Please consider supporting our work via Patreon ;

Please share this post to help to spread the word about the state of things….

/

RSS Feed

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

The latest edition of our weekly digest of property and finance news with a distinctively Australian flavour

Please consider supporting our work via Patreon ;

Please share this post to help to spread the word about the state of things….

Welcome to the Property Imperative Weekly to 1st September 2018, our digest of the latest finance and property news with a distinctively Australian flavour. Locally the bad news keeps coming, while US markets remain on the boil.

And by the way, if you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

And by the way, if you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

Listen to the podcast, read the transcript, or watch the video show.

NineNews published an article this week, claiming that Sydney and Melbourne dwelling values “may soon rise again” because of a decline in dwelling construction, citing a report saying that the rate of construction is expected to slow down, with the number of new homes built set to fall by up to 50,000 each year. So they said, that would mean 20,000 fewer homes built across the country each year than the 195,000 needed to meet future demand.

Indeed, the ABS reported this week that building approvals in July were 5.6 per cent lower than in the same month last year. Total seasonally adjusted dwelling approvals in July fell in New South Wales (-5.2 per cent), Victoria (-4.6 per cent), Queensland (-6.0 per cent), South Australia (-26.5 per cent) and Western Australia (-14.7 per cent). Seasonally adjusted approvals increased in Tasmania by 13.6 per cent. In trend terms, total dwelling approvals in July increased by 4.5 per cent in the Northern Territory and in the Australian Capital Territory (12.2 per cent).

The data shows its high rise apartments which are slowing the fastest (in response to slowing demand from investors) but it is worth noting that the volume of approvals for new detached houses have been tracking around their strongest levels in 15 years. The HIA said that weaker conditions in a number of states have typically been overshadowed by strong activity in Victoria. With Victorian home approvals now showing signs of weakness they expect the national trend – of declining building approvals – will continue throughout 2018.

The HIA also reported on new home sales for July, saying that consistent with the trend for much of 2018, July saw sales fall by 3.1 per cent compared to the previous month. Sales in 2018 thus far are 6.1 per cent lower than in the corresponding time in 2017. The noticeable new trend is that new home sales in Victoria are weakening. Victoria has experienced exceptionally strong conditions, which have been sustained over a number of years, obscuring weaker conditions in a number of other states. With Victorian new home sales now showing signs of weakness we expect the national trend – of declining sales – will continue throughout 2018.

The Sydney market has also been cooling throughout the year particularly in the new growth areas. The high volume of new apartments in metropolitan cities are competing for first home buyers and resulting in a slowdown in new detached home sales. Other regions in New South Wales, such as the Hunter, around the ACT and South and North Coasts, are continuing to see strong growth. They say the market for new home sales across the country is cooling for a number of reasons including a slowdown in inward migration since July 2017, constraints on investor finance imposed by state and federal governments and falling house prices. They expect that it will continue to slow over the next two years due to the adverse factors now starting to take effect the market.

Specifically, they say that finance has become increasingly difficult to access for home purchasers. Restrictions on lending to investors and rising borrowing costs have seen credit growth squeezed. Falling house prices in metropolitan areas have also contributed to banks tightening their lending conditions which have further constrained the availability of finance. An increase in interest rates charged by banks, which had been anticipated, will accelerate the slowdown in sales and ultimately new home building activity.

The latest data from the RBA and APRA confirm the fall in credit, with the monthly RBA credit aggregates for July showing total credit for housing up 0.2% in the month, to $1.77 trillion, with owner occupied credit up 0.5% to $1.18 trillion and investment lending down 0.1% to $593 billion. Investment housing credit fell to 33.4% of the portfolio, and business credit was 32.5%. APRA’s data showed that investor loan balances at Westpac, CBA and ANZ all falling, while NAB grew just a tad. Macquarie, HSBC. Bendigo Bank and Bank of Queensland grew their books, highlighting a shift towards some of the smaller lenders. Suncorp balances fell a little too. You can watch our separate video “Rates Up, Lending Down”, for more on this.

And of course we saw more out of cycle rates hikes from Westpac, who lifted variable rates for owner occupies and investors holding loans with them by 14 basis points – see out video “Westpac Blinks” for more on this – where we discuss the margin compression the experienced, thanks to rising international funding rates (see the BBSW) and the switch from interest only to principal and interest loans. Then on Friday, Suncorp and Adelaide Bank, both of whom had already lifted a couple of months back, lifted again. As I said yesterday, what is happening here is that funding costs are indeed rising. But the real story is that they are also running deep discounted rates to attract new borrowers, (especially low risk, low LVR loans) and are funding these by repricing the back book. This is partly a story of mortgage prisoners, and partly a desperate quest for any mortgage book growth they are capture. Without it, bank profits are cactus. Once again customer loyalty is being penalised, not rewarded. Those who can shop around may save, but those who cannot (thanks to tighter lending standards, or time, or both) will be forced to pay more

Damien Boey at Credit Suisse, writing before Suncorp And Adelaide Bank moved again said Westpac was the latest of the banks to hike variable rates across new and existing customers, following similar moves from BOQ, BEN, MQG and SUN over the past few months. Not only are out of cycle rate hikes broadening out across the system – we think that they will continue to broaden out across the majors, and become a recurring theme. This is because:

Even after some banks have hiked rates out of cycle, we still think that in aggregate there are more than 50bps of variable rate mortgage hikes in the pipeline based on already known developments in the money market. But the RBA only has 1.5% worth of rate cut ammunition left in its bag of tricks.

This means that the RBA has lost some autonomy over the monetary transmission mechanism, because effective borrowing rates can rise independently of the cash rate. In particular, Australian-US yield differentials are likely to further invert, undermining the carry trade appeal of the AUD/USD. The Fed still seems quite determined to hike rates. But the RBA is unlikely to be matching the Fed’s hawkishness given the slowdown in train, and given what the banks are doing to rates and credit supply.

So we are in for a period of more out of cycle rate rises, as well as tighter lending standards. No surprise, then that refinance rejections are rocketing, as we reported this week, and mortgage prisoners are getting locked in. The ABC story even got picked up by ZeroHedge in the US.

So back to that NineNews report, they missed completely the real reason why home prices are falling, it’s all about credit availability. Lending standards are tighter now – borrowing power is reduced, and so new loans are only available on tighter terms. If you want to understand the link between credit and home prices, which is still not widely understood, I recommend you watch my recent conversation with Steve Keen, who explains the mechanisms involved, and the policy failures behind them. See “Are Icebergs Fluffy? … A Conversation with Steve Keen”. This show has already become one of the most popular in the site, and it is really worth a watch.

The upshot though is home prices are likely to continue to fall. CoreLogic’s dwelling price index showed another fall in August, recording a 0.38% decrease in values at the 5-city level. This is the 11th consecutive monthly decline in home values, down a cumulative 3.4% over that period at the 5-city level: Quarterly values also fell another 1.3% In the year to August, with home values down by 3.09% at the 5-city level, driven by Sydney (-5.64%). Significantly, Perth’s housing bust continues to roll on, with dwelling values now down 13% since peaking in June 2014 after falling another 0.6% in August: the cumulative loss in values at 13% is greater than the 11.5% peak-to-trough falls experienced between 2009-09, and the duration of the downturn has hit 50 months – more than twice as long as prior downturns. Plus, rents there have similarly fallen, with median asking rents down 29% for both houses and units since June 2013.

My theory is, where Perth has gone, other centres are likely to follow as the great property reset rolls on. Melbourne and Victoria is deteriorating significantly, and remember there net rental yields are some of the lowest across the country. No, prices are not likely to recover anytime soon.

And if you want further evidence, auction clearance rates remain in the doldrums. It is interesting to see now the main stream media is beginning to talk about this, and I have been busy this week with interviews on Radio Melbourne, 2GB and elsewhere. Remember this is only the end of the beginning. I continue to believe 2019 will be a really bad year, what with more rate hikes, interest only loan switches, and decaying sentiment. As one industry insider told me this week, “some of my property investor clients have decided to try and sell before the falls bite”. It may be too late.

