The Official Cash Rate (OCR) remains at 1.5 percent. Given the weaker global economic outlook and the risk of ongoing subdued domestic growth, a lower OCR may be needed over time to continue to meet our objectives.

Domestic growth has

slowed over the past year. While construction activity strengthened in the

March 2019 quarter, growth in the services sector continued to slow. Softer

house prices and subdued business sentiment continue to dampen domestic

spending.

The global economic

outlook has weakened, and downside risks related to trade activity have

intensified. A number of central banks are easing their monetary policy

settings to support demand. The weaker global economy is affecting New Zealand

through a range of trade, financial, and confidence channels.

We expect low

interest rates and increased government spending to support a lift in economic

growth and employment. Inflation is expected to rise to the 2 percent mid-point

of our target range, and employment to remain near its maximum sustainable level.

Given the downside

risks around the employment and inflation outlook, a lower OCR may be needed.

Meitaki, thanks.

Summary

record of meeting

The Monetary Policy Committee agreed that the outlook for the economy

has softened relative to the projections in the May 2019 Statement.

The Committee noted that inflation remains slightly below the mid-point

of the inflation target and employment is broadly at its maximum sustainable

level. The Committee agreed that a lower OCR may be needed to meet its objectives,

given further deterioration in the outlook for trading-partner growth and

subdued domestic growth.

Relative to the May Statement, the Committee agreed that the

risks to achieving its consumer price inflation and maximum sustainable

employment objectives are tilted to the downside.

The members noted that global economic growth had continued to slow.

They discussed the recent falls in oil and dairy prices, and that several

central banks are now expected to ease monetary policy to support demand.

The Committee discussed the ongoing weakening in global trade activity.

A drawn out period of tension could continue to suppress global business

confidence and reduce growth. Resolution of these tensions could see

uncertainty ease.

The Committee discussed the trade, financial, and confidence channels

through which slowing global growth and trade tensions affect New Zealand. The

members noted in particular the dampening effect of uncertainty on business

investment. Some members noted that lower commodity prices and upward pressure

on the New Zealand dollar could see imported inflation remain soft.

While

global economic conditions had deteriorated, the Committee noted that domestic

GDP growth had held up more than projected in the March 2019 quarter. The members

discussed disparities in growth across sectors of the economy, with

construction strong and services weak. The members also discussed whether some

of the factors supporting growth in the quarter would continue.

The

members noted two largely offsetting developments affecting the outlook for

domestic growth: softer house price inflation and additional fiscal stimulus.

The

Committee noted that recent softer house prices, if sustained, are likely to

dampen household spending. The Committee also noted the recent falls in

mortgage rates and the Government’s decision not to introduce a capital gains

tax.

The

Committee noted that Budget 2019 incorporated a stronger outlook for

government spending than assumed in the May Statement. The members

discussed the impact on growth of any increase in government spending being

delayed, for example due to timing of the implementation of new initiatives and

current capacity constraints in the construction sector.

The

members discussed the subdued nominal wage growth in the private sector and the

apparent disconnect from indicators of capacity pressure in the labour market.

The Committee discussed the possibility of this relationship re-establishing.

Conversely, the continuing absence of wage pressure could indicate that there

is still spare capacity in the labour market. Some members also noted that

reduced migrant inflows could see wage pressure increase in some sectors.

The

Committee discussed whether additional monetary stimulus was necessary given

continued falls in global growth and subdued domestic demand. The members

agreed that more support from monetary policy was likely to be necessary.

The

Committee discussed the merits of lowering the OCR at this meeting. However,

the Committee reached a consensus to hold the OCR at 1.5

percent. They noted a lower OCR may be needed over time.

The Reserve Bank of New Zealand has released an important statement on the new approach they are going to adopt in policy setting. The focus will be on improving wellbeing. In addition they are expanding their dna to avoid group think. This follows their recent moves to lift bank capital.

There is so much here the RBA should embrace.

The Reserve Bank has significantly changed the way it makes monetary policy decisions, keeping itself in step with public expectations.

In a panel discussion last week at the Institute for Monetary and Economic Studies (Bank of Japan) in Tokyo, Reserve Bank Assistant Governor and General Manager of Economics, Financial Markets and Banking Christian Hawkesby talked about the importance of good decision making and governance, and of being credible and trusted, in achieving the long-term goal of improving wellbeing.

“We maintain our legitimacy as an institution by serving the public interest and fulfilling our social obligations. Keeping our ‘social licence’ to operate depends on maintaining the public’s trust that we are improving wellbeing,” Mr Hawkesby said.

“Thirty years ago New Zealand was prepared to accept a single expert – the Governor – making decisions about how to fight inflation. People now expect to see how and why decisions are made, expect that decision makers reflect wider society, and that current issues and concerns are factored into the decision making. By meeting these expectations, we can improve public trust in the legitimacy of the Reserve Bank’s work,” he said.

Mr Hawkesby outlined the new committee process that the Reserve Bank uses for deciding the official cash rate, noting that diversity among decision makers improves the pool of knowledge, insures against extreme views, and reduces groupthink.

“This diversity is needed to confront issues such as climate, technological, and other structural and social changes,” he said.

He also said that collaboration with government can be undertaken in a way that maintains the Reserve Bank’s political independence while working on the broader objective of improving wellbeing.

Here is the supporting speech.

Introduction

Tena koutou katoa

Thank you for the opportunity to talk about the Reserve Bank of New

Zealand and the changes we are making to maintain our credibility in

times of change.

I would like to focus on two building blocks of credibility:

renewing a social licence to operate by aligning our objectives with the needs of the public; and

achieving those objectives through good decision making enabled by a framework of good governance.

A common theme is the importance of transparency.

The imperative for change: Central banks in the 21st century

The first building block of credibility is the renewal of a social

licence to operate—by this I mean the legitimacy an institution earns by

serving the public interest. It is granted by the public when an

institution is seen to fulfil its social obligations.1

New Zealand was the first country to officially adopt inflation

targeting in 1989, with a number of central banks around the world

following the example.2

Under a single-decision-maker model, we brought inflation down from

around twenty percent to two percent in five years. In doing so, we

helped build our credibility during the high-inflation environment of

the times.3

Fast-forward to 2019, and monetary policy in New Zealand has

undergone major change. Firstly, we have adopted a dual mandate, focused

on achieving price stability and supporting maximum sustainable

employment. Secondly, we have adopted a committee structure for decision

making, and are delivering greater transparency in our decision making.

Why the change?

