The New Zealand Government, retail banks and the Reserve Bank are today announcing a major financial support package for home owners and businesses affected by the economic impacts of COVID-19.

The package will include a six month principal and interest

payment holiday for mortgage holders and SME customers whose incomes have been

affected by the economic disruption from COVID-19.

The Government and the banks will implement a $6.25 billion

Business Finance Guarantee Scheme for small and medium-sized businesses, to

protect jobs and support the economy through this unprecedented time.

“We are acting quickly to get these schemes in place to

cushion the impact on New Zealanders and businesses from this global pandemic,”

Finance Minister Grant Robertson said.

“These actions between the Government, banks and the Reserve

Bank show how we are all uniting against COVID-19. We will get through this if

we all continue to work together.

“A six-month mortgage holiday for people whose incomes have

been affected by COVID-19 will mean people won’t lose their homes as a result

of the economic disruption caused by this virus,” Grant Robertson said.

The specific details of this initiative are being finalised

and agreed urgently and banks will make these public in the coming days.

The Reserve Bank has agreed to help banks put this in place

with appropriate capital rules. In addition, it has decided to reduce banks

‘core funding ratios’ from 75 percent to 50 percent, further helping banks to

make credit available.

We are announcing this now to give people and businesses the

certainty that we are doing what we can to cushion the blow of COVID-19.

The Business Finance Guarantee Scheme will provide

short-term credit to cushion the financial distress on solvent small and

medium-sized firms affected by the COVID-19 crisis.

This scheme leverages the Crown’s financial strength,

allowing banks to lend to ease the financial stress on solvent firms affected

by the COVID-19 pandemic.

The scheme will include a limit of $500,000 per loan and

will apply to firms with a turnover of between $250,000 and $80 million per

annum. The loans will be for a maximum of three years and expected to be

provided by the banks at competitive, transparent rates.

The Government will carry 80% of the credit risk, with the

other 20% to be carried by the banks.

Reserve Bank Governor Adrian Orr, said: “Banks remain well

capitalised and liquid. They also remain highly connected to New Zealand’s

business sector and almost every household in New Zealand. Their ability to

extend credit to firms to bridge the difficult times created by COVID-19 is

critical and made more possible with today’s announcements. We will monitor

banks’ behaviour over coming months to assess the effectiveness of the

risk-sharing scheme.”

The Government, Reserve Bank and the Treasury continue to

work on further tailor-made support for larger, more complex businesses, Grant

Robertson said.

A further announcement from the Reserve Bank NZ today. They have established a Term Auction Facility to support the markets/banks, FX swap funding, and a $30bn US Swap line from the Fed. They also removed the credit tiers for ESAS account holders. All signs of Central Bank support for the financial plumbing.

New Zealand’s financial system remains sound, with strong capital and liquidity buffers.

Assistant Governor Christian Hawkesby said

the Reserve Bank is actively involved in financial markets to ensure

smooth market functioning despite the global uncertainty from COVID-19.

Regular market operations continue to ensure there is ample liquidity in

the financial system.

“The measures we are implementing today

provide additional support to domestic financial markets. We will ensure

our operations make financial markets operate smoothly,” Mr Hawkesby

said.

“We are working in tandem with the banks, the wider financial market community, and the Government.”

The provision of term funding

The Term Auction Facility (TAF) is a

program that will alleviate pressures in funding markets. The TAF gives

banks the ability to access term funding, with collateralised loans

available out to a term of 12 months.

Banks currently have robust liquidity and

funding positions and can manage short-term disruptions to offshore

funding markets. The opening of the TAF will provide confidence that the

Reserve Bank stands ready to support the market if needed. Further

operation details on the TAF are available in a Domestic Markets media release.

Providing funding in FX swap markets

The Reserve Bank is providing liquidity in the FX swap market, to ensure

this form of funding can be accessed at rates near the Official Cash

Rate (OCR). This activity will increase in the weeks ahead to support

funding markets.

Re-establishment of a USD swap line

The Reserve Bank has re-established a temporary USD swap line

with the US Federal Reserve. This will support the provision of USD

liquidity to the New Zealand market, in an amount up to USD 30 billion.

This is a facility that is being offered to many other central banks

globally.

Supporting liquidity in the New Zealand government bond market

The Reserve Bank has been providing liquidity to the New Zealand government bond market to support market functioning.

Ensuring a robust monetary policy implementation framework

To support the implementation of monetary

policy, the Reserve Bank is removing the allocated credit tiers for

Exchange Settlement Account System (ESAS) account holders. This change

means that all ESAS credit balances will now be remunerated at the OCR.

Under the previous framework, banks were charged a penalty rate on

deposits of cash balances above their allocated credit tiers.

The removal of credit tiers for ESAS

account holders will provide additional flexibility for the Reserve Bank

in its market operations, by keeping short-term interest rates anchored

near the OCR regardless of the level of settlement cash in the system.

This framework for monetary policy implementation (i.e. a floor system)

is common among other central banks overseas.

The Reserve Bank will continue to monitor

the use of our liquidity facilities and ESAS settlement accounts. We

anticipate that liquidity will continue to be distributed efficiently

throughout the banking system. If not, we will review our framework for

monetary policy implementation as needed.

A commitment to market functioning

The Reserve Bank has a number of tools to

provide additional liquidity and the ability to increase the size of

operations where needed. We are committed to using these to support

smooth market functioning.

In addition to the tools listed above, the Bank has an established role to provide liquidity in the New Zealand dollar foreign exchange market in periods of illiquidity or dysfunction, and is operationally ready to undertake this role if required.

Mr Hawkesby reiterated that the Reserve

Bank continues to monitor developments, and remains ready to act further

to ensure markets and the financial system operate in a stable and

efficient manner.

The Reserve Bank of New Zealand, Te Pūtea Matua, is taking

proactive steps to ensure it is well positioned to effectively and efficiently

manage New Zealand’s monetary policy in an environment of very low interest

rates.

In a speech launching its Principles on Using Unconventional Monetary Policy,

Reserve Bank Governor Adrian Orr said as kaitiaki (caretakers) of Te Pūtea

Matua, the Bank’s activities involve continuous assessment of our monetary

policy framework, including the most effective tools and their best

application.

Mr Orr said the Reserve Bank

has not, and still does not, need to use alternative monetary policy

instruments to the OCR, but it is best to be prepared.

“An inability to predict

what might happen next is no excuse for not preparing for what could happen.

That’s true for businesses, governments and central banks. It is in light of

both economic theory and recent global experience that we have been assessing

what alternative monetary policy tools may be available to the Reserve Bank of

New Zealand – and their relative desirability. We are fortunate, unlike many

other OECD economies, to have the time to prepare for such possible needs.”

