The coronavirus outbreak could result in a $319 billion loss for economies in the Asia Pacific, S&P Global Ratings has estimated, with Australia left vulnerable. Via InvestorDaily.

A

report from S&P has forecast growth in the APAC will slow to 4 per

cent in 2020, the lowest since the global financial crisis, as a result

of the virus.

The multinational

believes a U-shaped recovery will start later in the year, but by then,

economic damage in the region will reach US$211 billion ($319 billion).

Shaun

Roache, Asia-Pacific chief economist at S&P Global Ratings has said

the loss will be distributed across the household, non-financial

corporate, financial and sovereign sectors, with the burden to be on

governments to soften the blow with public resources.

“Some economic activities will be lost forever, especially for the service sector,” Mr Roache said.

The hardest hit economies have been Hong Kong, Singapore and Thailand, where people flows and supply chain channels are large.

Australia

is also exposed, with S&P forecasting its growth for the year to

touch 1.2 per cent, more than half of what it was in 2019 at 2.7 per

cent.

“Australia’s most disrupted

sectors employ a large share of workers which will weaken both the

labour market and consumer confidence,” Mr Roache said.

Services

in Australia account for a large slice of employment, the reported

noted, with accommodation and catering being sensitive to tourism and

discretionary consumer spending.

Along

with other economic experts, AMP Capital senior economist Diana Mousina

signalled she expects Australian GPD growth to be negative in the March

quarter, dragged by the bushfires and the virus.

Last

week’s rate cut to 0.5 per cent will assist households with mortgages

and businesses with debt, she wrote, but more stimulus is needed. AMP

Capital, as well as UBS have called the RBA will enact another cut in

April.

Ms Mousina anticipates fiscal

stimulus from government, starting with support for businesses hit by

COVID-19, followed by a broader boost to help investment and consumer

spending.

“However if government

stimulus does not prove to be enough (or come early enough) to support

the economy then the RBA is expected to start an asset purchase program

to further reduce the cost of borrowing,” she said.

As at Friday morning, there were 59 confirmed cases of COVID-19 in Australia, with two deaths.

APRA monitoring hits to financial system

The

prudential regulator has indicated it is assessing how the coronavirus

outbreak will affect the operation of financial institutions, with

chairman Wayne Byres saying the system is positioned to handle

volatility, but it will need considerable vigilance.

Speaking

to the standing committee of economics last week, Mr Byres said the

regulator has also been examining broader economic impacts from the

virus.

The financial system has

already copped hits from the extreme weather events over the summer.

Current estimates for total insured losses as a result of the bushfires,

storms, hail and floods across Australia are projected to be in the

order of $5 billion. The Australian cyclone system is still yet to end.

APRA

has reported the financial position of the insurance sector means it is

well placed to cover the claims, however, Mr Byres stated: “The

summer’s events will undoubtedly have an impact on the price and in some

cases, availability of insurance in the future.”

