The UK’s approach to financial crime has taken a turn for the better recently. The successful prosecutions in the LIBOR-rigging scandal are a signal that British authorities are coming close to their US peers in slapping down errant bankers. The trouble is, there is pressure to take the foot off the pedal.

Not only has the new boss of the City watchdog suggested that banks should be keeping their own houses in order, the threat of Brexit opens up the possibility that the UK will have to fight to maintain the primacy of London as a financial centre. If that effort leads to a softening of the controls on the banks and bankers, it would be a grave mistake.

London is currently listed as the top financial capital in the world. Its main strengths are stability and dynamism. Effective regulatory and enforcement regimes can promote trust and confidence from the public, which helps to underpin that financial stability.

Given the role of banks in the global financial crisis, it is a dangerous time to soften controls, even if the pressure from the industry is ever present. There is a clear risk that some bankers will return to prioritising profit at the expense of customers and ultimately, at the expense of the wider economy. That would suit no one in the capital and beyond over the long term.

Motivation

Brexit though, has upset the apple cart. The US watchdog for monitoring financial stability, the US Office for Financial Research recently said that political and financial uncertainties caused by Brexit may last for months or even years. That leaves the financial industry in flux.

In effect, UK voters’ decision to leave the European Union gives a potential opportunity for countries such as France, Germany and Luxembourg to strengthen their positions as international financial centres. The most immediate concern is whether banks will be able to sell financial products and services from London to customers in Europe when Brexit takes place. Bullish noises from politicians may not be enough to convince banking executives that their strategic decision should be left to the whim of EU negotiators.

London will fight to stay competitive, but the focus should be a determination for regulators, politicians and investigators to maintain their improving proactive and robust styles. A race to the bottom on oversight would be potentially dangerous. It would leave the door open to fresh scandals; even a fresh crisis. It is hugely important that the new chancellor of the exchequer, Philip Hammond, leads a tough regulatory approach.

You see, an effective, efficient and enforced regulatory regime can be a competitive advantage. Australia and Canada both emerged better than the UK from the global financial crisis. One of the many reasons is that the regulators in Australia and Canada were more proactive and robust in monitoring and supervising their banks.

In the UK, the Bank of England’s report into the failure of the Financial Supervisory Authority (predecessor of the current watchdog, the Financial Conduct Authority) found that there were inadequate resources. This affected the authority’s ability to supervise banks such as HBOS. Simply put, you need sufficient resources (both human and financial) to enable the various authorities to perform their jobs effectively.

Taking the lead

The Financial Conduct Authority (FCA) is the regulator for the financial sector. It sets guidelines, monitors behaviour and can stop people from operating in the industry if they break its rules. Its remit is to protect consumers, and it did so with a budget of £479m in 2015-16 and £452m in 2014-15.

That is already more than the budgets of equivalent bodies in Germany and in the US. But while it is encouraging that the FCA is well funded relative to its peers, it is also a worry that policy makers might see this as fat that can be trimmed.

I believe the funding levels for the UK regulator should actually be boosted as it seeks to rubber-stamp Britain’s reputation in the face of threats to the financial sector, and a change to the law would do it.

Until 2012, regulators were able to use the fines collected from banks to fund their work. However, the then chancellor, George Osborne, changed the law to draw the fine revenues into the Treasury. Under Osborne’s control, armed forces charities and the emergency services received the fines, not the authorities which had imposed them.

Clearly, these charities and services perform very important roles in society but a boost to the budget for policing financial crime would help society in its own and important way, while helping London to maintain that competitive edge. Although fines against individuals by the FCA have declined in recent years, the new senior managers regime, designed to improve individual accountability, may reverse this trend.

As old investigations close – some with success – it is vital that there are the resources and support to start new investigations. The UK has the largest financial services sector in the European Union, at least for now: if it is to grow sustainably, to support a post-Brexit economy, then oversight and enforcement must be stronger than ever.

