NAB today lifted its back book mortgage rates by up to 16 basis points, which marks the end of its initiative to hold rates lower.

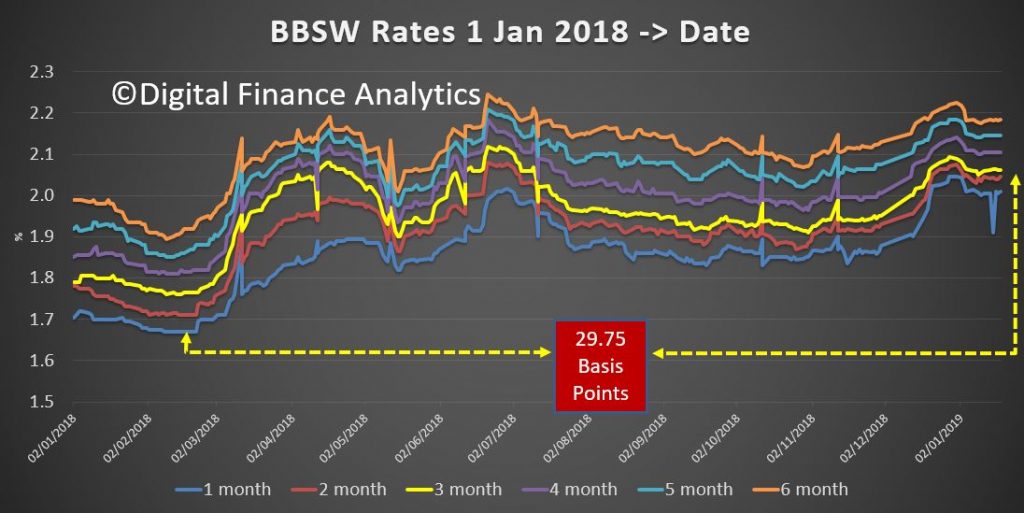

As we have been saying for some time margin pressure is building, as illustrated by the BBSW

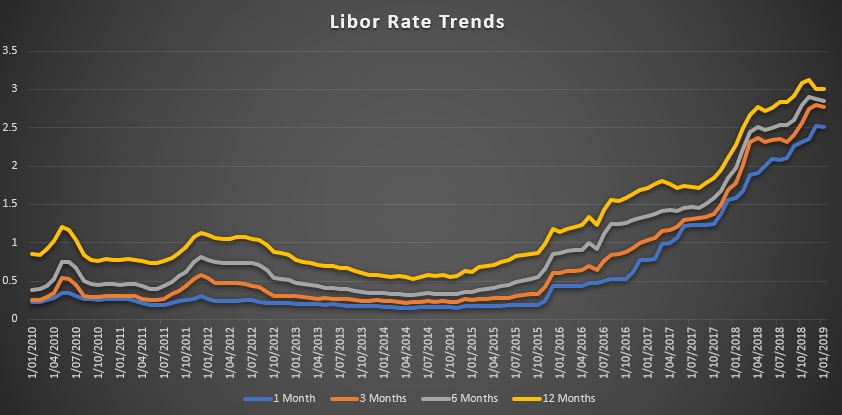

… and LIBOR rates

We expect more rises across the lending community, which will put more pressure on mortgage stress, which today stands at above one million households according to our surveys.

NABs chief customer officer Mike Baird said that the bank could no longer afford to absorb higher funding costs.

NAB lifted rates on existing principal and interest loans for owner occupiers by 12 bps to 5.36 per cent and interest-only loans for owner occupiers by 16 bps to 5.93 per cent.

The bank raised rates for

principal and interest loans for investors by 16 bps to 5.96 per cent

and for interest-only investors by 16 bps to 6.41 per cent.

NAB said its decision to keep variable rates on hold had saved 930,000 households around $70 million. The bank said it had raised rates for principal and interest loans by a smaller amount in order to encourage home owners to pay down their home loans sooner. Nice, but meaningless touch!