The Reserve Bank typically implements monetary policy by controlling the Official Cash Rate but as interest rates fall, this tool could be pushed to its limit in the future. Given this, in recent years, the Reserve Bank has been considering the unconventional monetary policy tools and policy framework that it would use to meet its policy targets.

The work to develop the

Reserve Bank’s preparation for unconventional monetary policies has involved:

Identifying the suite of possible ‘unconventional monetary policy tools’ available to the Reserve Bank;

Defining and making explicit the criteria the Reserve Bank would use to assess these tools, against both each other and also alternative policies all together (e.g., fiscal policy options);

Considering the relative benefits and costs of the tools, so as to operate on a ‘least surprise’ basis, and to ensure the Reserve Bank works in collaboration and with the agreement of fiscal authorities;

Considering not just the monetary policy efficacy of the tools, but also broader considerations related to our financial stability and efficiency mandate; and

Ensuring the tools are actually able to be utilised, including working with the important financial institutions that make up our system.

“We are confident of our

success in assessment and implementation, but we are also aware that these

tools work best when supported by wider stabilisation policies and additional

macroprudential considerations. In the event we ever had to use these

unconventional tools, our goal would be to ensure a strong and sustained

increase in economic activity, with inflation expectations remaining

well-anchored on our target mid-point.”

In the coming weeks the

Reserve Bank will release a series of technical papers explaining the tools in

more detail, examining their pros and cons, and outlining how they would

potentially be used.

Note:

The principles and speech do

not discuss current economic conditions or the Reserve Bank’s outlook for the

Official Cash Rate (OCR). The Reserve Bank’s next OCR decision is scheduled for March 25.

The Bank remains prepared in

its business continuity role to ensure a well-functioning financial system,

including ongoing consumer and business access to credit and cash, liquidity to

the banking system and a stable payments and settlements system.

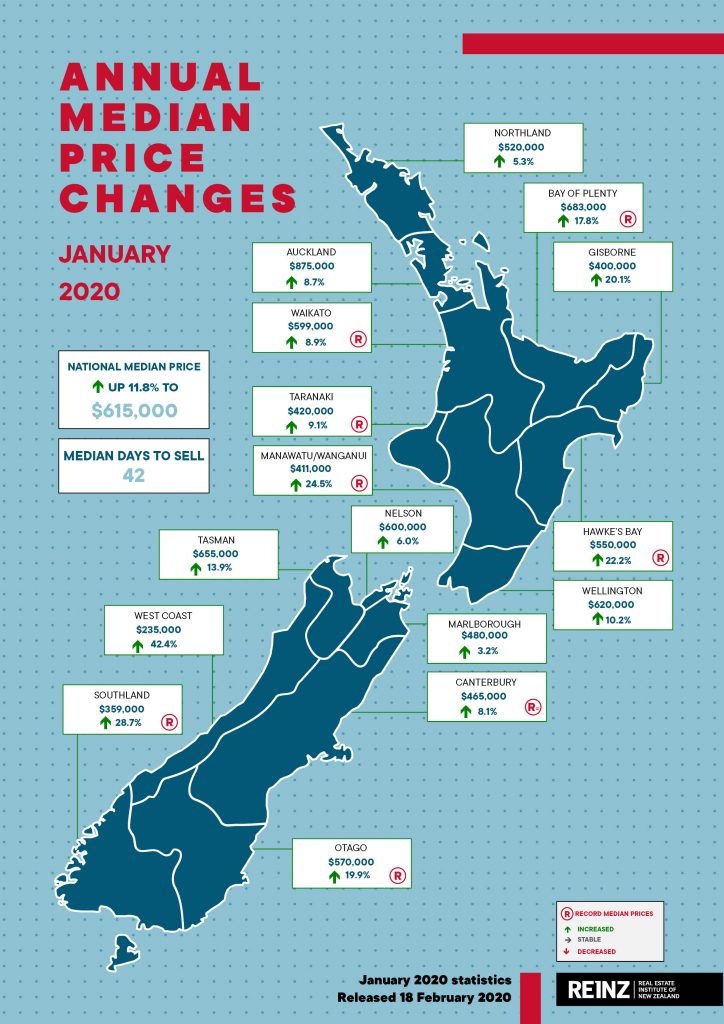

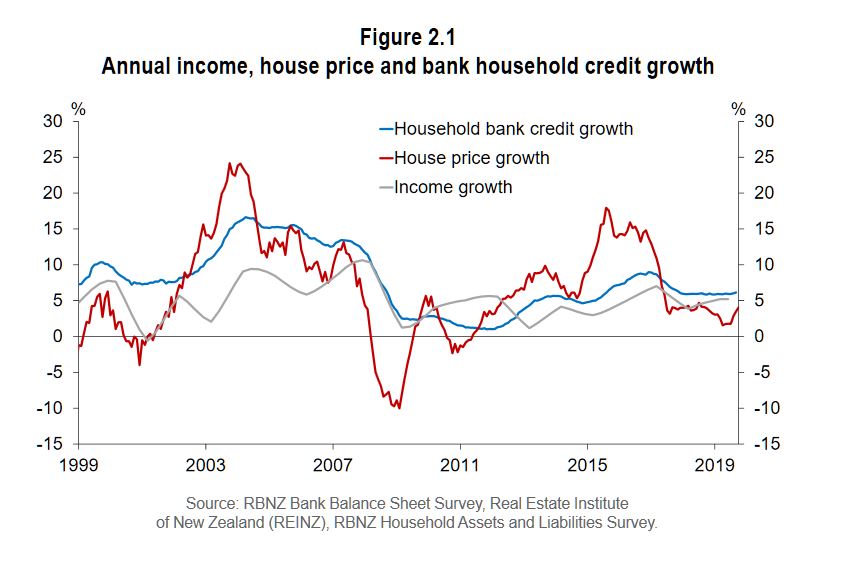

REINZ has released their January 2020 residential report today, and they reported the busiest January in 4 years. The annual average rise across New Zealand was 7%, with Auckland at 4.4% and other areas up 9.1%. Auckland is actually now among the faster-rising regions. Prices in Canterbury are rising, although to date this has been slower than many other regions.

In January the median number of days to sell a property nationally decreased by 6 days from 48 to 42 when compared to January 2019 – the lowest days to sell for the month of January in 3 years.

