The White House and Senate leaders reached a deal early Wednesday morning USA time on a massive stimulus package they hope will keep the nation from falling into a deep recession because of the coronavirus crisis, reports The Hill.

The agreement caps five days of intense negotiations that started Friday morning when Senate Majority Leader Mitch McConnell

(R-Ky.) convened Republican and Democratic colleagues, with talks

stretching late into the evening each of the following four days.

The

revamped Senate proposal will inject approximately $2 trillion into the

economy in the form of tax rebates, four months expanded unemployment

benefits and a slew of business tax-relief provisions. The deal includes

$500 billion for a major corporate loan program through the Federal

Reserve, a $367 billion small business rescue package, $130 billion for

hospitals and $200 billion for other “domestic priorities,” such as

transportation, veterans, child care and seniors.

The

bill will give a one-time check of $1,200 to Americans who make up to

$75,000. Individuals with no or little tax liability would receive the

same amount, unlike the initial GOP proposal that would have given them a

minimum of $600.

“At last we have a

deal. … the Senate has reached a bipartisan agreement,” McConnell

declared during a speech on the Senate floor after 1:30 a.m.

“We are going to pass this legislation later today,” he added.

Hundreds of billions of dollars

in buffer capital for the Treasury Department will allow the Fed to hand

out an additional $4 trillion in loans to distressed companies such as

U.S. airlines and Boeing, the nation’s leading airplane manufacturer.

Their stocks have been hit the hardest in the recent stock-market

selloff that had erased the gains made since President Trump took

office.

The Fed loan program,

which Democrats bashed as a corporate bailout program and Mnuchin’s

“slush fund,” was one of the biggest sticking points during the late

rounds of the negotiations.

Republicans

argued the Treasury Department needed $500 billion to help the Fed

inject enough liquidity into the economy, while Democrats were enraged

over a provision they said would let Mnuchin provide loans and

guarantees and then wait six months before disclosing who got the

assistance.

The S&P 500 Futures was little changed after the news.

This trifecta of risks – uncontaminated medical emergencies, insufficient economic-policy arsenals, and geopolitical white swans – will be enough to tip the global economy into persistent depression and a runaway financial-market meltdown. After the 2008 crash, a forceful (though delayed) response pulled the global economy back from the abyss. We may not be so lucky this time.

From Project Syndicate. The shock to the global economy has been both faster and more severe than the 2008 global financial crisis (GFC) and even the Great Depression. In those two previous episodes, stock markets collapsed by 50% or more, credit markets froze up, massive bankruptcies followed, unemployment rates soared above 10%, and GDP contracted at an annualized rate of 10% or more. But all of this took around three years to play out. In the current crisis, similarly dire macroeconomic and financial outcomes have materialized in three weeks.

Earlier

this month, it took just 15 days for the US stock market to plummet

into bear territory (a 20% decline from its peak) – the fastest such

decline ever. Now, markets are down 35%,

credit markets have seized up, and credit spreads (like those for junk

bonds) have spiked to 2008 levels. Even mainstream financial firms such

as Goldman Sachs, JP Morgan and Morgan Stanley expect

US GDP to fall by an annualized rate of 6% in the first quarter, and by

24% to 30% in the second. US Treasury Secretary Steve Mnuchin has warned that the unemployment rate could skyrocket to above 20% (twice the peak level during the GFC).

In other words, every component of aggregate demand – consumption, capital spending, exports – is in unprecedented free fall. While most self-serving commentators have been anticipating a V-shaped downturn – with output falling sharply for one quarter and then rapidly recovering the next – it should now be clear that the crisis is something else entirely. The contraction that is now underway looks to be neither V- nor U- nor L-shaped (a sharp downturn followed by stagnation). Rather, it looks like an I: a vertical line representing financial markets and the real economy plummeting.

Not

even during the Great Depression and World War II did the bulk of

economic activity literally shut down, as it has in China, the United

States, and Europe today. The best-case

scenario would be a downturn that is more severe than the GFC (in terms

of reduced cumulative global output) but shorter-lived, allowing for a

return to positive growth by the fourth quarter of this year. In that

case, markets would start to recover when the light at the end of the

tunnel appears.

But the best-case scenario assumes several conditions. First, the US, Europe, and other heavily affected economies would need to roll out widespread testing, tracing, and treatment measures, enforced quarantines, and a full-scale lockdown of the type that China has implemented. And, because it could take 18 months for a vaccine to be developed and produced at scale, antivirals and other therapeutics will need to be deployed on a massive scale.

