Several UK mortgage lenders have announced loan repayment holidays to support homeowners affected by coronavirus. Via Homes and Property

Royal Bank of Scotland said it will defer mortgage payments for up to three months to affected borrowers.

The state-backed bank is 62 per cent owned

by the taxpayer and has announced the emergency measures to support

customers who might lose their jobs or see their income decline if they

cannot work due to illness or lockdown.

A spokeswoman for RBS said: “We are monitoring the potential impact of coronavirus

across all our customers to ensure we can support them appropriately

through any period of disruption. We have a strong track record in

working with our customers who are affected by disruption outside of

their control.”

TSB also said borrowers could have mortgage repayment holidays for up to two months.

UK Finance said all its members were

putting measures in place to support borrowers affected by the virus.

Stephen Jones, the industry body’s chief executive said: “All providers

are ready and able to offer support to their customers who are impacted

directly or indirectly by COVID-19, which could include offering or

increasing an overdraft or allowing repayment relief for loan or

mortgage repayments: asking for help early is key.

“We would encourage customers who think

they may be affected to contact their provider as soon as possible to

discuss the support available to them.”

Miles Robinson, head of mortgages

at online broker Trussle, said: “Self-employed and gig economy workers

might be concerned about their income becoming more unstable, at least

temporarily, which may affect their ability to pay the bills at the end

of the month.

“The good news is that mortgage lenders

don’t live under a rock. They know that coronavirus is causing severe

uncertainty. They’re also aware that as a result of the outbreak, some

customers might be unable to make their monthly mortgage repayments.”

UK lenders adopted similar measures in the 2009 recession.

According to Moody’s on 15 January, UK Financial Conduct Authority (FCA) chief Executive Andrew Bailey, reiterated the organisation’s intention to improve so-called mortgage prisoners’ access to refinancing by relaxing current mortgage affordability regulations that preclude them refinancing into cheaper mortgage deals because they fail to meet affordability standards that were tightened in 2016.

Relaxing the mortgage affordability parameters for refinancing such borrowers’ mortgages would be credit positive for more than 60 UK RMBS securitisations containing pre-crisis assets, which equate to more than £29.0 billion of outstanding bonds.

The FCA has suggested that authorised UK lenders would be willing to refinance such mortgage prisoners if the borrower qualified for refinancing under the new rules, which would require the new mortgage installments to be lower than previous installments and for the borrower to be up to date with their payments. The new rules would replace current affordability tests for these borrowers, which make sure a borrower has enough money left to pay their mortgage installments in a stressed interest rate environment after covering all other basic needs (e.g. bills, food, childcare).

At present, a borrower refinancing with its current lender does not always require affordability re-testing, but some lenders, such as Southern Pacific Mortgage Limited and Bradford & Bingley plc, have stopped originating loans in recent years. Furthermore, a significant number of mortgage loans were sold to entities that are not authorised lenders, such as private equity firms or investment banks. In both cases, those affected borrowers can only refinance with new lenders, thus falling under the stricter affordability testing introduced post- crisis. FCA estimates that there are about 140,000 affected borrowers, 120,000 whose loans are owned by firms not authorised to lend and 20,000 borrowers whose lenders are inactive.

Moody’s expect performance to improve for securitisations containing legacy assets if the changes are enacted. The majority of mortgage prisoners’ installments accrue interest at relatively high floating rates. Therefore, their mortgage installments will increase in the event of an increased base rate, as is currently expected in the UK. Higher rates make affordability more challenging and have the potential to cause additional defaults.

If those borrowers can refinance at a lower interest rate, the mortgage loans instead exit the securitisation pools early, leading to increased credit enhancement for remaining noteholders and reduced future losses.

The exemption will have the greatest positive effect for more recent securitisations of pre-crisis mortgage loans because the majority of recent securitisations of legacy assets have been cleaned of arrears loans.

Transactions that closed prior to 2009, while also benefiting from the early repayment of loans and increased credit enhancement, are typically smaller in size and also usually already contain a high proportion of loans in arrears. Hence the redemption of loans by mortgage prisoners will tend to concentrate the pools’ exposure to loans with borrowers having real affordability problems.

One of the critical issues which is hardly discussed in the media is that fact that many savers have funds in accounts which are paying very low rates of interest, when in fact there are better deals available. This little guilty secret allows banks to pump up their margins, offer highly attractive rates to capture new customers then milk them down stream.

Paying lower interest rates to longstanding customers is a long-running pricing strategy used by firms around the world, and gets almost NO coverage. Its a blatant example of “price discrimination” which occurs when providers offer different prices to different customers that have the same costs to serve but different willingness to pay.

But now the UK’s Financial Conduct Authority has released a discussion paper on the problem, which we also see here in Australia. They believe this is unlikely to change without further intervention. They propose a solution which we think might be worth looking at here too. So today I am going to look through their report, and discuss the issue in depth.