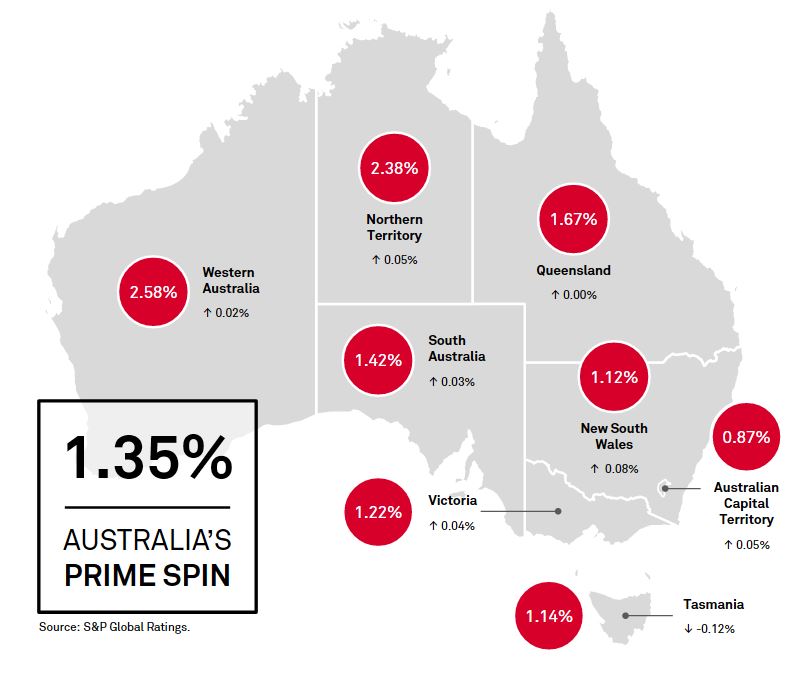

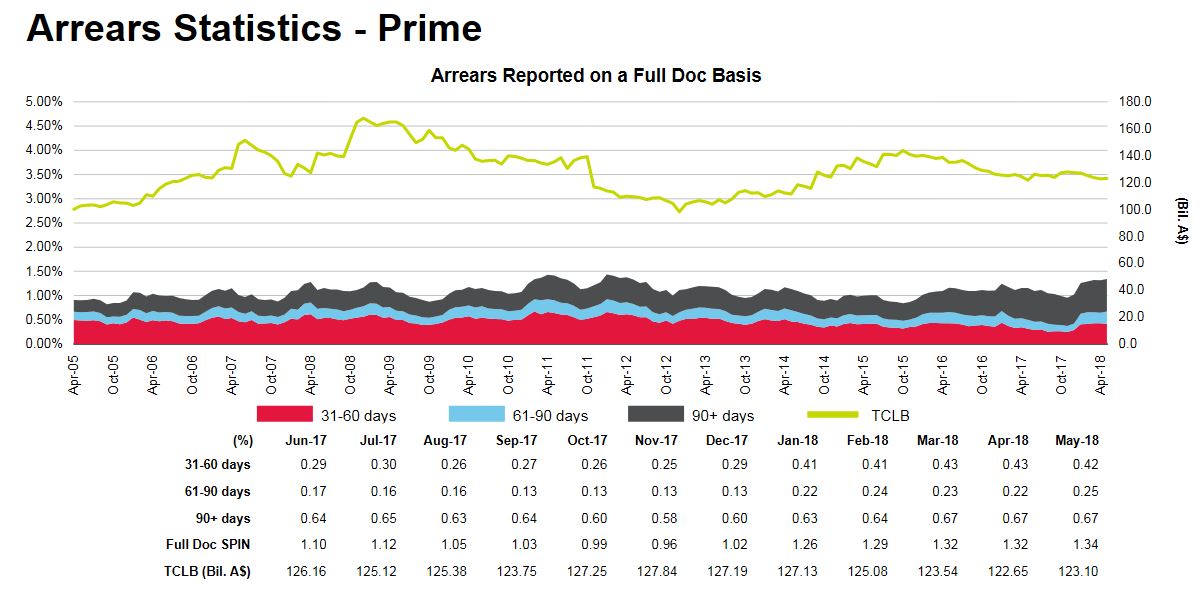

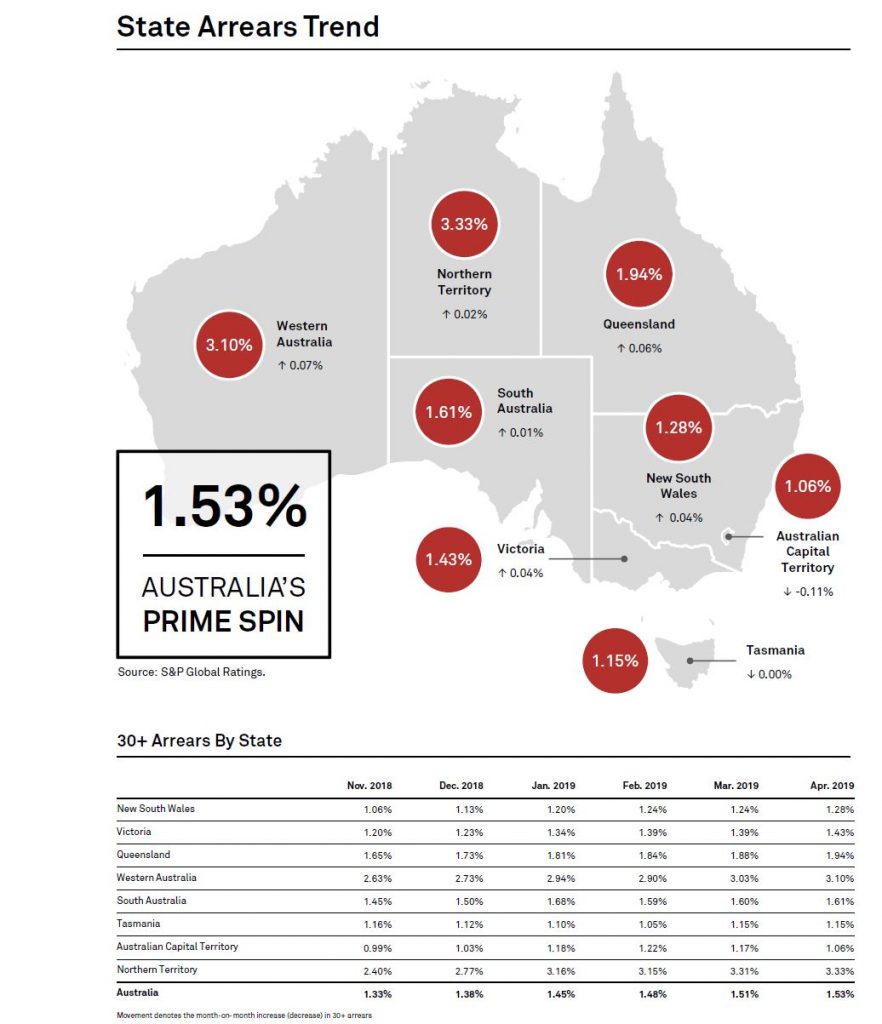

The S&P Spin Index for April shows a further rise in mortgage defaults, with WA and QLD leading the way. Only the ACT fell.

Now of course these are a myopic cross selection of loans, because they are those in the securitised pools. However, the rising trend continues.

