Since our last episode, the crisis in Greece has escalated further. Negotiations between the government and its creditors collapsed over the weekend, and restrictions on bank withdrawals will now follow.

The next step is for the government to issue the equivalent of IOUs to pay salaries and pensions. The country is seemingly on the slippery slope to exiting the euro.

Many of us doubted that it would come to this. In particular, I doubted that it would come to this.

Nearly a decade ago, I analyzed scenarios for a country leaving the eurozone. I concluded that this was exceedingly unlikely to happen. The probability of a Grexit, or any Otherexit, I confidently asserted, was vanishingly small.

My friend and UC Berkeley colleague Brad DeLong regularly reminds us of the need to “mark our views to market.” So where did this prediction go wrong?

Why a euro exit didn’t make sense

My analysis was based on a comparison of economic costs and benefits of a country exiting the euro. The costs, I concluded, would be severe and heavily front-loaded.

Raising the possibility, however remote, of exit from the euro would ignite a bank run in said country. The authorities would be forced to shutter the financial system. Economic activity would grind to a halt. Losing access to not just their savings but also imported petrol, medicines and foodstuffs, angry citizens would take to the streets.

Not only would any subsequent benefits, by comparison, be delayed, but they would be disappointingly small.

With the government printing money to finance its spending, inflation would accelerate, and any improvement in export competitiveness due to depreciation of the newly reintroduced national currency would prove ephemeral.

In Greece’s case, moreover, there is the problem that the country’s leading export, refined petroleum, is priced in dollars and relies on imported oil, which is also priced in dollars. So much for the advantages of a depreciated currency.

Agricultural exports for their part will take several harvests to ramp up. And attracting more tourists won’t be easy against a drumbeat of political unrest.

What went wrong?

How did Greece end up in this pickle? Some say that the specter of a bank run was no longer a deterrent to exit once that bank run started anyway due to the deep depression into which the Greek economy had sunk.

But what is remarkable is how the so-called bank run remained a jog – it was still perfectly manageable until the Greek government called its referendum on the terms of the bail out deal offered by international creditors, negotiations broke down and exit became a real possibility.

Nonperforming loans — ones that are in default or close to it — were already rising, to be sure, but the banks still had all the liquidity they needed. The European Central Bank supported the Greek banking system with emergency liquidity assistance (ELA) right up to the very end of June. Only when Greece stopped negotiating did the Central Bank stop increasing ELA. And only then did a full-fledged bank run break out.

So I stand by the economic argument. Where I need to mark my views to market, however, is for underestimating the role of politics. In particular, I underestimated the extent of political incompetence – not just of the Greek government but even more so of its creditors.

In January Syriza had run on a platform of no more spending cuts or tax increases but also of keeping the euro. It should have anticipated that some compromise would be needed to square this circle. In the event, that realization was strangely late in coming.

And Prime Minister Alexis Tsipras and his government should have had the courage of its convictions. If it was unwilling to accept the creditors’ final offer, then it should have stated its refusal, pure and simple. If it preferred to continue negotiating, then it should have continued negotiating. The decision to call a referendum in midstream only heightened uncertainty. It was a transparent effort to evade responsibility. It was the action of leaders more interested in retaining office than in minimizing the cost to the country of the crisis.

A hard lesson learned

Still, this incompetence pales in comparison with that of the European Commission, the ECB and the IMF.

The three institutions opposed debt restructuring in 2010 when the crisis still could have been resolved at low cost. They continued to resist it in 2015, when a debt write-down was the obvious concession to Mr Tsipras & Company. The cost would have been small. Pretending instead that Greece’s debts could be repaid hardly enhanced their credibility.

Instead, the creditors first calculated the size of the primary budget surpluses that Greece would have to run in order to hypothetically repay its debt. They then required the government to raise taxes and cut spending sufficiently to produce those surpluses.

They ignored the fact that, in so doing, they consigned the country to an even deeper depression. By privileging their own balance sheets, they got the Greek government and the outcome they deserved.

The implication is clear. Never underestimate the ability of politicians to do the wrong thing. I will try to remember next time.