Author: Alison Lui, Senior Lecturer in Law, Liverpool John Moores University

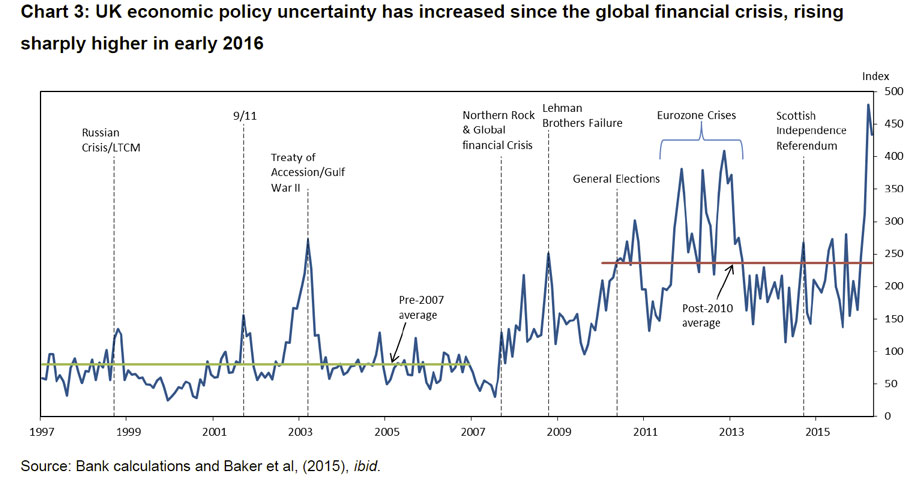

In a speech entitled “Uncertainty, the economy and policy“, given by Mark Carney, Governor of the Bank of England, he highlights that waves of uncertainty are washing over the UK economy, and these waves are getting larger. The result of the referendum is clear. Its full implications for the economy are not. But the question is not whether the UK will adjust but rather how quickly and how well. As risks have risen, further monetary policy interventions are likely, but he says there are limits to how much can be achieved with these levers.

… The decision to leave the European Union marks a major regime shift. In the coming years, the UK will redefine its openness to the movement of goods, services, people and capital. In tandem, a potentially broad range of regulations might change.

Uncertainty over the pace, breadth and scale of these changes could weigh on our economic prospects for some time. While some of the necessary adjustments may prove difficult and many will take time, the transition from the initial shock to the restructuring and then building of the UK economy will be much easier because of our solid policy frameworks.

At times of great uncertainty, households, businesses and investors ask basic economic questions. Will inflation remain under control? Will the financial system do its job?

In recent years, economic uncertainty has been elevated because of fragilities in the financial system and overhangs of public and private debt.

These challenges have been compounded by deeper forces that have radically altered the balance of saving and investment in the global economy. In the process, these have moved equilibrium interest rates into regions that monetary policy finds difficult to reach. Whether called ‘secular stagnation’ or a ‘global liquidity trap’, the drag on jobs, wages and growth is real.

All this uncertainty has contributed to a form of economic post-traumatic stress disorder amongst households and businesses, as well as in financial markets – that is, a heightened sensitivity to downside tail risks, a growing caution about the future, and an aversion to assets or irreversible decisions that may be exposed to future ‘disaster risk’.

Even before 23rd June, we observed the growing influence of uncertainty on major economic decisions. Commercial real estate transactions had been cut in half since their peak last year. Residential real estate activity had slowed sharply. Car purchases had gone into reverse. And business investment had fallen for the past two quarters measured. Given otherwise accommodative financial conditions and a solid domestic outlook, it appeared likely that uncertainty related to the referendum played an important role in this deceleration.

It now seems plausible that uncertainty could remain elevated for some time, with a more persistent drag on activity than we had previously projected. Moreover, its effects will be reinforced by tighter financial conditions and possible negative spill-overs to growth in the UK’s major trading partners.

As the MPC said prior to the referendum, the combination of these influences on demand, supply and the exchange rate could lead to a materially lower path for growth and a notably higher path for inflation than set out in the May Inflation Report. In such circumstances, the MPC will face a trade-off between stabilising inflation on the one hand and avoiding undue volatility in output and employment on the other. The implications for monetary policy will depend on the relative magnitudes of these effects.

Today, while the economy is more complex and our models less reliable, the Bank has identified the clouds on the horizon and can see that the wind has now changed direction.

Over the past few months, working closely with the Chancellor and with HM Treasury, we put in place contingency plans for the initial market shocks. They are working well.

Over the coming weeks, the Bank will consider a host of other measures and policies to promote monetary and financial stability.

In short, the Bank of England has a plan to achieve our objectives, and by doing so support growth, jobs and wages during a time of considerable uncertainty.

Part of that plan is ruthless truth telling. And one uncomfortable truth is that there are limits to what the Bank of England can do.

In particular, monetary policy cannot immediately or fully offset the economic implications of a large, negative shock. The future potential of this economy and its implications for jobs, real wages and wealth are not the gifts of monetary policymakers.

These will be driven by much bigger decisions; by bigger plans that are being formulated by others. However, we will relentlessly pursue monetary and financial stability. And by doing so we will facilitate the adjustments needed to realise this economy’s full potential.