The reform of our framework was not merely a simple choice based on

technical performance. As you can see in figure 1, when it comes to

inflation and growth, over the past 30 years inflation-targeting central

banks (e.g. New Zealand and the United Kingdom) have a pretty similar

track record to central banks with a dual mandate (e.g. Australia and

the United States). 4

The imperative for change comes from more than examining our history;

it comes from our expectations of the future, and the present we find

ourselves in. Our policy framework changed because times are changing.

For the Reserve Bank to maintain its credibility and relevance, we must

change too.

Figure 1: Inflation, and GDP growth across monetary policy frameworks5

Wellbeing of our people

Inflation has been low and stable in New Zealand for nearly 30 years.

There is a greater appreciation that low inflation is a means to an

end, and not the end itself. In the fight to lower inflation that was

perhaps easy to forget. The end goal is, of course, improving the

wellbeing of our people.6

For many in the general public, employment is one tangible measure of wellbeing. Employment can provide an opportunity to earn your own wage, contribute to society, and live a fulfilling life.

It is in this light that the Reserve Bank Act (1989) has been amended to include a dual mandate with an employment

objective alongside our price stability goal. Incorporating the

objective of supporting maximum sustainable employment, and equally

weighting it alongside inflation, emphasises our long-term goal of

improving New Zealanders’ wellbeing. This aligns us with the needs of

the public. And it helps us renew our social licence to operate – the

first building block for maintaining our credibility.

But it is not enough for the public to believe in and understand our

objectives. We must also prove to them that they can be achieved. This

brings us to the second building block necessary for maintaining

credibility: establishing modern governance principles for dealing with

modern problems, and translating good governance into good decisions.

Good governance

In preparing for our dual mandate, and a formal Monetary Policy

Committee (MPC), we have updated the principles and processes that form

our governance framework for monetary policy.

In pursuit of greater transparency, we have also published these

principles and processes in a comprehensive Monetary Policy Handbook

(the Handbook). 7 This is an essential document, for everyone from school students to MPC members.

Importantly, it is also a living document that will evolve as our understanding evolves.

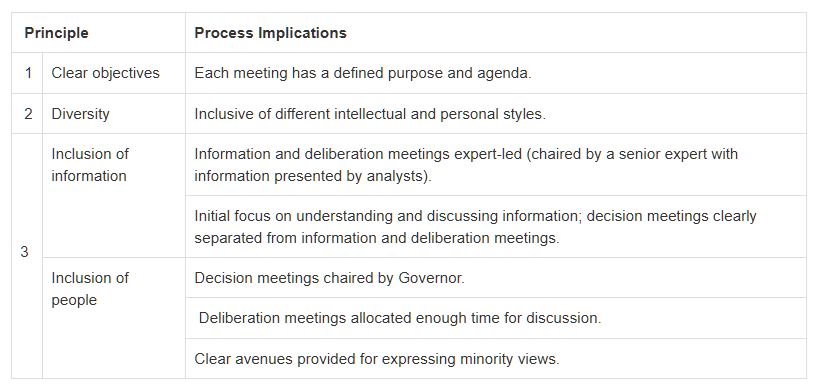

Principles

The first part of the Handbook I would like to cover is the section on MPC deliberation principles. 8

Figure 2: MPC deliberation principles

There are three principles which guide the deliberations within the MPC.

I’ve talked already about providing clarity around our objectives –

the equal weighting of our employment and inflation goals. This is the

first of our three principles.

The second, is diversity – diversity in the skills, experiences, thoughts, and personal characteristics of the MPC members.

The third, is inclusion – inclusion of information and people, ensuring decisions are made on the basis of all the available insights, and reflecting the views of all of the committee members.

Why are diversity and inclusion so important?

The governance literature shows that diversity and inclusion improves

the pool of committee knowledge, insures against extreme views, and

reduces groupthink.9 These principles drive the committee towards an unbiased policy decision – the best that is possible given existing information.

Think about this from a practical perspective. Modern monetary policy

is confronted by diverse issues such as climate, technological, and

other structural and social changes. A sole decision maker or uniform

committee cannot possibly hope to possess the broad range of insights

necessary to consider these issues.

A diverse committee operating in an inclusive environment can. It is

these additional insights that improve collective understanding, and

lead to better monetary policy decisions.

So you see these principles are not simply rhetorical devices. They

are carefully chosen pillars to support our credibility though good

decision making in achieving our dual mandate.

Good decision making

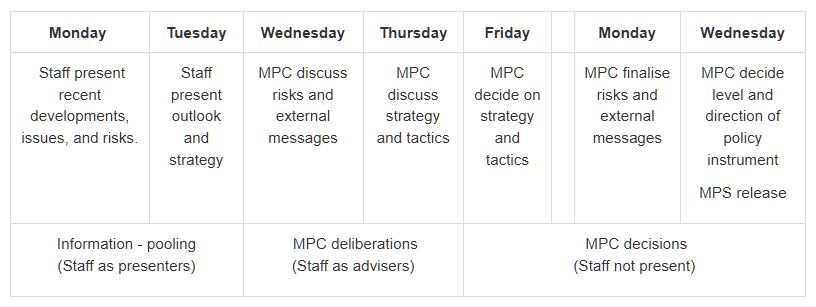

Processes

Our principles of good governance have directly influenced the policy-setting process of the MPC. 10

This is a process that has been designed with consensus-based decision

making front and centre, consistent with the agreement with the Minister

of Finance. 11

Figure 3: The structure of the forecast week for quarterly Monetary Policy Statements

We begin with information pooling, which flows through to MPC

deliberations, and culminates in the final decision making meeting.

As you can see, the policy-setting framework is highly collaborative

and deliberate. Deliberate in the sense that the process inspires lively

debate, giving MPC members every possible chance to challenge

assumptions, critique policy judgements and assess a range of policy

strategies to achieve our dual mandate objectives.

A crucial part of this is that the MPC members hold back their views

on the decision until the final stages, rather than starting with them.

This supports evidence-based decision making and guards against

confirmation bias.

The process begins with open information pooling on recent

developments and the outlook for the economy. Here, the MPC have the

opportunity to investigate and challenge the assumptions made in the

staff’s initial forecasts. This is where the MPC member’s judgement

enters the picture, and where creative tensions improve collective

understanding.

While the MPC members may enter the room with different insights and

questions about the economy, at the end of the information pooling stage

the committee shares a common reference point for the economic outlook.

There are numerous opportunities to discuss and reflect on key

issues, judgements, risks, strategy, and communication throughout the

week. There are also a number of anonymous internal surveys we perform

to gauge collective opinion among staff and MPC members.12

By the end of the week-and-a-half, the final monetary policy decision reflects the greater momentum of the MPC’s discussion.

We publish the final Official Cash Rate (OCR) decision, a Monetary Policy Statement (MPS), and a Summary Record of Meeting at the same time.

