The June 2016 finance data released by the ABS today underscores the fundamental in-balances in bank lending, and signals the underlying issues and risks in the economy.

Looking at the trend series of lending flows, we see that overall lending fell in the month by 1.21% compared with last month, or $819 million, and continues the fall in overall lending flows since March 2015. Remember the trend series irons out the monthly variations.

Looking at the trend series of lending flows, we see that overall lending fell in the month by 1.21% compared with last month, or $819 million, and continues the fall in overall lending flows since March 2015. Remember the trend series irons out the monthly variations.

But, if we look across the series, secured lending for owner occupied housing, rose 0.17% or $34 million, whilst secured housing alterations and additions fell 0.59% or $2 million. Personal credit fixed loans rose 0.81% or 35 million, whilst revolving personal credit fell 0.43% or 12 million.

Business lending is split into loans for investment housing, which rose 0.77% or 88 million, whilst lending for other commercial purposes fell by 3.26% or $617 million. Revolving business lending fell 3.82% or $330 million. Overall business lending, including for housing fell 2.21% or 859 million.

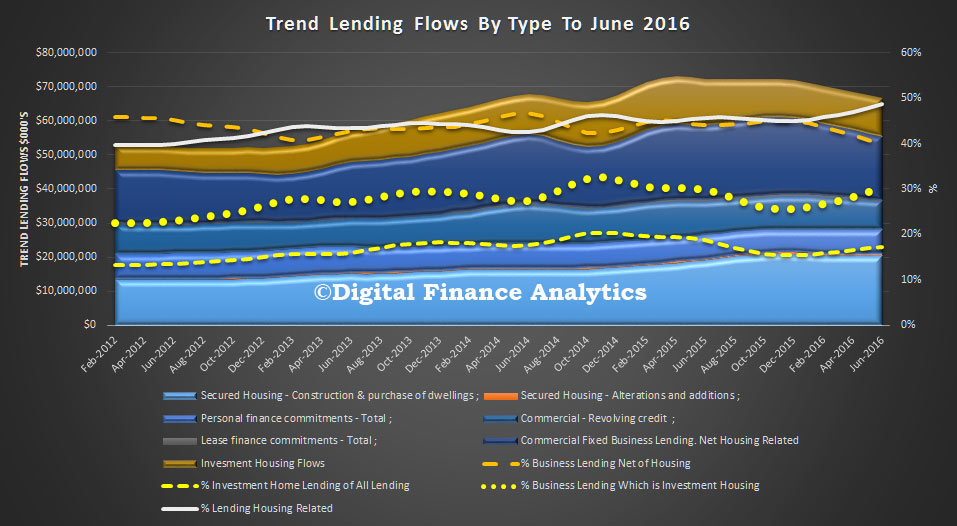

Then, look at the various ratios, as calculated from the chart above. More than 30% of all business lending was for investment housing, this is the highest in more than a year. Overall the banks lent 48.6% of their flows to housing related borrowing across the board, this has never been higher. The percentage of lending to business net of housing lending was down to 39.9%, significantly lower than ever before, even taking into account the period around the GFC, and investment housing related lending rose to 17.2% of all lending flows, compared with 12% in 2008.

This continues to be a worryingly myopic approach to building sustainable economic growth. Businesses are unwilling or unable to investment in growth related programmes, and banks prefer to lending to the “safe as houses” property sector.

Two points to make. First, real growth, sustainable growth, has to come from real productive investments, not just more housing which pumps up home prices and bank balance sheets, and makes households feel a little more wealthy (actually more “in hoc” to ever bigger banks).

Second, putting all the eggs in the housing basket simply exposes more to risk, should home prices begin to correct toward their long term values – values which are currently on average 25-30% above where they should be.

Underlying this is the risk reward trade off the banks are making, facilitated by the still too generous capital weightings for housing, compared with other lending categories. We need to have the ground shift such that there is more willingness for banks to lend to business. This will be hard, given the rising commercial exposures reported in this results season. The housing machine continues to consume all it its wake, leaving households with ever more debt, and no clear path to sustainable long term growth.