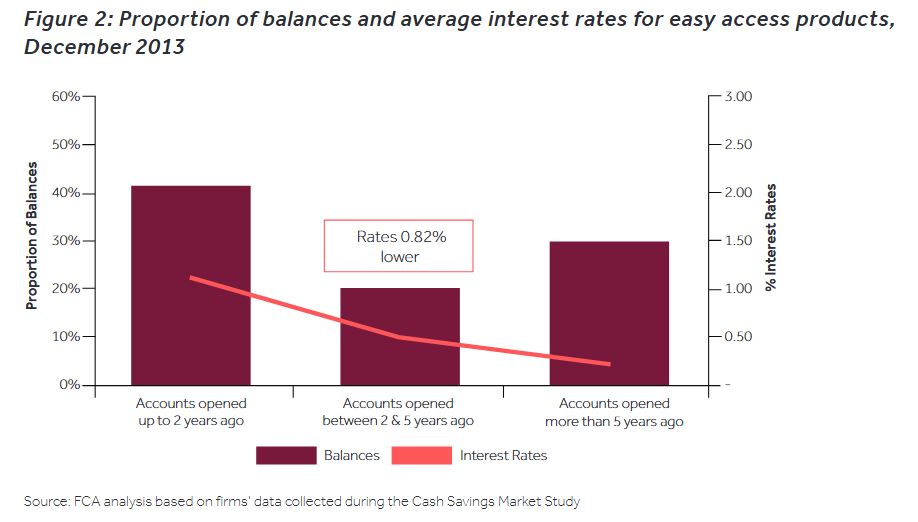

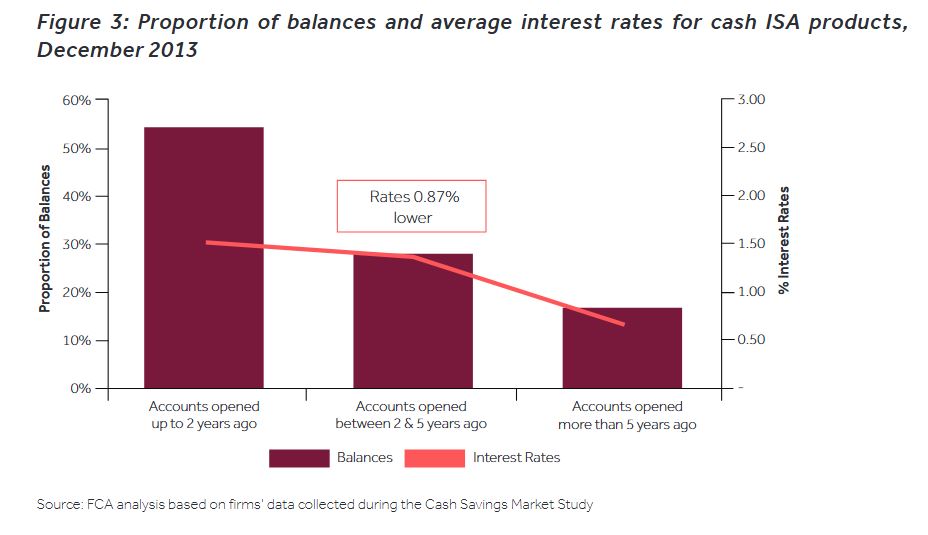

Many savers (yes there are still some with money in the bank despite the debt bomb), have their hard earned funds sitting in low interest paying accounts. Their research shows that 33% of the £354bn easy access savings account balances in savings accounts in the UK have been in accounts for more than 5 years, and that on average longstanding customers received on average 0.82% less than accounts opened more recently. A similar trend is also reported in the £108bn investment savings account, where again longstanding customers received on average 0.87% lower.

They call out the high level of consumer inertia in the cash savings market, with only 9% of consumers switching in the last 3 years. Their research also highlights that providers have multiple easy access products, leading to confusion for consumers, and large personal account providers have a competitive advantage over smaller providers.

So they has initiated a discussion about what should be done in the UK to improve outcomes for customers.

They say that consumers are put off switching by the expected hassle; large, well-established personal current account providers are able to attract most savings balances despite offering lower rates; and there is a lack of product transparency.

In fact this is the latest in a series of interventions which the FCA has been look at since 2015. They initially trialed

A switching box: provided to customers periodically, setting out the potential financial gains from switching. This would prompt customers to consider their choice of account and provider.

RSF: a simple ‘tear-off’ form and pre-paid envelope which would enable a customer to switch to a better paying account offered by their existing provider more easily (internal switching).

Neither worked that well, though the second, a simple tear-off form was a little more effective.

They also tried what they called a sunlight remedy for 18 months in 2015-16. In this trial, they asked firms to provide data on the lowest possible rate that customers could earn across all their easy access savings accounts and easy access cash ISAs. This was split into on-sale and off-sale accounts and branch and non-branch accounts. They released the data over 12 months, via publications. However, they found that the trial did not have a clear, measurable impact on providers’ rate setting strategies. There may be several reasons for this, including that the rates published did not always accurately reflect the rate being paid to most customers.

In the current paper they describe some of the other options they considered, including a complete price discrimination ban on easy access cash savings products. This would involve firms being required to offer single interest rates for all easy access cash savings accounts and easy access cash ISAs, irrespective of the length of time the account has been open.

Banning price discrimination would address the harm against longstanding customers. Under this approach, providers would be unable to offer different interest rates based on age of account. Longstanding customers would have the most to gain from this approach as they are likely to see an increase to their interest rates. Furthermore, customers would not have to take any action to be put on to the same rate as new customers.

