features. Secondly, many corporates don’t even last 50 years.

The Australian banks have also availed themselves of the opportunity to term out their funding for relatively little cost. The recently implemented Net Stable Funding Ratio (NSFR) further incentivises them to do this. As my colleague Christopher Kent noted a couple of days ago, the average maturity of new issuance of the Australian banks has increased from five years in 2013 to six years currently (Graph 10). As with other issuers, this materially reduces rollover risk. The banks have been able to issue in size at tenors such as seven or ten years that they historically often thought to be unattainable at any reasonable price.

Graph 10

While the low rate structure has often been perceived to be a challenge from the investor point of view, it has been an opportunity for issuers to reduce their rollover risk by extending debt maturities.

Conclusion

The structure of interest rates globally has been at an historically low level for a number of years. This has reflected the aftermath of the financial crisis and the associated monetary policy response. If the global recovery continues to play out as currently anticipated, one would expect that the monetary stimulus will unwind, which would see at least the short-end of yield curves rise.

At the same time, there have been factors behind the low structure of interest rates which are difficult to understand completely and raise questions about its durability. I have discussed some of them here today. In particular, I find it puzzling that there is little compensation for duration in the rate structure. While there are explanations for why interest rates may remain low for a considerable period of time, there is minimal compensation for the uncertainty as to whether or not this will actually occur. At the same time, equity prices embody a view of the future that robust growth can continue without generating a material increase in inflation. Again, there is little priced in for the risk that this may not turn out to be true.

The ongoing improvement in the global economy, together with the fiscal stimulus in the US has caused some investors to question these views. If interest rates continue to rise without a similar rise in expectations about future earnings growth, one would expect to see a repricing of other assets, particularly equity markets. Such a repricing does not necessarily mean a major derailing of the global recovery, indeed it is a consequence of the recovery, but it may have a dampening effect.

The ACCC has instituted proceedings in the Federal Court against credit reporting body, Equifax Pty Ltd (formerly Veda Advantage Pty Ltd), alleging breaches of the Australian Consumer Law (ACL).

The ACCC alleges that from June 2013 to March 2017, Equifax made a range of false or misleading representations to consumers, including that its paid credit reports were more comprehensive than the free reports, when they were not.

Equifax also allegedly represented that consumers had to buy credit reporting packages for it to correct information held about them, or to do so quicker. In fact, Equifax was required by law to take reasonable steps to correct the information in response to a consumer’s request for free.

In addition, the ACCC alleges that Equifax represented that there was a one-off fee for its credit reporting services, when its agreement provided that customer’s subscriptions to the services automatically renewed annually unless the consumer opted out in advance. We allege this renewal term is an unfair contract term, which is void under the ACL.

In all the circumstances, it is alleged that Equifax acted unconscionably in its dealings with vulnerable consumers including by making false or misleading representations, and using unfair tactics and undue pressure when dealing with people in financial hardship.

“We allege that Equifax acted unconscionably in selling its fee-based credit reporting services to vulnerable consumers, who were often in difficult financial circumstances,” ACCC Commissioner Sarah Court said.

“We allege that Equifax told people they needed to buy credit reporting services from them in situations when they did not. It is important for consumers to know they have the legal right to obtain their credit report and to correct any wrong information for free.”

By law, consumers are entitled to access their credit reporting information for free once a year, or if they have applied for, and been refused, credit within the past 90 days, or where the request for access relates to a decision by a credit reporting body or a credit provider to correct information included in the credit report.

One worrying takeaway from the first week of the Financial Services Royal Commission is how many elderly people are being adversely affected by irresponsible lending.

Such lending is often the result of an agreement with a family member, for example an adult child, to help that person financially by entering into a joint loan. These loans are secured against the older person’s home, which is a huge risk if the loan defaults and the older person cannot service the debt.

To ensure that older people contemplating joint loans are aware of the downside of transactions, there needs to be greater access to legal and financial advice prior to the transaction and better training for bank employees and loan officers about responsible lending obligations and the potential “unsuitabilty” of such loans.

Consideration should also be given to larger penalties for banks that provide unsuitable loans to older people.

On the face of it, there are laws that should safeguard elderly consumers from “getting in over their head”.

When a consumer applies for credit, the National Consumer Credit Protection Act obliges a credit provider to make reasonable inquiries about the consumer’s financial situation and their requirements and objectives.

However, the Consumer Action Law Centre says that “it is common that these steps are not adequately followed by lenders”.

Even if these steps are followed, the legislation does not define “substantial hardship”. There is a presumption that if a consumer must sell their principal residence to pay back a loan, this demonstrates substantial hardship.

Emotional lending

Of particular concern is when an older person is persuaded to enter into a joint loan with a third party, such as their son or daughter. These loans are invariably secured by the older person’s property, with the younger person agreeing to pay off the debt.

