And we discuss an alternative to the Major Banks who are closing outlets to secure profits for shareholders – the Customer Owned Banks. There are nearly 60 across the country focused on their members (customers) offering lower risk, more competitive banking services, including local branches.

You can find a list of local members here: https://www.customerownedbanking.asn.au/about-coba/list-of-our-members

So, I recommend switching to these community banks, away from the Majors. Funnily enough often the COBA banks offer better rates, and service than the others, and have the highest customer satisfaction!

Finally, digital is fine until the power goes out, and cash is still needed to maintain viable and dynamic local communities!

The latest edition of our finance and property news digest with a distinctively Australian flavour.

Go to the Walk The World Universe at https://walktheworld.com.au/

AUSTRALIA’S banking regulator APRA is picking and choosing which banks it is allowing to get away with breaking the law by misreporting whether their sites offer cash service provided by a teller according to an important article in The Regional. Kudos once again to Dale Webster for highlighting this important issue.

Errors in hundreds of minor and foreign bank sites included in the Australian Prudential Regulation Authority’s points of presence data for years, even decades, have been corrected over the past 17 months after being exposed by The Regional in May 2021.

In today’s show we look at the latest inquiry into Banking, which is looking at how regional areas in Australia are and should be supported. Whilst the short-hand answer might appear to be go on-line, the truth is connectivity in many areas is still shaky, some services still need face to face interaction, yet banks are shutting branches and removing ATMs, in an attempt to drive down costs. There has been a 24 per cent fall in regional bank branches over the last four years, and this does not count the increasing number only open for a few hours a week.

You can make a submission for the next month or so. https://treasury.gov.au/consultation/c2021-222961

I discuss with Robbie Barwick from The Citizens Party.

I discuss the latest developments on the Senate Inquiry into Australia Post with Robbie Barwick from the Citizens Party. Time to make a submission and show how important the future of the network is for Australia. This is way more than an issue of watches…

Nonbank online lenders are becoming more mainstream alternative providers of financing to small businesses. In 2018, nearly one-third of small business owners seeking credit reported having applied at a nonbank online lender. The industry’s growing reach has the potential to expand access to credit for small firms, but also raises concerns about how product costs and features are disclosed. The report’s analysis of a sampling of online content finds significant variation in the amount of upfront information provided, especially on costs. On some sites, descriptions feature little or no information about the actual products or about rates, fees, and repayment terms. Lenders that offer term loans are likely to show costs as an annual rate, while others convey costs using terminology that may be unfamiliar to prospective borrowers. Details on interest rates, if shown, are most often found in footnotes, fine print, or frequently asked questions.

The report’s findings build on prior work,

including two rounds of focus groups with small business owners who

reported challenges with the lack of standardization in product

descriptions and with understanding product terms and costs.

In addition, the report finds that a number of websites require prospective borrowers to furnish information about themselves and their businesses in order to obtain details about product costs and terms. Lenders’ policies permit any data provided by the small business owner to be used by the lender and other third parties to contact business owners, often leading to bothersome sales calls. Moreover, online lenders make frequent use of trackers to monitor visitors on their websites. Even when visitors do not share identifying information with the lender, embedded trackers may collect data on how they navigate the website as well as other sites visited.

Bank of Ireland has caved in to public pressure following a public outcry over its plans to heavily restrict cash transactions in its branches, via Irish Independent.

The bank came in for sustained criticism

after the Irish Independent revealed yesterday that it plans to restrict

over-the-counter cash withdrawals to a minimum of €700 and cash

lodgements to a minimum of €3,000 in an effort to push customers towards

using ATMs and self-service machines.

However, after criticism from Finance

Minister Michael Noonan, as well as groups representing consumers,

farmers, older people, rural dwellers and bank workers, the bank

conceded that what it called “vulnerable” customers could continue to

get cash and make withdrawals of smaller amounts of money at branch

counters.

The changes prompted fears of a renewed

bout of bank branch closures and staff lay-offs in the wake of the

bank’s move to severely restrict counter-based cash transactions.

Mr Noonan described the changes as

“surprising and unnecessary”, adding that he expects the bank to “fully

honour” its commitment to “vulnerable customers”.

Bank of Ireland said it would continue to

allow older customers and those unfamiliar with technology to make cash

transactions over the counter.