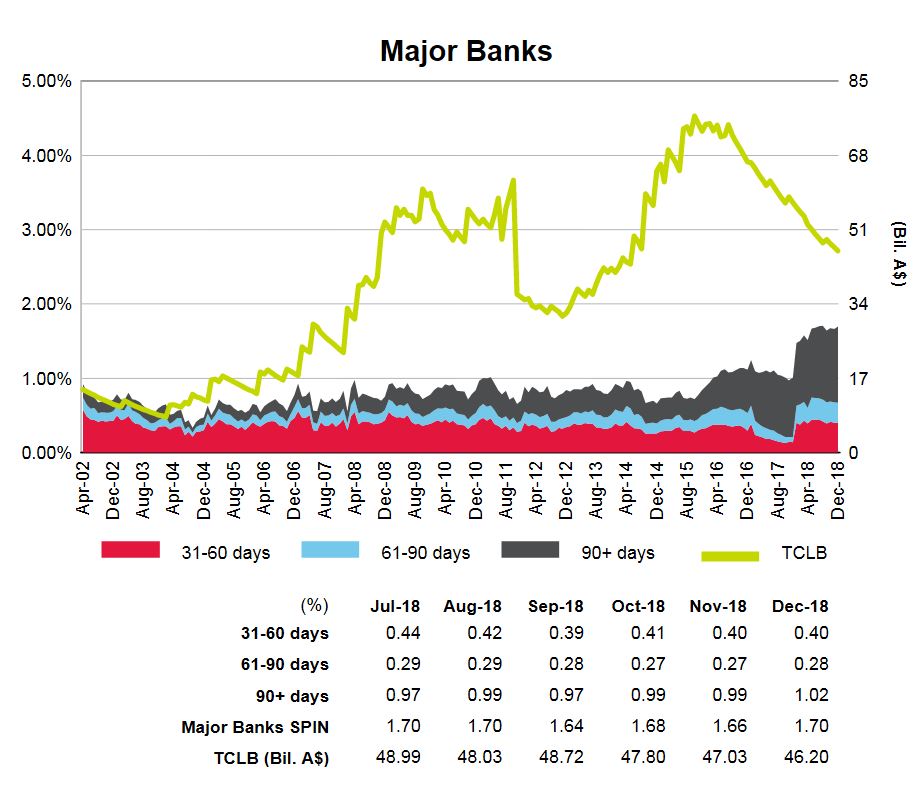

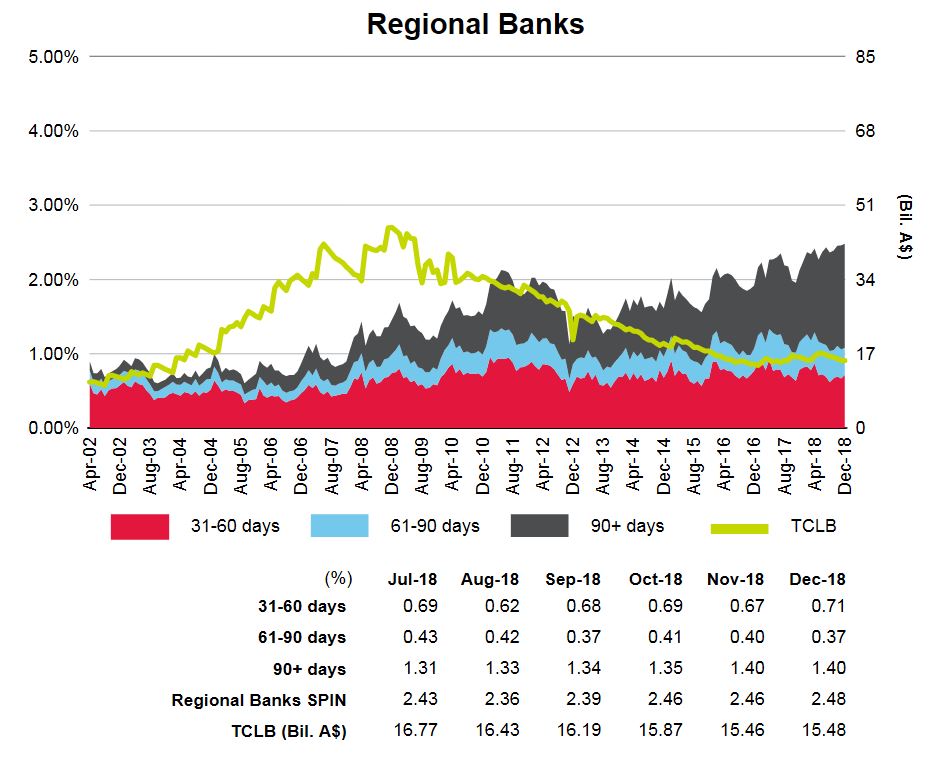

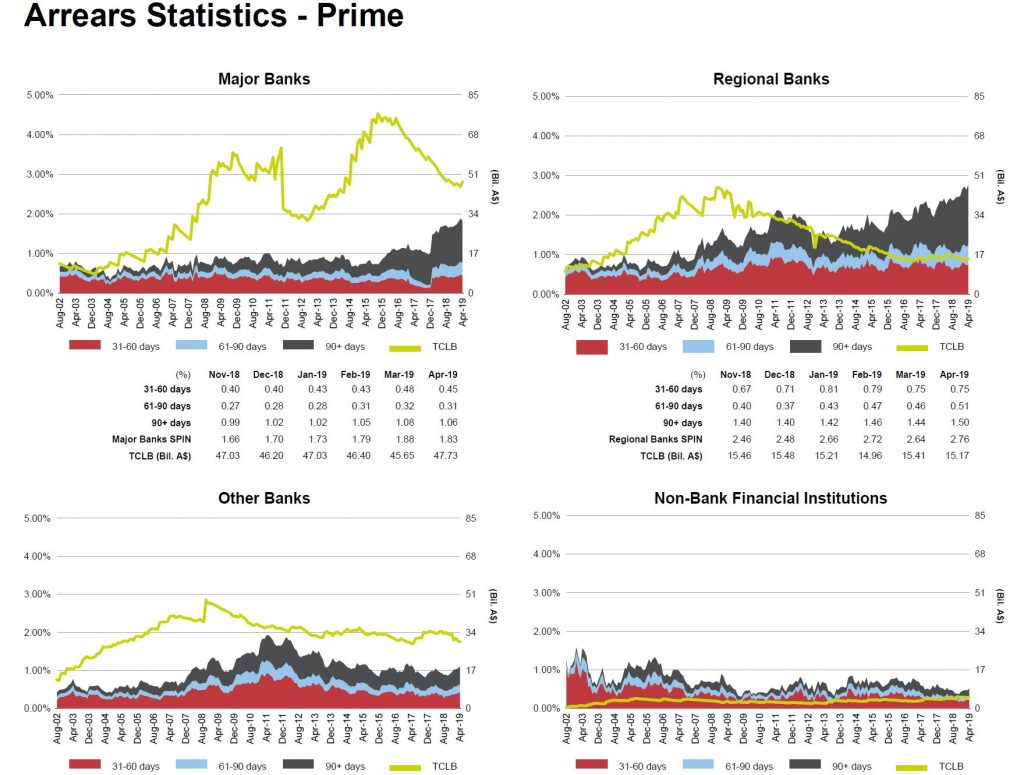

Within the mix, 90+ days arrears continue to climb especially among Regionals. It is worth reflecting that any upturn in the property market, to the extent it emerges, will have precisely NO effect on existing cash-strapped households, as the flat incomes, rising costs pincer movements continue to grip.

This was predictable, given the rising mortgage stress we have been detecting for some time. Of course the question becomes, will this lead to higher bank losses down the track?