And to add to the mix, ABC’s Michael Janda wrote an excellent piece this week on the advantage some large banks have with regard to how APRA assesses their capital base. The big four banks between them hold around 80 per cent of all Australian home loans. There are many factors that have led to this extreme market dominance: economies of scale, better credit ratings and an implicit Federal Government guarantee — all of which are linked. But the major banks — plus Macquarie and, recently, ING — also enjoy a regulatory benefit that is little known outside the financial sector, but provides a substantial competitive advantage. “The average capital risk weights of the standard banks is around 39 per cent, the major banks average around 25 per cent, and the actual cost [difference] of that equates to around 15 basis points in margins, so it’s not insignificant at all,” the chief executive of second-tier lender ME Bank, Jamie McPhee, told The Business. Those 15 basis points, or 0.15 percentage points, either have to be added onto the interest rate of mortgages that ME Bank and other smaller lenders offer or they take a hit to their profit margins.

For regional banks on the “standardised” system, the safest high-deposit, fully documented housing loans are considered just 35 per cent at risk, meaning they only have to hold $35,000 in capital on $1 million home loan. However, the major banks, plus Macquarie and ING, are allowed to set their own risk weights, using internal financial modelling under the internal ratings-based (IRB) approach. Until the Financial System Inquiry (FSI) there was no floor on how low these could be — a couple of the major banks were averaging less than 15 per cent on mortgages, meaning they held less than $15,000 in capital to protect against losses on $1 million home loan. Smaller banks have ‘disadvantage baked in’. However, on recommendations from that inquiry, the bank regulator APRA introduced a floor of 25 per cent on the average mortgage risk weight for these banks. That still leaves a significant difference between the amount of capital the big banks hold and what the smaller banks have to put aside.

APRA continues to argue that these more sophisticated banks deserve benefit from their investment in more advanced management systems, and yet APRAs recent reviews suggest significant issues. Here is a recent discussion between Senator Whish-Wilson and APRA Chair Wayne Byers discussing in a Senate committee hearing in May the outcomes from their targeted reviews of major bank lending practices in 2017, but only released publicly through the royal commission process earlier this year.

This casts doubt on whether the big four actually live up to the theory of having better risk assessment and management than the smaller banks. Is APRA still captured we ask, and should the playing field be levelled. We continue to think so.

So now to the markets. Locally, Bendigo and Adelaide Bank fell 0.26% on Friday to 11.59, Suncorp rose 0.06% to 15.49, Westpac fell 0.38% to 28.54, well down from a year ago, despite the mortgage rate hike, and CBA fell 1.26% to 71.24. More are getting negative on the banks, given recent events. The ASX 200 fell 0.51% to 6,319, just off its highs, as the financial sector fell away. The Aussie continues to fall against the US dollar, down a significant 0.96% to 71.93, and we continue to expect more weakness ahead.

Sentiment is rather different in the US markets, with the 10-year rate still elevated, and the gap to the 3 month Libor very narrow, as we discussed before a potential harbinger of a recession later. But the US stock markets remain in positive territory. The Dow Jones Industrial Average fell 0.09% to 25,964, still below its peak in February. The S&P 500 passed a new record in the week, and ended on Friday at 2,901. The VIX was down again, falling 4.95% to 12.87, indicating the market is risk off at the moment. The US Dollar Index Futures was up 0.43% to 95.05.

That said, the burst of optimism about trade in the market during the week, didn’t last until the closing bell on Friday. The U.S. announced a bilateral deal with Mexico on Monday. But tension built throughout the week as the U.S. announced there was a Friday deadline to bring Canada into a newly-revamped NAFTA. The U.S. and Canada missed that deadline, but announced that talks would resume next Wednesday, leaving the market facing more wait-and-see trading days. There was also drama during Friday’s discussions after the Toronto Star reported that Trump told Bloomberg off the record he had no plans to give any concessions at all to Canada. The president appeared to later confirm that stance in a tweet, saying Canada now knows where he stands.

Trade worries spread beyond North America, though. Trump told Bloomberg he was prepared to withdraw from the WTO if necessary. And he plans to move ahead with tariffs on $200 billion in Chinese imports as soon as a public-comment period concludes next week. China’s foreign ministry said Friday that the U.S. putting pressure on Beijing would not work.

The Yuan rose a little against the US Dollar, but remains way down on a year ago.

Meantime retail earnings dominated the calendar this week, leading to strong stock movements in the low-volume environment. The S&P Retail index ended up slightly for the week.

Among big movers, Abercrombie & Fitch stock plummeted on second-quarter revenue and same-store sales missed estimates. Best Buy stock tumbled despite better-than-expected second quarter revenue and earnings as online sales slowed and the company warned that it is “expecting a non-GAAP operating income rate decline in the third quarter.” And Tiffany & Co spiked on second-quarter results and strong outlook, but then tumbled in later sessions.

In tech, Tesla shares started the week with a quick drop and finished it lower as it scrapped plans to go private. CEO Elon Musk wrote in a blog late last week that he would not move forward with a plan to take the company private, noting that after speaking with retail and institutional shareholders that “the sentiment, in a nutshell, was ‘please don’t do this.’”

Musk had surprised the market out of the blue, tweeting he was thinking of taking the company private at $420 per share and had funding secured. The SEC was interested in whether the tweet was designed in a way to punish short sellers, according to reports.

The NASDAQ rose 0.26% to 8,109.5 in record territory driven by the booming sector.

Data out this week illustrated two contrasting segments of the U.S. economy, one stronger and one weaker. Economic indicators on the consumer side remained very strong. The Conference Board’s index of consumer confidence increased to 133.4 this month, compared to a reading of 126.7 forecast by economists. That was its highest level since October 2000. The University of Michigan’s August consumer confidence index was revised up to 96.2 from its preliminary measure of 95.3. And consumer spending, which accounts for more than two-thirds of U.S. economic activity, rose 0.4% last month, matching June’s reading and analyst forecasts.

But the National Association of Realtors said its pending home sales index, which measures signed contracts for homes where transactions have not yet closed, fell 0.7% to a reading of 106.2 after rising by a revised 1.0% in the previous month. Economists had forecast pending home sales rising 0.3% last month. So more questions on the housing sector ahead.

Oil closed out the month higher as traders balanced expectations of crude supply losses with the potential of trade wars denting global demand. China, the world’s largest commodity importer, has seen economic growth dwindle since the trade war with the U.S. kicked off, and a further escalation could dent growth, forcing Beijing to rein in crude imports. Oil prices ended the month nearly 2% higher on bets on renewed global supply shortage as U.S. sanctions on Iran’s crude exports are expected to reduce crude from market, underpinning higher crude prices. Both WTI and Brent crude are expected gain on a potential slump in Iranian exports, although gains in WTI prices will be limited as the refinery maintenance season is set to get underway. Oil prices were helped earlier in the week by an EIA report showing crude oil stockpiles fell much more than expected.

Gold moved a little higher this week, ending up 0.16% on Friday to 1,206, Bitcoin lifted 1.23% to 7,029

So, we can see a significant divergence between the local market here, dragged down by negative sentiment on banks and housing (and the increasing realisation of more issues ahead) and the US where stocks are at the highs despite the building risks from higher corporate debt and the yield curve inversion.

The two markets are poles apart.

The latest edition of our weekly finance and property news digest with a distinctively Australian flavour.

Please consider supporting our work via Patreon

Please share this post to help to spread the word about the state of things….

The latest edition of our weekly finance and property news digest with a distinctively Australian flavour.

Please consider supporting our work via Patreon

Please share this post to help to spread the word about the state of things….

Welcome to the Property Imperative weekly to 25th August 2018, our digest of the latest finance and property news with a distinctively Australian flavour. And what a week it was…

By the way, if you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

Watch the video, listen to the podcast or read the transcript.