The Summary Record of Meeting captures the key judgements

and risks underpinning the central forecasts and decision, as well as

indicating where members of the MPC had different views. We identify any

differing views, and communicate where the most significant

uncertainties lie in our baseline forecasts.13

If consensus cannot be reached, a vote by simple majority would be

carried out, and the reasoning behind different stances disclosed in the

Summary Record of Meeting.

Our desire is that the transparency provided in the Handbook can help

the public understand how the Bank’s collective ‘mind’ works. If the

public can see the analytical rigour in our decision making, they should

have greater confidence in the MPC’s conclusions, and thus more faith

in the Reserve Bank.

Our credibility will be supported in the long run if the decisions

made by the MPC are unbiased and effective ones. Our results will speak

louder than our words.

Monetary policy strategy and our May decision

So far I’ve talked about the principles and processes we follow in

setting policy. Now I’m going to cover how we ‘walk the talk’ in

formulating our monetary policy decisions.14

Sound and effective monetary policy strategy requires more than just

deciding whether the OCR should go up or down on any given day; instead

central banks need to be transparent about their views of the economy

over the medium-term and how monetary policy might respond to a changing

economic landscape.

In this regard, around twenty years ago, the Reserve Bank became a

pioneer in another way. When publishing our interest rate decisions, we

also began to publish a forward (and endogenous) projection of interest

rates in the future. We use this to capture the overall stance of

monetary policy.

This tool remains integral to how the MPC sets monetary policy and understands the potential trade-offs with a dual mandate.

The first monetary policy decision of the new MPC occurred last

month, in May. Our starting point was a New Zealand economy where the

labour market was operating near maximum sustainable employment, and

annual core inflation pressures were within our 1 to 3 percent target

range but below the 2 percent mid-point.

We discussed the slowdown in global growth, and how this might affect

New Zealand. We also addressed the recent loss of domestic economy

momentum since mid-2018, through both tempered household spending and

restrained business investment.

In order to continue achieving our policy objectives, we agreed that

additional monetary stimulus was needed to help bring inflation back to

the 2 percent mid-point and support maximum sustainable employment. We

then turned to the question of the magnitude of stimulus we wanted to

adopt (the stance) and the timing and means by which we would try to

deliver this (the tactics).

Figures 4–6 show how different OCR paths could have been used to

achieve our objectives. While each path was consistent with meeting our

objectives, they each offered different trade-offs.15

Figure 4: Official Cash Rate (OCR) paths to achieve alternative monetary policy stances

Figures 5-6: Inflation, and employment gap under alternative OCR paths

If we kept rates unchanged (the higher OCR path), our projections

suggested that it would have taken a number of years for inflation to

return to target, and employment would have fallen below the maximum

sustainable level.

If we lowered the OCR by around 75 basis points over the next 12 months

(the lower OCR path), our projections suggested it would result is a

situation where both inflation and employment would be overshooting

their targets.

By contrast, the baseline (our final published projection), with the

OCR around 40 basis points lower over the next 12 months, brought

inflation back to target in a reasonable time period, with employment

remaining near the maximum sustainable level. We decided this path

captured our preferred strategy, and was robust to the key risks we had

discussed.

After agreeing on the appropriate stance of monetary policy, MPC

turned to the tactical decision of where to set the OCR at the May

meeting, and decided to cut the OCR by 25 basis points to provide a more

balanced outlook for interest rates.

This brings us to discuss the future.

Maintaining credibility in the future

Our central view is that New Zealand’s interest rates will remain

broadly around current levels for the foreseeable future. However, we

need to be ready to adapt to changing conditions, to meet our objectives

even when confronted with unforeseen developments.

An issue that policymakers and academics are grappling with around

the world is the role of both monetary and fiscal stimulus in a world of

low interest rates.

There is emerging consensus that coordination is necessary for an optimal response of broader macroeconomic policy.16 For central banks, operational independence does not have to mean operational isolation.

Rather, collaboration with government can be done in a way that builds

and reinforces the social licence to operate, by showing a willingness

to work with other partners to do whatever is necessary to achieve the

broader objective—improving public wellbeing.

Even with coordination between monetary and fiscal policy, if further

macroeconomic stimulus is needed quickly, the first line of defence

will still inevitably fall upon central banks.17

In New Zealand, we are in the strong position of having further room to provide conventional monetary stimulus if required (using the OCR).

Having effective unconventional policy options expands the

toolbox of a central bank, which is naturally more relevant in a low

interest rate environment. In this spirit, we published a Bulletin article last year on the practicalities of unconventional monetary tools in a New Zealand context, and we continue to learn from the lessons of our central banking cousins.18

It’s better to have a tool and not need it, than need one and not have it.

Conclusion

In the Handbook, we explore the history of central banking objectives, and see how dramatically they have evolved over time. 19

We haven’t always had a mandate to support maximum sustainable

employment, or to achieve price stability, or even control over interest

rates or the money supply.

Nothing lasts forever, and it is possible that the role of central

banks may change again in the future. Our Handbook will inevitably

change. We need to be ready to adapt when changes beckon.

And it is not enough to grudgingly adapt. In order to

maintain credibility, central banks must embrace change and prove to the

public that they are capable of delivering on their objectives. To

remain credible is to remain relevant. Central banks should keep their

eyes open, and be ready to change tack. Our destination—a world with

improved wellbeing for our citizens—may not change, but the best route

for getting there may.

We must adapt. We must continue to improve the wellbeing of our citizens. We must remain credible.