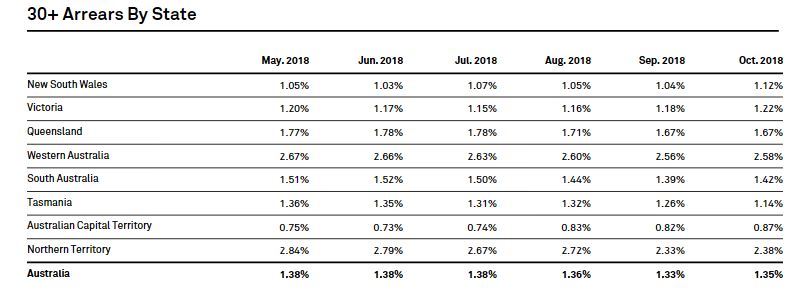

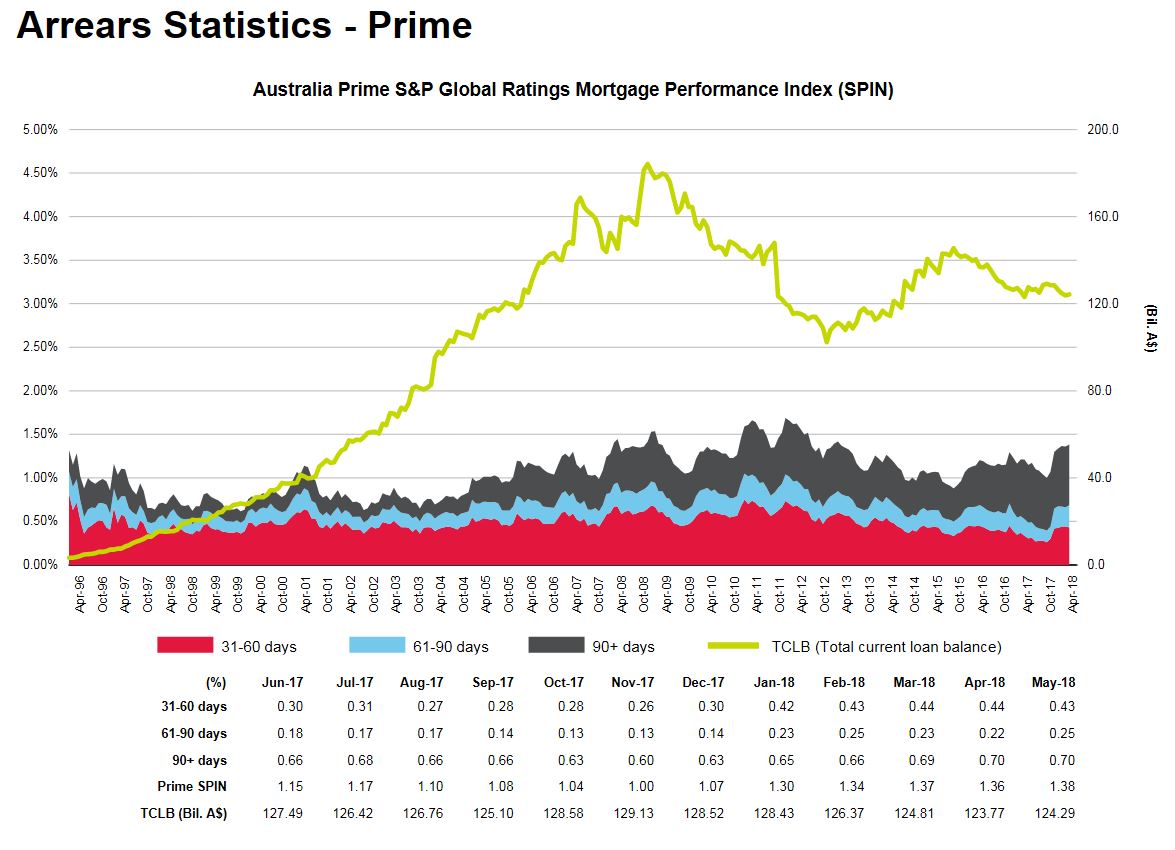

According to data from S&P Global Ratings relating to mortgage backed securities, the arrears rate rose in October 2018 (which is against normal trend).

Total SPIN index rose to 1.35%. The trend was consistent in all states and territories except Tasmania, where arrears fell to 1.14% in October from 1.26% the previous month. New South Wales recorded the largest increase in arrears in October, rising to 1.12% from 1.04% a month earlier. Arrears in New South Wales have been gradually rising throughout 2018, but remain the second lowest in the country, behind Australian Capital Territory.

WA stands out as the highest risk state, no surprise given the flat economy and many years of sliding home prices.

Investor and owner-occupier arrears increased in October. Investor

arrears increased to 1.25% in October from 1.19% in September and

owner-occupier arrears rose to 1.54% from 1.52% a month earlier. In our

opinion, the larger increase in investor arrears during the month partly

reflects the repricing of investor loans and interest-only loans, which

are more common among investors. This is also reflected in the

narrowing of the differential between investor and owner-occupier

arrears, which peaked at 0.61% in January 2017. The differential had

decreased to around 0.30% by October 2018, thanks to the ongoing

repricing of investor loans.

