Today we discuss some specific and concerning research we have completed on interest-only loans. Less than half of current borrowers have complete plans as to how to repay the principle amount.

Interest-only loans may seem like a convenient way to reduce monthly repayments, (and keep the interest charges as high as possible as a tax hedge), but at some time the chickens have to come home to roost, and the capital amount will need to be repaid.

Many loans are set on an interest-only basis for a set 5 year term, at which point the lender is required to reassess the loan and to determine whether it should be rolled on the same basis. Indeed the recent APRA guidelines contained some explicit guidance:

For interest-only loans, APRA expects ADIs to assess the ability of the borrower to meet future repayments on a principal and interest basis for the specific term over which the principal and interest repayments apply, excluding the interest-only period

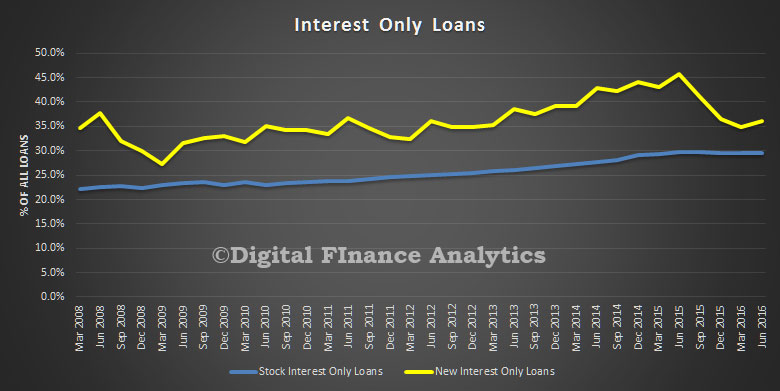

This is important because the number of interest-only loans is rising again. Here is APRA data showing that about one quarter of all loans on the books of the banks are interest-only, and that recently, after a fall, the number of new interest-only loans is on the rise – around 35% – from a peak of 40% in mid 2015. There is a strong correlation between interest-only and investment mortgages, so they tend to grow together. Worth reading the recent ASIC commentary on broker originated interest-only loans.

But what is happening at the coal face? To find out we included some specific questions in our household survey, and today we present the results.

But what is happening at the coal face? To find out we included some specific questions in our household survey, and today we present the results.

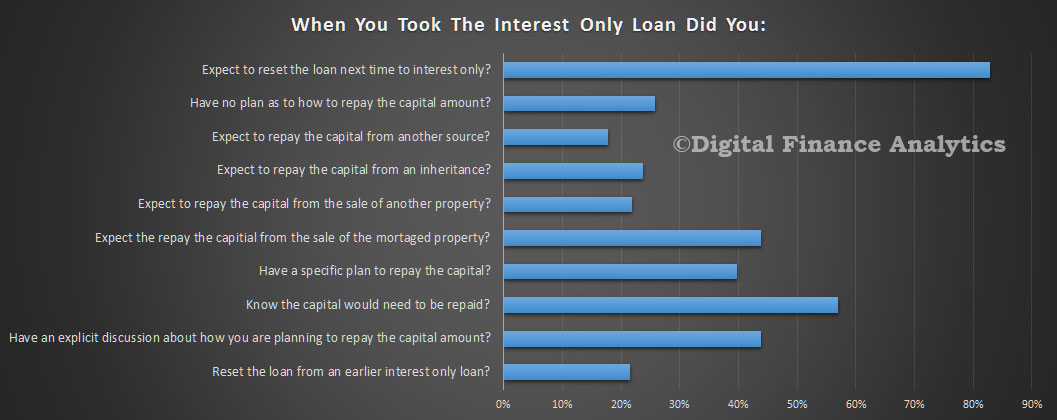

We were surprised to find that around 83% of existing interest-only loan holders expect to roll their loan to another interest-only loan, and to keep doing so. More concerning, only around 44% of borrowing households had an explicit discussion with the lender (or broker) at their last loan draw down or reset about how they plan to repay the capital amount outstanding. Some of these loans are a few years old.

Around 57% said they knew the capital would have to be repaid (we assume the rest were just expecting to roll the loan again) and 26% had no firm plans as to how to repay whereas 39% had an explicit plan to repay.

Around 57% said they knew the capital would have to be repaid (we assume the rest were just expecting to roll the loan again) and 26% had no firm plans as to how to repay whereas 39% had an explicit plan to repay.

Many were expecting to close the loan out from the sale of the property (thanks to capital appreciation) at some point, from the sale of another property, or from another source, including an inheritance.

Thus we conclude there is a potential trap waiting for those with interest-only loans. They need a clear plan to repay, at some point. It also highlights that the quality of the conversation between borrower and lender is not up to scratch.

We think some borrowers on an interest-only loan may get a rude shock, when next they try to roll their interest-only loan. If they do not have a clear repayment plan, they may not get a new loan. There is a debt trap laid for the unwary and the APRA guidelines have made this more likely.

Next time we will delve further into the interest only mortgage landscape, because we found the policies of the lenders varied considerably.

4 thoughts on “The Interest-Only Loan Debt Trap”