If the adult child does not pay off the debt, the older person – who is often asset-rich but income-poor – may be unable to service the loan. The older person’s property will be repossessed by the lender, forcing them to relocate, enter the rental market, or even become homeless.

The loans may arise simply because the older person wants to help their adult child through a difficult financial period. It is understandable that a parent would want to help if a business is failing or a child is at risk of losing their house.

But such loans often arise within an atmosphere of crisis (real or exaggerated), in which the adult child pressures the older person into entering into the loan.

In extreme cases, older people have been told that they will be unable to see their grandchildren if they do not enter into loans.

It is not always that the older person is vulnerable per se, but that they are “situationally vulnerable” because of concern for the well-being of a child, or the desire to maintain relationships.

The reality is that it is often difficult for the older person to refuse.

Karen Cox of the Financial Rights Legal Centre noted at the Royal Commission that these loans are:

outright exploitative … elderly persons [are] left in dire circumstances as a result of a loan for which they’ve seen absolutely no benefit.

Similar comments apply to other financial transactions made for the benefit of a third party such as entering into a “reverse mortgage”. This is where the older person takes out a loan against the equity built up in a home (or other asset), with the money given to a child to buy a house or prop up their business.

What could be done?

Advocates are rightly concerned about the financial consequences for older people who enter into such loans. However, the property does belong to the older person and they are entitled to make whatever decisions they want, including risky ones.

Elderly people should be fully informed of their obligations and the potential consequences, should a transaction goes wrong. Banks could lead the way with this.

One initiative would be for the banks to contribute to legal and financial advice for older people, or subsidise the provision of such advice at community legal centres.

Loan assessors and brokers must also be made aware of the risks of such transactions.

The Australian Bankers Association is introducing enhanced measures to address elder financial abuse and the risks associated with such loans should be emphasised.

Finally, the government should consider tougher penalties against credit providers who disregard responsible lending obligations. Presently, if a bank is found to have lent irresponsibly they will simply compensate the consumer for the loss. Meaningful penalties that deter reckless lending should be considered.

Author: Eileen Webb, Professor, Curtin Law School, Curtin University

The opaque pricing of discounts offered on residential mortgage rates makes it difficult for customers to make informed choices and disadvantages borrowers who do not regularly review their choice of lender, a report by the ACCC has found.

The ACCC’s Residential Mortgage Price Inquiry is monitoring the prices charged by the five banks affected by the Government’s Major Bank Levy: Australia and New Zealand Banking Group Limited (ANZ), Commonwealth Bank of Australia (CBA), Macquarie Bank Limited, National Australia Bank Limited (NAB), and Westpac Banking Corporation.

The Inquiry’s interim report, out today, reveals signs of less-than-vigorous price competition, especially between the big four banks.

“We do not often see the big four banks vying to offer borrowers the lowest interest rates. Their pricing behaviour seems more accommodating and consistent with maintaining current positions,” ACCC Chairman Rod Sims said.

“We have seen various references to not wanting to ‘lead the market down’, to have rates that are ‘mid-ranked’ and to ‘maintain orderly market conduct’.”

The ACCC has found that discounts are a major factor in the interest rates customers are paying. Banks offer varying levels of discounts, both advertised and discretionary, but the latter are not always transparent to consumers.

The criteria used by different banks for determining the total discount offered to borrowers includes many factors, such as the individual borrower’s characteristics, their value or potential value to the bank, and their ability to negotiate.

During the two years to June 2017, the average discount across the five banks under review on variable interest rate loans was 78-139 basis points off the relevant headline interest rate.

“The discounting by the big banks lacks transparency and it’s almost impossible for customers to obtain accurate interest rate comparisons without investing a great deal of time and effort. But the potential savings from these discounts are immense,” Mr Sims said.

The report also found the average interest rates paid for basic or ‘no frills’ loans are often higher than for standard loans at the same bank.

“We think many customers who opted for ‘basic’ or ‘no frills’ loans thinking they are saving money would be surprised to learn they might actually be paying more.”

The report’s other key findings include:

existing residential mortgage borrowers paid significantly higher interest rates than new borrowers at the same bank. Between 30 June 2015 and 30 June 2017, existing borrowers on standard variable interest rate residential mortgages at the big four banks were paying up to 32 basis points more (on average) than new borrowers,

the large majority of borrowers are paying lower interest rates than the relevant headline interest rate, and

the bank with the lowest headline rate is not always the bank with the lowest average rate paid by borrowers.

“These findings suggest that many bank customers would likely benefit from either switching mortgage providers, or approaching their bank for a better rate and indicating they are prepared to switch to get one,” Mr Sims said.

“It seems existing customers are not being rewarded for their loyalty; in fact they are worse off. For example on a $375,000 residential mortgage, a new borrower paying an interest rate that was 32 basis points lower would save approximately $1200 in interest over the first year of a loan.”