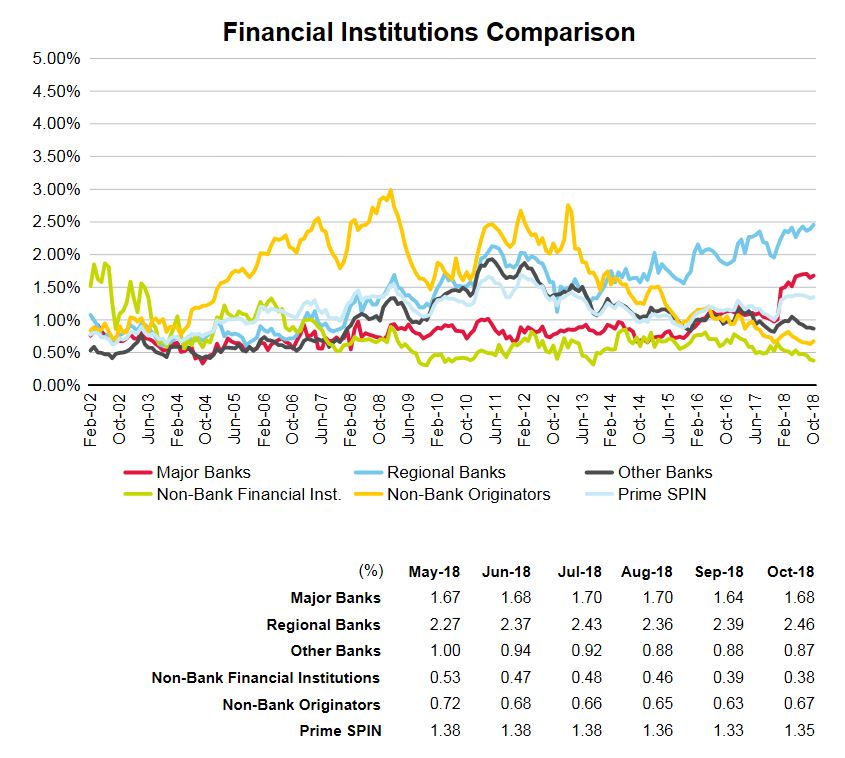

Arrears rose at the major and regional banks, offset by a small fall in the non-bank financial institutions. Defaults with non-bank originators rose.

S&P Global Ratings has just come out with a significant comment on “some weaknesses in the effectiveness of regulation in the banking sector, and the conduct, governance, and risk appetite shown by Australian banks”. Finally!!

The negative rating outlooks on systemically-important Australian banks reflect pressures on the Australian sovereign creditworthiness (Commonwealth of Australia; AAA/Negative/A-1+) and a possible tempering of our current highly supportive opinion concerning the Australian government’s tendency to support banks.

During the past quarter, we revised our economic risk trend for the Australian banking industry to positive from stable. This reflects our expectation that the trend of an orderly unwinding of economic imbalances, including for high property prices and private sector indebtedness, should continue for at least the next year.

By contrast, we recently negatively revised our view of the Australian banking sector’s industry risk. In our view, developments over the past two years in the Australian banking sector, including information coming out of hearings at the ongoing Royal Commission, highlight some weaknesses in the effectiveness of regulation in the banking sector, and the conduct, governance, and risk appetite shown by Australian banks.