“Bank of Ireland would like to confirm

that vulnerable customers, together with those elderly customers who are

not comfortable using self-service channels or other technology

solutions, will be assisted by branch staff to use the available

in-branch services.”

However, other banks are now expected to

follow the lead of Bank of Ireland by moving to set strict limits on

over-the-counter cash handling.

It comes after around 200 bank branches

were closed, mainly in rural areas, during the financial collapse, with

at least 10,000 retail bank staff laid-off.

Banks including Bank of Scotland, Danske, ACC and Irish Nationwide have already closed, limiting banking options for customers.

Now there are concerns that the move by

Bank of Ireland to effectively become a cashless bank will prompt more

branch shut-downs and redundancies.

Deputy chairman of the Consumers

Association Michael Kilcoyne said other banks were set to mirror Bank of

Ireland and discourage customers from withdrawing and lodging cash over

the counter.

This would make branches in rural areas less viable, he warned.

“The implications of the Bank of Ireland

move are very severe. If it gets away with this it will get rid of more

staff and close branches.

“This will be a further blow for rural Ireland,” he said.

Mr Kilcoyne predicted that AIB, Ulster Bank and Permanent TSB would make similar moves to curtail cash handling.

And banking union IBOA said it is seeking a

meeting with Bank of Ireland boss Richie Boucher over concerns the

changes would mean more job losses.

The Irish Farmers’ Association said the

changes would cause great difficulty for some farmers who are not

familiar with the bank’s online system.

Age Action accused the bank of ignoring the needs of older people by setting high limits on over-the-counter transactions.

As we discussed this week, the writing is on the wall for bank branches, and more will be closed in the months ahead as the digital revolution continues. You can read our latest research in our “Quiet Revolution” report.

Bankwest announced the closure of a significant number of branches on the east coast, as discussed in this segment.

In it, they argue that digital technology could be harnessed within the branch to enhance customer experience there, and that there is still a role for bank real estate. We are less convinced, as in Australia at least, the digital revolution is well advanced, and brokers provide an alternative face to face sales channel. But in-branch tech may give branches some extra utility, for a short while.

Far from rendering the bank branch obsolete, digital technology holds the key to the branch of the future.

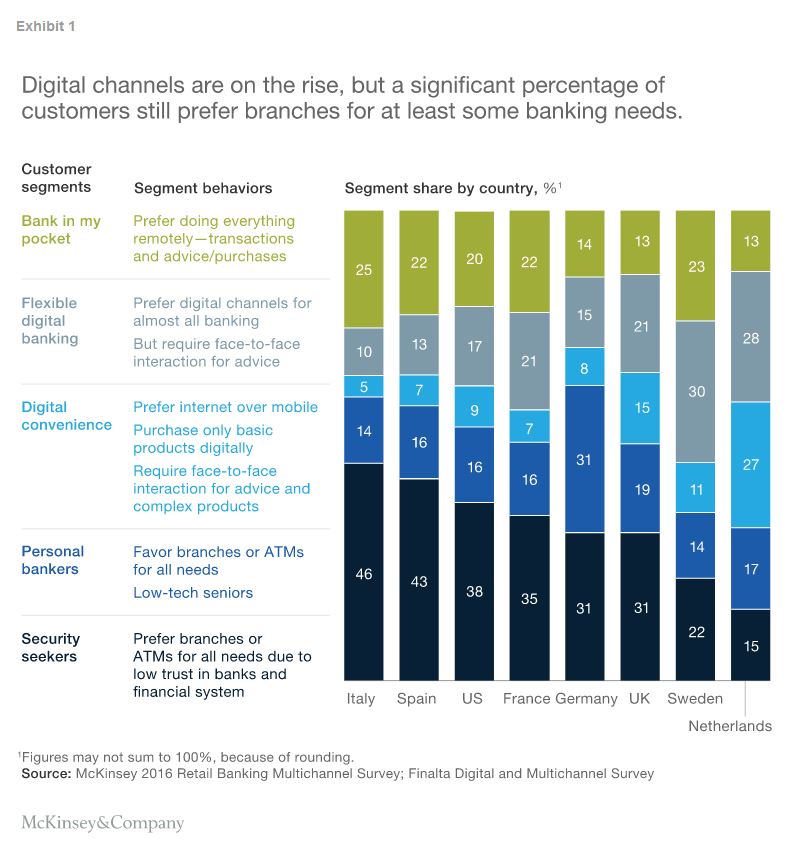

The bank branch as we know it, with tellers behind windows and bankers huddled in cubicles with desktop computers, needs reinvention. Most customers now carry a bank in their pockets in the form of a smartphone and only visit an actual branch to get cash or, occasionally, advice. Globally, financial institutions now process far more transactions digitally than in branches, and since the financial crisis of the late 2000s, more than 10,000 US bank branches have closed—an average of three a day.1