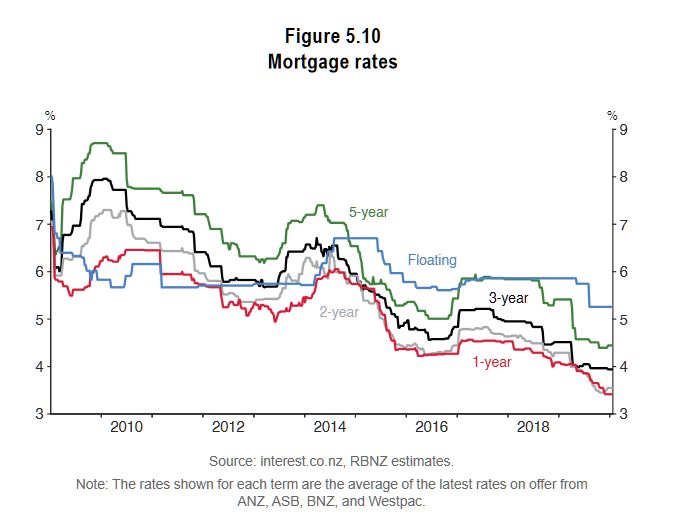

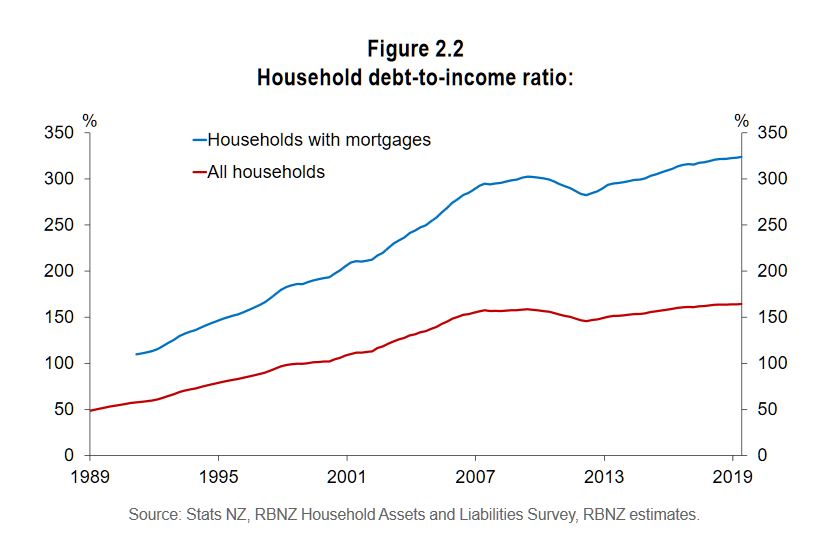

Low interest rates and lighter regulation are driving the market. Over 2019, the RBNZ cut the OCR from 1.75 percent to 1 percent and they indicate that the OCR will remain at 1 percent for some time. In response, household debt continues to rise. Lower debt servicing costs enables higher household spending on consumption, although returns from savings will be lower as well.

Over the past year New Zealand construction activity has ramped up substantially while net migration has steadily declined. The cancellation of earlier plans to introduce a capital gains tax has also helped to drive the market.

For New Zealand excluding Auckland, the number of properties sold increased by 0.9% when compared to the same time last year (from 3,279 to 3,308) – also the highest for the month of January in 4 years.

In Auckland, the number of properties sold in January increased by 9.7% year-on-year (from 1,180 to 1,295) – the highest number of residential properties sold in the month of January since January 2016.

Sales in Auckland were the highest for the month of January in four years, with particularly strong uplifts in sales volumes in North Shore City (+29.0%), Waitakere City (+28.6%) and Rodney District (+21.1%).

Regions outside Auckland with the highest percentage increase in annual sales volumes during January were: • Nelson: +42.6% (from 54 to 77 – 23 more houses) • Manawatu/Wanganui: +15.3% (from 281 to 324 – 43 more houses) – the highest for the month of January in 3 years • Bay of Plenty: +11.5% (from 340 to 379 – 39 more houses) – the highest for the month of January in 4 years • Marlborough: +11.3% (from 62 to 69 – 7 more houses). Regions with the largest decrease in annual sales volumes during January were: • Tasman: -29.3% (from 58 to 41 – 17 fewer houses) – the lowest since January 2017 • Southland: -27.2% (from 151 to 110 – 41 fewer houses) – the lowest for the month of January in 6 years • Otago: -17.1% (from 269 to 223 – 46 fewer houses) – the lowest for the month of January in 9 years.

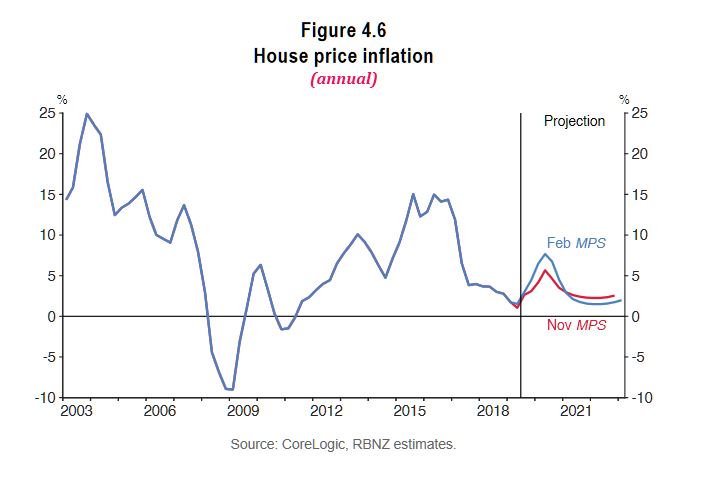

In the recent Reserve Bank NZ Monetary Policy Statement, they indicated that over the medium term, annual house price inflation is expected to slow as net immigration moderates, residential construction activity remains high, and the effects of past lower mortgage rates fade.

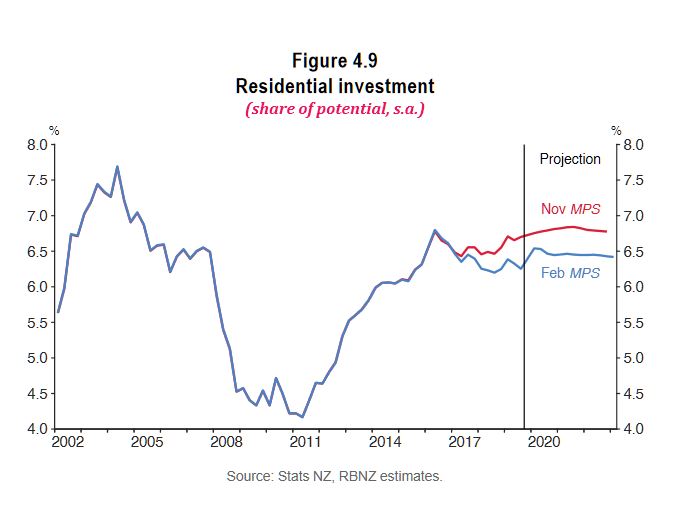

However, they expect residential investment growth is expected to pick up over the next six months, in line with recent high levels of residential building consent issuance. That said, residential investment is forecast to decline very gradually as a share of GDP later in the projection period, reflecting ongoing capacity constraints in the construction sector.