Scott Morrison, the new PM must carry much of the burden for our current economic situation, which to my mind is sliding by the day. Booming debt and flat wages have combined to drag way too high home prices lower, as the number of SME’s feeling the pressure continue to rise. Sprooking high jobs growth (measured on a simplistic basis which does not report underemployment, accurately) and in an environment where the cpi for real households is much higher than the quoted number means the GDP is likely to flag, as the Aussie continues to slide against the US. The bears are it seems out in force now. You can watch my discussion with John Adams, recorded before the spill “Is Parliament Fiddling While Rome Burns” for the political context.

We expect some unnatural acts from the new man, perhaps with first time buyers offered the chance to tap into super to “buy now” and probably overt attempts to trim migration ahead of the election ahead. Remember Morrison spent time at the Property Council, so he is so to speak, pro-property, and pro-property investment – thus the debt bubble may grow further and investors enticed back, at least to some extent. This means a harder fall if or when Labor sweeps to power as the property market turns to custard, what a nice incoming present.

And analysts seem to agree the bears are out. For example, Damien Boey at Credit Suisse says that in the year-to-2017, the Australian population grew by 388,056 people to 24,782,303 residents. According to the 2016 Census, the average number of people per household is 2.57894. Assuming this number remained steady throughout 2017 (an optimistic assumption), household formation was about 150,471 (388,056 divided by 2.57894). Now it is possible for replacement housing demand to rise as high as 25,000 per annum. Therefore, an optimistic estimate of underlying housing demand is around 175,000 per annum. This is below the current level of dwelling completions of around 210,000 per annum. In other words, Australia is in a situation of marginal housing oversupply to the tune of 35,000 per annum. Consistent with this state, house prices are falling moderately. However, it is now possible that marginal oversupply could become worse, due to changes in the political climate. For example, former Prime Minister Abbott, representing the shadow conservative wing of the ruling Liberal Party, has advocated in the past that he would like to cut immigration by up to 80,000 per annum. If the immigration intake is cut by 80,000 per annum, household formation would fall to 119,451 per annum, and underlying housing demand would fall to 144,450 per annum. At the current level of dwelling completions, this would increase marginal housing oversupply to 65,549 per annum, consistent with much faster house price declines. A 40,000 per annum cut to the immigration intake result in a 50,039 per annum housing glut. On top of all of this, we need to consider the risk that if the Liberal Party loses the next election, and the Labour government wins a majority, the new government would attempt to grandfather out negative gearing provisions for investment properties.

Boey does not include the tighter credit environment and high debt which is, as we discussed in this week’s live stream event, crimping households’ ability to borrow. In fact, this is the strongest negative impact on home prices, which is why we revised down our four economic scenarios, such that we think there is only a 5% probability of the RBA’s forecast for the economy playing out. All our other scenarios are more bearish. You can watch the full event on YouTube, including the chat during the session, we had more than 300 watch live on Tuesday. Our next event will be on the 18th September at 20:00 Sydney, and its already scheduled on the channel if you want to set a reminder.

We expect the next RBA rate move to be down, not up, whilst both Barclays and RBS this week pushed out their expectation of a potential cash rate rise from the RBA, due to weaker economic conditions to late 2019 or 2020.

Home prices continue to run lower, as the latest data from CoreLogic shows, with year to date falls of 3.44% in Sydney, and 3.29% in Melbourne, plus a fall of 1.95% in Perth. But also of note is that prices are now falling faster in Melbourne, down 0.59% this month so far, compared with 0.23% in Sydney. And auction clearance rates continue to languish, as more properties remain on the books for sale.

Of course, values are still up 35.3% since the 2010 peak at the 5-city level, driven overwhelmingly by exceptionally strong gains in Sydney at 58.5% and Melbourne 40.4%. But there has been little movement elsewhere (and in fact down in inflation-adjusted terms). And remember the CoreLogic index is driven by settlement data which is weeks behind transactions themselves.

CoreLogic also showed that as well as fewer seven-figure sales occurring now as values decline, the volume of more affordable homes selling is also falling. Their analysis shows that the share of sales under $400,000 homes has continued to decline over the past year. Nationally, 29.2% of all houses and 34.6% of all units sold over the 2017-18 financial year transacted for less than $400,000. The share of sales below this price point has fallen from 30.7% for houses and 35.4% for units a year earlier. The share of sales below $400,000 has increased slightly over the past few months for both houses and units.

An historic low 13.9% of combined capital city house sales and 25.8% of capital city unit sales were under $400,000 over the 2017-18 financial year. The share of sales below $400,000 has fallen over the year from 16.2% of houses and 27.1% of units. Although capital city dwelling values are falling, there continues to be fewer sales occurring below the $400,000 threshold.

The share of sales below $400,000 is predictably much larger across regional areas of the country than within the capital cities. Over the latest financial year, 49.6% of all regional house sales and 57.3% of all unit sales were for less than $400,000. House sales under $400,000 were at a record low and down from 51.6% the previous year while unit sales under $400,000 have increased over recent months but are lower than the 58.0% a year earlier.

Then consider falling rental yields. The AFR reported that Andreas Lundberg from Montgomery Investment Management believes that the sagging yield on residential rental properties in Sydney could drive prices lower if investors seek higher yields without an increase in rents. Sluggish rental growth is weakening the income-generating prospects of property, giving buyers another reason to avoid the asset class and potentially forcing prices to fall further. Such a “de-rating” of residential property is not out of the realm of possibility. “In a rational market, rental yield should drift higher but don’t think it’s a rational market. Mr Lundberg said official data showed property rental yields in Sydney are about 2.7 per cent – well below the long-term average of 4 per cent. “In an environment where rates are no longer falling and indebtedness is very high, rental yields should become a more important consideration in where you should invest your money,” he said.

If you look at Sydney, the annual fall in rental rates is significant, according to CoreLogic data. This is one reason why property investors are, and will continue to head for the exits. Rental yields remain the lowest in Melbourne (3.04%) and Sydney (3.21%) which, given the dim prospects for capital growth and tougher credit conditions, is likely to act as a further disincentive to investors in these markets and help push prices even lower. Labor’s proposed negative gearing and capital gains tax reforms will also add to the downward pressures.

We discussed the state of the property market in a prerecord for Nines’ Sixty Minutes to be broadcast in a few weeks. You can see my video blog which tells the story of the days filming “Talking Finance and Property On Channel Nine”.

Building Company Lend Lease, in their results, which were strong, specifically called out that they were preparing for Australia’s housing slowdown. “We have been participating in a slowdown for some time and most markets are past their peak,” The Group Chief Executive Steve McCann said. Presold lots in its big residential communities slowed to 3,231 lots in financial 2018 from 3,896 in the previous corresponding period. Their sales were down -17% year on year. Their share price is off its highs but up 24% over the past year. As building approvals are still pretty strong, perhaps Lend Lease market share is lower here now. That said, they are still holding a huge land bank and have diversified from residential building. They can afford to wait for the next property boom, down the track.

Westpac’s quarterly update was a salutary lesson in what’s happening in their mortgage book. The biggest property investor lender in the country reported that its net interest margin in June quarter 2018 was 2.06% compared to 2.17% in First Half. The 11bp decline mostly reflected higher funding costs and a lower contribution from the Group’s Treasury. We discussed this in more detail in our post “Through The Westpac Looking Glass” but the primary source of higher funding costs has been the rise in short term wholesale funding costs as the bank bill swap rate (BBSW) increased sharply since February. Every 5bp movement in BBSW impacts the Group’s margins by around 1bp and compared to 1H18, BBSW was on average 24bps higher in 3Q18, reducing the Group’s net interest margin by 5bps. As well as reduced Treasury activity of 4 basis points, 2 basis points came from the ongoing changes in the mix of the mortgage portfolio (less interest only lending) along with lower rates on new mortgages. Deposit pricing changes only had a small impact on margins in 3Q18. And finally, while overall credit quality was fine, mortgage 90+ day delinquencies in Australia were up 3bps over the three months ended June 2018 with most States recording some increase.