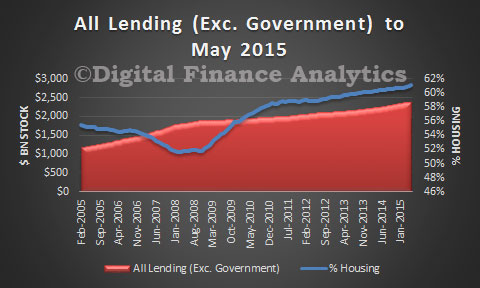

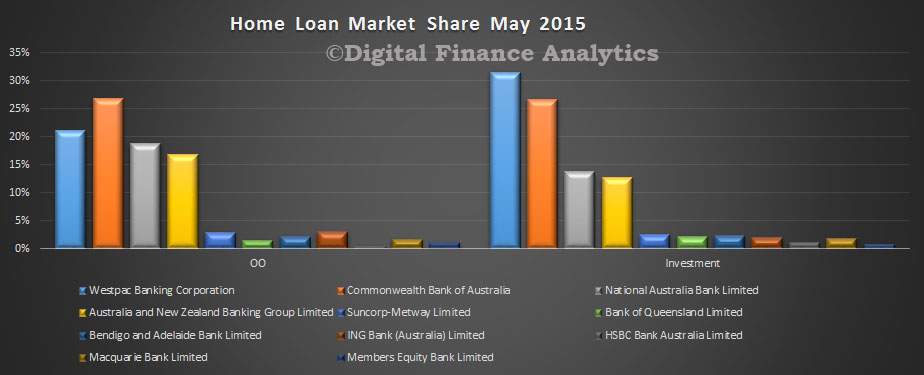

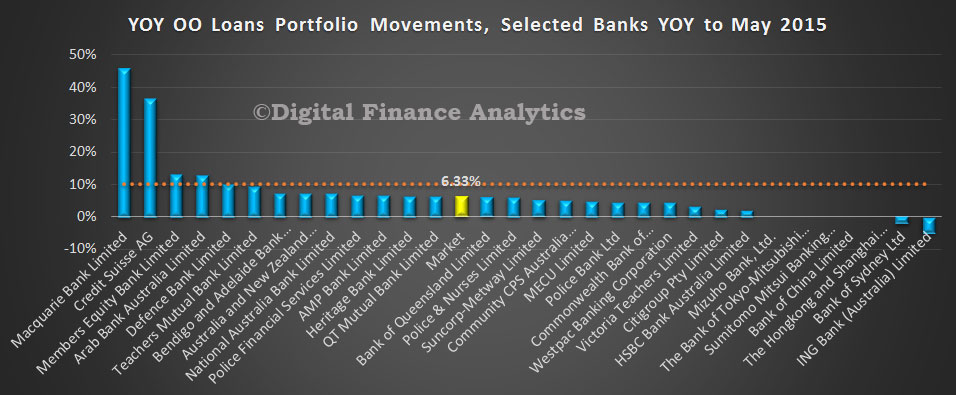

More detailed portfolio analysis shows that ANZ and NAB have been more aggressive on owner occupied loan growth than the other majors, but some of the smaller players are still making hay; Macquarie and Members Equity in particular.

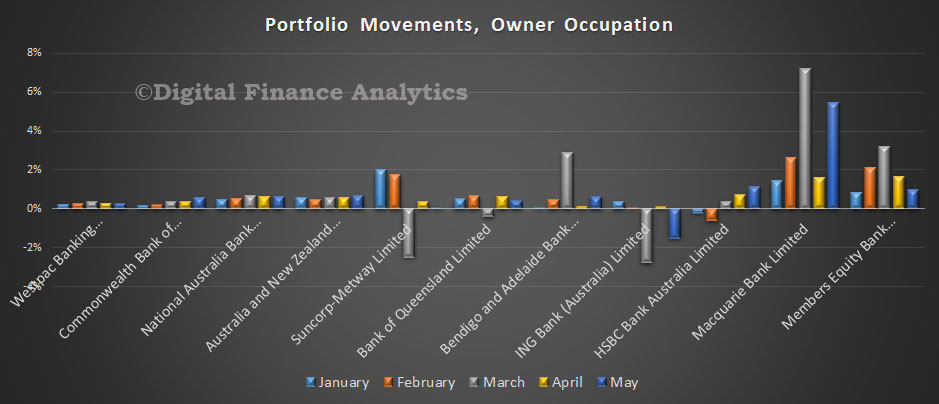

More detailed portfolio analysis shows that ANZ and NAB have been more aggressive on owner occupied loan growth than the other majors, but some of the smaller players are still making hay; Macquarie and Members Equity in particular. The average growth rate over the last 12 months was 6.33%, and we see many players below this, and ING’s portfolio share falling.