In a speech to the Institute of Chartered Accountants of Scotland on 11 February, Dame Clara examines the UK’s position as host to a global financial centre through the lens of the Financial Policy Committee’s two main objectives: its primary objective to maintain financial stability, and its secondary objective to support the Government’s economic policy, including its objectives for growth and employment; productive investment, innovation, competition and the lead role of the City of London in international financial markets.

In the context of financial “de-globalisation” and sharply falling cross-border capital flows, Dame Clara believes that now is a good time to consider the benefits of global markets and financial centres. Historically, Dame Clara notes, the development of global financial centres went hand-in-hand with the integration of international capital markets, because a more complete market can allocate capital with much greater efficiency.

According to an IMF staff discussion note, financial development increases a country’s resilience; mobilises savings, promotes information sharing, improves resource allocation and facilitates diversification and management of risk. It also promotes financial stability to the extent that deep and liquid financial systems with diverse instruments help dampen the impact of shocks.

But at the same time, financial deepening and connected markets can transmit shocks as well as dispersing and absorbing risk and driving growth. “Overall, however, with the right policy framework, choices and institutions, it seems clear that the benefits of financial globalisation are compelling,” Dame Clara observes.

Next, Dame Clara considers why global centres are needed, when advances in technology have made it feasible for the financial system to become decentralised.

On reason why it is good to be global is that a specialised financial centre can yield “agglomeration benefits” – the economies of scale arising from having an industry cluster in a particular location – and which can also improve access to finance for households and businesses.

Another benefit of centralisation is that it allows the authorities to see more. “The more that activity clusters in a small number of centres, the more that regulators and policymakers can take a holistic, systemic view of threats to financial stability,” Dame Clara says.

In the UK context, there are also economic benefits in being a global financial centre. “While the primary objective of financial stability is paramount for the FPC, the UK clearly has an interest in maintaining its strong position as a provider of these services. Provided the financial sector remains resilient – and our new regulatory framework seeks to ensure that it does – this is central to the FPC’s secondary objective.”

Following on from this, Dame Clara considers the conditions for the success or failure of financial centres. Looking back over time, she observes that while financial centres have tended to cluster around centres of economic power, they can remain in place and prosper even after economic power has shifted elsewhere.

“The UK has maintained its position right into this century, even though the days in which Britain was the dominant superpower are long gone.”

That said, the decline of a financial centre can be precipitated by an adverse event, such as war or a policy error that makes the continued provision of financial services impossible, uneconomic or simply destroys confidence in it. As such, one lesson to be drawn from history is that policy choices and institutions matter.

Looking forward, proximity to power may be less important for financial centres such as the UK, thanks to advances in communications technology. However, because moving is easier than it was in centuries past, the same factors that mean the UK can serve the world, allow for a wide range of alternative centres to become established, possibly leading to a decentralisation and fragmentation of the financial system. This would undermine the efficiency of global capital markets and harm global growth.

“To avoid this, authorities need to remain alert to shocks, including those arising from the geopolitical and wider macrofinancial environment, as well as the more ‘bread and butter’ risks that are visible on banks’ balance sheets. This is where the FPC can play an important role,” according to Dame Clara.

An environment where geography and sheer economic scale matter less, means that institutions may matter even more. “We need a clear, prudent, proportionate system of regulation, which is sensitive to the different risks and opportunities posed by different kinds of activity,” Dame Clara says.

Dame Clara concludes that: “International and global financial centres have historically played a crucial role in promoting both growth and stability. But policymakers cannot take their existence for granted. In a world where institutions and policy choices matter more than ever, a prudent and proportionate regulatory framework is essential to sustainable growth. That is what we on the FPC are seeking to achieve.

After the financial crisis of 2007/2008 which shook the British economy to its foundations. In the face of what became know as the “credit crunch”, bank after bank found itself stretched. Some would have failed had they not fallen into the arms of the taxpayer – at staggering expense to the public.

New requirements for banks to hold enough capital to prevent them from going under in the event of another financial crisis have been questioned by Sir John Vickers.

Not happy: Sir John has accused the Bank of England of going soft on the banks Credit: PA

In a stark warning Vickers, the author of 2011’s Independent Commission on Banking (ICB) report in the wake of the financial crisis and subsequent bailouts, has called the wisdom of the BoE’s requirements “questionable”. The Bank of England is now in charge of regulating Britain’s banks and, in a rather devastating intervention, Sir John Vickers has basically accused it of going soft on the sector.