Second,

monetary policymakers – who have already done in less than a month what

took them three years to do after the GFC – must continue to throw the

kitchen sink of unconventional measures at the crisis. That means zero

or negative interest rates; enhanced forward guidance; quantitative

easing; and credit easing (the purchase of private assets) to backstop

banks, non-banks, money market funds, and even large corporations

(commercial paper and corporate bond facilities). The US Federal Reserve

has expanded its cross-border swap lines to address the massive dollar liquidity shortage

in global markets, but we now need more facilities to encourage banks

to lend to illiquid but still-solvent small and medium-size enterprises.Subscribe now

Third,

governments need to deploy massive fiscal stimulus, including through

“helicopter drops” of direct cash disbursements to households. Given the

size of the economic shock, fiscal deficits in advanced economies will

need to increase from 2-3% of GDP to around 10% or more. Only central

governments have balance sheets large and strong enough to prevent the

private sector’s collapse.

But

these deficit-financed interventions must be fully monetized. If they

are financed through standard government debt, interest rates would rise

sharply, and the recovery would be smothered in its cradle. Given the

circumstances, interventions long proposed by leftists of the Modern Monetary Theory school, including helicopter drops, have become mainstream.1

Unfortunately

for the best-case scenario, the public-health response in advanced

economies has fallen far short of what is needed to contain the

pandemic, and the fiscal-policy package currently being debated is

neither large nor rapid enough to create the conditions for a timely

recovery. As such, the risk of a new Great Depression, worse than the

original – a Greater Depression – is rising by the day.

Unless

the pandemic is stopped, economies and markets around the world will

continue their free fall. But even if the pandemic is more or less

contained, overall growth still might not return by the end of 2020.

After all, by then, another virus season is very likely to start with

new mutations; therapeutic interventions that many are counting on may

turn out to be less effective than hoped. So, economies will contract

again and markets will crash again.

Moreover,

the fiscal response could hit a wall if the monetization of massive

deficits starts to produce high inflation, especially if a series of

virus-related negative supply shocks reduces potential growth. And many

countries simply cannot undertake such borrowing in their own currency.

Who will bail out governments, corporations, banks, and households in

emerging markets?

In any case, even if the pandemic and the economic fallout were brought under control, the global economy could still be subject to a number of “white swan” tail risks. With the US presidential election approaching, the crisis will give way to renewed conflicts between the West and at least four revisionist powers: China, Russia, Iran, and North Korea, all of which are already using asymmetric cyberwarfare to undermine the US from within. The inevitable cyber attacks on the US election process may lead to a contested final result, with charges of “rigging” and the possibility of outright violence and civil disorder

Similarly, as I have argued previously, markets are vastly underestimating the risk of a war between the US and Iran this year; the deterioration of Sino-American relations is accelerating as each side blames the other for the scale of the health emergency. The current crisis is likely to accelerate the ongoing balkanization and unraveling of the global economy in the months and years ahead.

First a quick reminder that there is a third party webinar being run tomorrow Thursday. The promoter says there are still spaces. Here is the link. It appears some had issues with completing the registration, but I understand this is now fixed. Contact me via the DFA Blog is you have any issues.

In addition, I will be recording a show with Harry in the next few days, and that will be showing on the DFA channels. If there are questions you would like me to ask, again send them via the DFA Blog.

I caught up with Guy Standing, Professorial Research Associate at SOAS University of London, a Fellow of the British Academy of Social Sciences, and co-founder and now honorary co-president of the Basic Income Earth Network (BIEN), an international NGO that promotes basic income.

His latest and new book is Battling Eight Giants: Basic Income Now.

Today in one the richest countries in the world, 60% of households in poverty have people in jobs, inequality is the highest it has been for 100 years, climate change threatens our extinction and automation means millions are forced into a life of precarity. The solution? Basic Income.

Here, Guy Standing, the leading expert on the concept, explains how to solve the new eight evils of modern life, and all for almost zero net cost. There is a better future, one that makes certain all citizens can share in the wealth of the modern economy. Far from being a new idea, Standing shows how the roots of basic income go back to the Charter of the Forest, one of two foundational documents of the state – the other, sealed on the same day, being the Magna Carta.