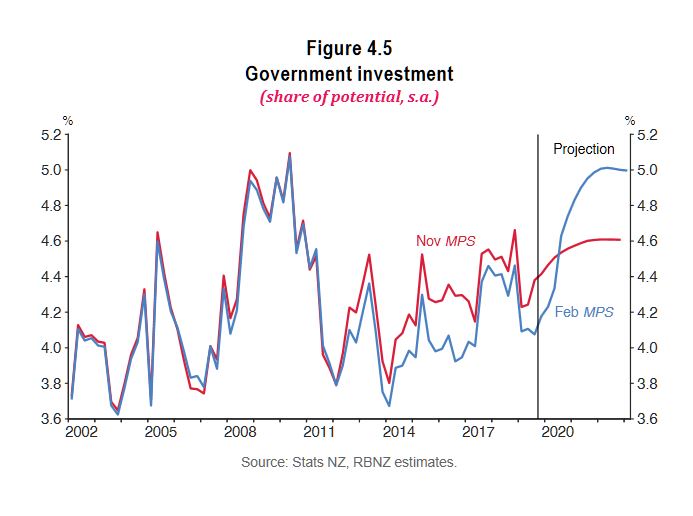

In December 2019, the Government announced a substantial investment package of $12bn, equivalent to around 4 percent of annual nominal GDP. The Treasury forecasts that $8.1bn will be spent between June 2020 and June 2024, mainly on infrastructure projects

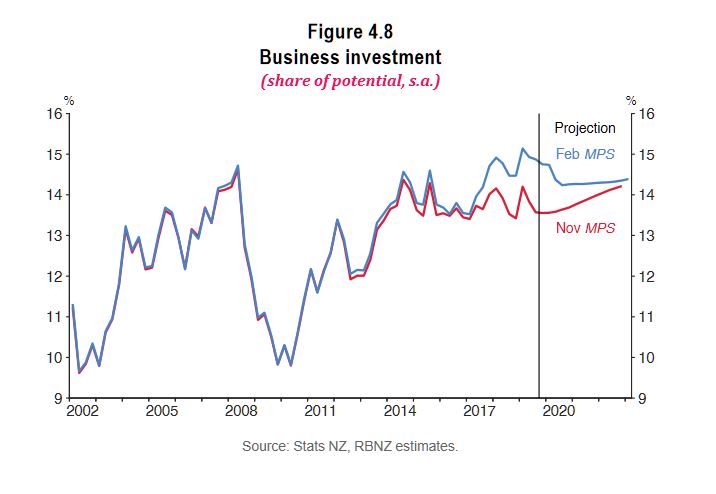

Which is probably just as well, given that business investment is forecast to fall ahead.

Financial system vulnerabilities remain elevated and more effort is required to ensure that the system remains resilient over the longer-term, Reserve Bank Governor Adrian Orr says in releasing the November Financial Stability Report.

International risks to the

financial system have increased. Global growth has slowed amid continued

uncertainty about the outlook for world trade. This has resulted in reductions

in long-term interest rates to historic lows, including in New Zealand. While

necessary to maintain near-term inflation and employment objectives, prolonged

low interest rates can promote excess debt and investment risk-taking, and

overheat asset prices, Mr Orr says.

Mr Orr noted that the Reserve Bank’s Loan-to-Value Ratio (LVR) restrictions have been successful in reducing the more excessive household mortgage lending, thereby improving the resilience of banks to a significant deterioration in economic conditions.

But, there remains the risk that prolonged low interest rates could lead to a resurgence in higher-risk lending. As such, we have decided to leave the LVR restrictions at current levels at this point in time.

Mr Orr says the Reserve Bank

is committed to bolstering the long-term resilience of the financial system.

“Strong bank capital buffers are key to enabling banks to absorb losses and

continue operating when faced with unexpected developments. The Reserve Bank

has proposed increasing these buffers further with final decisions on the

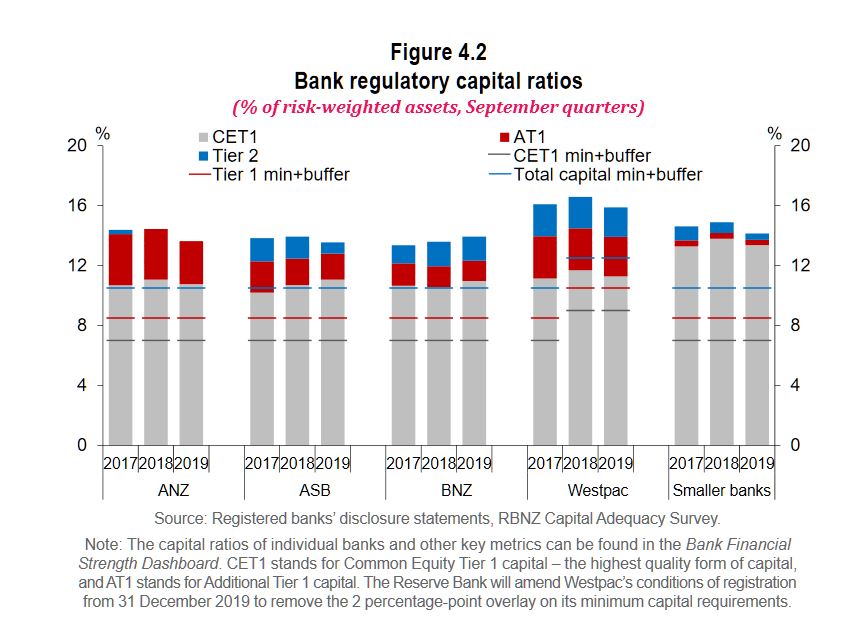

Capital Review proposals to be announced on 5 December.”

Deputy Governor Geoff

Bascand says good governance and robust risk management processes within

financial institutions are important to maintain long term resilience. Our

recent reviews of banks and life insurers, and the number of recent breaches in

key regulatory requirements, reinforces the need for financial institutions to

improve their behaviour.

“We are engaging with

industry to ensure that they strengthen their own assurance processes and

controls. We have also reviewed our own supervisory strategy and will be taking

a more intensive approach, which will involve greater scrutiny of institutions’

compliance,” Mr Bascand says.

“Some life insurers have low

solvency buffers over minimum requirements. Recent falls in long-term interest

rates are putting further pressure on solvency ratios for some of these

insurers. Affected insurers are preparing plans to increase solvency ratios and

are subject to enhanced supervisory engagement. This highlights the need for

insurers to maintain strong buffers, and insurer solvency requirements will be

reviewed alongside an upcoming review of the Insurance (Prudential Supervision)

Act.”