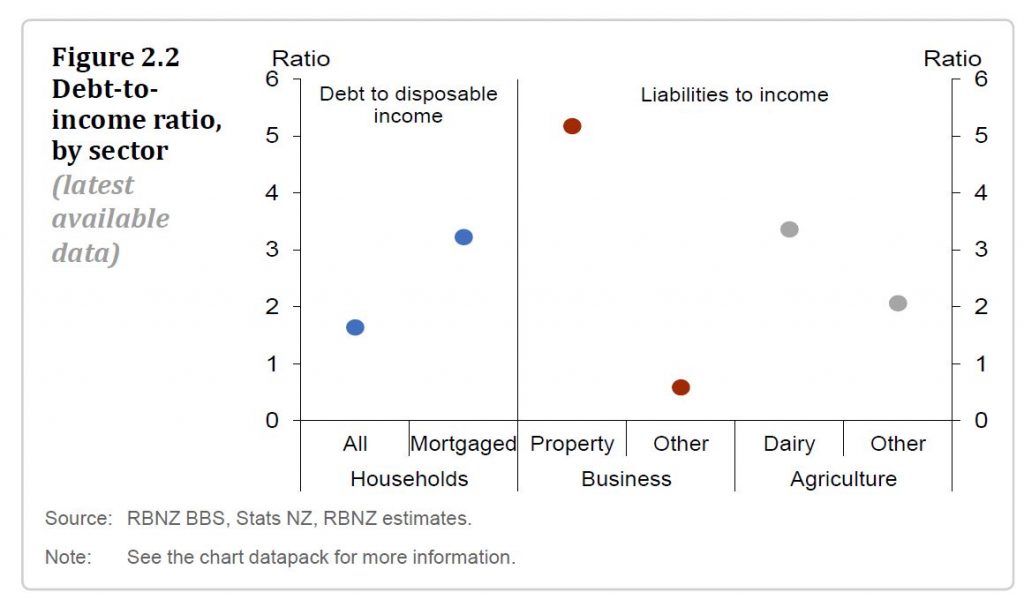

The New Zealand financial system remains resilient to a broad range of economic risks. However, financial system risks remain elevated, and ongoing effort is necessary to bolster system soundness and efficiency.

Domestically,

debt levels are high in the household and dairy sectors, leaving borrowers and

lenders exposed to unanticipated events. Similar challenges exist globally,

given current high public and private debt levels, and stretched asset prices

in many of New Zealand’s trading partners.

Some regions have recently had high house price growth. This is not an immediate financial stability concern as those regions have smaller and less stretched housing markets than Auckland. But if strong price growth continued, the financial system would become more exposed to those regions. The Global Financial Crisis (GFC) showed that house prices can fall dramatically in small regions.

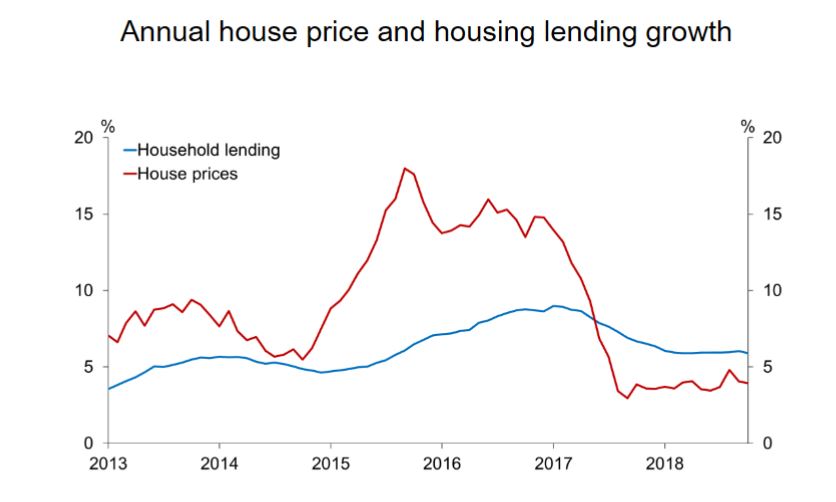

At a national level, the growth of household debt and house prices has slowed, but household debt has still grown faster than income in the past year. Housing market pressures could re-emerge if there is a strong response to the recent decline in mortgage rates, or reduced uncertainty about the future tax treatment of property investments.

Given this environment, the financial system’s vulnerability to risks in the household sector remains elevated, and must continue to be closely monitored and managed.

The capacity for some foreign governments and central banks to respond to unanticipated negative events is also limited by their current high government debt and low nominal interest rates. It is imperative to improve New Zealand’s financial system resilience while conditions are conducive.