So we see the pincer movements at work, deep discounting to try to attract new business, a switch from interest only loans, reducing interest take, a hike in funding costs and higher delinquencies. Combined these forces are enough to put considerable pressure on the bank, as well as others in the sector. Their share price fell 2.43% on Friday to 27.66, just above their 12-month low of 27.30 in June. We see more downside than upside in the banking sector and remember the Royal Commission is still grinding away.

In comparison CBA, the largest owner occupied lender was up 0.2% to 70.89 on Friday. The ASX 200 ended the week at 6,247, up a little on Friday after the ructions in Canberra this week, but below its recent highs. Again, we see more downside than upside.

The Aussie against the US Doller ended at 73.26, up 1.08% on Friday. Looking at the daily chart, AUD/USD was at one-point climbing back into its familiar consolidation range from June. By the close of play, it remains right on the May 2017 low. That was also its largest daily gain since June 4th. From a bigger picture, its dominant downtrend since February still remains in play. But for now, the pair may consolidate between near-term resistance and support. The former is around 73.82 or the August 21st high. A push above that exposes a descending resistance line composed of the July and August highs. This line also intersects the February trend, making for a potentially stubborn area of resistance. In the event Aussie Dollar pushes above that and potentially reverses its significant progress to the downside, we may eventually get to the June 6th high at 76.77.

On the other hand, immediate support is at 72.38 which is the low set on Friday. A descent under that then exposes the current 2018 low at 72.03. Continuation of AUD/USD’s dominant downtrend would then involve getting beyond the December/May 2016 lows between 71.60 and 71.45. We think the longer term trajectory will be lower as the local economy slows further. The risk is there to go below 70 cents ahead.

Across to the US markets, where the bull market is still running. The Dow Jones Industrial ended up 0.52% to 25,790, up 0.52% on Friday, still below its February highs. But the Benchmark S&P 500 stock index clinched its longest bull-market run on Friday, closing above its previous January high, as Federal Reserve Chairman Jerome Powell affirmed the U.S. central bank’s current pace of rate hikes.

The S&P had last reached a new closing high on Jan. 26, then retreated more than 10 percent, a correction that lasted until Feb. 8. Friday’s new closing high confirmed that the index’s bull run remained intact. Speaking at a research symposium in Jackson Hole, Wyoming, Powell said the Fed’s gradual interest rate hikes were the best way to protect the economic recovery, maintain strong job growth and keep inflation under control. His comments did little to change market expectations of a rate hike in September and perhaps again in December. Investors said they were reassured that Powell’s comments stayed in line with previous commentary from the Fed regarding policy. Economic data also boosted sentiment. New orders for key U.S.-made capital goods increased more than expected in July and shipments growth held firm, the Commerce Department said. The index was up 0.62% to 2,875.

However, Housing numbers continue to give the market pause. It’s recently been the part of the economy waving the most red flags. Data on existing home sales released by the National Association of Realtors on Wednesday showed a surprise drop. Existing home sales fell 0.7% in July from the previous month to an annualized pace of 5.34 million units. Economists had forecast a 0.6% increase to an annualized pace of 5.44 million. Sales are now 1.5% below a year ago and have fallen on an annual basis for five-straight months, according to NAR, especially at the lower end of the market. The report also showed that the median existing-home price for all housing types in July was $269,600, up 4.5% from July 2017 ($258,100). July’s price increase marks the 77th straight month of year-over-year gains. In addition, new home sales fell short, dropping to a nine-month low in July. New home sales fell 1.7% last month to an adjusted annual rate of 627,000 units. Economists expected a rise to 645,000 units.

And Moody’s highlighted that once again at the late stage of a cyclical boom, there are signs of excessive risk taking. This time, the most serious developing threat to the current cycle is lending to highly leveraged nonfinancial businesses. While businesses appear to be in good shape in aggregate, a significant number of highly leveraged companies are taking on sizable amounts of debt. This is evident in the rapid growth of so called leveraged loans—loans extended to companies that already have considerable debt. These loans tend to have floating rates—typically Libor plus a spread—with a below-investment-grade (Baa or less) rating.

Leveraged loan volumes are setting records, and loans outstanding have increased at a double-digit pace over the past five years to nearly $1.4 trillion. Businesses use the loans to finance mergers, acquisitions and leveraged buyouts, followed by refinancing, and to pay for dividends, share repurchases and general expenses.

Powering leveraged lending is demand from the collateralized loan obligation market. CLOs are leveraged loans that have been securitized, and global investors can’t seem to get enough of them. This is clear from the thin spreads between CLO yields and comparable risk-free Treasuries.

Approximately one-half of leveraged loans currently being originated are packaged into CLOs, with CLO outstandings approaching $550 billion.

To meet the strong demand for leveraged loans from the CLO market, lenders are easing their underwriting standards. According to the Federal Reserve’s survey of senior loan officers at commercial banks, a net 15% of respondents say they lowered their standards on commercial and industrial loans to large and medium-size companies this quarter compared with the previous quarter. The only other time loan officers eased as aggressively on a consistent basis was at the height of the euphoria leading up the financial crisis in the mid-2000s. Standards for loans to small companies have not eased nearly as much, since they are much less likely to be bundled into a CLO.

Considering the leveraged loan and junk corporate bond market together, highly indebted nonfinancial companies owe about $2.7 trillion. Their debts have been accumulating quickly as creditors have significantly eased underwriting standards. As interest rates rise, so too will financial pressure on these borrowers. Despite all this, global investors appear sanguine, as credit spreads in the CLO and junk corporate bond market are narrow by any historical standard.

Regulators are undoubtedly nervous—they issued guidance to banks to rein in their leveraged lending in 2013—but an increasing amount of the most aggressive lending is being done by private equity, mezzanine debt, and other institutions outside the banking system and regulators’ purview.

Now consider that subprime mortgage debt outstanding was close to $3 trillion at its peak prior to the financial crisis. Insatiable demand by global investors for residential mortgage securities drove the demand for subprime mortgages, inducing lenders to steadily lower their underwriting standards.

Subprime loans were adjustable rate, which became a problem in a rising rate environment as borrowers didn’t have the wherewithal to make their growing mortgage payments. Regulators were slow to respond, in part because they didn’t have jurisdiction over the more egregious players.

It is much too early to conclude that nonfinancial businesses will end the current cycle in the way subprime mortgage borrowers did the previous one. Even so, while there are significant differences between leveraged lending and subprime mortgage lending, the similarities are eerie.

We will make a longer post later on this important issue, but it does highlight that even amid the booming US markets, the bears are stalking their prey.

Finally, to round out our review, the fear index – the VIX was lower, down 3.38% to 11.99 on Friday, Gold was higher, up 1.53% to 1,213, though still well down across the year and Bitcoin ended the week at a slightly higher 6,722, up 3.5% on Friday though just one day after the U.S. Securities and Exchange Commission (SEC) rejected proposed rule changes for nine bitcoin ETFs, the Commission initiated a review of all related decisions. As a result, three rejection orders made on August 22 are now stayed pending the review by the SEC Chairman and the Commissioners. This is the first time the SEC initiated a review of its staff decisions on bitcoin ETFs. Their initial rejections were driven by concerns about the underlying markets so this just might indicate a change of view. Bitcoin of course is way off its highs of more than 18,000, but this might just signal a change in sentiment. We will see.

So in summary, the Bears are in town!

Welcome to the Property Imperative weekly to 11th August 2018, our digest of the latest finance and property news with a distinctively Australian flavour. Another week, more data, so let’s dive straight in.

And by the way, if you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

Watch the video, listen to the podcast or read the transcript.

We start with the trauma from Turkey which showed how fragile the financial markets are at the moment. Turkey’s finance minister (the President’s Son in Law) unveiled a new plan for their economy. The new economic stance will be one with “determination” — that’s a key part of it, he said. It will “transform” Turkey’s economy. It will also have a “strategic” and “powerful infrastructure.”

U.S. President Trump has repeatedly lashed out at Turkey over the continued detention of pastor Andrew Brunson, whom Turkish officials accuse of terrorism for his part of the failed 2016 coup, and no progress was made as delegates from both NATO countries met in Washington this week. Then Donald Trump, tweeted that he would double tariffs on Turkish steel and aluminum products.