It would also increase transparency as providers would be unable to obfuscate prices by making interest rates for all customers clear. This would make it easier for customers to understand and compare their interest rate. It would therefore be beneficial for competition as it would make it easier for customers to shop around for a potentially better value product with an alternative provider.

It may be beneficial for smaller providers with smaller back-books as it would not affect them as much as providers with larger back-books. Smaller providers would therefore be able to continue to offer higher rates than large providers, attracting customers.

This would make it easier for small firms to attract new balances and thus expand. The increased transparency adds to this effect as customers would be able to compare rates more easily and understand how different providers treat their customers.

However, the FCA says that although they have not performed any detailed modelling of this potential remedy, they believe that the unintended consequences of this approach could be significant and may outweigh the intended benefits. First, retail deposits make up a vital part of providers’ funding strategies, with 87% of funding generated by customer deposits (either current accounts or savings accounts).

This approach is, therefore, likely to have an adverse impact on funding models. It would significantly decrease flexibility and reduce providers’ ability to alter their pricing strategies to manage their funding requirements, ie by either shedding or attracting deposits. They

consider that this could lead to significant unintended consequences. They, therefore, believe that a less restrictive option would be more proportionate relative to the harm. Secondly, the impacts may be offset by significantly reducing front-book interest rates across the board, particularly for larger providers. This is because providers may find it too costly to increase interest rates on all back-book accounts. This may reduce the benefits of shopping around for more active customers who wish to remain with a larger provider.If the customer knows they are getting the best internal rate, there may be less of an incentive to shop around at all. If fewer customers shopped around, this may have the effect of further entrenching the power of the incumbents.

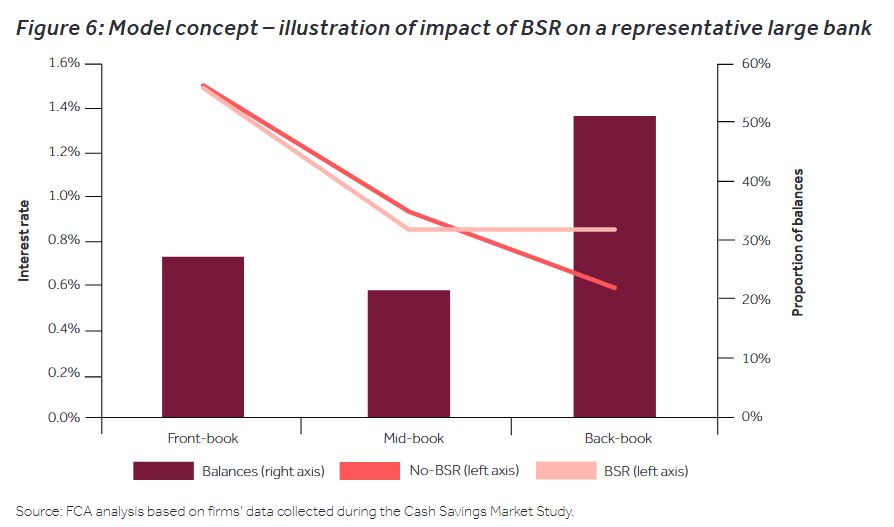

So, instead, they suggesting the introduction of a basic-savings-rate (BSR).

The BSR would involve providers applying single interest rates (BSRs), respectively, to all easy access cash savings accounts and to all easy access cash ISAs which have been open for a set period of time (for example, 12 months). Individual providers could decide the level of their BSR, and would be able to vary it. Providers would remain able to offer different interest rates to customers in the period before the BSR applies (the front-book).

The BSR option that they have modelled is based on providers having broadly 3 groups of customers:

front-book customers who opened their accounts less than 1 year earlier

mid-book customers who opened their accounts between 1 and 2.5 years earlier

back-book customers who opened their accounts over 2.5 years earlier

They suggest that consumers could gain £300m per year – (actually a range of £150m – £480m)

This is a net transfer from firms to customers, taking into account the ‘waterbed effect’ between the different customer groups. They envisage that a BSR could apply to an account after it has been open for a specified length of time. Providers would retain the freedom to offer a full range of easy access products to front-book customers (ie on accounts before the BSR applies) and would also be free to offer the BSR to front-book customers.

They envisage that a BSR could apply to all banks and building societies that offer easy access cash savings accounts and easy access cash ISAs. Credit unions were excluded from the scope of the CSMS as most products they offer could not be substituted for others. Most credit unions offer a dividend rather than an advertised interest rate on their savings. This dividend can depend on how much profit the credit union has made in the year.