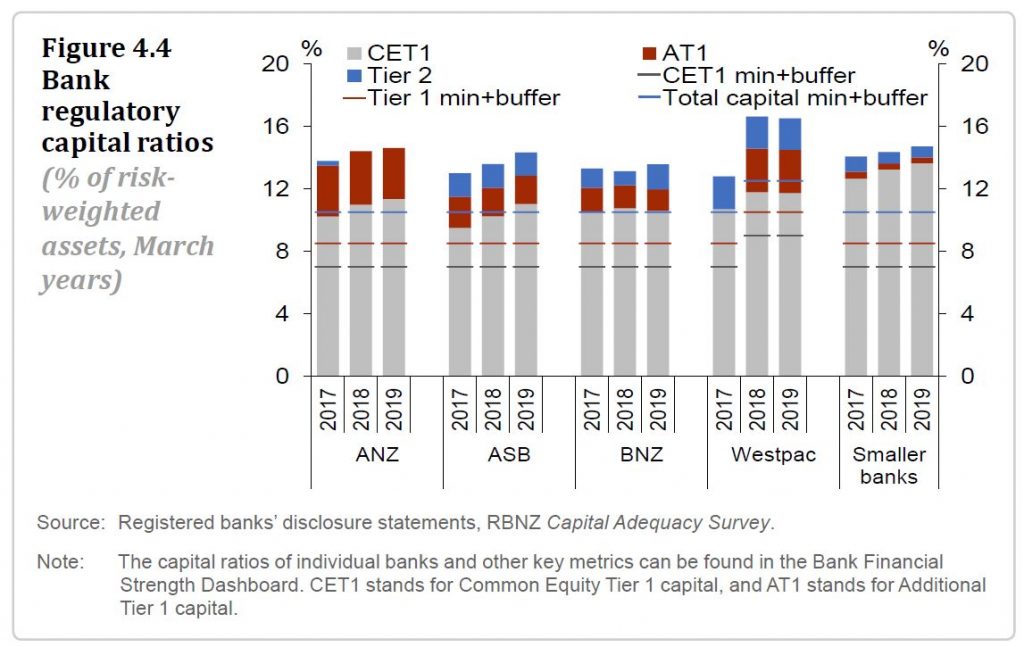

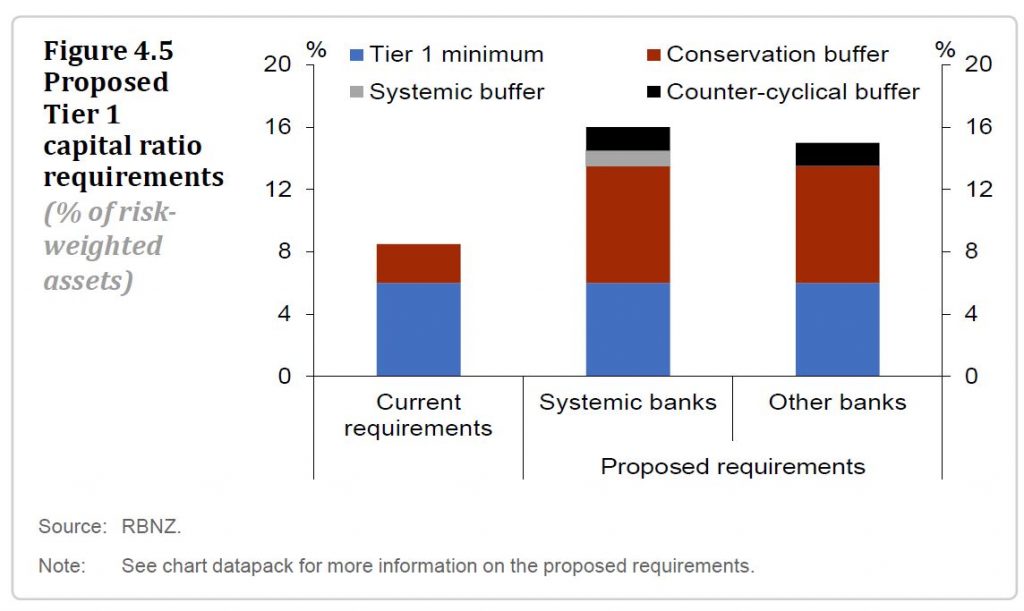

Increasing financial institutions’ capital positions is central to ensuring that they can withstand severe shocks. We have proposed higher capital requirements for banks, and are currently reviewing public submissions on this proposal.

There is also a need for some insurers and non-bank deposit takers to improve their capital buffers. We will be reviewing insurer solvency standards in the months ahead.

Financial

resilience also includes service providers taking a long-term customer outcome

focus, to both maintain confidence and promote sound resource allocation. We

will ensure banks and insurers respond to the issues identified in our recent

review of their conduct and culture.

A longer-term

focus is also necessary for financial firms to adapt to the changing

competitive, regulatory, and natural environment.

Insurers are changing how they manage their exposure to natural disaster events, which is altering affordability. Risks associated with climate change are also impacting on the accessibility of insurance, with potential flow-on effects on bank lending. These risks must be appropriately identified and priced, so as to best ensure a stable transition over coming years.

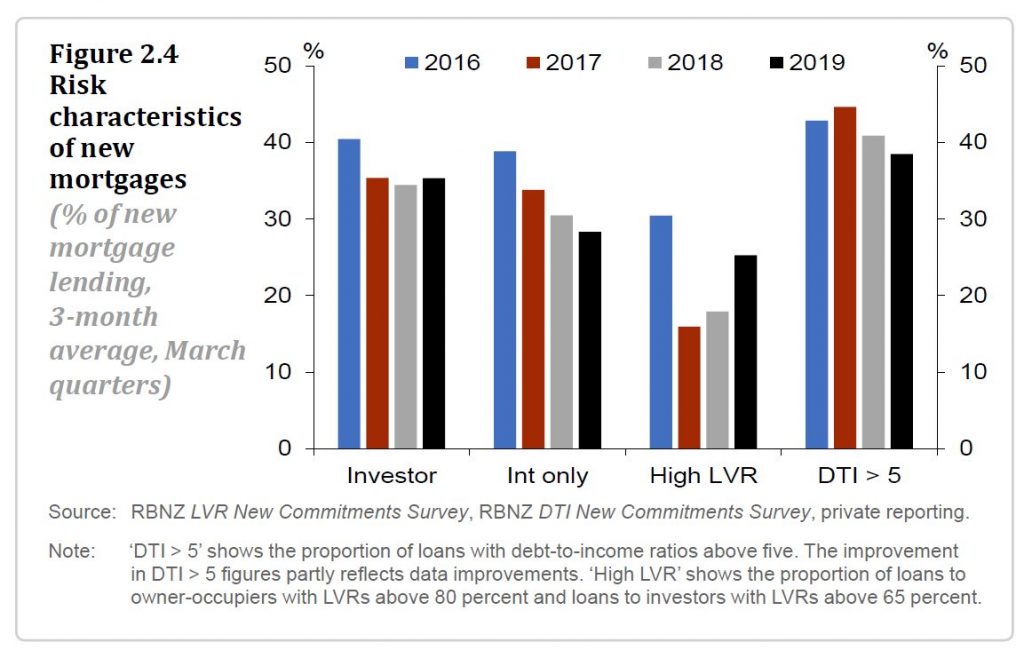

The Reserve Bank’s loan-to-value ratio (LVR) restrictions have been successful in reducing some of the risk associated with high household indebtedness. The current LVR settings remain appropriate for now, with any further easing subject to continuing subdued growth in credit and house prices and banks maintaining prudent lending standards.

The Official Cash Rate (OCR) has been reduced to 1.5 percent. They signalled risks from China and Australia, and that lower mortgage rates might help household finances and housing.

The Monetary Policy

Committee decided a lower OCR is necessary to support the outlook for

employment and inflation consistent with its policy remit.

Global economic growth

has slowed since mid-2018, easing demand for New Zealand’s goods and services.

This lower global growth has prompted foreign central banks to ease their

monetary policy stances, supporting growth prospects.

However, there is

uncertainty about the global economic outlook. Trade concerns remain, while

some other indicators suggest trading-partner growth is stabilising.

Domestic growth slowed

from the second half of 2018. Reduced population growth through lower net

immigration, and continuing house price softness in some areas, has tempered

the growth in household spending. Ongoing low business sentiment, tighter

profit margins, and competition for resources has restrained investment.

Employment is near its

maximum sustainable level. However, the outlook for employment growth is more

subdued and capacity pressure is expected to ease slightly in 2019.

Consequently, inflationary pressure is projected to rise only slowly.

Given this employment

and inflation outlook, a lower OCR now is most consistent with achieving our

objectives and provides a more balanced outlook for interest rates.

Summary record of meeting – May 2019 Statement

The Monetary Policy Committee agreed on the economic

projections outlined in the May 2019 Statement in order to provide a

sound basis on which to form its OCR decision.

The Committee noted that inflation is currently

slightly below the mid-point of the inflation target, and that employment is

broadly at the targeted maximum sustainable level. However, the members agreed

that given the recent weaker domestic spending, and projected ongoing growth

and employment headwinds, there was a need for further monetary stimulus to

meet its objectives.

The Committee agreed that the risks to achieving its

consumer price inflation and maximum sustainable employment objectives were

broadly balanced around the projection. Possible alternative outcomes were

noted on the upside and downside.

A key downside risk relating to the growth projections was a larger than anticipated slowdown in global economic growth, particularly in China and Australia, New Zealand’s largest trading partners. The Committee agreed that the projections adequately captured the observed global slowdown and its impact on domestic employment and inflation.