“This is a significant saving,” Mr Sims said.

In addition to examining the way banks make their mortgage pricing decisions, the ACCC’s Residential Mortgage Pricing Inquiry final report will detail if the banks have adjusted their pricing in response to the Government’s Major Bank Levy.

As at November 2017, the five banks stated no specific decisions had been made to adjust residential mortgage prices in response to the Major Bank Levy.

Indeed, one bank considered whether the costs could be passed on to customers and suppliers at a range of different time periods, including after the end of the ACCC inquiry.

The ACCC’s final report will examine these issues further.

Background

On 9 May 2017 the Treasurer, the Hon. Scott Morrison MP, issued a direction to the ACCC to inquire into prices charged or proposed to be charged by Authorised Deposit-taking Institutions (ADIs) affected by the Major Bank Levy in relation to the provision of residential mortgage products in the banking industry in Australia. The Major Bank Levy came into effect from 1 July 2017, and the Inquiry will consider residential mortgage prices for the period 9 May 2017 until 30 June 2018.

The ACCC’s interim report examines the motivations, influences, and processes behind the residential mortgage pricing decisions of the five banks during the period 1 July 2015 to 30 June 2017.

The ACCC is reporting on this period in order to have a baseline against which to compare pricing decisions for the review period set by the Treasurer.

The ACCC will continue to examine the banks’ mortgage pricing decisions and how they have dealt with the Major Bank Levy through to 30 June 2018.

The ACCC has used its compulsory information gathering powers to obtain documents and data from the five banks on their pricing of residential mortgage products. The ACCC has supplemented its analysis of the documents and data supplied by the five banks with data from the Reserve Bank of Australia (RBA), Australian Prudential Regulation Authority (APRA) and the Australian Bureau of Statistics (ABS).

This inquiry is the first task of the ACCC’s Financial Services Unit (FSU), which was formed as a permanent unit during 2017 following a commitment of continuing funding by the Australian Government in the 2017-18 Budget. Alongside the ACCC’s role in promoting competition in financial services through its enforcement, infrastructure regulation, open banking, and mergers and adjudication work, the FSU will monitor and promote competition in Australia’s financial services sector by assessing competition issues, undertaking market studies, and reporting regularly on emerging issues and trends in the sector.

ASIC has today released a report setting out the details of the changes made by the big four banks to remove unfair terms from their small business loan contracts of up to $1 million.

The report, Unfair contract terms and small business loans (REP 565), provides more detailed guidance to bank and non-bank lenders about compliance with the unfair contract terms laws as they relate to small business.

The report follows the announcement in August 2017 that the big four banks had committed to improving terms of their small business loans following work with ASIC and the Australian Small Business and Family Enterprise Ombudsman (ASBFEO). (See 17-287MR).

ASIC Deputy Chair Peter Kell said, ‘The UCT report provides further guidance to help banks and other lenders ensure that their small business loans are fair, and do not breach the rules prohibiting unfair contract terms.’

The report:

Identifies the types of terms in loan contracts that raise concerns under the law

Provides details about the specific changes that have been made by the banks to ensure compliance with the law

Provides general guidance to lenders with small business borrowers to help them assess whether loan contracts meet the requirements under the unfair contract terms law

‘ASIC will review small business lending contracts across the market. There are no excuses for failure to comply with the UCT laws, and we will consider all regulatory options available to us if we identify lenders whose unfair contracts break the law.’

ASIC will monitor the four banks’ use of the clauses to ensure they are not applied or relied on in an unfair way. ASIC will also examine other lenders’ loan contracts to ensure that their contracts do not contain terms that raise concerns under the unfair contract terms law.

ASIC and ASBFEO will continue work together to ensure small business loan contracts comply with the unfair contract terms law.

Unfair contract terms protections were extended to small business from 12 November 2016.

ASIC and the ASBFEO have been working with the big four banks to ensure their small business loan contracts meet the standards that are required by the unfair contract terms law (refer: 17-139MR).

Small business loans are defined as loans of up to $1 million that are provided in standard form contracts to small businesses employing fewer than 20 staff are covered by the legal protections.

In August 2017, ASIC and the ASBFEO welcomed the changes to small business loan contracts by the big four banks (refer 17-278MR) that have:

Ensured that the contract does not contain ‘entire agreement clauses’ which prevent a small business borrower from relying on statements by bank officers (e.g. about how bank discretions will be exercised)

Limited the operation of broad indemnification clauses

Addressed concerns about event of default clauses, including ‘material adverse change’ events of default and specific events of non-monetary default (e.g. misrepresentations by the borrower)

Limited the circumstances in which financial indicator covenants will be used in small business loans and when breach of a covenant will be considered an event of default

Limited their ability to unilaterally vary contracts to specific circumstances with appropriate advance notice.