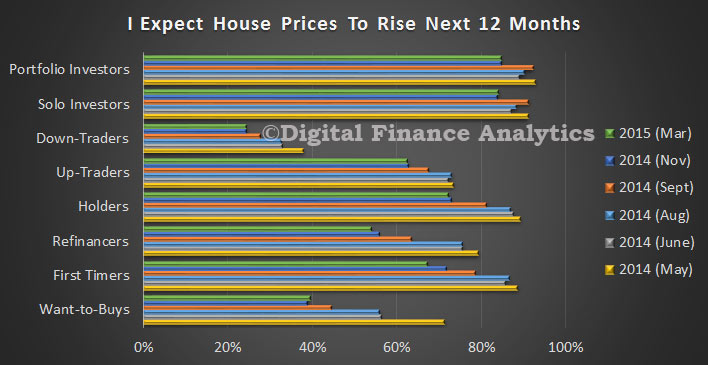

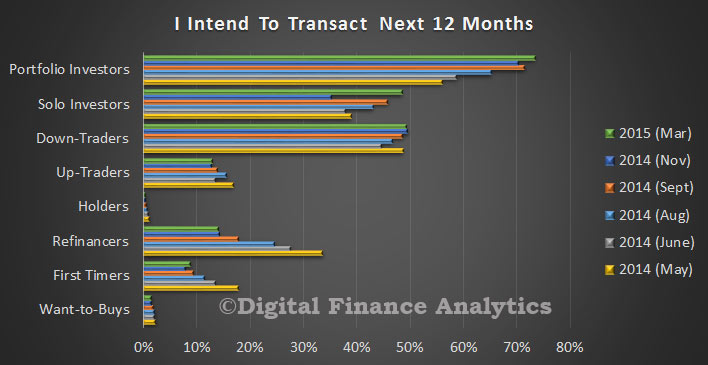

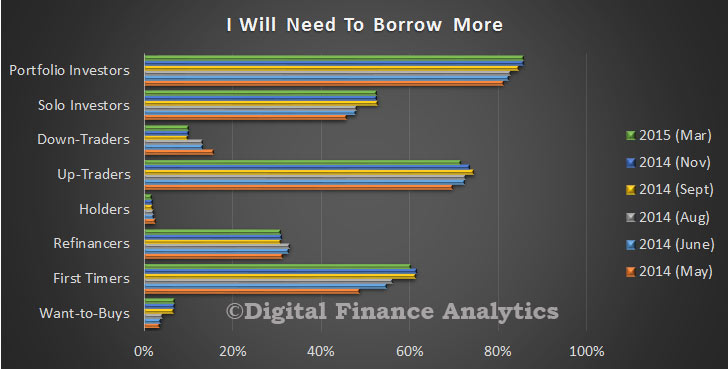

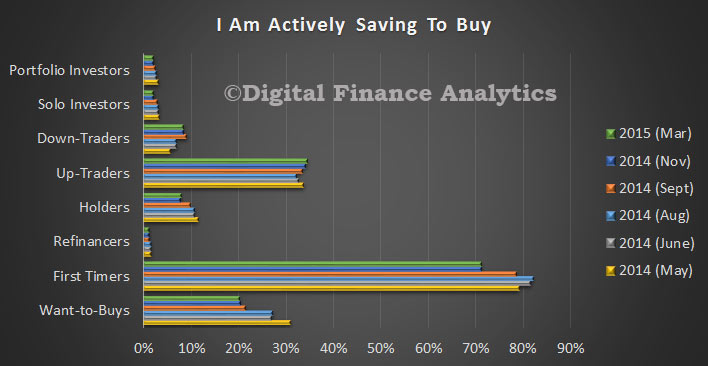

The Property Imperative, Fourth Edition, published April 2015 is available free on request. This report which summarises the key findings for our research into one easy to read publication. We continue to explore some of the factors in play in the Australian residential property market by looking at the activities of different household groups using our recent primary research, customer segmentation and other available data. Specifically we look at the property investment juggernaut and how we are becoming a nation of property speculators. It contains:

- results from the DFA Household Survey to end March 2015

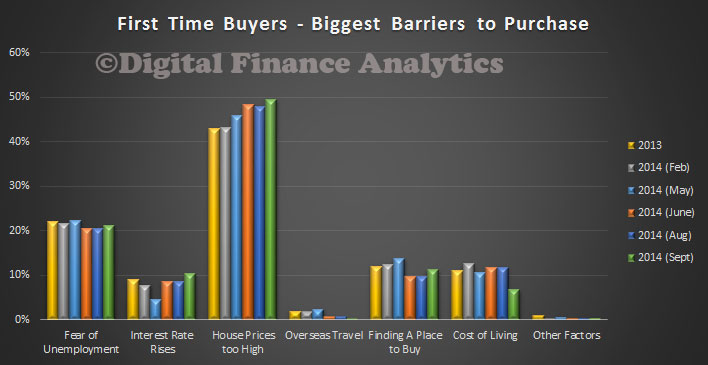

- a focus on first time buyer behaviour and overseas property investors

- an update of the DFA Household Finance Confidence Index

Go here to request a copy.

Go here to request a copy.From the introduction:

This report is published twice each year, drawing data from our ongoing consumer surveys and blog. This edition dates from April 2015.

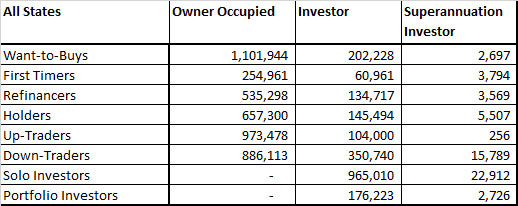

The Australian Residential Property market is valued at over $5.4 trillion and includes houses, semi-detached dwellings, townhouses, terrace houses, flats, units and apartments. In the past 10 years the total value has more than doubled. It is one of the most significant elements driving the economy, and as a result it is influenced by state and federal policy makers, the Reserve Bank, Banking Competition and Regulation and other factors. Residential Property is therefore in the cross-hairs of many players who wish to influence the economic fiscal and social outcomes of Australia. The Reserve Bank (RBA) has recently highlighted their concerns about potential excesses in the housing market is on their mind, when considering future interest rate cuts.

According to the Reserve Bank (RBA), as at February 2015, total housing loans were a record $1.43 trillion , with investment lending now at a record 34.4%, and representing more than half of all loans made last month. There were more than 5.2 million housing loans outstanding with an average balance of about $241,000. Approximately two-thirds of total loans were for owner-occupied housing, while one-third was for investment purposes. 36.9% of new loans issued were interest-only loans. This report will explore some of the factors in play in the Australian Residential Property market. We will begin by describing the current state of the market by looking at the activities of different household groups leveraging recent primary research and other available data. We also, in this edition, feature recent research into first time buyers and foreign investors; and look at household finance confidence.