They say it would be important for the BSR to be communicated effectively to consumers. This would ensure that consumers are aware of the changes to their interest rate on their savings account and prompt them to consider their choice of savings account and firm; in doing so, they may increase competitive pressure. In addition to providers’ current obligations on the communication of interest rate changes, to provide clarity to consumers before they open their account, providers could:

display their BSR prominently on their webpage, clearly stating that this is their ‘Basic Savings Rate’ and that it is comparable

include the BSR in summary boxes for easy access accounts; they could make the interest rate that would apply after 12 months clear and include a projection of the balance of the account when the BSR applies based on a £1,000 account balance.If a BSR were to be proposed, the FCA’s current view is that providers should communicate the change to existing customers when they first implement the BSR. Sunlight remedy linked to a BSRAs a development of the sunlight remedy trialled in 2015-16, they could introduce a sunlight remedy linked to the BSR. They could ask providers to report their BSRs to the FCA to be published on the FCA website biannually. The aim of this would be to bring to light firms’ strategies towards their longstanding customers. They would expect this to:

be reported by the media as an indicator of how firms treat longstanding customers, exerting reputational pressure on firms to change their behaviour

increase back-book rate transparency, removing a switching barrier by making it easier for customers to understand if they are getting a good dealThey believe that publishing BSRs on the FCA webpage would be more successful than the sunlight trial, given that the BSRs would be directly comparable across firms. they, therefore, believe this would be more likely to have an effect on providers’ rate-setting strategy.

I think its time we had a debate in Australia about the same issue, because data from my surveys highlights that many savers are not getting the best returns they could. So far as I can see ASIC has not even looked at the problem, more shame on them. Another case where regulators here are asleep, and customers are being ripped off as a result – does that sound familiar?

Lloyds Banking Group said on Monday that it was stopping people buying cryptocurrencies using credit cards, following moves last week from several major U.S. lenders.”Across Lloyds Bank, Bank of Scotland, Halifax and MBNA, we do not accept credit card transactions involving the purchase of cryptocurrencies,” the company told CNBC in a statement.

Concerns have been mounting that people buying digital currencies like bitcoin with credit cards could be getting into debt given wild price swings, particular recently given bitcoin fell below $8,000 for the first time in over two months.

U.K. Prime Minister Theresa May told Bloomberg in a recent interview that the government should consider looking at cryptocurrencies “very seriously.”

Other regulators around the world from China to South Korea have also bought in rules to try to regulate the space.

The Financial Conduct Authority (FCA) is the conduct regulator for 56,000 financial services firms and financial markets in the UK and the prudential regulator for over 18,000 of those firms. The FCA recently published feedback on its Discussion Paper on Distributed Ledger Technology (DLT).

In April 2017 The FCA announced that it was seeking stakeholder views on the potential for future development of DLT in the markets the FCA regulates.

The FCA received 47 responses from a wide range of market participants including regulated firms, national and international trade associations, technology providers, law firms and consultancies.

DLT has come to greater public prominence as it underpins digital currencies such as Bitcoin. This paper is not about Bitcoin or other so-called cryptocurrencies. Rather its remit is to consider the range of ways that DLT can impact on financial services and the regulatory implications.

Respondents expressed particular support for the FCA maintaining a ‘technology-neutral’ approach to regulation and welcomed the FCA’s open and proactive approach to new technology, including our Sandbox and RegTech initiatives.

The feedback also suggested that current FCA rules are flexible enough to accommodate the use of DLT by regulated firms and no changes to specific rules were proposed. Many respondents suggested that DLT solutions could deliver regulatory requirements more efficiently than current systems, substantially reducing costs for firms and regulators alike.

However, some respondents doubted the compatibility of permissionless networks (permissionless networks allow general public visibility of transactions online and are open for broad participation whilst permissioned networks typically feature a ‘gatekeeper’ who controls access) with our regulatory regime. Based on the feedback and its own work, overall the FCA is open to all forms of deployment of DLT (including both permissioned and permissionless DLT networks) provided the operational risks are properly identified and mitigated.

The FCA will continue to monitor DLT-related market developments, and keep its rules and guidance under review in the light of those developments. It will work collaboratively with industry, HM Treasury, the Bank of England, the Information Commissioner’s Office and other UK bodies to ensure a co-ordinated approach towards DLT in the UK. At an international level, the FCA will work closely with national and international regulatory bodies to shape regulatory developments and standards.

On the Initial Coin Offering (ICO) market, the FCA will gather further evidence and conduct a deeper examination of the fast-paced developments. Its findings will help to determine whether or not there is need for further regulatory action in this area beyond the consumer warning issued in September. In the meantime, the FCA highlights how an ICO-related business proposition needs to be designed to satisfy the ‘consumer benefit’ condition for access to the FCA’s Innovate facilities.

Christopher Woolard, Executive Director of Strategy and Competition at the FCA, said:

“The original paper opened a discussion about DLT and the volume and breadth of responses we received from the industry demonstrates the significance of this issue. DLT has the potential to transform practices across a number of markets, sharpening competition and improving risk management. At the same time we have to be alive to the risks of certain applications of it. We will continue to work with a range of agencies and firms to ensure a co-ordinated approach to the use of DLT in financial services.”

The UK House of Commons Committee of Public Accounts has published an important report on The growing threat of online fraud (Sixth Report of Session 2017–19).The key observation is that Banks do not accept enough responsibility for preventing and reducing online fraud and there is no data available to assess how well individual banks are performing. Unless all banks start working together, including making better use of technology, there will be little progress on tackling card fraud and returning money to customers.

One key issue is that unlike credit cards, where transactions are automatically refunded in case of dispute, payments made by customers via online banking on their instruction (“authorised push payments”), to a fraudulent destination is not. It has been estimated that between 40% and 70% of people who are victims of scams do not get any money back. Banks are reported to be holding at least £130 million of funds that cannot accurately be traced back and returned to fraud victims, an amount that UK Finance said was probably a conservative estimate.