His recent books include Basic Income: And How We Can Make It Happen (2017), The Corruption of Capitalism: Why Rentiers Thrive and Work Does Not Pay (2016); with others, Basic Income: A Transformative Policy for India (2015); A Precariat Charter: From Denizens to Citizens (2014); and The Precariat: The New Dangerous Class (2011), which has been translated into 23 languages.

[Note: to comply with YT I edited certain words and replaced them with more generic ones, but did not change the meaning in 5 separate places]. The full non edited version is available via the DFA podcast edition. The link to that will be pinned to the video.

The New Zealand Government, retail banks and the Reserve Bank are today announcing a major financial support package for home owners and businesses affected by the economic impacts of COVID-19.

The package will include a six month principal and interest

payment holiday for mortgage holders and SME customers whose incomes have been

affected by the economic disruption from COVID-19.

The Government and the banks will implement a $6.25 billion

Business Finance Guarantee Scheme for small and medium-sized businesses, to

protect jobs and support the economy through this unprecedented time.

“We are acting quickly to get these schemes in place to

cushion the impact on New Zealanders and businesses from this global pandemic,”

Finance Minister Grant Robertson said.

“These actions between the Government, banks and the Reserve

Bank show how we are all uniting against COVID-19. We will get through this if

we all continue to work together.

“A six-month mortgage holiday for people whose incomes have

been affected by COVID-19 will mean people won’t lose their homes as a result

of the economic disruption caused by this virus,” Grant Robertson said.

The specific details of this initiative are being finalised

and agreed urgently and banks will make these public in the coming days.

The Reserve Bank has agreed to help banks put this in place

with appropriate capital rules. In addition, it has decided to reduce banks

‘core funding ratios’ from 75 percent to 50 percent, further helping banks to

make credit available.

We are announcing this now to give people and businesses the

certainty that we are doing what we can to cushion the blow of COVID-19.

The Business Finance Guarantee Scheme will provide

short-term credit to cushion the financial distress on solvent small and

medium-sized firms affected by the COVID-19 crisis.

This scheme leverages the Crown’s financial strength,

allowing banks to lend to ease the financial stress on solvent firms affected

by the COVID-19 pandemic.

The scheme will include a limit of $500,000 per loan and

will apply to firms with a turnover of between $250,000 and $80 million per

annum. The loans will be for a maximum of three years and expected to be

provided by the banks at competitive, transparent rates.

The Government will carry 80% of the credit risk, with the

other 20% to be carried by the banks.

Reserve Bank Governor Adrian Orr, said: “Banks remain well

capitalised and liquid. They also remain highly connected to New Zealand’s

business sector and almost every household in New Zealand. Their ability to

extend credit to firms to bridge the difficult times created by COVID-19 is

critical and made more possible with today’s announcements. We will monitor

banks’ behaviour over coming months to assess the effectiveness of the

risk-sharing scheme.”

The Government, Reserve Bank and the Treasury continue to

work on further tailor-made support for larger, more complex businesses, Grant

Robertson said.

And so it starts. The latest musings from Australian’s army of economists are beginning to wake up to the grim reality. Reality is not friendly. And the news will likely get worse ahead.

First, Westpac says that the unemployment rate is set to reach 11% by June. The economy is now expected to contract by 3.5% in the June quarter. And a sustained recovery is not expected until Q4.

Just last week they forecast a peak in the unemployment rate of 7%. Since then we got more extensive shutdowns than originally envisaged. Economic disruptions are set to be larger as the government moves to address the enormous health challenge which the nation now faces.

They says that historically, recessions have tended to emanate from investment cycles, particularly those centred on property and building with the initial shock centred on construction. As this recession will hit services much harder, the loss in jobs will be much quicker, but so too can the rebound be much faster, all dependent on how many firms remain solvent.

In usual recessions it is often uncertain whether the economy is in recovery phase whereas the signals around government policy (particularly shutdowns) will be much clearer and households and business will respond.

Their latest forecasts are based on an assessment of the expected impact of the Package on jobs and growth.The two stimulus packages cost a total of $25.8bn in 2019/20 and $36.3bn in 2020/2021.Of that total of $62bn, $22.85bn is allocated to direct payments to the unemployed and social security beneficiaries while $31.9bn is set aside for small business to retain workers.

However small business only receive cash if they retain workers. The subsidy (keeping cash which is withheld from workers for PAYE tax) is only, say, 20–30% of the direct cost of the worker. Given the current hugely challenging outlook for business, the Package will be measured in terms of its success in keeping people in work.