The requirement is expected to impose a buffer that equates to 0.5 per cent of risk-weighted assets (RWA) across the banking sector, in addition to existing global ones under Basel II rules from European regulators, but that’s less than the three per cent recommended by the report.

“Some UK banks are so important internationally that they have extra equity requirements to protect global stability. The BoE proposal adds some, but relatively little, further equity to protect domestic stability. The ICB proposal, by contrast, went well beyond global requirements to boost the resilience of the UK banking system,” he said, writing in the Financial Times.

Ring-fencing provides no reason to go easy on capital requirements…the Bank of England should think again.

The systematic risk buffer (SRB) as it’s known, would apply to the UK’s biggest banks such as Lloyds, HSBC, Barclays and RBS, and their soon to be ring-fenced retail banking operations, but not smaller banks and challenger banks to promote competition in the market.

“Given the awfulness of systemic bank failures, ample insurance is needed, and equity is the best form of insurance. The recent volatility in bank stocks underlines the importance of strong capital buffers. The BoE should think again,” Vickers warned.

In September 2011, Sir John’s Independent Commission on Banking (ICB) reported back with a series of reforms designed to make the banking system safer and less dependent on state bailouts.

Back in 2011, two of the ICB’s key recommendations were that:

1) banks “ring-fence” their traditional retail deposits and conventional lending from their riskier operations.

2) that the biggest (and therefore the most risky) ring-fenced banks should be required to hold back an extra layer of capital – known as a “Systemic Risk Buffer” – to offset the risk of the loans they make and, if necessary, absorb losses.

The ICB set the additional Systemic Risk Buffer at 3% of a bank’s Risk Weighted Assets and intended it to apply to six of our biggest lenders. Last month the Bank ofThis is biting criticism. Sir John is basically accusing the Bank of England of failing to implement what the ICB recommended. There’s no suggestion of anything underhand – the Bank has publicly set out its justifications, it’s just that Sir John Vickers believes they are weak.

As part of the legislative package implementing the recommendations of the Independent Commission on Banking in the UK, the Financial Policy Committee (FPC) is required to produce a framework for a systemic risk buffer (SRB) for ring-fenced banks and large building societies.

The SRB is one of the elements of the overall capital framework for UK banks and building societies as set out by the FPC in its publication ‘The framework of capital requirements for UK banks’, which was published alongside the December 2015 Financial Stability Report.

The SRB will be applied to individual institutions by the Prudential Regulation Authority (PRA) and will be introduced, like the ring-fencing rules, from 2019.

Deputy Governor, Financial Stability, Jon Cunliffe said:

“These new rules will mean that large UK banks and building societies are more resilient to adverse shocks, enabling them to continue to lend to households and businesses even in times of stress. The financial crisis demonstrated the long-lasting damage that can be caused when large banks become distressed and have to cut back lending to the economy. These proposals are intended to reduce the risk of this happening again.”

Summary of the proposals

It is proposed that those banks and building societies with total assets above £175bn will be set progressively higher SRB rates as total assets increase through defined buckets (see table below). HM Government required the FPC to produce a framework for the SRB at rates between 0% and 3% of risk-weighted assets (RWAs). Under the FPC’s proposals, ring-fenced bank sub-groups and large building societies in scope with total assets below £175bn will be subject to a 0% SRB.

Based on current information, under these proposals the FPC expects the largest ring-fenced bank in 2019 to have a 2.5% SRB. In line with the FPC’s previous announcement on the leverage ratio framework, those institutions subject to the SRB will also be set a 3% minimum leverage ratio requirement, together with an additional leverage ratio buffer calculated at 35% of the applicable SRB rate. For example, an institution with an SRB rate of 1% would have an additional leverage ratio buffer of 0.35%.

As stated in the FPC’s capital framework document in December, the proposed calibration is expected to add around an aggregate 0.5 percentage points of risk-weighted assets to equity requirements of the system in aggregate.

Total Assets (£bns)

Risk weighted

SRB rate

Lower threshold

Upper threshold

0%

-

<175

1%

175

<320

1.5%

320

<465

2%

465

<610

2.5%

610

<755

3%

≥755

The consultation will close on 22 April and the FPC intends to finalise the framework by 31 May 2016. The buffer will apply from 2019.

The UK Prudential Regulation Authority (PRA) and Financial Conduct Authority (FCA) have launched the New Bank Start-up Unit. The Unit is a joint initiative from the UK’s financial regulators giving information and support to newly authorised banks and those thinking of becoming a new bank in the United Kingdom.