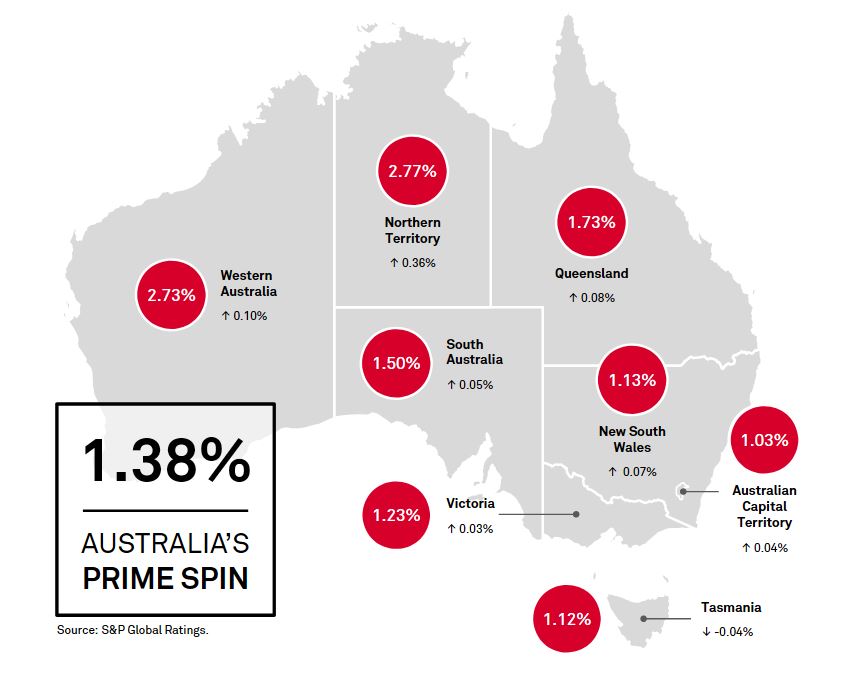

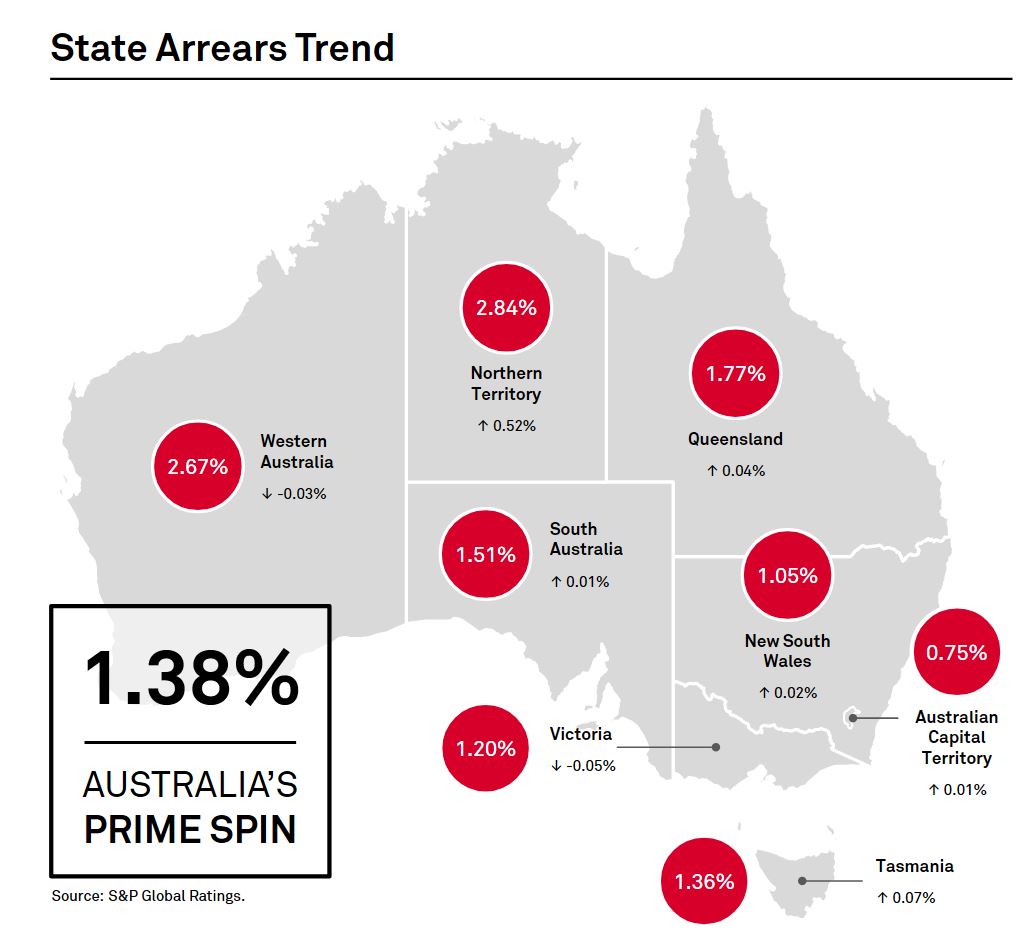

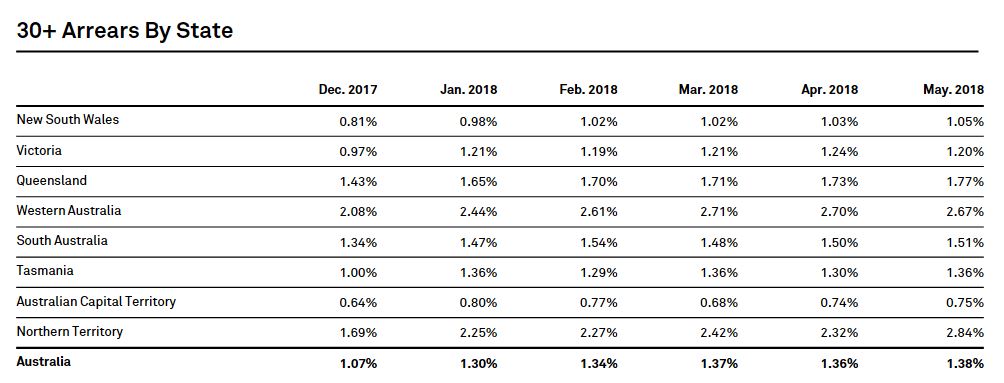

The latest S&P Ratings SPIN index to May 2018, based on their portfolio of mortgage backed securities showed a further move up in defaults compared with last month, from 1.36% to 1.38%.

In fact, Western Australia’s default rates improved a little, as did Victoria, but there were rises in New South Wales of 0.02%, Queensland of 0.04% and Northern Territory up 0.52%. ACT has the lowest default rate at 0.75%, followed by New South Wales at 1.05% while the Northern territory and Western Australia have the highest rates of 30 default at 2.84% and 2.67% respectively.

Looking across the period in default, the most significant rise across prime loans was in the 61-90 days bracket, up from 0.22% in April to 0.25% in May. 90 day plus arrears remained the same at 0.67%.

Significantly, the larger hikes were see in the major bank portfolios, with the prime spin rising from 1.36% last month to 1.38% in May. There was a rise in 61-90 day past due loans, from 0.22% last time to 0.25%.

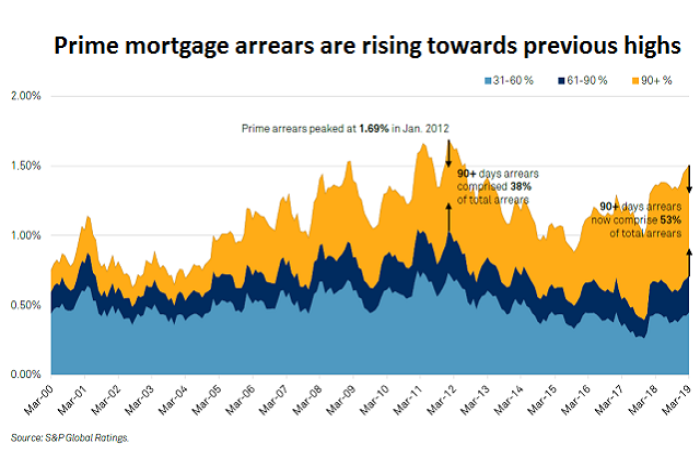

Whilst these moves are small, arrears are now as high as they were back in 2011, and interest rates are much lower today, so this highlights the risks in the system. This does not appear to be a seasonal issue, it is more structural.

Ratings Agencies are a funny breed, and I am not going to enter the debate as to whether they are ahead of the curve – some will say their track record around the time of the GFC was appalling – and whether they are truly independent; but they are taken seriously by the markets, which reacts when they publish their reports. So today we look at Moody’s assessment of Australia, and Standard and Poor’s Mortgage Delinquency Reports.

So first, to Moody’s who confirmed their rating of Aaa and which puts Australia in an exclusive club alongside United States, Switzerland, Sweden, Norway, Denmark, Netherlands and New Zealand.

They just reviewed the rating (some other agencies still have a negative watch on Australia, meaning they are more concerned about the outlook, given our exposure to foreign trade and debt) and Moody’s concluded that thanks to good GDP numbers, relatively low (on an international basis) Government debt – at only 42% of GDP, though up from 26.5% five years ago and strong institutions (RBA and APRA), the rating is confirmed. The bonus income from higher resources prices also helped.

This rating is important because it directly translates to the cost of government debt, and is a signal to the international community of the economic strength of the country.

Now Moody’s did highlight some concerns about the Government needing to control spending in order to bring the budget back into balance as forecast, against a fraught political background – by which I assume they mean the independents in the Senate and their perchance for blocking the passage of legislation; and also the risks from high levels of household debt in a flat wage environment. But they make the point that on a relative basis Australian Households are still enjoying a high per capital income ($50,334 in 2017) is in line with other Aaa economies, and this they say, offers capacity to absorb income shocks, and a base to support taxes as needed.