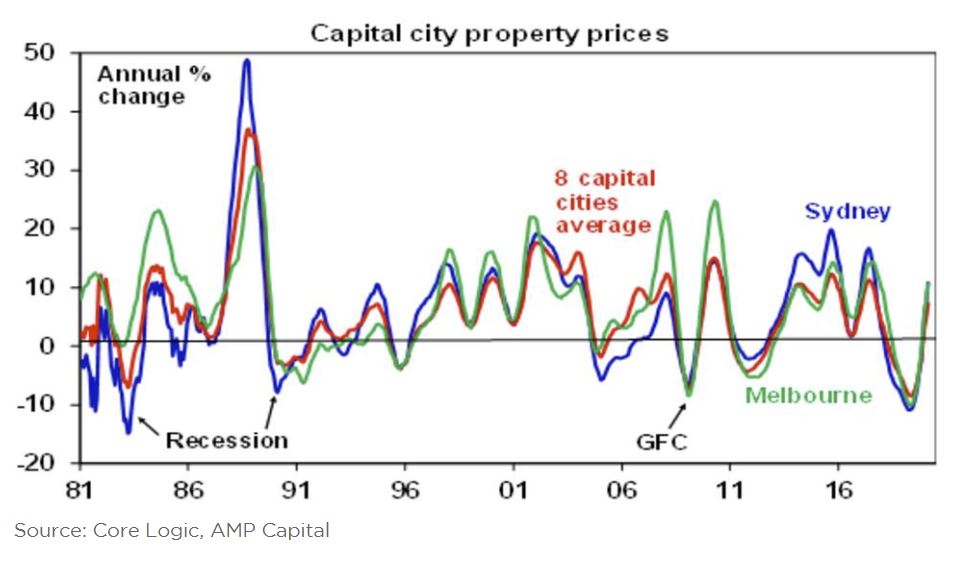

And AMP’s Shane Oliver says:

Auction

clearance rates and sales momentum are showing some signs of slowing

this month. This may reflect an increasing desire on the part of buyers

and sellers to put property transactions on hold to avoid being exposed

to the virus unnecessarily. Social distancing policies will only

intensify this. On its own this may crash transactions but may just

flatten price gains.

However, it’s the likely recession that we

have now entered due to coronavirus related shutdowns that imposes the

big risk. We expect at least two negative quarters of GDP growth in the

March and June quarters with the risk that the September quarter is also

negative. And the contraction could be deep because big chunks of the

economy will be largely shut – tourism, travel, and entertainment with a

severe flow on to parts of retailing. The toilet paper, sanitiser and

canned/frozen food boom may help supermarkets for a while – but as

Deutsche Bank recently calculated for every $1 spent on such items there

is $15 spent on things that are vulnerable to social distancing.

Past large share market falls have seen a

mixed impact on property prices. The 1987 50% share market crash

actually boosted home prices as investors switched from shares to

property. But the key is what happens to unemployment as this often

forces sales and crimps demand. Back in 1987 the economy remained strong

and unemployment fell but the recessions of the early 1980s and early

1990s saw falls in average national capital city home prices of 8.7% and

6.2% respectively as unemployment rose. The GFC share market fall of

55% also saw a 7.6% home price fall, even though it wasn’t a recession,

because unemployment rose from 4% to nearly 6%.

