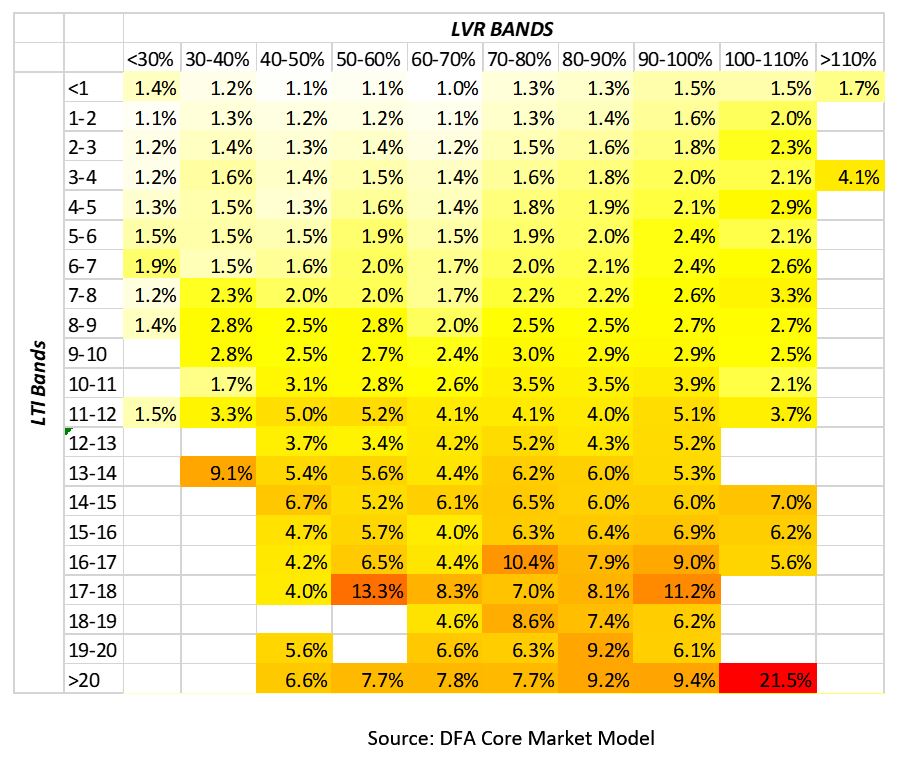

Traditional thinking is that higher loan to value loans are more risky than lower loan to value loans. We see this in the way banks price in risk, through their underwriting standards, and Lenders Mortgage Insurer premiums rise as LVR rises.

However, portfolio analysis from our core market model shows this is a myopic view of risk. When we run our weekly updates of the model we market to market property values, and also update incomes and mortgage payments to take account of changes.

In a rising market, LVR’s tend to improve, because the value of the property rises, creating capital which can insulate the lender in a case of default.

Loan to income metrics give a much more accurate calibration of risk, as we see mortgage stress rising significantly in line with higher LTI measures. In the current environment debt servicing ratios are also important, as mortgage rates are on the rise as incomes are only growing for some, whilst costs of living are rising.

So, here is a (pretty) chart which shows our take on risk of default across LVR and LTI metrics. LTI gives a better read on risk, and in fact the matrix of the two dimensions offers the most accurate calibration.

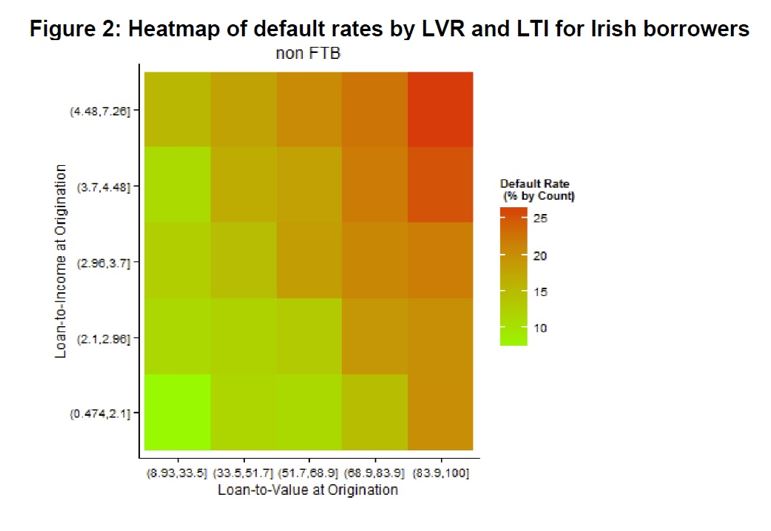

Interestingly, similar conclusions were cited by the Bank of England recently, using data from Irish borrowers after the GFC.

Interestingly, similar conclusions were cited by the Bank of England recently, using data from Irish borrowers after the GFC.

One thought on “Where Are The Mortgage Risks Lurking?”