The joint New Bank Start-up Unit will assist new banks to enter the market and through the early days of authorisation. It will draw staff from the PRA and the FCA with a dedicated helpline and email address. It will provide new banks with the information and materials they need to navigate the process to become a new bank, as well as with focused supervisory resource during the early years of authorisation.

The New Bank Start-up Unit will provide named case officers for firms during the authorisation process at both the PRA and the FCA and a greater level of supervisory support during the new bank’s early years after they have been authorised.

New banks will benefit from:

access to the New Bank Start-up Unit helpline;

access to supervisors at both the PRA and the FCA via the helpline;

regular capital and liquidity reviews, if appropriate;

monthly regulatory update emails;

invitations to seminars targeted at new and prospective banks and separately banks’ senior management and NEDs; and

invitations to events, alongside other firms, on key regulatory conduct topics.

Andrew Bailey, Deputy Governor, Prudential Regulation, Bank of England and CEO of the Prudential Regulation Authority said: “The New Bank Start-Up Unit builds on the work we have already done to reduce the barriers to entry for prospective banks, which has led to twelve new banks now authorised since April 2013. These new banks are a key part of bringing innovation to the sector, particularly where there is a gap in the market – whether it is the service they provide, the customers they target, the products they sell or the technology they use. With the launch of the New Bank Start-up Unit, applicants will now benefit from having a single place where they can get the advice and guidance they need to start a new bank and support once they are authorised.”

Tracey McDermott, Acting CEO of the FCA said: “The New Bank Start-Up Unit will help those who want to start a new bank in the UK navigate the regulatory process. Increasing competition in the banking sector is important for consumers and the new Unit will offer firms an accessible way to find the information they need to get themselves authorised”.

Economic Secretary to the Treasury Harriett Baldwin said: “A key part of our long term plan is to boost competition in banking, driving the industry to offer the best possible products and services to customers”. “I’m therefore delighted that the Prudential Regulation Authority and Financial Conduct Authority have now established a dedicated New Bank Start-up Unit, helping new banks to enter the market and through the early days of authorisation”.“Building on the three new banks that have already established this Parliament, this unit will help to stimulate even more competition and diversity in Britain’s banking sector.”

Fitch Rating. says that after its latest stress tests, the Bank of England’s (BoE) assessment is that the UK banking sector is adequately capitalised and the results will not force any capital planning revisions. Further sector-wide capital step-ups are unlikely in future.

Capital ratios are likely to remain stable, held up by the BoE’s increased use of countercyclical buffers. These will be built up as lending growth accelerates and will be released when the cycle turns. The BoE’s intention is that banks’ capital planning should become more efficient and flexible. The BoE’s Financial Policy Committee indicated that it considers a Tier 1 capital adequacy ratio of 11% to be appropriate for the sector. Fitch expect banks to set their internal buffers relative to this level and plan their capital needs relative to the level of sensitivity to stress test inputs.

Results from yesterday’s stress test show that, under the baseline scenario, the seven participating banks are improving their capital positions. But the Royal Bank of Scotland Group (RBS; BBB+/Stable) and Standard Chartered (A+/Negative) did not meet the BoE’s capital requirements under the stress scenario. Both banks have taken, or are taking steps this year to address capitalisation.

The regulator will use future stress test results to assess individual banks’ capital requirements. Fitch expects the tests to become more sophisticated and more qualitative in nature. This is already the case in the US where the Federal Reserve’s annual Comprehensive Capital Analysis and Review plays an important role in how the country’s leading banks assess their capital planning exercises.

In the UK, annual cyclical tests will be run to capture risks from financial cycles, with the severity of scenarios increasing as risks build up. This should produce more rounded stressed results. Latent risks not captured by the annual cyclical scenario will be introduced every other year when the BoE will run a biannual stress test. Fitch thinks the banks should, over time, be able to anticipate broad movements in the annual cyclical scenario, making it easier for them to set internal buffers above minimum regulatory requirements, based on their expected sensitivity to the regulatory stress test.

The 2015 stress test hurdles – a 4.5% common equity tier 1 (CET1) ratio and a 3% leverage ratio – were not particularly onerous. All participating banks met these. But hurdle rates will evolve and banks will need to meet their Pillar 1 minimum CET1 ratios under stressed scenarios, plus any additional requirements set by the regulators under Pillar 2A and buffers for systemically important banks.

The UK Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA) has published the Review into the failure of HBOS Group. The Review concludes that ultimate responsibility for the failure of HBOS rests with the Board and senior management. They failed to set an appropriate strategy for the firm’s business and failed to challenge a flawed business model which placed inappropriate reliance on continuous growth without due regard to risks involved. In addition, flaws in the FSA’s supervisory approach meant it did not appreciate the full extent of the risks HBOS was running and was not in a position to intervene before it was too late.