The Committee noted that additional stimulus from

central banks had underpinned growth and reduced the likelihood of a

more-pronounced slowdown. With some indicators of global growth improving in

recent months, a faster recovery in global growth was possible. However, on

balance, the Committee was more concerned about a continued slowdown rather than

a faster recovery.

The Committee discussed other potential risks to

domestic spending. The members acknowledged the importance of additional

spending from households, businesses, and the government, to meet their

inflation and employment targets. However, they noted several important

uncertainties.

The Committee noted upside and downside risks to the

investment outlook. Capacity pressure could see investment increase faster than

assumed. On the downside, if sentiment remained low as profitability remains

squeezed, investment might not increase as anticipated over the medium term. It

was also noted that firms’ ability to invest is constrained by the current

competition for resources.

A potential source of additional demand discussed by

the Committee included government spending being higher than currently

projected, in view of the current strength of the Crown balance sheet. This

view was balanced by the impact of any increase in government investment being

delayed, for example due to timing of the implementation of new initiatives and

current capacity constraints in the construction sector. The implications for

monetary policy remain to be seen.

Some members noted that with lower mortgage rates and easing of loan-to-value requirements, any possible pick-up in the housing market could support household spending growth more than anticipated.

The Committee noted that employment is currently near

its maximum sustainable level. However, it was agreed that the outlook for

employment growth is more subdued and capacity pressure is expected to ease

slightly in 2019.

The Committee agreed that overall risks to the

inflation projection were balanced. The Committee noted the outlook for

inflation is below the target mid-point for longer than projected in the February

Statement.

The recent period of rising domestic inflation was

discussed. The Committee noted that the near-term outlook was more subdued due

to lower capacity pressure. It was also noted that cost pressures remain

elevated, and that there is a risk firms may pass these costs on as higher

consumer prices by more than assumed. However, it was agreed that inflation

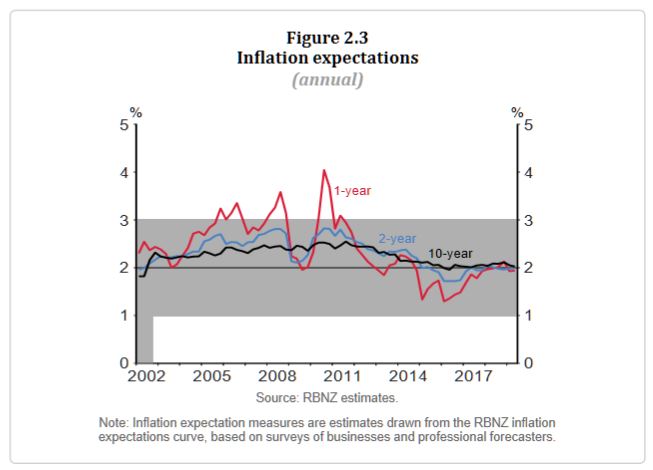

expectations remain well anchored at the mid-point of the target range.

The Committee also noted the relatively subdued

private sector wage growth, despite businesses suggesting that the inability to

find labour is a significant constraint on their growth. The Committee noted

the limited pass-through of the nominal wage growth to consumer price

inflation.

Some members noted slower global growth reducing

imported inflation was a downside risk to the inflation outlook.

The Committee reached a consensus that, relative to

the February Statement, a lower path for the OCR over the projection

period was appropriate. The lower path reflected the economic projections and

the balance of risks discussed, and is consistent with both inflation and

employment remaining near the Committee’s objectives.

After discussing the relative benefits of holding the

OCR and committing to a downward bias, versus cutting the OCR now so as to

establish a more balanced outlook for interest rates, the Committee reached a

consensus to cut the OCR to 1.50 percent.

Central Banking Publications has

named the Bank Financial Strength Dashboard as ‘Initiative of the Year’ in its

annual awards.

In announcing the award, Central Banking commented that very few

central banks have opened up their financial system to public scrutiny to quite

the same level as the Reserve Bank of New Zealand.

They said that by revealing key

metrics on the banking sector in a visual format that can be taken in at a glance,

the Reserve Bank has hit on a simple method of boosting discipline among banks.

Reserve Bank Governor Adrian Orr

said the award was a great honour.

“We aspire to be a ‘Great Team, Best

Central Bank’ and the award recognises a significant step towards that goal,”

Mr Orr said.

“Awareness among consumers and

investors is an important aspect of ensuring a sound financial system. The Dashboard

is designed to make it easy to access and understand the financial position of

New Zealand banks. By keeping the public informed about risks to the sector,

banks themselves are held to greater market discipline.

“The Dashboard

has proven very popular, with more than 10,000 visits per quarter since its

launch and we believe this has significantly broadened the audience for

prudential disclosures.

“It is the result of huge effort and

dedication from many people in our organisation and the sector at large. I

congratulate them all and encourage people to use the Dashboard

when making banking decisions,” Mr Orr said.

Background

Central Banking Publications is a

financial publisher owned by Incisive Media and specialising in public policy

and financial markets, with emphasis on central banks, international financial

institutions and financial market infrastructure and regulation.

Central Banking Publications was

founded in 1990, and makes a number of annual awards to central banks and

market participants over a range of categories. This is the sixth year of the

awards.

The Reserve Bank previously won the

‘Initiative of the year’ award in 2016 for its enterprise risk management

system. It has also won ‘Central Bank of the Year’ in 2015 and Reserve Bank

senior adviser Leo Krippner won the award for ‘Economics in Central Banking’ in

2017.

Judging was by the Central Banking

Awards Committee, which is made up of the Central Banking Editorial Team and

Editorial Advisory Board, comprising former senior central bank governors from

around the world.

The awards will be presented at a gala dinner in

London on 13 March.

I discuss the latest developments in the New Zealand property market with Joe Wilkes. We look at the latest from the Reserve Bank, Deposit Bail-In and Bank Scorecards. Also highly relevant to other markets.

Please share this post to help to spread the word about the state of things….

Caveat Emptor! Note: this is NOT financial or property advice!!

The Reserve Bank New Zealand says that risks to New Zealand’s financial system have eased over the past six months, but vulnerabilities persist. In particular, households remain exposed to financial shocks due to their large mortgage debt burden.

But they are easing the loan to value restrictions from January 2019.

Up to 20 percent (increased from 15 percent) of new mortgage loans to owner occupiers can have deposits of less than 20 percent.

Up to 5 percent of new mortgage loans to property investors can have deposits of less than 30 percent (lowered from 35 percent).

They say that both mortgage credit growth and house price inflation have eased to more sustainable rates, reducing the riskiness of banks’ new housing lending. In response, we are easing our loan-to-value ratio (LVR) restrictions on banks’ new mortgage loans. If banks’ lending standards are maintained we expect to further ease LVR restrictions over the next few years.