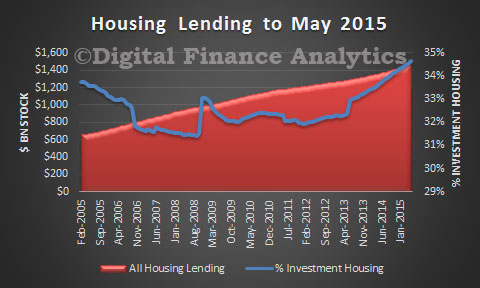

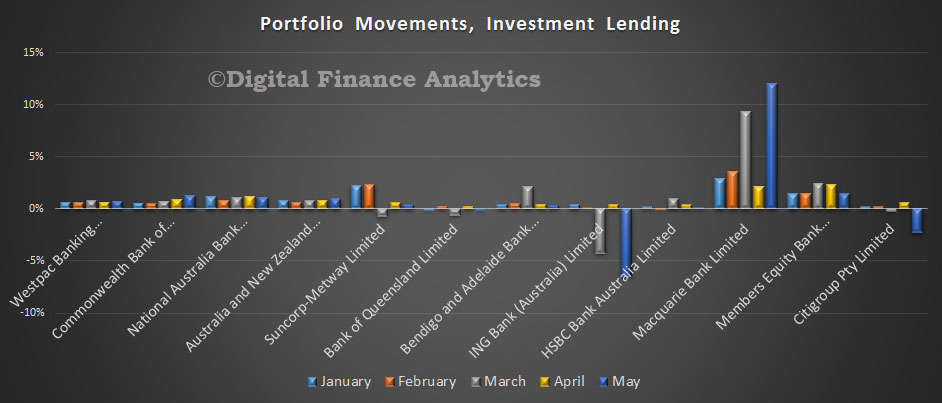

The average growth rate over the last 12 months was 6.33%, and we see many players below this, and ING’s portfolio share falling. Turning to portfolio movements on investment loans, Westpac has slowed their growth relative to the other majors, and Macquarie is still lending hard.

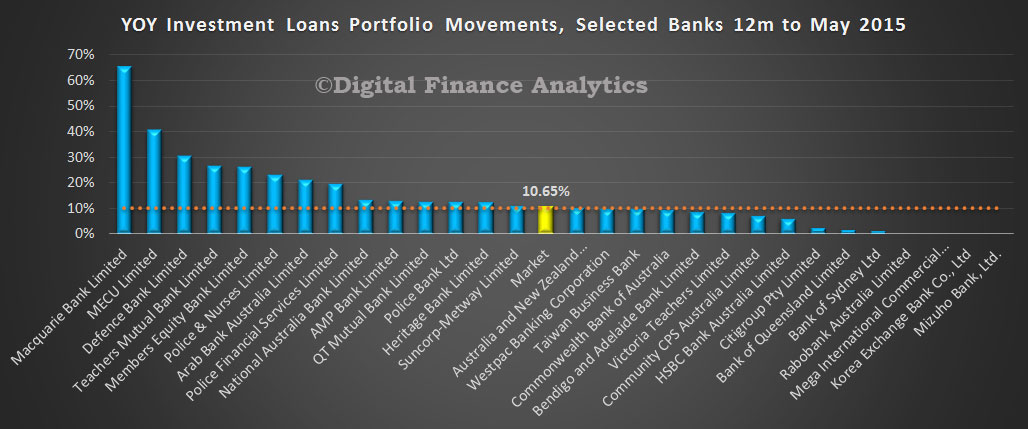

Turning to portfolio movements on investment loans, Westpac has slowed their growth relative to the other majors, and Macquarie is still lending hard. The market average growth over the past year was 10.65%, above the 10% APRA “alert” level. Some of the smaller players are well above (and we think APRA was concerned about some of these players and their rapid growth). We also see several of the majors above the threshold and they might expect to receive a “please explain” letter from the regulator. That said, no-one is clear on when the 10% hurdle should be measured from, so they might have until December to get into line. If they do, they would be required to slow their growth in coming months. There are some signs of discounts falling and LVR thresholds lowering. The regulatory noose may be tightening, but so far to little effect.