This review was originally started by the former regulator, the Financial Services Authority (FSA). Its purpose is to analyse the causes of the firm’s failure, and to draw out lessons for the future, for both the industry and the regulatory system as a whole.

On 1 October 2008 HBOS was approaching a point at which it was no longer able to meet its liabilities as they fell due and so sought Emergency Liquidity Assistance from the Bank of England. This report seeks to explain why HBOS failed, the role that HBOS Board and senior management played in the failure and the FSA’s supervision of HBOS.

The main period covered by the FCA/PRA Report (the Review Period) is from January 2005 to the point of failure, though it draws on earlier materials going back to the creation of HBOS in 2001, and some materials from after the point of failure where these provide useful context to help the explanation of failure. The Report draws on the records of the firm, the FSA as supervisor of HBOS, interviews with the main individuals involved, and other relevant outside sources. Documentary evidence has been combined with interviews, so that individuals could give theirown account of events, and supplemented by representations received from a number of parties.

The paradox of the story is that at the time, and indeed up until quite near to its failure, HBOS was widely regarded as a success story. The 2001 merger of Halifax and Bank of Scotland had yielded double-digit profit growth in all but one of the years up to end-2006 and analysts’ and brokers’ views were positive at least until early 2007. But, by this time, the seeds of the firm’s destruction had already been sown as a flawed strategy led to a business model that was excessively vulnerable to an economic downturn and a dislocation in wholesale funding markets.

The failure of HBOS can ultimately be explained by a combination of factors:

Its Board failed to instil a culture within the firm that balanced risk and return appropriately,and lacked sufficient experience and knowledge of banking.

The result was a flawed and unbalanced strategy and a business model with inherent vulnerabilities arising from an excessive focus on market share, asset growth and short-term profitability.

This approach permitted the firm’s executive management to pursue rapid and uncontrolled growth of the Group’s balance sheet, and led to an over-exposure to highly cyclical commercial real estate (CRE) at the peak of the economic cycle, lower quality lending, sizable exposures to entrepreneurs, increased leverage, and high and increasing reliance on wholesale funding. The risks involved were either not identified or, where identified, not fully understood by the firm.

There was a failure by the Board and control functions to challenge effectively executive management in pursuing this course or to ensure adequate mitigating actions.

HBOS’s underlying balance sheet weaknesses made the Group extremely vulnerable to market shocks and ultimately failure as the crisis of the financial system intensified.

There was an extended period of inflows of capital to developed economies, resulting in low yields, declining awareness of risk and asset price bubbles, in which market discipline – investors, analysts, rating agencies and other third parties – failed to constrain firms from undertaking risky strategies.

An overall systemic crisis in which the banks in worse relative positions were extremely vulnerable to failure. HBOS was one such bank.

Ultimate responsibility for the failure of HBOS rests with its Board. However, another striking feature of HBOS’s failure is how the FSA did not appreciate the full extent of the risks HBOS was running and did not take sufficient steps to intervene before it was too late.

The FSA Board and executive management failed to ensure that adequate resources were devoted to the supervision of large systemically important firms such as HBOS. This gave rise to:

a risk assessment process that was too reactive, with inadequate consideration of strategic

insufficient focus on the core prudential risk areas of asset quality and liquidity in a benign economic outlook; and

too much trust being placed in the competence and capabilities of firms’ senior management and control functions, with insufficient testing and challenge by the FSA.

Andrew Bailey, Deputy Governor of the Bank of England, CEO of the PRA and Accountable Executive for the HBOS Review said “The story of the failure of HBOS is important both to provide a record of an event which required a major contribution by the public purse, and because it is a story of the failure of a bank that did not undertake complicated activity or so-called racy investment banking. HBOS was at root a simple bank that nonetheless managed to create a big problem.”

Sir Brian Pomeroy, Senior Independent Director at the Financial Conduct Authority and Chairman of the HBOS Review Steering Committee said:

“The review into HBOS has involved a dedicated team sourcing and considering a huge amount of material including reviewing around a quarter of a million documents and interviews with 80 key individuals. I am hugely thankful for the painstaking work the team have done to compile a comprehensive report. While much has already been written about the failure of HBOS, I believe this to be the definitive account and to be a thorough, fair and balanced view of what occurred.”