Westpac New Zealand Limited (Westpac) has retained its

accreditation as an internal models bank following completion of an extensive

remediation process required by the Reserve Bank.

In 2017 the Reserve Bank

required Westpac to undertake an independent review of its compliance with

internal models obligations. The review found that Westpac was using a number

of unapproved models and that it had materially failed to meet requirements around

model governance, processes, and documentation.

The Reserve Bank imposed a

precautionary capital overlay in light of the regulatory breaches, and gave

Westpac 18 months to remedy the failures or risk losing its accreditation as an

internal models bank.

Deputy Governor Geoff

Bascand says that following the remediation process, Westpac is now operating

with peer-leading processes, capabilities and risk models in a number of areas.

“Westpac has taken the

findings of the independent review as an opportunity to make meaningful

improvements to its risk management, and we commend it for its co-operative and

constructive engagement in working with Reserve Bank over the remediation

period.

“The changes that Westpac

has made to its internal processes, governance and resourcing, as well as a

suite of new credit risk models for which it has sought approval, have given us

confidence in its capital modelling and compliance and satisfied us that it now

meets the internal models bank standard.

“Looking forward, we will continue

to hold all internal model banks to the same high standards.”

Internal models banks are

accredited by the Reserve Bank to use approved models to calculate their

regulatory capital requirements. Accreditation is earned through maintaining

high risk management standards, and comes with stringent responsibilities for

the bank’s directors and management.

Banks are required to

maintain a minimum amount of capital, which is determined relative to the risk

of each bank’s business. The way that risk is measured is important for

ensuring that each bank has an appropriate level of capital to absorb large and

unexpected losses.

The Reserve Bank will amend

Westpac’s conditions of registration from 31 December to remove the two

percentage point overlay applying to its minimum capital requirements.

As a condition of retaining

its accreditation Westpac will need to satisfy several ongoing requirements,

which it has committed to resolving, Mr Bascand says.

The Reserve Bank of New Zealand (RBNZ) and Financial Markets

Authority (FMA) today released their findings on life insurers’ responses to

the joint Conduct and Culture Review.

Overall, the regulators were

disappointed by the responses. Significant work is still needed to address the

issues of weak governance and ineffective management of conduct risk,

identified in the regulators’ report earlier this year.

Rob Everett, FMA Chief

Executive, said: “While we’re disappointed, we’re not surprised as the

responses confirm what we found in our original review. It’s clear that

progress has been slow and not as far-reaching as required.

Some providers have started

work to identify the customer and conduct issues they face, others have not

provided any detail on this.”

Sixteen life insurers were

asked to provide work plans outlining the steps they will take to improve their

existing processes and address the regulators’ findings and recommendations.

There was wide variance in

the comprehensiveness and maturity of the plans provided.

Adrian Orr, Reserve Bank

Governor, said, “We’re disappointed the industry’s response has been

underwhelming. The sector has failed to demonstrate the necessary urgency and

prioritisation, around investment in systems, to provide effective governance

and monitoring of conduct risk.”

There was also a wide

variance in the quality and depth of the systematic review of policyholders and

products. Some did not complete this exercise and others did not provide data

on the number of policyholders affected or the estimated cost of remediation

activities. Insurers that completed the exercise identified at least 75,000

customer issues requiring remediation, with a value of at least $1.4 million.

Some of the new issues identified included:

Overcharging of premiums and benefits not being updated due to system errors, human errors and under-reporting of deaths

Poor customer conversations overlooking eligibility criteria and poor post-sale communications, which lead to declined claims and underpayment of benefits

Poor value products were identified, where premiums charged were not fair value for the cover provided.

Sales incentives and

commissions

The FMA and RBNZ committed

to report back on staff incentives and commissions for intermediaries. Previous

reports by the FMA reflected the concerns with conflicted conduct associated

with high up-front commissions and other forms of incentives, (like overseas

trips) paid to advisers.

Although some insurers have

committed to removing sales incentives for employees and their managers, not

all committed to removing or altering indirect sales incentives.

Those providers that have

removed sales incentives for employees don’t typically use external advisers to

distribute products. Providers using external advisers told the regulators that

changing long-held business arrangements and distribution models is difficult

and will take time to implement.

Mr Everett said, “We’re

ready to work with life insurers to ensure they prioritise their focus on

serving the needs of their customers, while at the same time balancing the need

to remunerate advisers for the important work they do to help these customers.

But we do not think high up-front commissions create confidence that insurers

and advisers are acting in the best interests of customers.”

Mr Orr said, “Good

governance within insurance firms requires the effective management of conflicts

of interest. We need to see much better systems and controls in place to manage

the inherent conflicts where advisers or sales staff are offered incentives to

sell or replace insurance policies.”

Next steps

Those companies that have

not undertaken comprehensive systematic reviews of policyholders and products

have been asked to complete further reviews of their systems to identify

issues, and to develop mature plans to respond and remediate any of their

findings. These plans must be completed by December 2019.

The FMA and RBNZ will

continue to monitor how the insurers are responding to recommendations and

implementing their work plans. Life insurers are currently not legally required

to become more customer-focused and the FMA and RBNZ found that the sector has

a weak appetite for change.

Deficiencies in some of the

plans received, and some insurers’ lack of commitment to implementing the

regulators’ recommendations, further demonstrates the need for additional

obligations to be included in the regulation of conduct of life insurers.

There is an interesting paper the Reserve Bank NZ has put out, seeking comments by 31 August. The Future of Cash Use. It was issued in June 2019.

The paper describes the transition to digital alternatives, and explains some of the reasons. But what caught my eye was this section. “All members of society will lose the freedom and autonomy that cash provides, be more exposed to cyber threats, and lose the ability to use cash as a back-up form of payment”. And “other activity in the shadow economy is unlikely to be affected by the disappearance of cash as people find other ways to circumvent the law”.

So two points, New Zealand followers you might want to read the paper, and make a submission – not been much publicity so far.

Those following the DFA campaign relating to the War on Cash in Australia, here is more evidence that the proposal to ban cash transactions above $10,000 will not achieve their stated aims – but of course there is a wider monetary policy objective, as we have discussed.

6 Considerations arising from having less cash in society

Given the trends in cash demand and the cost pressures on the

commercial supply of cash in New Zealand, it is possible that cash will

become less widely available or used in the medium to long term. The

effects of less cash in society would be felt more keenly by certain

groups of people who rely on cash and for whom no practicable substitute

exists. The severity of these impacts would be worsened if the

transition to a society with less cash acceptance occured before

mitigating measures could be put in place. Further, the size of the

affected groups might not be large enough to motivate cash providers to

ensure future cash availability, but the size might also not be

negligible.