Another lender has repriced their back book, citing higher funding costs. “We have absorbed higher funding costs for the last twelve months in order to delay the impact for our home loan customers. Unfortunately, funding costs remain high and are likely to remain elevated into the foreseeable future.” It’s connected with the Bank of Queensland, who already lifted, of course.

As a result, Virgin Money has announced changes to its variable rates for all existing principal and interest (P&I) and interest only (IO) home loans, increasing rates by 20 basis points (bps).

However, the majority of standard variable rates for new home loan applications will remain unchanged, with only a few set to increase.

They also announced small reductions of between 5bps and 10bps for some new fixed rates products with an LVR below 90%.

So once again loyalty is NOT being rewarded.

The interest rate changes are effective Friday, 11 January 2019.

The Bank of Queensland has announced that they will lift mortgage rates for existing borrowers, thanks to higher funding costs, and pressures on bank deposits. The BBSW (interbank funding rate) has risen, and there are limits to how far deposit rates can be cut. We expect other banks to follow.

BOQ announced today that funding cost pressures and “intense”

competition for term deposits were partly behind its decision to lift

interest rates.

The rates of more than 20 of the bank’s home loan products will rise

from Friday with most set to increase by 0.18 percentage points,

including the standard variable rates for owner-occupiers and investors.

The standard variable rate for owner-occupiers paying principal and interest will rise from 5.70% to 5.88% ( comparison rate of 6.04%), while the standard variable investment housing rate will rise from 6.33% to 6.51% (comparison rate of 6.67%).

Six of its line of credit products, including the Clear Path Line of Credit Rate, will also rise by 0.18 percentage points.

The Economy Owner Occupier principal and interest home loan is the only one among the changes that will have a smaller hike of 0.11 percentage points to 3.99% (comparison rate of 4.15%).

As we highlighted yesterday, mortgage stress is on the rise with more than one million households under pressure, and these rate rises will created more pressure on household budgets.

The opaque, discretionary pricing of residential mortgages by banks makes it difficult and time consuming for borrowers to shop around and stifles price competition, a report by the ACCC has found.

The ACCC’s Residential Mortgage Price Inquiry monitored the prices

charged by the five banks affected by the government’s Major Bank Levy

between 9 May 2017 and 30 June 2018.

The ACCC’s final report

found the unnecessarily high search costs or effort required by

borrowers to find better prices reduces their willingness to shop

around, but that many borrowers who negotiate with their bank can get a

much better price.

“Pricing for mortgages is opaque and the big four banks have a lot of

discretion. The banks profit from this and it is against their

interests to make pricing transparent,” ACCC Chair Rod Sims said.

“Borrowers may not be aware they can negotiate with their lender on

price, both before and, particularly, after they have established their

mortgage.”

As at 30 June 2018, an existing borrower with an average-sized

mortgage could initially save up to $850 a year in interest if they

negotiated to pay the same interest rate as the average new borrower at

the five banks under review. For many borrowers the gain will be much

larger.

It appears that media attention on banks from the Banking Royal

Commission, the Productivity Commission’s Inquiry into competition in

the Australian financial system and the ACCC’s inquiry prompted some

borrowers to approach their lender for a better rate.

The ACCC reports that about 11 per cent of borrowers with variable

rate mortgages had the price of their current residential mortgage

reduced by one of the five banks under review in the year to 30 June

2018.

“I encourage more people to ask their lender whether they are getting

the lowest possible interest rates for their residential mortgage and,

as they do so, be ready to threaten to switch to another lender,” Mr

Sims said.

“I am afraid that the threat of switching banks will often be necessary to achieve a competitive mortgage rate.”

When directing the ACCC to conduct this inquiry, the Treasurer

requested the ACCC to report whether it found any evidence of the five

banks passing on the costs associated with the Major Bank Levy to

residential mortgage borrowers.

“The ACCC found no evidence that the five banks changed prices

specifically to recover the cost of the Major Bank Levy, whether in part

or in full, during the price monitoring period,” Mr Sims said.