Debt levels also remain high in the agriculture sector, particularly for dairy farms, implying ongoing financial vulnerability. Balance sheets need to be further strengthened. In the medium-term, an industry response to a variety of climate change-related challenges appears likely, requiring investment.

While domestic risks have eased, global financial vulnerability has risen. Significant build-ups in debt and asset prices, and ongoing geopolitical tensions, overhang financial markets. This vulnerability is highlighted by the current elevated price volatility in equity and debt markets. New Zealand’s exposure to these global risks has reduced somewhat, as New Zealand banks have become less reliant on short-term, and foreign, funding.

The domestic banking system remains sound at present. We are using this period of relative calm to reassess whether the banking system has sufficient capital to weather future extreme shocks. Our preliminary view is that higher capital requirements are necessary, so that the banking system can be sufficiently resilient whilst remaining efficient. We will release a final consultation paper on bank capital requirements in December.

The banking system remains profitable, reflecting banks’ low operating costs and strong asset performance. While positive overall, banks’ low costs have been partly achieved through underinvestment in core IT infrastructure and risk management systems in New Zealand. This was highlighted in our review of bank’s conduct and culture with the Financial Markets Authority. We will be jointly reviewing banks’ responses to our review in March 2019, and following up as required.

CBL Insurance Ltd was placed into full liquidation by the High Court on 12 November. Aside from CBL, the insurance sector as a whole is meeting its minimum capital requirements. However, capital strength has declined and a number of insurers are operating with small buffers. The insurance industry must ensure it has sufficient capital to maintain solvency in all business conditions. Our ongoing review of conduct and culture in the insurance sector with the Financial Markets Authority will illuminate the industry’s risk management capability. The review will be released in January 2019.

The Reserve Bank of New Zealand has kept the Official Cash Rate (OCR) at 1.75 percent. They expect to keep the OCR at this level through 2019 and into 2020. Their latest statement on monetary policy was released.

There are both upside and downside risks to our growth and inflation projections. As always, the timing and direction of any future OCR move remains data dependent.

The pick-up in GDP growth in the June quarter was partly due to temporary factors, and business surveys continue to suggest growth will be soft in the near term. Employment is around its maximum sustainable level. However, core consumer price inflation remains below our 2 percent target mid-point, necessitating continued supportive monetary policy.

GDP growth is expected to pick up over 2019. Monetary stimulus and population growth underpin household spending and business investment. Government spending on infrastructure and housing also supports domestic demand. The level of the New Zealand dollar exchange rate will support export earnings.

As capacity pressures build, core consumer price inflation is expected to rise to around the mid-point of our target range at 2 percent.

Downside risks to the growth outlook remain. Weak business sentiment could weigh on growth for longer. Trade tensions remain in some major economies, raising the risk that trade barriers increase and undermine global growth.

Upside risks to the inflation outlook also exist. Higher fuel prices are boosting near-term headline inflation. We will look through this volatility as appropriate. Our projection assumes firms have limited pass through of higher costs into generalised consumer prices, and that longer-term inflation expectations remain anchored at our target.

We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.

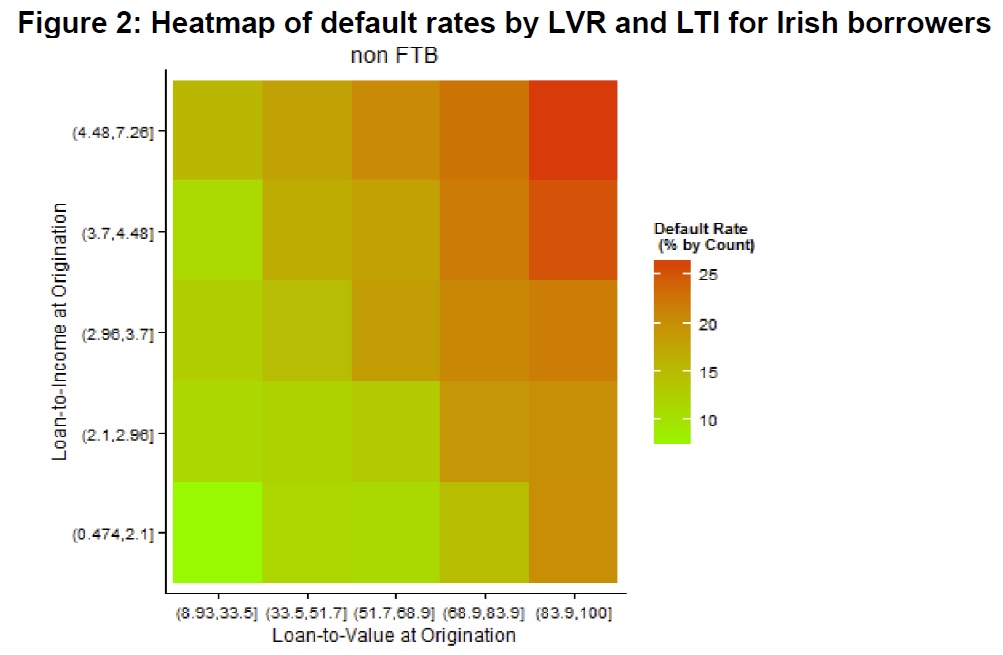

The NZ Reserve Bank has released its consultation paper on possible DTI restrictions. The 36+ page report is worth reading as it sets out the risks ensuring from high risk lending, leveraging experience from countries such as Ireland.

Interestingly they build a cost benefit analysis, trading off a reduction in the costs of a housing and financial crisis with a reduction in the near-term level of economic activity as a result of the DTI initiative and the cost to some potential homebuyers of having to delay their house purchase.

Submissions on this Consultation Paper are due by 18 August 2017.

In 2013, the Reserve Bank introduced macroprudential policy measures in the form of loan to-value ratio (LVR) restrictions to mitigate the risks to financial system stability posed by a growing proportion of residential mortgage loans with high LVRs (i.e. low deposit or low equity loans). This increase in borrower leverage had gone hand-in-hand with significant increases in house prices, particularly in Auckland. The Reserve Bank’s concern was the possibility of a sharp fall in house prices, in adverse economic circumstances where some borrowers had trouble servicing loans. Such an event had the potential to undermine bank asset quality given the limited equity held by some borrowers.

The Reserve Bank believes LVR restrictions have been effective in reducing the risk to financial system stability that can arise due to a build-up of highly-leveraged housing loans on bank balance sheets. However, LVRs relate mainly to one dimension of housing loan risk. The other key component of risk relates to the borrower’s capacity to service a loan, one measure of which is the debt-to-income ratio (DTI). All else equal, high DTI ratios increase the probability of loan defaults in the event of a sharp rise in interest rates or a negative shock to borrowers’ incomes. As a rule, borrowers with high DTIs will have less ability to deal with these events than those who borrow at more moderate DTIs. Even if they avoid default, their actions (e.g. selling properties because they are having difficulty servicing their mortgage) can increase the risk and potential severity of a housing related economic crisis.