This section summarises the information in table 1 and Appendix A and

the issues that should be considered if cash use and availability

decline.

Issue 1: People who are financially or digitally excluded could be severely negatively affected.

Cash provides access to the financial system for those who face

barriers to financial inclusion. Further, in a society with less cash,

barriers to digital inclusion could become barriers to financial

inclusion.

Barriers to financial inclusion include limited access to the

banking system due to either a lack of trust in online security, skill

or motivation to use online financial platforms, or banking

restrictions. People who are not banked or have limitations to accessing

the banking system tend to be people without identification and proof

of address, people with convictions, people with poor credit histories,

people with disabilities, illegal immigrants and children.Elderly people

typically rely more than others on cash as a form of payment.

This could be due to low trust in online payments, low ability or

low motivation to learn new payment techniques. People with physical

disabilities, such as sight or intellectual impairments, might also find

cash a useful form of money. Children are also subject to financial

exclusion as banks do not issue debit cards to children under the age of

13. Further, New Zealand banks have full discretion in the customers

they service. This means that some people who do not meet certain bank

policies cannot obtain or keep accounts with those banks. Appendix A

describes additional groups that rely on cash rather than digital money.

Barriers to digital inclusion include insufficient internet

coverage, affordability constraints for technology hardware or data

plans, lack of skills, lack of confidence and low motivation to use

digital platforms. For example, even if people have access to the

internet they might not be motivated to upload personal details to an

online bank account due to privacy concerns.

Issue 2: Tourists, people in some Pacific islands and people who use

cash for cultural customs might be negatively affected if they cannot

use substitutes.

Tourists

Currently most tourists use cash as a reliable and easy-to-use form

of payment. Reserve Bank research has revealed that cash is typically

issued to Auckland and overseas and sent back to the Reserve Bank from

the South Island. This movement is likely due to the movement of

tourists. Many retailers in New Zealand do not accept credit cards (or

contactless payments) due to their higher interchange fees, preferring

instead to accept debit and EFTPOS cards (which require a New Zealand

bank account) that incur much lower costs for the retailers.We

are not aware of the extent to which inbound tourists’ own financial

services’ fees or portability, or their prior understanding of

transacting in New Zealand, influence this behaviour.

As per Appendix A, tourist access to payments in New Zealand could be

met by overseas-issued debit cards if cash were not available. Further,

competition might cause some retailers to accept tourist credit cards

despite higher interchange fees if cash was not available. Bounie et al

(2015) show that higher competitive pressures (the threat of losing

sales) increase the probability that a retailer will accept credit card

payments despite the higher costs.

Even if electronic payment alternatives were reliable, tourists might

be disadvantaged due to language and cultural barriers that create

actual and perceived barriers to payments in New Zealand. Further,

tourists might be particularly vulnerable to risks of robbery or loss

of payment cards if they could not rely on cash as a back-up payment.

Pacific Islands

Niue, the Cook Islands and Tokelau rely on New Zealand banknotes and

coins for their physical currency. The size of these island economies

has been thought to be a contributing factor to their use of New Zealand

currency. In addition, these islands are formally defined as states in

free association within the Realm of New Zealand. New Zealand banknotes

are also used in the Pitcairn Islands.

The Reserve Bank does not have a formal arrangement to supply these

economies with banknotes and coins. The supply of banknotes and coins to

these islands is facilitated by commercial providers, tourists, and

transfers from families. There are no ATMs on Niue and Tokelau. The Cook

Islands has two ATM providers and also issues its own banknotes and

coins. These islands also have access to digital money as in New

Zealand.

Cultural customs

New Zealand’s banknotes have been referred to as the country’s

business card. The designs on the notes represent many of our cultural

icons and contribute to our national cultural identity. Cash is also

used in many cultural customs in New Zealand. Some cultures that use

cash as gifts in traditional ceremonies might find that part of their

cultural identity is lost if they can no longer access cash easily. For

instance:

A Chinese custom is to give cash to junior family members and

friends during celebrations including New Year (Hoong Bouw — giving

money in red envelopes), at funerals, and during tea ceremonies in

traditional Chinese culture.

Some cultures have a wedding money dance where cash is gifted to

the bride and groom as they dance (the Philippines’ Saya ng Pera, and

the Taualuga in Samoa, Tonga and Western Polynesia).

Western cultures give coins to children who lose their baby teeth (Tooth Fairy).

Issue 3: All members of society will lose the freedom and autonomy

that cash provides, be more exposed to cyber threats, and lose the

ability to use cash as a back-up form of payment.

If cash use and availibility were to decline, an issue for all

members of society could be the loss of freedom that cash provides in

terms of autonomous spending and wealth stores, privacy, ability to live

off the grid, and ability to avoid the banking system. This could

result in a significant loss of social freedom in aggregate and

increased cyber security risks (leading to an increase in national

security risks). Lastly, society would lose the benefit of cash as a

‘back-up’ form of payment, although the usefulness of cash in this role

is limited.

Reduced freedom

Cash is anonymous, so provides consumers with autonomy or discretion

in how they choose to spend their money or store their wealth. The

feature of full anonymity creates personal and societal freedom and has

not been replicated in digital currencies. There are three elements in

this freedom; the first relates to the desire for privacy in making

transactions, the second relates to the desire to avoid banks or

government regulation, and the third relates to exposure to cyber-crime.

First, cash payments and balances cannot easily be traced. Central

agents and third parties (such as banks and governments) cannot easily

intervene or stop cash payments outside the banking system. This is a

unique feature of cash and is not fully replicated by any other form of

money. This anonymity gives people full control of and discretion with

their finances. Independent bank accounts could provide personal

freedoms but they are not always available or sufficient. For example,

individuals who are in abusive and controlling circumstances might

benefit from cash as it is easier to obtain and hide when other personal

freedoms are restricted.35

Additionally, people might feel that they benefit from the choice of

using an anonymous form of payment if it were ever needed.

However, the difficulty in tracing cash makes it relatively more

vulnerable to theft, accidental losses and fraudulent payments

(inadvertently accepting counterfeit notes). For this reason, some argue

that people would be better off with a partially anonymous form of

payment, where only the minimum information is given regarding the

identity of the payer and payee in each transaction, but each

transaction is recorded. These payments include, for example, vouchers,

and prepaid gift (debit or scheme) cards.36

Second, the offline and anonymous features of cash enable people to

separate their transactions and stores of wealth from the banking system

and some government interventions. There are legitimate motivations for

this separation.

There is currently no guarantee of the safety of bank deposits in New Zealand.37

Banks take household and business deposits and lend them to borrowers

— there is a risk that borrowers might not be able to service their

debts. Households and businesses could lose their deposits if banks were

engaging in overly-risky lending or if a severe series of events

occurred and many loans were not repaid.