The ACCC did find that measures announced by APRA in March 2017 to

limit new interest-only residential mortgage lending created an

opportunity for banks to synchronise increases to headline variable

interest rates for interest-only mortgages.

“We were not surprised banks seized the opportunity to increase

prices for interest-only loans. These price rises were enabled by the

oligopoly market structure in which the big four banks collectively have

a market share of about 80 per cent,” Mr Sims said.

ANZ was the first bank to announce increases to these interest-only

rates in June 2017. It did so safe in the knowledge that its move would

put the other banks at risk of breaching the APRA limits.

The other four banks, therefore, announced similar changes in the

same month. Together, the big four banks estimated revenue gains of over

$1.1 billion for their 2018 financial year, primarily as a result of

these rate increases.

“We consider that ANZ increased its rates, clear in its belief that,

given the APRA limits, the other big four banks would follow its lead,

and this expectation proved correct,” Mr Sims said.

The ACCC calculated that the rate increases by the five banks would

have added, in the first year, about $1300 in interest charged to the

average-sized owner-occupier interest-only standard variable mortgage.

“Such is the oligopolistic nature of banking that the banks all took

the opportunity to increase rates on both new and existing interest-only

mortgages, despite APRA’s measures only applying to new lending,” Mr

Sims said.

The ACCC also compared the approach to pricing of a sample of seven

banks that were not subject to the Inquiry. Three of these banks were

particularly focussed on competing on price, and therefore have lower

rates. Some of the banks in our sample rely heavily on brokers and

aggregators to gain market share. The ACCC notes that these banks, and

other lenders in a similar position, are likely to be more vulnerable to

future regulatory changes that affect the use of brokers as a

distribution channel.

In this report the ACCC notes that the new Consumer Data Right will,

among other things make it much easier for consumers to compare

available interest rates.

“The ACCC looks, in particular, to the Consumer Data Right to empower consumers in their dealings with banks,” Mr Sims said.

On 9 May 2017 the Treasurer, the Hon. Scott Morrison MP, issued a

direction to the ACCC to inquire into prices charged or proposed to be

charged by Authorised Deposit-taking Institutions affected by the Major

Bank Levy in relation to the provision of residential mortgage products

in the banking industry in Australia. The Major Bank Levy came into

effect from 1 July 2017.

The five banks affected by the levy are Australia and New Zealand

Banking Group Limited (ANZ), Commonwealth Bank of Australia, Macquarie

Bank Limited, National Australia Bank Limited, and Westpac Banking

Corporation.

The ACCC used its compulsory information gathering powers to obtain

documents and data from the five banks on their pricing of residential

mortgage products. The ACCC supplemented its analysis of the documents

and data supplied by the five banks with data from the Reserve Bank of

Australia (RBA), Australian Prudential Regulation Authority (APRA) and

the Australian Bureau of Statistics (ABS).

This Inquiry was the first task of the ACCC’s Financial Services Unit

(FSU), which was formed as a permanent unit during 2017 following a

commitment of continuing funding by the Australian Government in the

2017-18 Budget. Alongside the ACCC’s role in promoting competition in

financial services through its enforcement, infrastructure regulation,

open banking, and mergers and adjudication work, the FSU will monitor

and promote competition in Australia’s financial services sector by

assessing competition issues, undertaking market studies, and reporting

regularly on emerging issues and trends in the sector.

The FSU is currently examining the pricing of foreign currency

conversion services in Australia to evaluate whether there are

impediments to effective price competition in the sector. An inquiry

report is to be delivered to the Treasurer by 31 May 2019.

Today ING says it is increasing variable rates for investor mortgage customer by 15 basis points. The changes come into effect from Tuesday 25 September and is for both new and existing investor loan customers.

This is the second rise in rates – ING had already increased its rates in June by 10 basis points for owner occupier loans.

This will put more pressure on the investor segment, already wilting under the strain.

Recently of course all the big banks but NAB repriced their entire book, attributing the rise to pressure from international funding. The rate hikes already signalled will now start to bite.