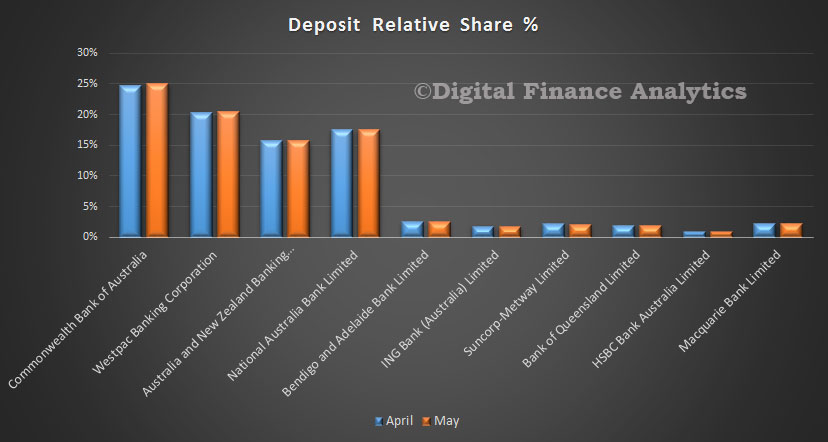

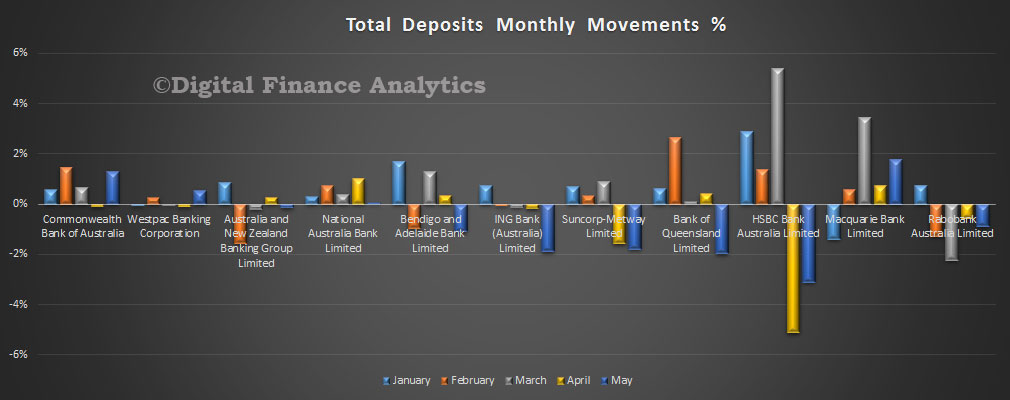

The market average growth over the past year was 10.65%, above the 10% APRA “alert” level. Some of the smaller players are well above (and we think APRA was concerned about some of these players and their rapid growth). We also see several of the majors above the threshold and they might expect to receive a “please explain” letter from the regulator. That said, no-one is clear on when the 10% hurdle should be measured from, so they might have until December to get into line. If they do, they would be required to slow their growth in coming months. There are some signs of discounts falling and LVR thresholds lowering. The regulatory noose may be tightening, but so far to little effect. Turning to deposits, we saw growth of 0.04% to $1,83 trillion.

Turning to deposits, we saw growth of 0.04% to $1,83 trillion. CBA picked up share a little at the expense of some of the smaller lenders, including ING, Bendigo, Suncorp, Bank of Queensland and Rabobank. Many of the smaller players have cut their deposit rates harder to “manage” profitability (i.e. squeeze savers).

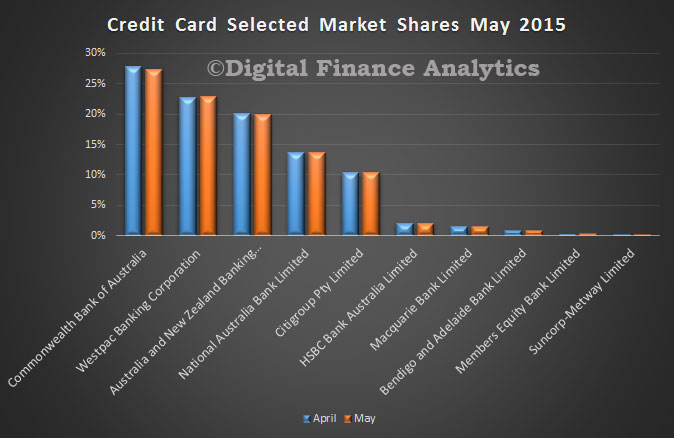

CBA picked up share a little at the expense of some of the smaller lenders, including ING, Bendigo, Suncorp, Bank of Queensland and Rabobank. Many of the smaller players have cut their deposit rates harder to “manage” profitability (i.e. squeeze savers). Finally, credit cards, total borrowing fell 0.38% in the month, to $41.2 billion. Little overall change in position, though we note CBA lost a little share, whilst Westpac gained slightly. The current focus on card interest rates may have an impact in coming months, but little impact so far.

Finally, credit cards, total borrowing fell 0.38% in the month, to $41.2 billion. Little overall change in position, though we note CBA lost a little share, whilst Westpac gained slightly. The current focus on card interest rates may have an impact in coming months, but little impact so far.