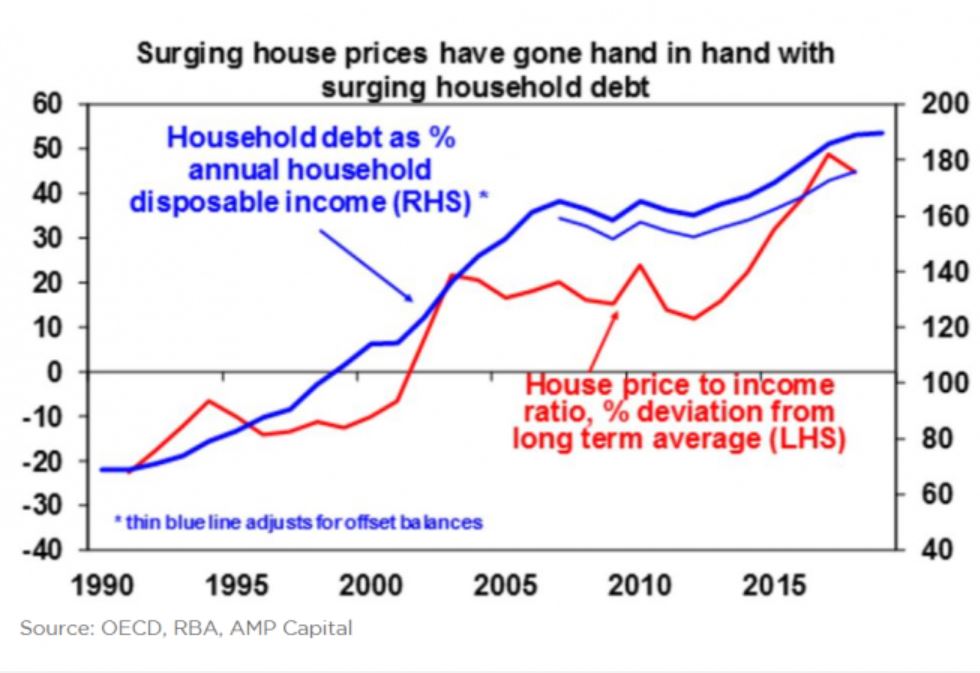

If the recession turns out to be long – pushing unemployment to say 10% or more – then this risks tripping up the underlying vulnerability of the Australian housing market flowing from high household debt levels and high house prices. The surge in prices relative to incomes (and rents) over the last two decades has gone hand in hand with a surge in household debt relative to income that has taken Australia from the low end of OECD countries to the high end.

So he says “we have always concluded that the combination of high prices and debt on their own won’t trigger a major crash in prices unless there are much higher interest rates or a recession. Unfortunately, we are now facing down the barrel of the latter. A sharp rise in unemployment to say 10% or beyond risks resulting in a spike in debt servicing problems, forced sales and sharply falling prices. This could then feedback to weaken the broader economy as falling home prices lead to less spending and a further rise in unemployment and more defaults and so on. This scenario could see prices fall 20% or so”.

Bear in mind though that part of this

would just be a reversal of the 9% bounce in average capital city prices

seen since mid-last year.

It’s also not our base case but it highlights why governments and the RBA really have to work hard to avoid letting the virus cause a lot of company failures, surging unemployment and household defaults.

And Goldman Sachs is still relatively sanguine.

Goldman

Sachs said it was now forecasting a 6 per cent contraction in the

domestic economy in 2020 — the biggest since the 1920s Great Depression —

with unemployment peaking at 8.5 per cent.

On the upside, the strength of Australian

bank balance sheets in terms of funding, liquidity and capital left them

“significantly less vulnerable than compared to any point in the recent

past”.

“Similarly, the source of historic loan

losses for banks — corporate balance sheets — enter this downturn in a

better condition than at any point in the last 40 years, with close to

all-time-low levels of gearing and all-time low debt-servicing ratios,”

Goldman said.

But given the scale of the forecast

contraction, bad debts were now expected to rise significantly to 50bps

of loans and slash bank earnings by 20 per cent.

A hard-landing scenario would wipe out between 50-70 per cent of the sector’s earnings.

International Monetary Fund Managing Director Kristalina Georgieva made the following statement today following a conference call of G20 Finance Ministers and Central Bank Governors:

“The human costs of the Coronavirus pandemic are already

immeasurable and all countries need to work together to protect people and

limit the economic damage. This is a moment for solidarity—which was a major

theme of the meeting today of the G20 Finance Ministers and Central Bank

Governors.

“I emphasized three points in particular:

“First, the outlook for global growth: for 2020 it is negative—a recession at least as bad as during the global financial crisis or worse. But we expect recovery in 2021. To get there, it is paramount to prioritize containment and strengthen health systems—everywhere. The economic impact is and will be severe, but the faster the virus stops, the quicker and stronger the recovery will be.

“We strongly support the extraordinary fiscal actions many

countries have already taken to boost health systems and protect affected

workers and firms. We welcome the moves of major central banks to ease monetary

policy. These bold efforts are not only in the interest of each country, but of

the global economy as a whole. Even more will be needed, especially on the

fiscal front.

“Second, advanced economies are generally in a better

position to respond to the crisis, but many emerging markets and low-income

countries face significant challenges. They are badly affected by outward

capital flows, and domestic activity will be severely impacted as countries

respond to the epidemic. Investors have already removed US$83 billion from

emerging markets since the beginning of the crisis, the largest capital outflow

ever recorded. We are particularly concerned about low-income countries in debt

distress—an issue on which we are working closely with the World Bank.

“Third, what can we, the IMF, do to support our members?