Actually the BBSW has come back somewhat, but remains elevated. This chart shows the divergence to the cash rate. The point is as the majors fund some of their book from short term sources the funding gap is real and sustained.

Westpac also put the cat among the pigeons by cutting mortgage rates by up to 110 basis points for new business, as they seek to dominate the meager pickings in the changed market. This is being funded by the back book repricing, so lower risk mortgage holders who shop around may be able to grab a low low rate, for now.

In a change from honeymoon offers, the banks new loan packages includes discounts of up to 80 basis points for the life of the loan.

Expect more specials from the other major players. This may also put more pressure on NAB, who held their rates last week.

The new Westpac Group rates will also apply for new lenders for Bank of Melbourne, BankSA and St George Bank.

The offer excludes owner occupied loans with interest only repayments or to switches within the Westpac Group.

There is also an offer to first time buyers, with an 85 basis point discount for 5 years and a lower discount beyond.

Westpac has tightened their lending policies again for existing borrowers with a focus on commitments such as Afterpay and leases.

Bottom line is there is merry dance of cross subsidization in play as existing borrowers are forced to pay more, (the back book) while certain classes of refinacing and first time buyers are being enticed. However, bearing in mind that home prices are likely to fall further, buyers should beware. Always read the small print!

We also wonder how sustainable these discounts are given current margin pressures. But I guess volume and margin are being traded off at least to an extent!

After CBA and ANZ followed Westpac in hiking variable mortgage rates, we were all watching for NAB’s reaction. Well today that came with confirmation that they will keep rates on hold for now. So their rate will still be 5.24%.

NAB chief executive Andrew Thorburn said today:

“We are listening and acting differently… We need to rebuild the trust of our customers, and by holding our NAB Standard Variable Rate longer, we help our customers for longer. By focusing more on our customers, we build trust and advocacy, and this creates a more sustainable business.”

NAB say the decision benefits more than 930,000 NAB customers. If NAB had increased its SVR by 15 basis points, the average home loan customer with a $300,000 loan would have paid an extra $28 each month, or $336 a year, on their repayments. A customer with a $500,000 home loan would have paid an extra $47 each month, or $564 per year, on their repayments.

The next round of banks reports are due late October/early November, with ANZ reporting its full-year financial results on October 31, followed by NAB on November 1 and Westpac on November 5.

Commonwealth Bank of Australia has today announced it will increase its variable home loan rates, following a sustained increase in funding costs. All variable home loan rates will increase by 15 basis points from 4 October 2018.

For owner occupiers, the standard variable home loan rate will increase to 5.37% per annum for customers with principal and interest repayments, and 5.92% per annum for customers with interest only repayments.

For investors, the standard variable home loan rate will increase to 5.95% per annum for customers with principal and interest repayments, and 6.39% per annum for customers with interest only repayments.

Angus Sullivan, Group Executive Retail Banking Services Commonwealth Bank, said: “We have made this decision after careful consideration. We are very conscious of the impact that increasing interest rates will have on our customers, however it is important that we price our home loan products in a way that reflects underlying costs.