People might also want to remove their savings from the banking

system if the Reserve Bank charged negative interest rates to stimulate

the economy. Cash provides an avenue for people to avoid this form of

government intervention or any other government intervention that might

occur in the future, such as capital controls.

Relatedly, people might want to store wealth outside the banking

system if they have low fundamental trust in banks or the government.

Examples are individuals who have immigrated to New Zealand from

countries where trust in the financial system is low, or where

government appropriations of assets were not uncommon. If there were

less cash in society, individuals would lose their privacy and autonomy

from government in the sense that all their transactions and savings

would be fully traceable if permitted by law.

Third, storing and transacting in cash reduces exposure to

cybercrime, such as financial losses and identity fraud. On a societal

level, New Zealand might be more exposed to cybercrime such as

state-funded cyber threats if it were totally reliant on the banking

system and digital money for all transactions and savings. On a personal

level, some people might prefer to keep their identities and finances

offline due to cyber concerns.

The loss of freedom in society in the above three areas could result

in demand for a form of digital currency issued by the central bank that

replicates some of the autonomy of cash. There are other assets in

which people could store their wealth that are offline and removed from

the financial system, for example, commodity assets and property.

However, these are more difficult to transform into spendable money and

can come with a different set of risks including fluctuating values.

Therefore, people might demand a central bank digital currency that

provides lower traceability than current electronic payments and

accounts and presents an alternative to the banking system. This could

be in the form of accounts with the central bank or tokens issued by the

central bank, which carry a very low risk of default and sit outside

the commercial banking system. A central bank digital currency could

also be designed to provide a low cost form of payment to put downward

pressure on uncompetitive prices in the payment system. Alternatively,

consumers might ask for deposit protection and greater regulation of the

banking system.38

People might also value the freedom and autonomy of cash for

illegitimate reasons. As noted in section 2, cash is used in the shadow

economy to facilitate illegal transactions or as a means to hide income

and reduce tax and other obligations. The International Monetary Fund

estimated New Zealand’s shadow economy at 11.7 percent of GDP in 1991

-2015. 39

It is difficult to assert what might occur in the shadow economy if we

had less cash. At the margin, some shadow economy activities could be

reduced as people consider the additional difficulty of engaging in them

without anonymous payments. For example, some people might be

dissuaded from buying illegal goods and services if they could not avoid

leaving electronic records of their purchases. However, it is also

possible that criminal activity would innovate to other mechanisms or

forms of payment discussed below.

There is debate on whether the anonymity of cash enables crime or

whether illegal transactions would continue without cash. Rogoff (2016)

and McAndrews (2017) agree that, without cash, criminals could use

commodity money (i.e. gold), foreign currency, and inflated invoices.

But they disagree on the extent to which these substitutes would be

used. Rogoff (2016) argues that there is no complete substitute for

cash, so criminal activity would be hindered if there were less cash in

society. McAndrews (2017) argues that inflated invoices would become the

most likely medium of exchange for criminals. He suggests that a

society without cash would likely move towards deeper institutional

corruption of businesses as criminals launder money obtained from

illegal transactions. He also warns that innocent businesses could find

themselves forced into money laundering as criminals look for businesses

to issue inflated invoices.

Issue 4 considers how some tax evasion might be reduced by less cash.

Loss of emergency back up

Cash can be a back-up payment mechanism when electronic payment

systems are not in operation or otherwise unavailable. The Reserve Bank

survey on cash use indicated that 37 percent of people held cash just in

case it was needed (i.e. not for immediate transactions). Cash is

particularly useful in case of ‘personal emergencies’, or localised or

short disruptions in electronic payments systems, and after large-scale

events conditional on the availability of retail stores able to accept

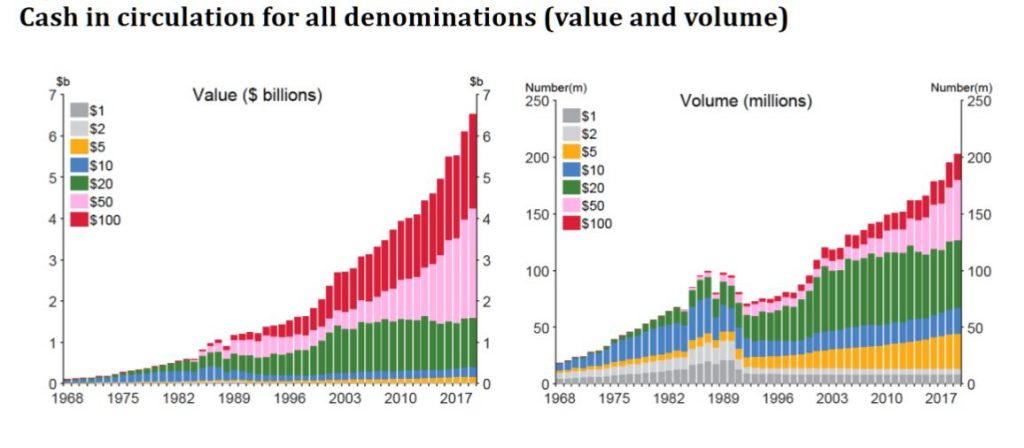

it. Figure 2 shows a spike in CIC as a percent of GDP in 1999 that could

be attributed to the ‘Y2K’ uncertainty.

Cash has several limitations in its usefulness as a back-up payment

in case of large-scale events or natural disasters. Because the supply

of cash and most retail operations are reliant on electricity and

communications, IOUs between small groups or people who are known to

each other might be more effective in periods of long electricity

outages such as those that occur in natural disasters. There might also

not be sufficient cash infrastructure capacity to meet a national

transition to cash in an emergency.

In addition, the National Risk Unit does not recommend including cash

in a civil defence kit or give guidance on the best means of payment in

a national disaster response period. This could be because people

already have their essentials in their civil defence kits, retail stores

might not be operating, and emergency responders will provide

additional supplies. In the weeks following the Christchurch February

2011 earthquake, public demand for cash did not increase substantially.

Commercial banks anticipated an increase in demand for cash and

increased their stores of cash and set up temporary ATMs based on

generators. However, the bulk of these cash stores returned to the

Reserve Bank relatively quickly. Figure 2 shows CIC did not peak as a

share of the population during 2011.

Issue 4: On balance, there would be limited effects on budgeting, financial stability and government revenue.

Transitioning to a society with less cash does not significantly or

negatively affect household budgeting, financial stability and

government revenue.