As a result, the Turkish Lira plummeted further. In the course of an hour, it reached a new low of 6.80 to the dollar, marking its worst daily performance in over a decade. This from Bloomberg:

It recovered a little afterwards, but it has lost about 40% of its value against the dollar since the start of the year.

Many fear the fallout could spread beyond Turkey’s border, prompting traders to abandon riskier assets like stocks in search of safe-havens like gold, yen and Treasuries. Volatility, as measured by the VIX “fear index”, rose nearly 17%, highlighting investor concerns about the broader impact of a possible crash in Turkey’s economy.

One analyst said the exposure to a slump in Turkey’s economy is “pretty international,” though limited to the banking sector, but data from the Bank for International Settlements showed that Japanese banks are owed $14 billion, U.K. lenders $19.2 billion and the United States about $18 billion. Enough to make a dent.

The Turkish Lira also moved the same way against the Euro, up 14.33%. “We’re not going to lose the economic warfare” being waged against Turkey said President Erdogan.

In the US, core consumer prices rose by their quickest pace in a decade in July and topped market forecasts, keeping the Federal Reserve on track to raise interest rates twice more this year. The data add to a robust picture of the US economy, which grew by a speedy annual rate of 4.1 per cent in the June quarter. The unemployment rate is close to its lowest level in 18 years. Core inflation, which strips out volatile energy and food prices and is closely followed by the Fed, rose 2.4 per cent year on year in July and up from 2.3 per cent in June. That was the fastest annual pace of core inflation since September 2008.

While headline inflation is rising more quickly than average hourly earnings, wages may pick up given the strength of the labour market. The Fed seems well positioned to carry on tightening policy at its current pace, with no reason to either speed up or slow down. That said, the Turkish situation took the probability of two more cuts down a little according to Bloomberg.

The US dollar was relatively steady following the inflation data. The DXY index, tracking the US currency against a weighted basket of global peers, was up 0.8 per cent following the inflation figures, having been up 0.6 per cent before the data release. The index rose above 96 on Friday for the first time in 11 months.

Looking at the US indices, the NASDAQ slipped 0.67% to 7,838 on Friday, while the DOW Jones Industrial slipped 0.77% to 25,313. Gold futures slide a little to 1,219 and Copper was down 0.74% to 2.75. Oil futures rose 1.45% to 67.78, as the International Energy Agency warned that the recent cooling in the market may not last. Bitcoin was weaker, down 6.03% to 6,153, not helped by the news that creditors of the defunct coin exchange Mt. Gox are trying to recoup money.

European shares also fell on Friday as worries over a dramatic fall in the Turkish lira jolted financial markets amid concerns of the region’s banks’ exposure to upheaval in Turkey. The Germans DAX fell 1.99% to 12,424.

Asian stocks closed mostly lower on Friday as global investors opted to sell risk assets while they also continued to assess the impact of the latest tit-for-tat in the trade war between the U.S. and China.

China’s Shanghai Composite index managed to eke out meagre gains on high volatility. The index had recorded seven straight swings of 1% or more, the longest stretch since Chinese markets crashed in 2015.

In other emerging markets currency, the Russian rouble continued its decline, hitting fresh two year lows, after the US imposed fresh sanctions against the Kremlin for its alleged part in poisoning a former British spy and his daughter in the UK. It closed at 67.71, up 1.52%.

The Aussie continued to slide, as expected, down 1.04% on Friday to 72.96. And we also slipped against the British pound, down 0.63%.

Trade Tariffs continue to worry the market, with Fitch suggesting there is every reason to believe the United States’ trade dispute with China will get worse before it gets better, and that the US trade deficit will widen further rather than shrinking.

Now that they are on the receiving end of US tariffs, Chinese policymakers have three options. First, they could capitulate, by scaling back many of the “discriminatory practices” identified in the US Trade Representative’s March 2018 report on technology transfers and intellectual property. So far, there is no indication that China is considering this option. Second, China could escalate the dispute. It could set its own tariffs higher than those of the US, apply them to a larger range (and greater dollar value) of US exports, or offset the impact of US tariffs on Chinese exporters by allowing the renminbi to depreciate against the dollar. Alternatively, policymakers could look beyond trade in goods to consider capital flows and related businesses associated with US firms, effectively allowing the authorities to impede US financial and nonfinancial firms’ Chinese operations. As with the first option, this one seems unlikely, at least at this stage of the dispute. So far, China has chosen the third option, which lies between capitulation and escalation. China has retaliated, but only on a like-for-like basis, matching US tariff rates and the dollar value of trade affected. At the same time, it has tried to claim the moral high ground, by eliciting international condemnations of protectionism and unilateralism. This hasn’t been difficult, given that several other major economies are currently facing US tariffs. Securing such third-party buy-in is critical for the Chinese leadership’s domestic position. If the government were perceived at home as being bullied by the US, it would have to take a much tougher line in the trade dispute.

Fitch thinks that the US actually has rather limited options, despite having initiated the dispute. Even for a notoriously unpredictable administration, a full and unconditional reversal on tariffs seems out of the question. But so is the status quo, now that China has already levelled the playing field by retaliating in kind. That leaves only escalation – a possibility that the Trump administration has already raised by threatening additional tariffs on all imports from China

With the US locked in a trade war with China and other nations, Gregory Daco at Oxford Economics suggested that higher tariffs could gradually filter through to producer and consumer prices, supporting expectations of a gradual pick-up of inflationary pressures.

Locally, the RBA released its quarterly Statement on Monetary Policy with updated forecasts for inflation, unemployment and economic growth. The central bank has downgraded its inflation forecast for 2018. The RBA now expects both core and underlying inflation to rise by 1.75% to December 2018, down from the May forecasts of 2.25% and 2% respectively. Beyond that time frame, the central bank kept its inflation forecasts relatively unchanged. Previously, it expected both core and underlying inflation to reach 2.25% by the middle of 2020. In Tuesday’s rate announcement, Lowe also said that “a further gradual decline in the unemployment rate is expected over the next couple of years to around 5%”. The bank has maintained its forecasts that the unemployment rate will stay at around 5.25% through to June 2020, before dropping to 5% in December.

It’s also worth looking at Lowe’s speech on Wednesday, when he said that “Electricity prices in some cities have declined recently after earlier large increases, and changes in government policy are likely to result in a decline in child care prices as recorded in the CPI,” Lowe said. “There have also been changes to some state government programs that are expected to lead to lower measured prices for some services.” In Tuesday’s rates decision, Lowe said “the central forecast is for inflation to be higher in 2019 and 2020 than it is currently”.

The central bank slightly bumped up its forecasts for GDP growth in Q2 2018, to 3% from 2.75%. Longer-term, the bank’s growth projections were little-changed. It still expects GDP growth to average 3.25% over the next two financial years, before falling to 3% in June 2020 and remaining at that level through to December.

Given the projections were the first to include a time frame out to December 2020, the forecasts confirmed that underlying inflation pressures are expected to remain low for at least the next two and a half years. The latest set of projections confirmed that the RBA still looks set to keep interest rates on hold for the foreseeable future.

The Royal Commission hearings were back with avengence this week, with NAB’s MLC Wealth management business in the spotlight first, and later in the week IOOF. We saw more of the poor cultural norms on display, with investors being charged for no service, and attempts to block the release of documents and the late delivery of evidence to the commission. In fact, the CEO of NAB went as far as releasing an apology in Twitter. NAB shares ended up slightly to $28.09.

Shares in IOOF, Australia’s second largest wealth manager fell as senior executives from the fund manager appeared before the commission. At the close, the shares were down 2.7% to $8.73. Questioning in the royal commission centred around payments to related parties and the flow of cash back to the super fund from external fund managers when IOOF invests in those funds. Michael Hodge, senior counsel assisting the royal commission, said: “One of the things we are trying to understand is how trustees go about dealing with these volumes based fees where a percentage of the investment of the trust’s money is being paid to another part of the retail group.” Tendered to the commission today was a letter from prudential regulator APRA to IOOF about the conflicts of interest between members of the IOOF super fund and shareholders of IOOF.