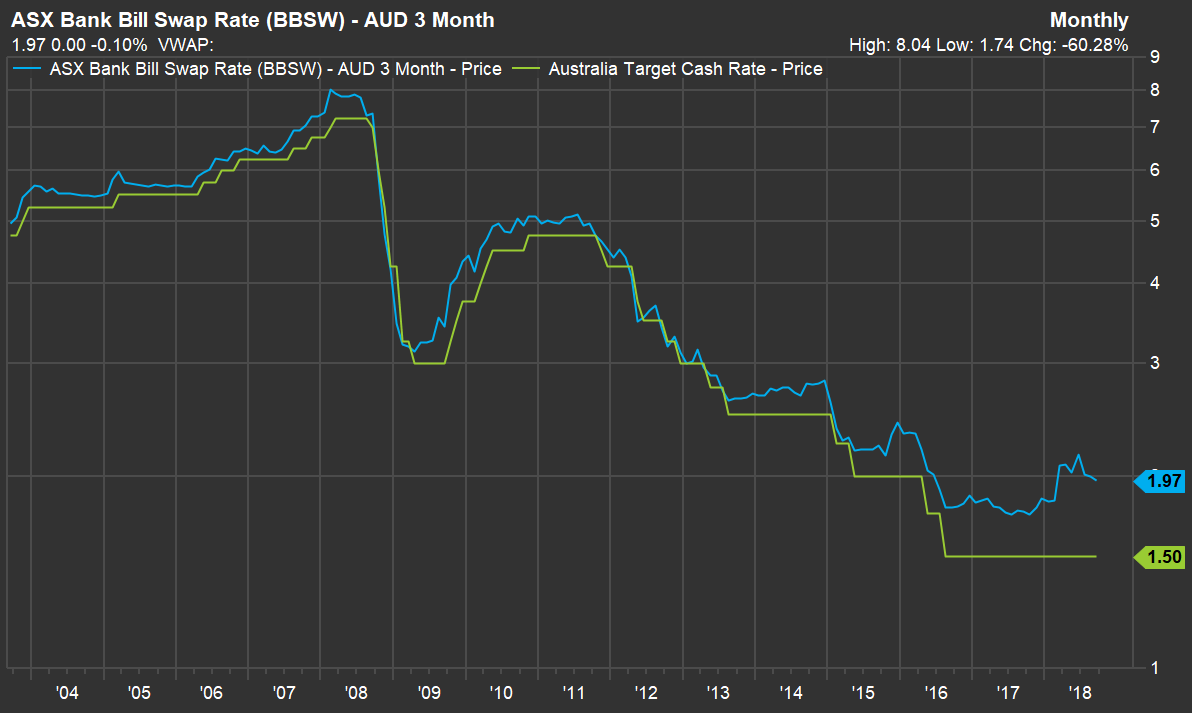

“Over the past six months, we have seen funding costs increase significantly, driven primarily by a rise in the 90 day Bank Bill Swap Rate. These changes have increased the cost of providing loans to our customers.

“We have absorbed these higher funding costs over the past six months in the hope that they would ease. Unfortunately, the costs have remained high and it is now expected that they will remain elevated for the foreseeable future.

“As a result of this, we have made the decision to raise our variable home loan rates to partially offset the increased costs. We understand this will have an impact on household budgets. To allow our customers time to prepare, this change will not take effect for four weeks, giving homeowners an opportunity to look at their options.

“For customers looking for more certainty around their mortgage repayments, we continue to offer a range of fixed rate options that may be suitable. These include a 3.79% per annum two year fixed rate for owner occupier customers, with principal and interest repayments, on our wealth package.

“We also encourage customers with interest only repayments to consider whether a lower rate principal and interest home loan would better meet their needs. Customers can switch online, in-branch or over the phone at no cost.

“Our customers can speak with one of our home lending specialists, who can review their home loan options free of charge, to ensure that their arrangements remain appropriate for their circumstances.”

The increase to our variable home loan rates will come into effect on 4 October 2018

The music continues with ANZ announcing it will increase its variable interest home loan rates. This of course is the second of the big four banks to raise mortgages in response to higher funding costs.

Variable interest rates for home and residential investment loans will rise by 16 basis points (Westpac’s was 14 basis points), effective September 27. This means the declared rate for a principal and interest loan will now be 5.36%. That said, NO rise for ANZ home loan customers in drought-declared regional Australia are planned.

Fred Ohlsson, ANZ Group Executive Australia, says the decision to lift was a difficult one.

“We know the impact rising interest rates have on family budgets,” he says.

“The reality is it is more expensive for us to fund our home loans on wholesale markets and we also needed to balance the needs of all stakeholders.

“There is no change to the effective rates of our home loan customers in drought declared regional Australia benefiting more than 70,000 of our customers.

“We wanted to play our part in keeping cash in regional towns impacted by the drought and we hope this will also assist both families and small businesses in these areas.”