While the full macroprudential framework will be reviewed in 2018, the Reserve Bank has elected to consult the public prior to the review. This consultation concerns the potential value of a policy instrument that could be used to limit the extent to which banks are able to provide loans to borrowers that are a high multiple of the borrower’s income (a DTI limit). A number of other countries have introduced DTI limits in recent years, often in association with LVR restrictions. In 2013, the Bank and the Minister of Finance agreed that direct, cyclical controls of this sort would not be imposed without the tool being listed in the Memorandum of Understanding on Macroprudential Policy (the MoU). Hence, cyclical DTI limits will only be possible in the future if an amended MoU is agreed.

The purpose of this consultation is for the Reserve Bank, Treasury and the Minister of Finance to gather feedback from the public on the prospect of including DTI limits in the Reserve Bank’s macroprudential toolkit.

Throughout the remainder of the document we have listed a number of questions, but feedback can cover other relevant issues. Information provided will be used by the Reserve Bank and Treasury in discussing the potential amendment of the MoU with the Minister of Finance. We present evidence that a DTI limit would reduce credit growth during the upswing and reduce the risk of a significant rise in mortgage defaults during a subsequent severe economic downturn. A DTI limit could also reduce the severity of the decline in house prices and economic growth in that severe downturn (since fewer households would be forced to sharply constrain their consumption or sell their house, even if they avoided actual default). The strongest evidence that these channels could materially worsen an economic downturn tends to come from countries that have experienced a housing crisis in recent history (including the UK and Ireland). The Reserve Bank believes that the use of DTI limits in appropriate circumstances would contribute to financial system resilience in several ways:

– By reducing household financial distress in adverse economic circumstances, including those involving a sharp fall in house prices;

– by reducing the magnitude of the economic downturn, which would otherwise serve to weaken bank loan portfolios (including in sectors broader than just housing); and

– by helping to constrain the credit-asset price cycle in a manner that most other macroprudential tools would not, thereby assisting in alleviating the build-up in risk accompanying such cycles.

The policy would not eliminate the need for lenders and borrowers to undertake their own due diligence in determining that the scale and terms of a mortgage are suitable for a particular borrower. The focus would be systemic: on reducing the risk of the overall mortgage and housing markets becoming dysfunctional in a severe downturn, rather than attempting to protect individual borrowers. The consultation paper notes that DTIs on loans to New Zealand borrowers have risen sharply over the past 30 or so years, with further increases evident since 2014. This partly

reflects the downward trend in interest rates over the period. However, interest rates may rise in the future. While the Reserve Bank is continuing to work with banks to improve this data, the available data also show that average DTIs in New Zealand are quite high on an international basis, as are New Zealand house prices relative to incomes.

Other policies (such as boosting required capital buffers for banks, or tightening LVR restrictions further) could be used to target the risks created by high-DTI lending. The Bank does not rule out these alternative policies (indeed, we are currently undertaking a broader review of capital requirements in New Zealand) but consider that they would not target our concerns around mortgage lending as directly or effectively. For example, while higher capital buffers would provide banks with more capacity to withstand elevated housing loan defaults, they would do little to mitigate the feedback effects between falling house prices, forced sales and economic stress.

The Reserve Bank has stated that it would not employ a DTI limit today if the tool was already in the MoU (especially given recent evidence of a cooling in the housing market and borrower activity), it believes a DTI instrument could be the best tool to employ if house prices prove resurgent and if the resurgence is accompanied by further substantial volumes of high DTI lending by the banking system. The Reserve Bank considers that the current global environment, with low interest rates expected in many countries over the next few years, tends to exacerbate the risk of asset price cycles arising from ‘search for yield’ behaviour, making the potential value of a DTI tool greater.

The exact nature of any limit applied would depend on the circumstances and further policy development. However, the Reserve Bank’s current thinking is that the policy would take a similar form to LVR restrictions. This would involve the use of a “speed limit”, under which banks would still be permitted to undertake a proportion of loans at DTIs above the chosen threshold. By adopting a speed limit approach, rather than imposing strict limits on DTI ratios, there would be less risk of moral hazard issues arising from a particular ratio being seen as “officially safe”. Exemptions similar to those available within the LVR restriction policy would also be likely to apply.

Interesting note from the New Zealand Reserve Bank, “Evaluating alternative monthly house price measures for New Zealand” which highlights that whilst there are various methods which can be applied to measuring home prices, none is perfect. The data-intensive “Hedonic” approach as advocated by some in Australia, did not come out on top.

They also highlight the “quality-mix problem, which refers to the fact that the composition of houses sold will differ from period to period, making it difficult to discern whether observed price changes reflect genuine movements in underlying house prices or simply changes in the composition of houses sold. For example, prices may increase from one month to the next simply because of an increase in the average size of

houses sold. Larger homes tend to sell for higher prices, so it’s not clear whether the observed increases in prices represent genuine market movements or simply changes in sales composition. This quality-mix problem is of particular concern in the property market since

housing quality varies significantly along multiple dimensions.

This paper outlines the production of three monthly house price indices (HPIs) for New Zealand produced using data from the Real Estate Institute of New Zealand (REINZ) using three alternative methodologies. REINZ approached the Reserve Bank of New Zealand at the end of 2015 for technical guidance on possible improvements to their house price index methodology, in light of significant improvements to their dataset in recent years. The paper documents the guidance, providing an overview of the alternative methodologies and an empirical evaluation of the resulting indices.

The database provided by REINZ is a rich unit-record sales dataset with information on price, location, valuation, and property characteristics (such as the number of bedrooms and the floor area). We use the database to produce HPIs based on three well-established and widely adopted methodologies: 1) sales-price to appraisal ratio (SPAR); 2) hedonic regression; and 3) repeat sales. All three methods are found to produce credible-looking indices, which match the turning points and well-established cyclical properties of New Zealand’s existing house price statistics.

As a benchmarking exercise, the three candidate indices are evaluated alongside a simple median and a stratified median index (similar to the methodology currently used by REINZ). Applying a range of criteria to assess index performance, we find that all three alternative candidate methodologies out-perform the simple median and the stratified median methodologies.

The SPAR method is found to perform the best, due to lower month-to-month noise (especially for more disaggregated regional indices), greater stability as more data are added, robustness to sample changes, and higher accuracy in predicting sales prices.