They suggest that household income growth will be lower than government forecasts, but they are still looking for GDP growth around 2.75%. They also suggest that Government spending will remain under pressure given the expected 6% rise in social welfare programmes including health and NDIS.

In terms of risks, they see two first is rising household debt, which they say exposes the economy and government finances. Second is Australia’s reliance on overseas funding, which may be impacted by changes in internal investor sentiment. Rate rises abroad might lift the cost of government and bank borrowing, adding extra pressure on the economy. But their judgement is, these risks are not sufficient to dent the prized Aaa ratings.

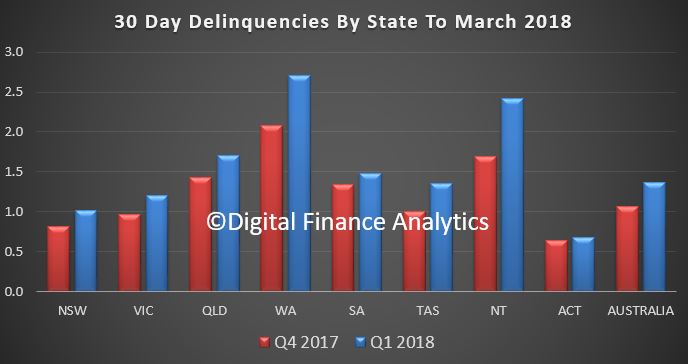

But, now square this with S&P Global Ratings RMBS Performance Watch to 31st March 2018. They revised arrears data for February and March 2018 to reflect an originators’ revisions to arrears data for these months. As a result, the prime 30 day SPIN including noncapital market issuance was 1.37% in Q1 2018, up from 1.07% the previous quarter.

They say that loans more than 90 days in arrears were at a historically high level at the end of Q1, indicating that mortgage stress has increased for some borrowers.

In addition, the major banks which account for around 43% of total prime RMBS loans outstanding recorded the largest movement in arrears during Q1 and are now trending above the prime SPIN. On the other hand, nonbank financial institutions saw their loans more than 30 days in arrears fall to 0.50% in Q1 2018 from 0.60% in Q4 2017.

Arrears for nonconforming RMBS increased to 4.19% in Q1 2018 from 4.08% in Q4 2017. Some of this increase is off the back of a decline in outstanding loan balances. Arrears on investment loan arrears reached 1.19% in Q1. Owner-occupier loan arrears were 1.56% at the end of Q1.

Half of all interest-only loans in Australian RMBS transactions will reach their interest-only maturity date by 2019. We expect this transition to be more pronounced for investor loans, of which 46% have an interest-only period compared with 12% of owner-occupier loans underlying RMBS transactions.

Prepayment rates are declining. The average prepayment rate for March is 19.58% and they believe some borrowers could be facing refinancing difficulties in the face of tougher lending conditions. A slowdown in refinancing activity can precipitate a rise in arrears, particularly in the nonconforming sector because borrowers have fewer options available to manage their way out of financial difficulty.