As part of the Review, Andrew Green QC was asked to provide an independent assessment of whether the decisions taken on enforcement by the former regulator, the FSA, were reasonable. The PRA and FCA are therefore also today publishing Andrew Green QC’s report into the FSA’s enforcement actions following the failure of HBOS

In his report, Andrew Green QC recommends that the PRA and FCA should now consider whether any former senior managers of HBOS should be the subject of an enforcement investigation with a view to prohibition proceedings.

The PRA and FCA will conclude a review as to whether further enforcement action should be taken as early as possible next year.

Banks must address long-term problems and make it easier for customers to take charge of their accounts, the UK’s Competition and Markets Authority (CMA) stated this week.

Publishing its provisional findings as part of an in-depth investigation into the £16 billion current account and business banking sectors, the CMA has found that banks do not have to work hard enough to compete for customers.

The investigation has identified a number of competition problems in both the personal current account (PCA) and small and medium-sized enterprise (SME) banking markets. Low levels of customer switching mean that banks are not put under enough competitive pressure, and new products and new banks do not attract customers quickly enough. There is a particular problem in SME banking where many SMEs open their business current accounts (BCA) at the same bank where they have their PCA, then stick with that bank for their business loans.

57% of consumers have been with their PCA provider for more than 10 years, and 37% for more than 20 years. Customers with current accounts are faced with complex overdraft charges and limited information on product and service quality, which, along with limited effective comparison tools, makes it very difficult for customers to know what they are paying and to compare banks and products.

Bank customers fear that switching their current account to a new bank will be complicated, time-consuming and risky. The Current Account Switch Service (CASS) was set up to make the process easier and is functioning reasonably well, but awareness and confidence remain low. Only 3% of customers switched their PCA in 2014 and just 16% looked at alternative accounts.

The CMA found that overdraft users are even less likely to switch PCAs than other users. Heavy overdraft users, in particular, could save up to £260 a year if they switched. On average, current account users could save £70 a year by switching.

The investigation also discovered that accounts which are more expensive and below average quality are not losing customers to cheaper and better alternatives at the rate that would be expected in a well-functioning market.

The lack of competitive pressure in SME banking is highlighted by the fact that more than 50% of start-ups looking for a SME account choose the bank with which they have a personal current account, over 90% stay with their BCA when the initial free banking period comes to an end, and around 90% then go to their BCA provider when they are looking for business loans.

As in the case of PCAs, the opening and/or switching process is seen to be time-consuming, and at risk of things going wrong. SME charging structures are complex and difficult to compare, there are no service quality measures to aid comparison and there are limited effective price comparison tools for SMEs.

The CMA investigation did find a number of positive developments: new entrants into both PCA and SME banking, innovative products becoming available, the digital innovations associated with online and mobile banking, and new tools like Midata and CASS, which have the potential to increase searching and switching.

Despite these encouraging developments, because too few customers are switching, banks do not have strong enough incentives to work hard to compete for customers through better products or cheaper prices, and smaller or better banks find it hard to gain a foothold.

The CMA has published an initial list of remedies, which sets out possible measures aimed at addressing these issues by increasing competition and securing a better deal for customers. It will develop these proposals over the coming months. It is important that any new remedies are really effective, so the CMA will be testing its proposals carefully.

Potential remedies include:

Requiring banks to prompt customers to review the service they receive from their bank through receiving individual messages at certain ‘trigger points’. These trigger points could include a loss of service, closure of their local branch, unarranged overdraft charges or a change in the terms and conditions of their account. In the case of SMEs a key trigger point could come at the end of free banking periods.

Making it easier for consumers and businesses to compare bank products by upgrading Midata, an industry online tool, launched with the support of government, that gives consumers access to their banking history at the touch of a button. Midata allows consumers to easily access their banking data from their bank and input it directly into a price comparison website which can then analyse their transactions, and alert them to available bank accounts which best suit their needs. An improved Midata could have a radical impact on consumer choice in retail banking markets.

Requiring the creation of a new price comparison website for SMEs – currently nothing effective exists to fulfil this role.

Requiring banks to help raise public awareness of, and confidence in, switching bank accounts, through increasing their funding for a widespread and sustained advertising campaign promoting CASS and improving the service it offers.

Requiring better sharing of information with credit reference agencies, banks and financial advisers – making it easier for SMEs to shop around for loans and cutting out the need for multiple application form filling.

The CMA provisionally decided not to recommend remedies aimed at ending free if-in-credit (FIIC) accounts as it saw no convincing evidence that the prevalence of the FIIC model distorted competition, noted that some banks have already devised accounts which compete with FIIC through the rewards they offer, and also noted that FIIC accounts give a reasonable deal to many customers.