We are concentrating bilateral and multilateral surveillance on this crisis and policy actions to temper its impact.

We will massively step up emergency finance—nearly 80 countries are requesting our help—and we are working closely with the other international financial institutions to provide a strong coordinated response.

We are replenishing the Catastrophe Containment and Relief Trust to help the poorest countries. We welcome the pledges already made and call on others to join.

We stand ready to deploy all our US$1 trillion lending capacity.

And we are looking at other available options. Several low- and middle-income countries have asked the IMF to make an SDR allocation, as we did during the Global Financial Crisis, and we are exploring this option with our membership.

Major central banks have initiated bilateral swap lines with emerging market countries. As a global liquidity crunch takes hold, we need members to provide additional swap lines. Again, we will be exploring with our Executive Board and membership a possible proposal that would help facilitate a broader network of swap lines, including through an IMF-swap type facility.

“These are extraordinary circumstances. Many countries are

already taking unprecedented measures. We at the IMF, working with all our

member countries, will do the same. Let us stand together through this

emergency to support all people across the world.”

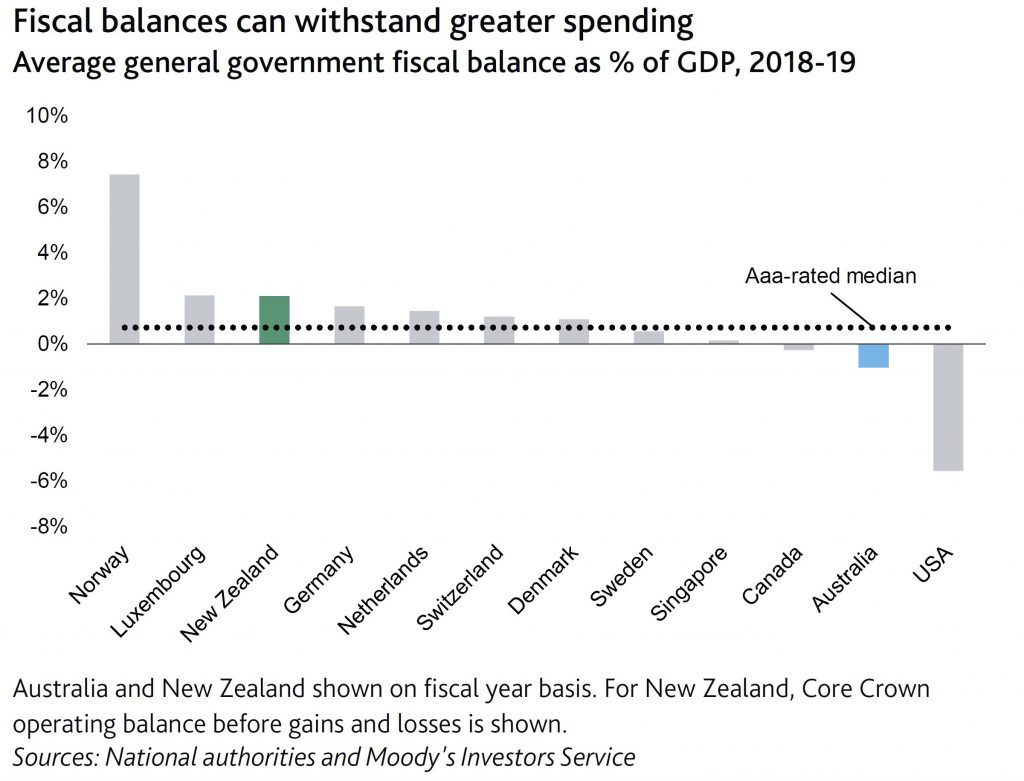

Moody’s says that on 22 March, Australia (Aaa stable) announced economic relief measures, totalling AUD66 billion ($38.2 billion, or around 3% of GDP) in support to households, businesses and guarantees to small and medium-sized enterprises (SMEs), in addition to a package announced previously and a set of measures aimed at supporting credit.

On 17 March, New Zealand (Aaa stable) announced a NZD12.1 billion ($7.3 billion), or 4% of GDP, stimulus package to provide immediate support to the economy and alleviate the disruption caused by the coronavirus outbreak.

Both governments have indicated that they will adopt further measures amid the rapidly deteriorating global economic outlook.