As the proportion of payments made by digital means continues to rise, stronger safeguards, and clearer account abilities should be placed on the banks. This is not a topic the banks want to discuss. Indeed, in evidence, individual banks know how they compare with others, but told the committee that banks did not publish individual numbers because then the fraudsters would target the ‘weakest’ of the banks. Of course, it might be in the banks’ own interest not to be transparent and publish individual data, as it could deter customers.

They found card not present fraud was significant, and needed to be reduced.

Finally, there was a need for better consumer awareness.

We suspect the situation in Australia is somewhat similar.

In summary, Online fraud is now the most prevalent crime in England and Wales, impacting victims not only financially but also causing untold distress to those affected. The cost of the crime is estimated at £10 billion, with around 2 million cyber-related fraud incidents last year, however the true extent of the problem remains unknown. Only around 20% of fraud is actually reported to police, with the emotional impact of the crime leaving many victims reluctant to come forward. The crime is indiscriminate, is growing rapidly and shows no signs of slowing down. Urgent action from government is needed, yet the Home Office’s response has been too slow and the banks are unwilling to share information about the extent of fraud with customers. The balance needs to be tipped in favour of the customer.

Online fraud is now too vast a problem for the Home Office to solve on its own, and it must work with a long list of other organisations including banks and retailers, however it remains the only body that can provide strategic national leadership. Setting up the Joint Fraud Task in 2016 was a positive step, but there is much still to do. The Department and its partners on the Joint Fraud Taskforce need to set clear objectives for what they plan to do, and by when, and need to be more transparent about their activities including putting information on the Home Office’s website.

The response from local police to fraud is inconsistent across England and Wales. The police must prioritise online fraud alongside efforts to tackle other sorts of crime. But it is vital that local forces get all the support they need to do this, including on identifying, developing and sharing good practice.

Banks are not doing enough to tackle online fraud and their response has not been proportionate to the scale of the problem. Banks need to take more responsibility and work together to tackle this problem head on. Banks now need to work on information sharing so that customers are offered more protection from scams. Campaigns to educate people and keep them safe online have so far been ineffective, supported by insufficient funds and resources. The Department must also ensure that banks are committed to developing more effective ways of tackling card not present fraud and that they are held to account for this and for returning money to customers who have been the victims of scams.

The Bank of England release their Financial Stability Report today, which includes the results of recent stress tests. Though the stress tests show that UK Banks could handle the potential losses in the extreme scenarios, the FPC is raising the UK counter cyclical buffer rate from 0.5% to 1% with binding effect from 28 November 2018. In addition buffers for individual banks will be reviewed in January 2018, to take account of the probability of a disorderly Brexit, and other risk factors hitting at the same time.

They highlighted risks from higher LTI mortgage and consumer lending, and the potential impact of rising interest rates. They still have their 15% limit on higher LTI income mortgages (above 4.5 times). They are concerned about property investors in particular – defaults are estimated at 4 times owner occupied borrowers under stressed conditions! Impairment losses are estimated at 1.5% of portfolio.

Beyond this, they discussed the impact of Brexit, and potential impact of a disorderly exit.

Finally, from a longer term strategic perspective, they identified potential pressures on the banks (relevant also we think to banks in other locations). There were three identified , first competitive pressures enabled by FinTech may cause a greater and faster disruption to banks’ business models than they currently expect; next the cost of maintaining and acquiring customers in a more competitive environment could reduce the scope for cost reductions or result in greater loss of market share and third the future costs of equity for banks could be higher than the 8% level that banks expect either because of higher economic uncertainty or greater perceived downside risks.

Here is the speech and press conference.

The FPC’s job is to ensure that UK households and businesses can rely on their financial system through thick and thin. To that end, today’s FSR and accompanying stress tests address a wide range of risks to UK financial stability. And they will catalyse action to keep the system well‐prepared for potential vulnerabilities in the short, medium and long terms.

In particular, this year’s cyclical stress test incorporates risks that could arise from global debt vulnerabilities and elevated asset prices; from the UK’s large current account deficit; and from the rapid build‐up of consumer credit. Despite the severity of the test, for the first time since the Bank began stress testing in 2014 no bank needs to strengthen its capital position as a result.

Informed by the stress test and our risk analysis, the FPC also judges that the banking system can continue to support the real economy even in the unlikely event of a disorderly Brexit. At the same time, the FPC has identified a series of actions that public authorities and private financial institutions need to take to mitigate some major cross cutting financial risks associated with leaving the EU.

The Bank’s first exploratory scenario assesses major UK banks’ strategic responses to longer term risks to banks from an extended low growth, low interest rate environment and increasing competitive pressures enabled by new financial technologies. The results suggest that banks may need to give more thought to such strategic challenges.

The Annual Cyclical Stress Test

Today’s stress test results show that the banking system would be well placed to provide credit to households and businesses even during simultaneous deep recessions in the UK and global economies, large falls in asset prices, and a very large stressed misconduct costs. The economic scenario in the 2017 stress test is more severe than the deep recession that followed the global financial crisis. Vulnerabilities in the global economy trigger a 2.4% fall in world GDP and a 4.7% fall in UK GDP falls.