The bottom line, is that poor corporate behaviour and the inability of regulators to get to the key facts was again in evidence, and again, consumers lose out as a result. It is shameful.

The CBA’s full-year results to 30 June 2018 (FY18) highlighted the pressure on Australian banks with an increase in wholesale funding costs squeezing CBA’s net interest margin in 2H18, slower loan growth and continued investment into the business and compliance contributed to higher expenses. Mortgage arrears also trended upwards due to some pockets of stress, and while they have not translated into higher provision charges as yet due to strong security values, continued moderation in Australian house prices may result in higher provisioning charges in future financial periods. CBA shares were up 0.03% on Friday to 75.39, and several commentators are claiming the worst is over for them, unlike for AMP, who also reported, and whose shares remain in the doldrums, reflecting the major changes to turn that ship around. Suncorp also reported and they did pretty well in the tight market, their shares rose after their results, and now stands at 15.63.

However, expect more bad news ahead, placing pressure on profit growth for all Australian banks. Increased regulatory and public scrutiny of the sector may make it difficult for the larger banks to reprice loans to incorporate the increase in wholesale funding costs, meaning net interest margins are likely to face some downward pressure. Loan growth is likely to further slow as the housing market continues to moderate, while compliance costs continue to rise due to the scrutiny on the sector. And of course the most prominent scrutiny is the royal commission into misconduct in the banking, superannuation and financial services industry, which has already identified a number of shortcomings within the industry.

That said, CBA’s FY18 results show a level of resiliency despite these issues. The bank reported cash net profit after tax from continuing operations declined 5% to AUD9.2 billion in FY18, but this was driven by a number of one-off charges, including a AUD700 million fine to settle a civil case in relation to breaches of anti-money laundering and counter-terrorism financing requirements. Cash net profit after tax from continuing operations rose by 4% to AUD10.0 billion when the one-off items were excluded.

CBA has much more to do to fix its reputation, and strong capital ratios are not sufficient to allay the concerns in the business. It is more about culture and putting customers first.

So, perhaps no surprise this week, the Greens called for the big banks to be broken up. They said “It’s time that banks became banks again. Australians are sick and tired of these massive financial institutions getting away with murder because they can throw stacks of money at the two old political parties. Our banks should be working for us, not against us and this policy will make sure that happens.

Under the Greens proposal: Banks will no longer be able to own wealth management businesses that both create financial products and spruik them to unsuspecting customers. Consumers will be able to easily distinguish between the simple and essential products and services that the vast majority of Australians use—deposits and loans, superannuation and insurance—and the more complex and selective activity that is the domain of big business, the wealthy, and the adventurous. By removing hidden conflicts of interest, Australians will be able to trust that the advice they’re getting from their banker is designed to line their own pocket, not the other way round. The watchdogs have failed. They would strip ASIC of its responsibility for overseeing consumer protection and competition within the essential services of basic banking, insurance and superannuation and return them to the ACCC.

But we believe there is much more to do than just breakup the banks. We will be discussing this in a future post. The major banks have too much market power, as we discussed on our recent video How Much Market Power Do “The Big Four” Hold? and they continue to milk customers using poor business practice, for example in the home loan market, the mortgage rate you get is hard to compare, and obtuse. We discussed this in our show “Price Information In the Home Loan Market”.

You might also like to watch our show on the latest lending statistics and mortgage stress data, “Lending, Stress and All Things DFA”, as we are not going to have time to cover these today.

So quickly to the property market. Once again prices continue to fall in the main centres of Sydney and Melbourne.

In terms of auctions, CoreLogic says that last week the number across the combined capital cities fell with 1,324 held with a final clearance rate of 54 per cent, down from the previous week. Combined clearance rates have levelled out somewhat remaining within the low to mid 50 per cent range for 13 consecutive weeks. They note that despite the continued slowing in the market, clearance rates are still tracking higher each week relative to the same period in 2012; during the last significant downturn in home values.

Melbourne’s final clearance rate came in at 57 per cent across 629 auctions last week compared with 911 last year returning a substantially higher clearance rate of 73.9 per cent. Sydney’s final auction clearance rate fell to 51.9 per cent across 462 auctions last week, down on the previous weeks. In same week last year, 620 homes went to auction and a clearance rate of 66.4 per cent was recorded.

This week, 1,320 capital city auctions are currently being tracked by CoreLogic; remaining relatively steady on last week’s final result which saw 1,324 auctions held. Over the same period one year ago, there was a considerably higher 2,040 homes taken to auction.

In June, according to the latest ABS housing finance data, first-home buyers accounted for 18.1% of the growth in owner-occupier loans, continuing a trend seen throughout this year. The chart from the RBA helps illustrate the effect that first home-buyers are having on the market. Clearly, there’s a trend underway in Sydney and Melbourne: The value of cheaper homes is holding up, while more expensive home prices have gone into reverse.

This is explained by increasing incentives in NSW and Victoria for first time buyers, and also more lower priced small apartments are coming on stream. The figures tie in with recent trends evident in the Sydney market, with more evidence of recent price falls among higher-end properties valued above $2 million.

Of course the question is, with prices falling, and likely to continue to fall further, could first time buyers get a better deal later by waiting for further falls. That, in my view is a tricky call but our modelling of future credit growth suggests first time buyers will continue to prop up the lower end of the market for some time to come yet.

And finally today, mark your diary, the next DFA live stream event will be on Tuesday 21st August at eight PM Sydney. I will be providing more information shortly about the event, but is already scheduled on the channel if you want to set a reminder. And feel free to send questions in beforehand.

Welcome to the Property Imperative weekly to 4th August 2018, our digest of the latest finance and property news with a distinctively Australian flavour.

By the way if you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

Watch the video, listen to the podcast, or read the transcript.

A big week of news to cover, so let’s get straight in at the deep end with the Productivity Commission report on Competition in Financial Services which was released on Friday. The final report, which was released earlier than expected really highlights the never-mind-the customer attitude of the industry and its regulators. They call out regulatory failure and conflicts of interest across the sector, referring to opaque pricing, unsuitable products, no reward for customer loyalty as well as product complexity and faux competition. Major players have too much market power, and have fingers in multiple segments of the market. Customers lose out as a result. They made a wide range of recommendations, including the introduction of a best interest obligation for all providers in the home loans market, mortgage Brokers trail commissions should be phased out, ASIC to ensure that the interests of borrowers are adequately safeguarded in the LMI market, APRA is singled out for myopic regulation. ACCC should focus on encouraging competition across the industry and safeguarding the interests of consumers in the regulatory system, the new payments system needs a proper access regime and the Payments System Board of the RBA should ban all card interchange fees. We discussed the implications in our recent video, and the link to that is above. In summary a number of critical reforms which if implemented could certainly change the landscape for financial customers in Australia for the better, whilst clipping the wings of the major incumbents. We discussed this on ABC Radio. Good Job, Productivity Commission. Let’s now see if the Government is up to the challenge.

There was a bit of good news on the retail front, with turnover for June, the month of the end of year sales, where deep discounting was the hallmark. The ABS says retail turnover rose 0.4 per cent seasonally adjusted, which follows a 0.4 per cent rise in May. The trend estimate, which I prefer, reported a 0.3 per cent in June following a rise of 0.4 per cent in May 2018. Compared to June 2017, the trend estimate rose 3.1 per cent. In trend terms, clothing and footwear rose 0.7%, department stores rose 0.5% and household goods 0.3%. Across the states, New South Wales and Victoria rose 0.5%, ACT 0.8% and Tasmania 0.9%. Queensland was flat and WA rose just 0.1%, so again the variations are significant. Online retail turnover contributed 5.7 per cent of total retail turnover in original terms in June 2018, a rise from 5.6 per cent in May 2018. In June 2017 online retail turnover contributed 4.1 per cent to total retail.