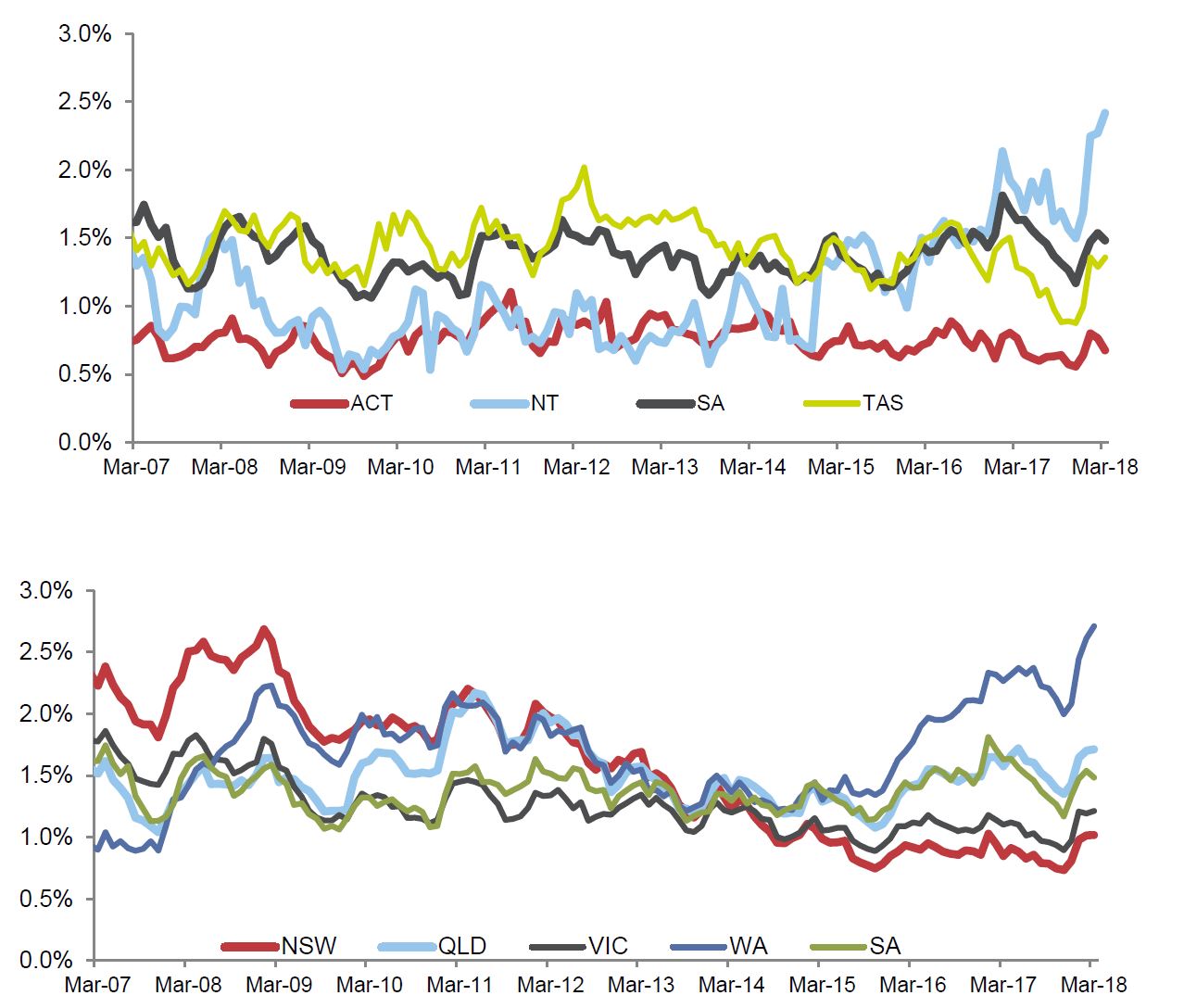

Across the states, the Australian Capital Territory in Q1 2018 again had the lowest arrears of all the states and territories, at 0.68%. Western Australia meanwhile again recorded the nation’s highest arrears, at 2.71%. Arrears rose during Q1 in most parts of the country. South Australia recorded the biggest year-on-year improvement in arrears, with loans more than 30 days in arrears declining to 1.48% in Q1 2018 from 1.63% in Q1 2017.

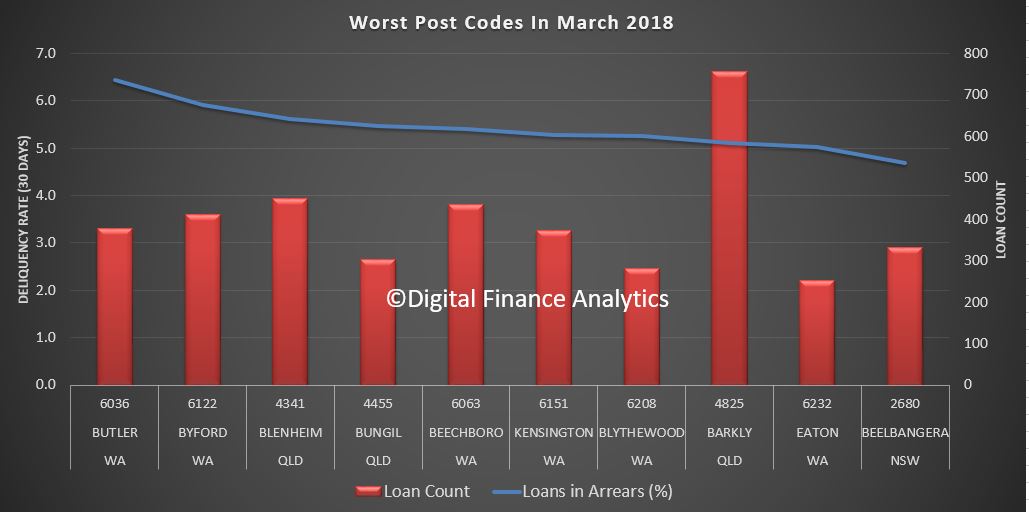

Nine of the 10 worst-performing postcodes in Q1 2018 are in Queensland and Western Australia. These included Butler, and 6036, Byford 6122, both in Western Australia, Blenheim 4341 and Bungil 4455 in Queensland, Beechboro 6063, Kensington 6151 and Blythewood 6208 in Western Australia, Barkly 4825 in Queensland, Eaton in Western Australia and Beelbangera 2680 in New South Wales.

They called out some important risk factors around interest rate rises and debt servicing.

Household indebtedness in Australia is high, particularly by international standards. This does not provide much headroom if the economic situation deteriorates or when interest rates start rise. Low interest rates and improving employment conditions are keeping mortgage arrears low in the Australian mortgage sector, but Australian borrowers’ sensitivity to rate rises has increased. A rapid ratcheting up of interest rates, as occurred between September 2009 and October 2011, when rates went up by around 2 percentage points, would see arrears go beyond their previous peaks, given household indebtedness has continued to increase during the past five years.

Debt serviceability issues are exacerbated in more subdued economic climates when refinancing opportunities are limited, particularly for borrowers of a higher credit risk, because lenders invariably tighten their lending criteria. In this scenario, some borrowers will find it harder to manage their way out of their financial situation, leading to higher arrears and potential losses. In our opinion, self-employed borrowers, nonconforming borrowers, and borrowers with high LTV loans are more likely to face greater refinancing difficulties in more subdued economic climates.

Property prices affect the level of net losses in the event of borrower default. From an RMBS perspective, the strong appreciation in property prices has increased borrowers’ equity for well-seasoned loans, and this helps to minimize the level of losses in the event of a borrower default. While property price growth is slowing, most loans underlying Australian RMBS transactions are reasonably well insulated from a moderate decline in prices. Given the high seasoning of the Australian RMBS sector of around 64 months, most borrowers have built up a reasonable degree of equity, as evidenced by the sector’s weighted-average LTV ratio of 60%. This provides a buffer against a moderate property price decline. Higher LTV ratio loans are more exposed to a decline in property prices because they have not built up as much equity to absorb potential losses. Around 14 % of total RMBS loans have high LTV ratios of more than 80%.

They conclude that arrears to trend higher if interest rates rise. Improving employment conditions and historically low interest rates will keep defaults low in the short to medium term, however. Economic headwinds such as softening property prices, rising interest rates, and tougher refinancing conditions will create cash-flow pressures for some borrowers.

So, two agencies with different perspectives. Personally, based on the data we have from our surveys, and as we discussed in our recent posts on both mortgage stress and household financial confidence, we suspect the SPIN data is closer to the mark – but bear in mind that RMBS mortgage pools are carefully selected, and many not contain higher risk loans. So even this may be understating the real state of play.

And in a way that nicely highlights the uncomfortable juxtaposition between the top level macroeconomic picture, and real life among Australian households. The trouble is, the state of the latter is very likely to impinge on the former as mortgage debt grinds on. And this could certainly lead to more issues down the track

Blog")