In the stress scenario, there is a sudden reduction in investor appetite for UK assets and sterling falls sharply, as vulnerabilities associated with the UK’s large current account deficit crystallise. Bank Rate rises sharply to 4.0% and unemployment more than doubles to 9.5%. UK residential and commercial real estate prices fall by 33% and 40%, respectively. In line with the Bank’s concerns over consumer credit, the stress test incorporated a severe consumer credit impairment rate of 20% over the three years across the banking system as a whole. The resulting sector‐wide loss of £30bn is £10bn higher than implied by the 2016 stress test.

The stress leads to total losses for banks of around £50 billion during the first two years ‐ losses that would have wiped out the entire equity capital base of the banking system ten years ago. Today, such losses can be fully absorbed within the capital buffers that banks must carry on top of their minimum capital requirements. This means that even after a severe stress, major UK banks would still have a Tier 1 capital base of over £275 billion or more than 10% of risk weighted assets to support lending to the real economy.

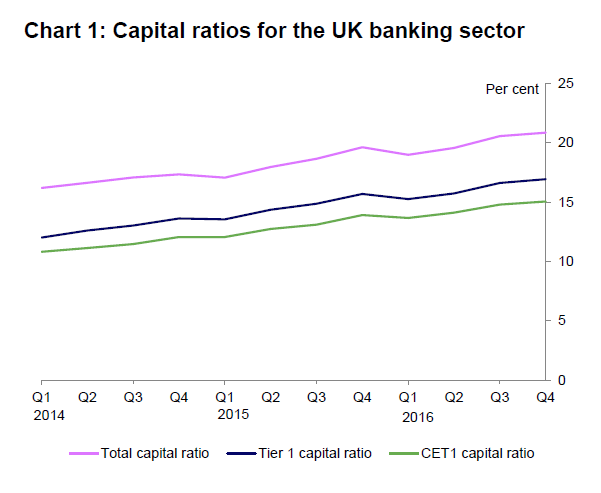

This resilience reflects the fact that major UK banks have tripled their aggregate Tier 1 capital ratio over the past decade to 16.7%.

Countercyclical Capital Buffer

Informed by the stress test results for losses on UK exposures, the FPC’s judgement that the domestic risk environment—apart from Brexit—is standard; and consistent with the FPC’s guidance in June; the FPC is raising the UK countercyclical buffer rate from 0.5% to 1% with binding effect from 28 November 2018. In addition, as previously announced, capital buffers for individual banks will be reviewed by the PRC in January. These will reflect the firm‐specific results of the stress test, including the judgement made by the FPC and PRC in September. These buffers can be drawn on as necessary during a downturn to allow banks to support the real economy.

Brexit

There are a range of possible outcomes for the future UK‐EU relationship. Consistent with its remit, the FPC is focused on scenarios that, even if the least likely to occur, could have the greatest impact on UK financial stability. These include scenarios in which there is no agreement or transition period in place at exit. The 2017 stress test scenario encompasses the many possible combinations of macroeconomic risks and associated losses to banks that could arise in this event. As a consequence, the FPC judges that, given their current levels of resilience, UK banks could continue to support the real economy even in the event of a disorderly exit from the EU.

That said, in the extreme event in which the UK faced a disorderly Brexit combined with a severe global recession and stressed misconduct costs, losses to the banking system would likely be more severe than in this year’s annual stress test. In this case where a series of highly unfortunate events happen simultaneously, capital buffers would be drawn down substantially more than in the stress test and, as a result, banks would be more likely to restrict lending to the real economy, worsening macroeconomic outcomes. The FPC will therefore reconsider the adequacy of a 1% UK countercyclical capital buffer rate during the first half of 2018, in light of the evolution of the overall risk environment. Of course, Brexit could affect the financial system more broadly. Consistent with the Bank’s statutory responsibilities, the FPC is publishing a checklist of steps that would promote financial stability in the UK in a no deal outcome.

It has four important elements:

– First, ensuring that a UK legal and regulatory framework for financial services is in place at the point of leaving the EU. The Government plans to achieve this through the EU Withdrawal Bill and related secondary legislation.

– Second, recognising that it will be difficult, ahead of March 2019, for all financial institutions to have completed all the necessary steps to avoid disruption in some financial services. Timely agreement on an implementation period would significantly reduce such risks, which could materially disrupt the provision of financial services in Europe and the UK.

– Third, preserving the continuity of existing cross‐border insurance and derivatives contracts. Domestic legislation will be required to achieve this in both cases, and for derivatives, corresponding EU legislation will also be necessary. Otherwise, six million UK insurance policy holders with £20 billion of insurance coverage, and thirty million EU policy holders with £40 billion in insurance coverage, could be left without effective cover; and around £26 trillion of derivatives contracts could be affected. HM Treasury is considering all options for mitigating these risks.

– Fourth, deciding on the authorisations of EEA banks that currently operate in the UK as branches. Conditions for authorisation, particularly for systemic firms, will depend on the degree of cooperation between regulatory authorities. As previously indicated, the PRA plans to set out its approach before the end of the year. Irrespective of the particular form of the United Kingdom’s future relationship with the EU, and consistent with its statutory responsibility, the FPC will remain committed to the implementation of robust prudential standards. This will require maintaining a level of resilience that is at least as great as that currently planned, which itself exceeds that required by international baseline standards.