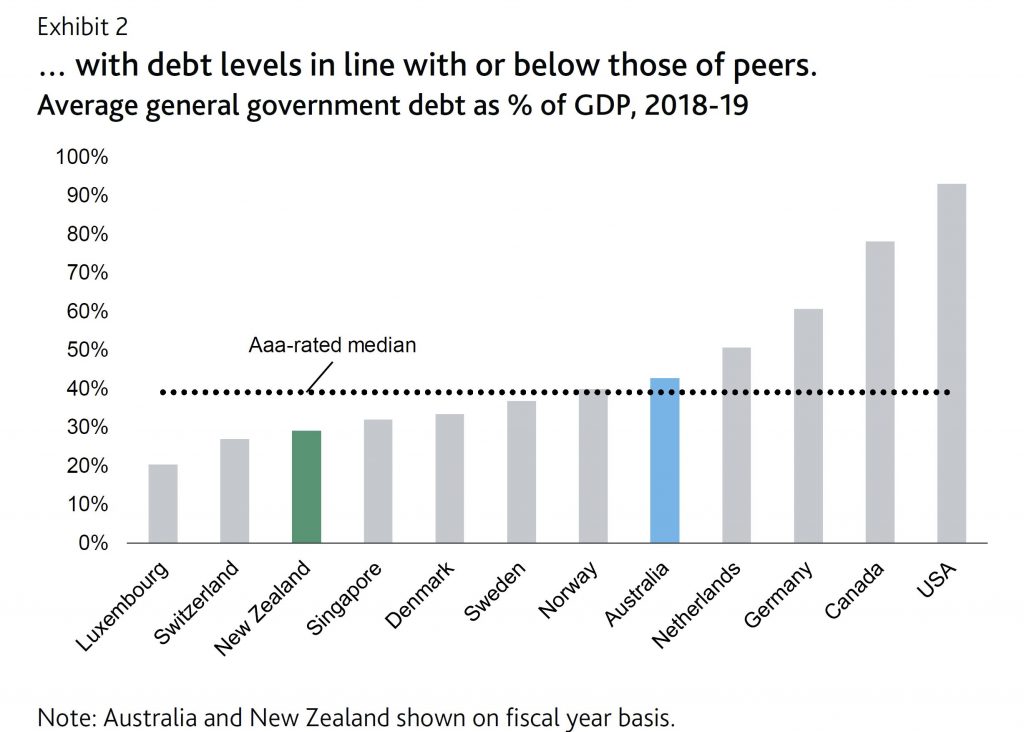

The measures highlight the strong institutional capacity of both Australia and New Zealand to develop emergency fiscal responses during an unprecedented global shock. The measures also demonstrate a high degree of fiscal flexibility that allows for larger near-term budgetary expenditure without threatening longer-term fiscal strength.

In addition to the previously announced AUD17.6 billion support to the economy, the Australian government plans to spend about AUD25 billion in support to businesses in this and the next fiscal year (the fiscal year ends in June), AUD21 billion in support to households and to offer AUD20 billion of guarantees to SMEs. Measures include a boost to SMEs’ cash flow, with upfront payments, temporary relief on creditors’ claims for financially distressed companies, a direct lump-sum payment to individuals and, specifically, to vulnerable households among other measures.

The New Zealand government will spend NZD6 billion by June 2020, as around NZD5.1 billion of the entire package is allocated as wage subsidies for affected businesses in all regions and sectors. The measure aims to stave off a significant deterioration in the labor market. The government has also announced various business tax changes to alleviate businesses’ cash flow pressures and NZD500 million in additional spending on public healthcare, much of which will go on measures that prevent transmission of the coronavirus in the country.

These stimulus packages come in addition to ongoing monetary policy stimulus in both economies. The Reserve Bank of Australia (RBA) has cut its policy rate by 50 basis points so far in March and offered an at least AUD90 billion (0.5% of GDP) special funding facility to commercial banks, which includes an incentive to increase lending to small and medium sized businesses.

The Reserve Bank of New Zealand (RBNZ) delivered an emergency policy rate cut of 75 basis points on 16 March, in addition to announcing a 12- month delay to the increase in bank capital requirements, which it estimates will allow banks additional lending capacity of around NZD47 billion (16% of GDP).

The RBA has also announced a quantitative easing program, aimed at ensuring the yield on three-year government bonds remains around 0.25%, while the RBNZ has left the door open for unconventional monetary policy including largescale asset purchases. {Subsequently Announced].