This means households are spending more than their income growth, by continuing to tap into their savings. So it will be interesting to see if the retail momentum continues, or sags in July after the end of season sales.

Continuing the “cat among the pigeons” theme, ANZ parted company from its competitors by cutting its variable home loan rate for new customers. While banks including the CBA have cut fixed loan rates and offered “honeymoon deals” in recent weeks, the ANZ is the first to move on variable rates. The ANZ told mortgage brokers it was bringing down its basic principal and interest home rate for owner-occupiers by 0.34 percentage points to 3.65 per cent. The ANZ offer only applies to new customers looking for a loan valued at 80 per cent or less than the value of their property. Loan-to-value ratios above 80 per cent remain unchanged at 3.99 per cent. As we discussed in our separate post “ANZ Ups The Ante In The Mortgage Wars” – the industry is homing in on lower risk customers in an attempt to maintain loan book growth. We also discussed this significant event on 2GB’s Money Show with Ross Greenwood. As Ross said, picture the lions around a shrinking watering hole trying to protect their territory!

Also this week ASIC released their review of exchange traded products (ETP’s) in Australia. These are open-ended investment products that are traded on a securities exchange market. ETPs trade and settle like shares and give investors exposure to underlying assets without owning those assets directly. They differ from listed funds because they are open-ended. This means that the number of units on issue may increase or decrease daily depending on investor demand. ETPs, especially exchange traded funds (ETFs), are increasingly popular with retail investors and self-managed superannuation funds (SMSFs). This is because of their accessibility, perceived low cost, transparency, intraday liquidity, diversification benefits and ability to provide exposure to new asset classes. There has been steady growth in both funds under management and the number of ETP products available on the market in Australia. ASIC called out a number of concerns, including the question of spreads and liquidity, the concentration of market makers, and the lack of good disclosure. More of the same-ol’ same -ol’. Potential investors should be wary.

Data from the Household, Income and Labour Dynamics in Australia HILDA survey came out this week and showed again the rise in the proportion of the household population who is renting, with the number of Australian renters eventually becoming homeowners plummeting over the last 15 years – particularly for those between the ages of 18 and 24. The survey found the overall proportion of people living in rental accommodation has increased by 23 per cent since 2001 to 31.3 per cent in 2016. They called out “The growing evidence of ‘intergenerational inequality’”. The data also chimes with our surveys, that more households are under financial pressure thanks to flat incomes and rising costs. It’s worth highlighting their data only runs to 2016, so it’s already a couple of years old. We think the trends continue to grow, based on our latest Mortgage Stress data which will be out next week.

And another survey from mortgage lender State Custodians found that as many as 15% of surveyed homeowners have faced challenges when trying to refinance, due to falling property prices. The figures published by State Custodians also revealed that young people were the most affected, with around 34% of those under the age of 34 saying they’ve been unsuccessful in re-financing because of declining property values. This highlights the rise of “mortgage prisoner’s” who cannot refinance to get the better deals because of little or no equity, or other financial pressures.

And talking of households in financial pressure, the number of Australians falling behind on their mortgages will rise in the next two years as interest-only loans end and repayments get more expensive, ratings agency Moody’s warned this week. Delinquencies on loans that have converted from interest-only to principal and interest are running at double the rate of those still on interest-only, they said. About 40 per cent of loans by Australian banks in 2014 and 2015 were interest-only for five years, meaning a large portion are set to come under pressure with higher repayments in 2019 and 2020, said Moody’s. This backs up our findings, which estimates that more than 970,000 Australian households are now believed to be suffering housing stress. We discussed this in our video Wither Interest Only Loans.

Genworth, the Lender’s Mortgage Insurer related their 1H18 results this week and their profit remains under pressure, as claim rates rise. The Delinquency Rate increased from 0.51% in 1H17 to 0.54% in 1H18, and they pointed and increase in the number of delinquencies in Western Australia, New South Wales and to a lesser extent South Australia. This was partially offset by a decrease in delinquencies in Victoria and Queensland. New delinquencies were down in the half (1H18: 5,565 versus 1H17: 5,997). Delinquencies in mining areas are showing signs of improving. In non-mining regions there are indications of a softening in cure rates.

Turning now to property, the home price slides continue, as we discussed in our post “Home Price Falls Are Just Starting (…more to come!). We discussed the importance of looking at the local, micro property markets as the averages mean nothing. For example, over the past year prices are down more than 20% in some suburbs, and not necessarily where you might expect.

And talking of videos, do check out the latest in our series of Adams/North discussions, “The Great Airbrush Scandal – Policy Failure of the Year!”, where we dissect APRA’s Bank Stress Tests and conclude they were not fit for purpose. This one has already generated a large number of comments and observations. John suggests our regulators are asleep at the wheel! You can also read his original article.

Corelogic says Auction volumes are lower across each individual capital city this week with 1,224 homes scheduled to go under the hammer, down from 1,536 last week. A further sign of weakness in the property sector. Melbourne is particular is slowing fast.

Last week the homes taken to auction across the combined capital cities, returning a final auction clearance rate of 55.6 per cent, down from 57.0 per cent across 1,257 auctions the previous week. Over the same week last year, 1,987 homes went to auction and a clearance rate of 68.7 per cent was recorded. Melbourne’s final clearance rate was recorded at 58.5 per cent across 802 auctions last week, compared to 59.9 per cent across 613 auctions over the previous week. This time last year 956 homes were taken to auction across the city and a much stronger clearance rate was recorded (75.6 per cent). Sydney’s final auction clearance rate came in at 52.4 per cent across 469 auctions last week, down from 55.2 per cent across 407 auctions over the previous week. Over the same week last year, 714 homes went to auction returning a clearance rate of 65.4 per cent. Across the smaller auction markets, clearance rates improved across Canberra and Perth, while Brisbane and Adelaide saw clearance rates fall week-on-week. There were no auctions recorded in Tasmania last week. Of the non-capital city auction markets, the Hunter region was the best performing in terms of clearance rate, with 10 of the 14 reported auctions selling (71.4 per cent), followed by Geelong with a 65.0 per cent clearance rate across 20 results. The busiest region for auctions was the Gold Coast where 39 homes were taken to auction, returning a clearance rate of just 32.3 per cent.

Building approvals in June were slightly stronger in trend terms, rising by just 0.1% as reported by the ABS. The Mainstream media fixated on the stronger, but less reliable seasonally adjusted figures. Among the states and territories, dwelling approvals rose in June in the Australian Capital Territory (5.8 per cent), South Australia (5.6 per cent), Northern Territory (4.8 per cent), Tasmania (2.2 per cent), Western Australia (1.7 per cent) and New South Wales (0.2 per cent) in trend terms. Dwelling approvals fell in trend terms in Queensland (1.6 per cent) and Victoria (1.2 per cent). Overall momentum is slowing in our view, as demand for high-rise investment apartments ease.