Biennial Exploratory Scenario

Over the longer term, the resilience of UK banks could also be tested by gradual but significant changes to business fundamentals. For the first time, the FPC and PRC have examined the strategic responses of major UK banks to an extended low growth, low interest rate environment combined with increasing competitive pressures in retail banking from increased use of new financial technologies. FinTech is creating opportunities for consumers and businesses, and has the potential to increase the resilience and competitiveness of the UK financial system as a whole. In the process, however, it could also have profound consequences for the business models of incumbent banks. This exploratory exercise is designed to encourage banks to consider such strategic challenges. It will influence future work by banks and regulators about longer‐term issues rather than informing the FPC and PRC about the immediate capital adequacy of participants.

Major UK banks believe they could, by reducing costs, adapt to such an environment without major changes to strategy change or by taking more risk. The Bank of England has identified clear risks to these projections:

– Competitive pressures enabled by FinTech may cause a greater and faster disruption to banks’ business models than they currently expect.

– The cost of maintaining and acquiring customers in a more competitive environment could reduce the scope for cost reductions or result in greater loss of market share.

– The future costs of equity for banks could be higher than the 8% level that banks expected in this scenario either because of higher economic uncertainty or greater perceived downside risks.

Conclusion

The FPC is taking action to address the major risks to UK financial stability. Given the tripling of their capital base and marked improvement in their funding profiles over the past decade, the UK banking system is resilient to the potential risks associated with a disorderly Brexit.

In addition, the FPC has identified the key actions to mitigate the impact of the other major cross cutting issues associated with a disorderly Brexit that could create risks elsewhere in the financial sector.

And on top of its existing measures to guard against a significant build‐up of debt, the FPC has taken action to ensure banks are capitalised against pockets of risk that have been building elsewhere in the economy, such as in consumer credit.

As a consequence, the people of the United Kingdom can remain confident they can access the financial services they need to seize the opportunities ahead.

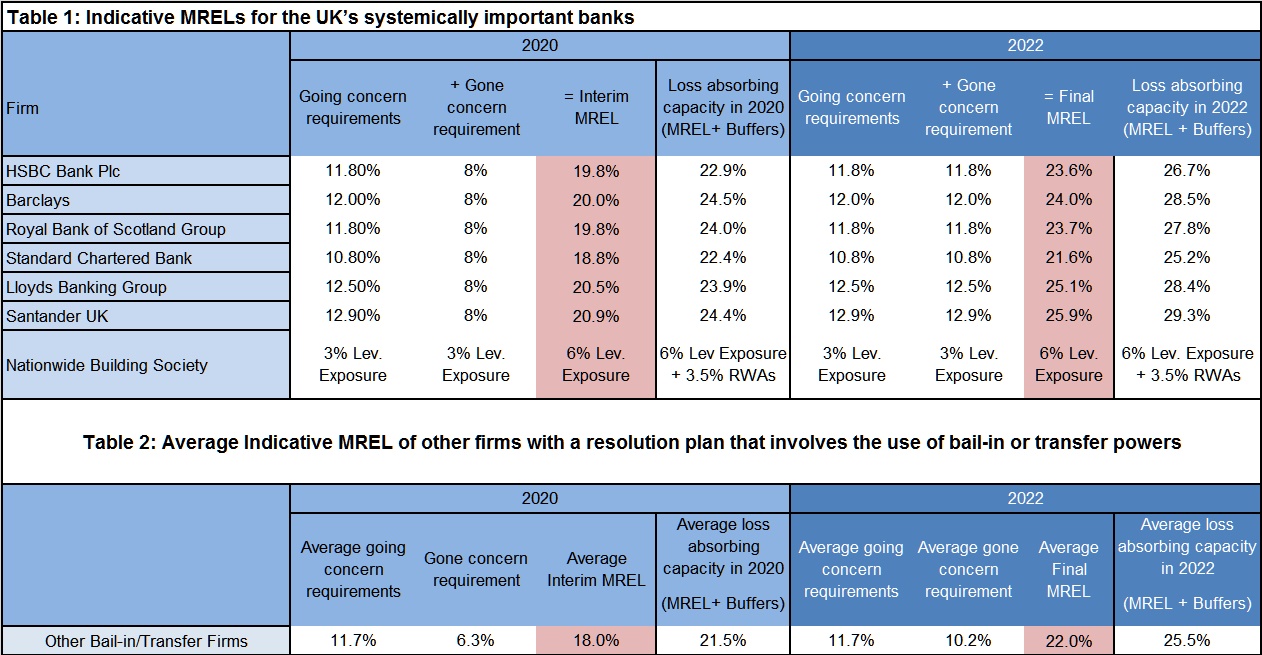

Given the current debate about “Unquestionably strong” banks, it is worth reading the Bank of England’s approach to minimum loss-absorbing capacity these institutions must hold, and how it can comprise both ‘going concern’ and ‘gone concern’ resources.