After accounting for these stimulus packages, Moody’s expects a moderate weakening in both governments’ fiscal positions, with Australia’s surplus turning to a deficit in fiscal 2020. New Zealand plans to fund its stimulus package with increased debt issuance and a drawdown in cash reserves, pushing net debt above the target range of 15%-25% of GDP.

Beyond these measures, weaker revenue growth because of slower economic activity and the triggering of automatic stabilizers will weaken fiscal balances. Moody’s does not view this near-term budgetary expansion by both sovereigns as significantly threatening their fiscal strength. Indeed, it highlights the flexibility and capacity that both governments possess to utilize fiscal policy to support their credit profiles amid an increasingly difficult global economic environment. Particularly for New Zealand, fiscal surpluses and debt levels below Aaa-rated peers provide ample fiscal flexibility

According to the New Daily, Victoria to close schools and NSW is to shut restaurants, and pubs; and cross-border controls will be in place.

Australia is fragmenting as the coronavirus sees state borders closed and premiers embrace sweeping lockdowns.

In

what is confirmation Australians must prepare to face the country’s

most extreme virus safety measures to date, NSW Premier Gladys

Berejiklian has declared non-essential services will shut down within 48

hours.

Victoria also confirmed just

before 3pm Sunday (local time) that schools would shut on Tuesday and

there will be progressive closures of businesses such as pubs and

restaurants.

Schools in NSW will remain

open on Monday, but the premier is likely to make further announcements

on education in the days to come.

ACT

Chief Minister Andrew Barr announced that the territory would follow the

lead of NSW as it was “impossible” to have different arrangements from

the surrounding region.

Victorian

Premier Daniel Andrews made a similar announcement to the NSW premier,

confirming “non-essential” services will be forced to close.

“This is not something that we do lightly,” Mr Andrews said.

“But

it’s clear that if we don’t take this step, more Victorians will

contract coronavirus, our hospitals will be overwhelmed, and more

Victorians will die.”

Supermarkets,

petrol stations, pharmacies, convenience stores, and freight service –

including home delivery of food – will remain open across Victoria and

NSW.

Victorian Premier Daniel Andrews released this statement on Sunday afternoon.

Political

leaders are meeting on Sunday night to consider urgent powers that

would see citizens banned from travelling between suburbs and in between

so-called COVID-19 “red zones”.

“Tonight

I will be informing the National Cabinet that NSW will proceed to a

more comprehensive shutdown of non-essential services,” Ms Berejiklian

said in a statement.

“This will take place over the next 48 hours.”

NSW Health on Sunday confirmed 97 new COVID-19 cases, bringing the state’s tally to 533.

Authorities

have still not been able to work out the source of infection for 46 of

those cases, but they do know those people became infected within

Australia.

The NSW Premier confirmed the strict rules would be rolled out in the next 48 hours.

Victorian

cases jumped by 67 overnight and the government confirmed there had

been outbreaks in regional areas including Warrnambool and the Surf

Coast.

The call to shut down schools goes against the advice from the federal government.

Prime

Minister Scott Morrison persisted with the message for the past week

that the health advice was that it was best to keep children at school.

The call by Mr Andrews makes Victoria the first state to officially close classroom doors to stop the spread of coronavirus.

Children in other nations have already stopped going to school.

The Victorian government said it was bringing forward the school holidays.

It remains to be seen whether the ban on physical class attendance will extend into term two.

Meanwhile,

South Australia has confirmed it will effectively close its borders in a

bid to stop the spread of COVID-19 following an outbreak within a group

of tourists travelling around the Barossa Valley.

Premier

Steven Marshall announced on Sunday that anyone entering the state

would be subject to a mandatory 14-day isolation period.

The measures will take effect from 4pm on Tuesday.

“The

health of South Australians is unquestionably our No.1 priority and

that is why we are acting swiftly and decisively to protect them from

the impact of this disease,” he said.

“We do not make this decision lightly but we have no choice”.

South

Australia’s borders will be monitored 24 hours a day and anyone

entering the state will be forced to sign a declaration agreeing to

self-isolate.

State authorities moved to declare a “major emergency” on Sunday, triggering the shutdown.

But Police Commissioner Grant Stevens admitted authorities were limited in their ability to enforce the isolation orders.

SA Police have been checking on those who have already been ordered to self-isolate after disembarking international flights.

He

said authorities were “relying on people’s community and sense of

goodwill to do the right thing”, and that overwhelmingly people had been

complying with orders.

Similar restrictions have been put in place in Tasmania and the Northern Territory.

In the NT, there are major fears for indigenous communities.