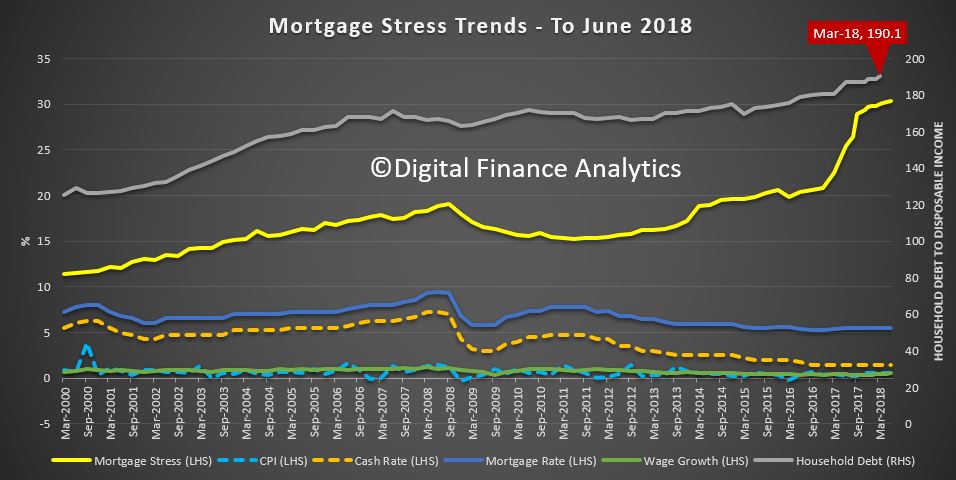

And overall lending for housing is still tracking higher despite investor lending sliding, according to the latest RBA and APRA figures for June. Owner occupied housing lending rose 0.6% or $6.6 billion to $1.18 trillion, while investment lending fell $800 million, down 0.1% in seasonally adjusted terms, or rose $1 billion, up 0.2% in original terms. (I have no idea what adjustments the RBA makes, it’s not disclosed!). Investment lending fell to 33.5% of the portfolio. Total lending for housing is a new record $1.77 trillion, and remember this is at a time when housing debt to income is knocking on the 200 door, and we are one of the most in debt nations on the planet. Lest we forget, loans need to be repaid, eventually! We discussed both the credit data and the building approvals in our video “Another Housing Record Set”. We have not fundamentally addressed the credit elephant in the room. Despite all the noise. Perhaps the regulators would like to tell us, how much debt is too much? We clearly have not hit their pain threshold yet, despite the rising financial stress in many households.

So to the markets. Locally, the ASX100 finished down a little on Friday to 5,126, still significantly higher than earlier in the year. The banks were down, for example, CBA fell 1.15% on Friday, to end the week at 72.83, in reaction to the Productivity Commission report. Westpac fell 0.96% to end at 28.91. AMP also fell, down 0.85% on Friday, to 3.50, despite a broker’s report suggesting there may be long term value in the stock, after a restructure. The market was perhaps not convinced.

The Aussie was below 74 cents against the US dollar, despite a small rise on Friday, to 73.97, but higher, up 0.29% to 5.05 against the Chinese Yuan. It appears China is flexing its currency muscles in response to the US trade tariffs.

The Bank of England lifted their cash benchmark rate 0.25% to 0.75% as inflation is above the lower bounds target, despite the uncertainty surrounding Brexit (be it hard or soft). The Aussie was up 0.62% on Friday against to UK Pound to 0.56 cents in reaction to the news.

Across the pond in the US market, Apple took market attention for a host of reasons this week, including reaching a historic Wall Street milestone by becoming the first U.S. company to hit $1 trillion in market capitalization. Apple Inc stock hit the target number of $207.05 (based on the numbers of shares outstanding reported in its 10Q) just before noon on Thursday. Shares closed solidly above that Friday at 207.99. Shares moved into trillion-dollar territory following a strong earnings report earlier this week. On Tuesday, Apple’s fiscal third-quarter results beat on the top and bottom lines, driven by sales of the pricier iPhone X and subscription revenue to services such as Apple Music and its App Store. Apple also lifted the cloud that was hovering over the tech sector following weak reports from Facebook and Twitter. The NASDAQ ended the week at 7,812, a strong finish, but not a record, despite the Apple price. The S&P Information Technology sector index finished at 1,277.05 Friday, compared with 1,262.27 a week ago.

The July US employment report gave the market more evidence that the economy is humming along at a pace that won’t alarm the Federal Reserve. Although the rise in nonfarm payrolls was less than expected for July, jobs gains for the two previous months were revised up by 59,000, making the overall rise about in line with forecasts. And average hourly earnings showed wage inflation at the same year-on-year pace as before. That leaves the Fed set up to continue its plan of gradually rising rates. “The economy is growing really strongly and headline inflation set to hit 3% next week, so the case for September and December Fed rate hikes remains strong,” ING Chief International Economist James Knightley said.

Fed fund futures are still pricing in the next rate hike to be at the next September 25-26 meeting. Odds for an additional increase in December remained little changed after the release at around 65%.

The Fed had its say this week as well. The Federal Open Market Committee kept rates unchanged as expected, and also kept the language in its statement substantially the same. The FOMC said it continues to expect that further gradual increases in the target range for the federal funds rate will be consistent with “sustained expansion of economic activity, strong labor market conditions and inflation near the Committee’s symmetric 2% objective over the medium term.” That reaffirmed investor expectations that the central bank remained on track to hike rates twice more this year. “The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation,” the Fed said in its statement.

A report on Tuesday showed that the Fed’s preferred measure of inflation, the core personal consumption expenditures price index, which excludes food and energy prices, was up 0.1% and 1.9% on a year-over-year basis. The Fed targets inflation of 2%.

Oil settled lower for the day and week Friday, as concerns about a trade war stifling demand hurt sentiment. On the New York Mercantile Exchange crude futures for September delivery fell 47 cents to settle at $68.65 a barrel. Oilfield services firm Baker Hughes reported on Friday that the number of U.S. oil drilling rigs in operation fell by 2 to 861, pointing to tightening U.S. output. And the weekly oil inventories numbers showed an unexpected rise in U.S. stockpiles, further weighing on prices. Concerns also remained about escalating output from the OPEC and Russia. On June 22-23, OPEC, Russia and other non-members agreed to return to 100% compliance with oil output cuts that began in January 2017, after months of underproduction elsewhere had pushed adherence above 160%. Even though output continued to decline in Iran, Libya and Venezuela, the survey suggested that compliance had only fallen to 111% in July, suggesting more room for increasing production from the likes of Saudi Arabia or OPEC’s non-member ally Russia.

Trade worries whipsawed this week, keeping the market on edge, amid conflicting reports of U.S. action and proposed retaliation from China. Tensions on Wall Street eased significantly on Tuesday on a report from Bloomberg that both sides were trying to restart trade talks. But that was quickly countered by another report that the U.S. was considering raising tariffs on $200 billion in Chinese goods to 25% from 10%, which the White House later confirmed was under consideration. On Friday, China shot back with a potential plan for tariffs on $60 billion of U.S. goods. “The U.S. side has repeatedly escalated the situation against the interests of both enterprises and consumers,” China said, according to Reuters. “China has to take necessary countermeasures to defend its dignity and the interests of its people, free trade and the multilateral system.” White House Economic adviser Larry Kudlow warned China not to underestimate President Donald Trump.

The Dow Jones ended at 25,462, up 0.54%, high, but not at a peak, while, the US Dollar Chinese Yuan sat at 6.83, right at the top of its range, and China exerts pressure on the rate.

Bond rates were down a little, with the 10 Year benchmark sitting at 2.95, well down from its 3.12 in May. At the short end, the 3-month bond rate is 2.00, still at the top of its range. Libor is still sitting at 2.34, at the top of its range, signalling higher funding costs in the system.

Gold continues lower, at 1,222, as many risk investors are favouring the US Dollar at the moment. Bitcoin ended the week at 7,443 up 0.65% on Friday, but below its recent highs.

So back once more to cats and pigeons. Next week we will be hearing the latest from the Royal Commission in sessions covering wealth management. NAB and MLC are up first, but I will be especially interested in the evidence from the Industry superfunds. We suspect more revelations as the Commission works its magic. And the results from CBA will be a highlight, it will be interesting to see what they report in terms of net interest margin. I am expecting more loan repricing, both up and down.

It’s never a dull moment in the finance and property sector, so expect more turbulence ahead. The bumpy ride continues….

Welcome to the Property Imperative weekly to 28th July 2018, our digest of the latest finance and property news with a distinctively Australian flavour.

Watch the video, listen to the podcast, or read the transcript.

By the way, if you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

Today we start with local economic news. The latest headline inflation rate came it at 2.1%, but the relevant underlying rate was 1.9%. This is even below the 2.0% the RBA forecast in May and continues the trend here, and elsewhere. Economists are scratching their heads as to why, some referring to the not so trusty Phillips curve, globalisation, charging work practices, automation, or something else. We suspect the high consumer debt and limited spending power has played a significant role. Despite the low number, we do not expect the RBA to react with a rate cut.