These rules represent one of the last pillars of post-crisis reforms designed to make banks safer and more resilient, and to avoid taxpayer bailouts in future. Banks are now required to hold several times more loss-absorbing resources than they did before the crisis, while annual stress tests check firms’ resilience to severe but plausible shocks. Banks are now also structured in a way that supports resolution. The Bank of England now has the legal powers necessary to manage the failure of a bank, and significant progress has been made to ensure there is coordination between national authorities should a large international bank fail.

The new rules will be introduced in two phases. Banks will be obliged to comply with interim requirements by 2020. From 1 January 2022, the largest UK banks will hold sufficient resources to allow the Bank of England to resolve them in an orderly way.

What is MREL?

MREL is a critical part of a resolution strategy. It determines the minimum loss-absorbing capacity these institutions must hold, and it can comprise both ‘going concern’ and ‘gone concern’ resources.

Going-concern resources, typically in the form of common equity, absorb losses in times of stress and ensure that a bank can keep operating and that it can maintain the supply of credit to the economy.

Gone-concern resources, typically in the form of debt, absorb losses when a bank undergoes resolution or is placed into insolvency.

Smaller institutions that provide banking activities of a scale that means that they can be allowed to go into insolvency if they fail, will satisfy MREL by simply meeting their minimum regulatory capital requirements as a going concern. There is no gone-concern requirement for these firms. More detail on the capital framework for bank capital is set out in the Supplement to the December 2015 Financial Stability Report.

But larger banks and building societies with a size or functions that mean they have a resolution plan involving the use of the Bank’s resolution tools will be required to hold additional MREL beyond their going-concern requirements.

In addition, firms are expected to hold going-concern capital buffers on top of these requirements. The buffers are calibrated to recognise systemic importance or idiosyncratic exposures, and are intended to be used so that banks can absorb losses without breaching minimum requirements. As these capital buffers are not permitted to count towards meeting MREL, they add to the total loss-absorbing capacity of each bank.

How much MREL must larger firms hold?

The MREL for large firms is needed in a resolution both to absorb losses and to recapitalise their continuing business. Our policy is that from 1 January 2022 they should be required to hold both their going-concern requirements together with additional MREL of an amount equal to those going concern requirements. In other words, their MREL will be two times their going-concern requirements.

These UK firms will become subject to interim requirements on 1 January 2020, prior to the final requirements coming into force in 2022. We will review our approach to calibration of the 2022 MREL for all firms before the end of 2020, before we set final MRELs. In doing so, we will have particular regard to any intervening changes in the UK regulatory framework, as well as institutions’ experience in issuing liabilities to meet their interim MRELs.

Table 1 below provides the estimates of the interim and final consolidated MREL requirements that we have sent to each of the UK’s global and domestic systemically important banks. As a firm’s MREL will depend upon its going concern requirements in a particular year, these 2020 and 2022 MRELs are simply indicative and are based on the calibration methodology set out in our Statement of Policy, with reference to the firms’ minimum capital requirements and balance sheets as at December 2016.

In addition to the global and domestic systemically important UK banks, there are eight other UK banks and building societies that currently have a resolution plan that involves the use of resolution tools by the Bank (rather than reliance on the insolvency regime). These are:

Clydesdale Bank

The Co-operative Bank

Coventry Building Society

Metro Bank

Skipton Building Society

Tesco Bank

Virgin Money

Yorkshire Building Society.

Table 2 provides the average of the indicative 2020 and 2022 MRELs and total requirements for these other firms.

We have provided an average for these firms as publishing MRELs for each of them would also reveal the firm-specific element of their capital assessments, many of which have not previously been disclosed. Accordingly, the Prudential Regulation Authority will consider its disclosure policy and undertake the appropriate consultations before a final decision on publishing individual MRELs for these firms is taken.

The Co-operative Bank has been excluded from the calculation of the average because the firm is currently seeking a sale, which has the potential to significantly affect The Co-operative Bank’s balance sheet. Therefore an indicative MREL based on The Co-op’s balance sheet today may not be a useful guide to the eventual requirement.

Lloyds Bank intends to shrink hundreds of its UK branches due to growing numbers of customers using online banking, according to a BBC report.

Its new “micro-branches” will have no counters and just two staff carrying mobile tablets, who will help customers use in-store machines, such as pay-in devices.

The new “micro” format will use much less space than existing branches, in some cases as little as 1,000 square feet.

The bank said the reason for the move was a “profound change in customer behaviour” which has seen growing numbers of transactions move online.

Some of the branches being converted will be Halifax and Bank of Scotland branches.

Jakob Pfaudler, Lloyds’ chief operating officer for retail, told the BBC: “We have a lot of branches that used to have a lot of footfall, and therefore feel quite empty and intimidating for customers. So when there’s too much space we may board up places in existing branches.”

In 2014, Lloyds announced a separate plan to close 400 branches over three years, with the loss of 9,000 jobs. It will have 1,950 left in the UK by the end of 2017.

The latest release from the Bank of England shows that the common equity Tier 1 (CET1) capital ratio for the UK banking sector increased by 0.3 percentage points (pp) on the quarter to 15.1%, 1.1 pp higher than in Q4 2015.

The quarterly increase was driven by small movements in both the level of CET1 capital (increase) and in the level of total risk-weighted assets (decrease).

The reduction in risk-weighted assets was driven by small decreases in most risk categories.