Budgeting

Cash is widely cited as a budgeting tool. Psychological studies show

that paying in cash incites a higher psychological pain of parting with

funds. This is because the tangible nature of cash results in high

transparency of payments and so generates a greater awareness of

spending.40

This greater ‘pain of paying’ encourages less spending and is useful

for managing discretionary spending, but it could reduce willingness to

pay bills or debt. Shah et al. (2016) suggest that consumers should

automate their essential payments and savings using online banking then

spend disposable (leftover) income using cash. Cash might also be useful

for limiting spending when people need to keep money separate for other

purposes.

People who prefer to use cash for budgeting might benefit from new

electronic budgeting tools such as budgeting applications on mobile

phones. For example, several banks in Dubai provide real time balance

updates or notifications every time money is spent, replicating the

relatively high ‘pain of paying’ that cash provides.

Cash is not the only nor the most important budgeting tool available

for people with low or no disposable incomes, high debts, overspending

habits, or poor mental health. For these groups, commonly cited

budgeting tools include awareness and education, direct credits,

multiple bank accounts, and removing overdrafts and credit. Cash is used

for people who are in full financial management in a Total Money

Management programme as they are allocated their weekly spending in

cash.41

However, the anonymity of cash makes it difficult for budgeting

advisors to identify areas of overspending. Cash also enables people to

default on automatic payments (for bills or debts) as they can withdraw

their full bank account balances into cash. Further, withdrawing money

into cash puts people at a higher risk of robberies than if they did not

withdraw their money. For example, people who withdraw their income

payments from ATMs at night to avoid automatic payments (processed in

the morning) face a risk of robbery, particularly if these habits are

well known in the community.

Financial stability

A society with less cash does not pose a risk to financial stability.

Cash represents a claim on the government and carries low default risk.

In theory, the ability of depositors to convert their savings into cash

represents a form of market discipline on banks that encourages them to

operate prudently. However, there is little empirical evidence to

support this. Engert et al. (2018) evaluate the bank runs during the

2007 – 2008 Global Financial Crisis and determine that cash withdrawals

are a small and unimportant source of market discipline on banks. Shin

(2009) finds that the Northern Rock bank run was triggered predominantly

by wholesale runs, and the in-branch runs to cash were insignificant.

Market discipline is only one form of discipline safeguarding our

financial system. Another form is regulatory discipline. The Reserve

Bank is mandated to use prudential regulation and supervision to

contribute to a stable financial system. The third form is

self-discipline, whereby financial market institutions self-regulate to

ensure their ongoing prudent operation.

The second aspect of stability is payment stability. Migrating from

two payment systems to one payment system would consolidate operational

risk in the single payment system. Greater emphasis would be required

on ensuring the operational reliability of the single payment system if

people could not easily revert to cash if there were a system outage.

Most electronic payments (except cryptocurrencies) rely on the same

back-end payment systems which, exhibit several single points of

failure.42

Increased tax revenue and reduced seignorage

Government revenue could be affected in two ways if cash use and

availability declined. First, removing the availability of notes and

coins might increase tax revenue as businesses would no longer use cash

to reduce their tax bills. The Inland Revenue Department has reported

that the most common ‘hidden economy’ activity is the underreporting of

taxable income, which includes income from cash jobs and transactions.43

Exactly how much tax revenue is lost due to this type of activity is

unknown. A tax working group paper suggests that unincorporated

self-employed individuals under-report approximately 20 percent of their

gross income. This estimate is based on a study commissioned by Inland

Revenue44

and could represent $850 million per annum in lost tax revenue from

unincorporated (non-trust or non-corporation) taxpayers. There is

considerable uncertainty as to the extent to which this number includes

self-employed people who are evading tax by underreporting cash revenue

versus other types of underreporting. It is also not certain that those

reducing their tax burdens by underreporting cash revenue would increase

their tax payments if cash were used less.45

Second, seignorage revenue might decline if the value of CIC declined

significantly. Seignorage revenue is the profit the Reserve Bank makes

from producing and selling cash and investing the profits, as well as

any profit the Reserve Bank makes from financial market trading. 46

The Reserve Bank estimates that it made around $148 million in

seignorage revenue last financial year by issuing cash and investing the

profits.

Other activity in the shadow economy is unlikely to be affected by

the disappearance of cash as people find other ways to circumvent the

law, as described in Appendix A. People who can no longer launder cash

will likely switch to other methods.

The New Zealand Reserve Bank has today published a summary of submissions on its consultation proposing a new mortgage bond standard aimed at supporting confidence and liquidity in New Zealand’s financial markets.

Submissions on the new

proposed mortgage bond standard are broadly supportive of the introduction of a

high grade residential mortgage backed securities framework for New Zealand –

known as Residential Mortgage Obligations (RMO).

The new standard aims to reduce

contingency risks for the Reserve Bank as a lender of last resort, ensuring

financial intermediaries supply sufficient high quality and liquid assets. The

standard also aims to provide issuers and investors with an additional funding

and investment instrument, supporting the development of deeper markets.

Assistant Governor and

General Manager of Economics, Financial Markets and Banking Christian Hawkesby

said he was pleased with the range and depth of feedback received during the

consultation process.

“The consultation process

has been successful in delivering improvements to the initial concept for a new

mortgage bond standard to support financial intermediation, liquidity

management and funding in New Zealand’s markets.”

The feedback from issuers, investors

and other market participants has been constructive and it will help inform the

Reserve Bank’s final policy decision which is expected to be published by the

end of 2019.

The Reserve Bank has decided

to update repo-eligibility conditions for RMBS in

the transition to the final RMO policy. This includes a new approval process

and requirement for a more detailed RMBS reporting template.

The New Zealand Reserve Banks says the Official Cash Rate (OCR) is reduced to 1.0 percent. The Monetary Policy Committee agreed that a lower OCR is necessary to continue to meet its employment and inflation objectives.

Employment is around its

maximum sustainable level, while inflation remains within our target range but

below the 2 percent mid-point. Recent data recording improved employment and

wage growth is welcome.

GDP growth has slowed over

the past year and growth headwinds are rising. In the absence of additional

monetary stimulus, employment and inflation would likely ease relative to our

targets.

Global economic activity

continues to weaken, easing demand for New Zealand’s goods and services.

Heightened uncertainty and declining international trade have contributed to

lower trading-partner growth. Central banks are easing monetary policy to

support their economies. Global long-term interest rates have declined to

historically low levels, consistent with low expected inflation and growth

rates into the future.

In New Zealand, low interest

rates and increased government spending will support a pick-up in demand over

the coming year. Business investment is expected to rise given low interest

rates and some ongoing capacity constraints. Increased construction activity

also contributes to the pick-up in demand.

Our actions today

demonstrate our ongoing commitment to ensure inflation increases to the

mid-point of the target range, and employment remains around its maximum

sustainable level.