Structural remedies, such as forcing the break-up of banks, were also provisionally rejected as it was decided that they were not likely to be effective in addressing the competition concerns found. The problems in the market are unlikely to be resolved by creating more, smaller banks; it is the underlying issue of lack of switching which has to be addressed.

Alasdair Smith, Chairman of the retail banking investigation, said:

Banking is a sector of huge importance that affects every household and business in the country.

We think customers need to be put in charge of their banking.

There have been long-standing concerns about the retail banking market, where many customers could save money and get better services by switching accounts. This investigation was an opportunity to take a detailed and independent look at the sector.

Despite some encouraging developments, particularly in the shape of challengers that have entered the market in recent years, for too long banks have been able to sit back and take their existing customers for granted.

We don’t think that customers will truly benefit from a more competitive marketplace until they can compare accounts more easily and feel confident that they can switch without risk, and that is why our provisional remedies are aimed at giving customers control.

We are considering a series of measures that will have a far-reaching impact on how banks operate and will empower account-holders to search for and switch to the account that suits them.

The investigation is looking separately at Northern Ireland, but has made the same findings for Northern Ireland as it has for Great Britain.

The full provisional findings report along with over 30 appendices will be published later next week. The CMA will now consult and hold detailed discussions with all interested parties on the findings and possible remedies ahead of publishing its final report in May 2016. The CMA is also reviewing measures put in place by its predecessor body, the Competition Commission, in 2002 and 2008, to remedy concerns in the SME banking and Northern Ireland personal current account sectors.

The Prudential Regulation Authority’s (PRA) ring-fencing policy proposals limit, but do not prevent, ring-fenced banks (RFB) to lend to non-ring-fenced sister banks (NRFB) and impose no added restrictions on dividend payments. This will allow some fungibility of funding and capital within group companies. Standalone Viability Ratings (VR) assigned to RFBs and NRFBs will therefore remain interdependent, reducing rating gaps between them, says Fitch Ratings.

The PRA has sought to eliminate the use of intra-group concessions across the ring-fence and now expects banks to apply third-party credit discipline to such exposures. This will improve analytical transparency which we view positively.

We envisage that UK banks subject to ring-fencing will adopt one of two models depending on the relative size of their non-ring-fenced activities, prior to the January 2019 deadline. Banks have to submit their plans by January 2016, according to the PRA’s consultation paper published on 15 October.

VRs assigned to RFBs are likely to be constrained by limited geographical and product diversification and, provided these remain largely focused on UK retail and SME lending, we do not expect to see much ratings differentiation between them. We already indicated in our September 2014 comment, accessed by clicking on the link below, that VRs for RFBs narrowly focused on domestic retail and SME business are likely to be capped in the ‘a’ range.

The UK ring-fencing rules apply to banks with more than GBP25bn of core deposits from SMEs and individuals. Most banks affected by ring-fencing have very limited (if any) wholesale and investment banking activities and therefore these groups will adopt models dominated by RFBs. This will be the case for Lloyds and RBS.

In these instances, the ability of the larger RFB to lend up to 25% of its regulatory capital to the smaller NRFB should be a significant positive ratings factor for the NRFB’s VR. This is because the NRFB will be able to benefit from ordinary support flowing from the larger RFB.

For groups whose non-retail, corporate and investment banking business is significant, as is the case for Barclays and HSBC, the importance of the NRFB within the restructured group is likely to be significant, or even dominant. The RFB’s ability to fund its NRFB sister will likely be less material simply because of the banks’ relative sizes. Under this model, we believe that management will seek to structure RFB and NRFB subsidiaries to ensure these remain robust on a standalone basis, maintaining strong and balanced funding and liquidity and meeting adequate capitalisation levels.

A clearer picture about the likely ratings outcome for RFBs and NRFBs will emerge once further details of group restructuring are available. Much will depend on exactly what activities are kept in or out of the fence. Resolution strategies (‘single point of entry’ or ‘multiple point of entry’), depending in particular on the volumes, form and source of ‘loss absorbing’ debt, will also be relevant for ratings and will add a separate layer of uncertainty to ratings within a UK banking group until more clarity emerges.

But, as far as regulations are concerned, our opinion is that the PRA proposals will not create a particularly ‘high’ fence, reducing intra-group rating differentials. By preserving the ability to share capital and funding across RFBs and NRFBs, the PRA is demonstrating that it is keen for RFBs to continue to enjoy the benefits of remaining part of broader banking groups.