Despite such systemic changes, branches remain an essential part of banks’ operations and customer-advisory functions. Brick-and-mortar locations are still one of the leading sales channels. Even in digitally advanced European nations, between 30 and 60 percent of customers prefer doing at least some of their banking at branches, according to McKinsey research.

Changing customer behavior and the emergence of new technologies spell not the end of the branch but rather the advent of the “smart branch.” Smart branches use technology to boost sales and improve customer experience significantly. When done right, applying the concept transforms the way a bank branch operates (reduced staffing), significantly lowers real-estate requirements, and alters customer interaction (targeted, relevant sales and service-to-sales programs)—with a resulting 60 to 70 percent improvement in branch effectiveness, as measured by cost savings and increased sales.

Our research shows that although many banks have started to adopt elements of the smart-branch model, most are not extracting the full value potential. Making branches smart is not a matter of simply installing new machines or buying a suite of tablet computers. Smart-branch transformation builds on three pillars: the seamless integration of cutting-edge branch technology, which has become cheaper, more reliable, and more accessible; the adoption of radically new, teller- and desk-free branch formats at every location; and the use of digital technology and advanced analytics to improve the operating model in branches, including personalized, data-driven sales and real-time performance management and skill development.

Bankwest has announced it would close selected east coast branches, as it prioritises its investment in digital and broker/third-party offerings to meet changing customer needs.

There should be no surprise, as we foreshadowed the demise of the branch in our most recent edition of our report “The Quiet Revolution“. We said:

Our research shows that consumers have largely migrated into the digital world and have a strong expectation that existing banking services will be delivered via mobile devices and new enhanced services will be extended to them. Even “Digital Luddites”, the least willing to migrate are nevertheless finally moving into the digital domain. Now the gap between expectation and reality is larger than ever.

This is certainly not a cost reduction exercise, although the reduction in branch footprint, which we already see as 10% of outlets have closed in the past 2 years, does offer the opportunity to reduce the running costs of the physical infrastructure.

29 branches will close over a three-week period from 17 August, concentrating Bankwest’s east coast footprint into 14 key branches.

Impacted customers are being informed of the closures and will receive guidance on alternative banking options available to them by email, letters and store signage.

Closures will affect about 200 colleagues and Bankwest is placing a priority on supporting these people over the coming weeks.

The move is the latest step in Bankwest’s strategic refocus (announced March 2017) on evolving and improving its offering to retail and small business customers nationwide.

Managing Director Rowan Munchenberg said rapid changes in the digital space required Bankwest to make important decisions on where to invest to deliver great value for customers and grow nationally.

“Many people still value face-to-face interactions, but customers increasingly expect seamless self-service options that allow them to do their banking when and where they choose,” he said.

“We’re seeing a consistent trend of customers choosing mobile banking over in-branch options for their transaction needs, with an 88 per cent rise in app logins over the past three years.

“So, we’re transforming our organisation to respond more rapidly to these changing customer needs by adopting new ways of working and embracing new technologies.

“But we know we can’t match the major banks’ nation-wide footprint and also deliver world class digital services, so we will prioritise digital channels and broker relationships.

“This change does not impact Western Australia, where our strong brand and established footprint enables us to maintain highly competitive branch and digital offerings.”

Mr Munchenberg said the change had been a difficult decision, given a significant number of east coast colleagues would be affected.

“We will work with and support impacted colleagues in the coming weeks, doing what we can to help them identify other opportunities, be they within or outside of the Group,” he said.

“We are writing to affected customers to outline options, such as using Australia Post’s Bank@Post services and, for business customers, taking advantage of CBA branches.

“Ultimately, this change means we can provide better services to more customers in the future.”

Expect more branch closures in the months ahead as the revolution continues….

I discussed the future of ATMs with Neil Mitchell on 3AW following the banks’ removal of withdrawal fees last year. Now many banks are removing these devices as usage falls, but should they have a social obligation (in the light of the Royal Commission)?