Over a third of the world’s banks lag on technology and scale, and are unprepared for an economic downturn, according to global consultancy firm McKinsey and Co, via InvestorDaily.

The

firm used its annual banking review to warn banks that they risked

“becoming footnotes to history” if they did not scale up and embrace

technological change.

“About 35 percent of banks globally are both subscale and suffer from operating in unfavorable markets,” the report reads.

“Their business models are flawed, and the sense of urgency is acute.”

According

to the report, banks need to merge with or acquire more companies and

forge new partnerships in order to build scale and weather the financial

storm.

They also need to be prepared for an “arms race on technology”.

“Both

banks and fintechs today spend approximately 7 percent of their

revenues on IT; but while fintechs devote more than 70 percent of their

budget to launching and scaling up innovative solutions, banks end up

spending just 35 percent of their budget on innovation with the rest

spent on legacy architecture,” the report reads.

The report noted

the efforts of Amazon in the US, which offers businesses traditional

banking services while connecting them to the Amazon “ecosystem” of

non-financial products and services, and pointed to blockchain and

artificially intelligent systems as some of the advances banks need to

embrace in order to survive.

Banks could also outsource some

“non-differentiating” activities – activities that do not differentiate

the bank from its competitors, such as “know your customer” and

anti-money laundering compliance, which can represent as much as 7 per

cent and 12 per cent of costs.

However, some factors – like geography – were outside of bank control.

The

report noted that North American banks hit a ROTE of 16 per cent in

2018, while European banks barely managed half of this, with

implications for their performance in the event of downturn.

The report also warned of the potential impact of a downturn on public perception of banks.

“Because

of the special role they play in society, they, perhaps more than other

industries, benefit from society in areas such as deposit protection

and regulation as a means of constraining supply,” the postscript to the

report reads.

“In return, they are particularly accountable in

an era of rising inequality and falling faith in historically trusted

institutions; beyond shareholders to society and the sustainability of

the environment in which they and their clients operate.”

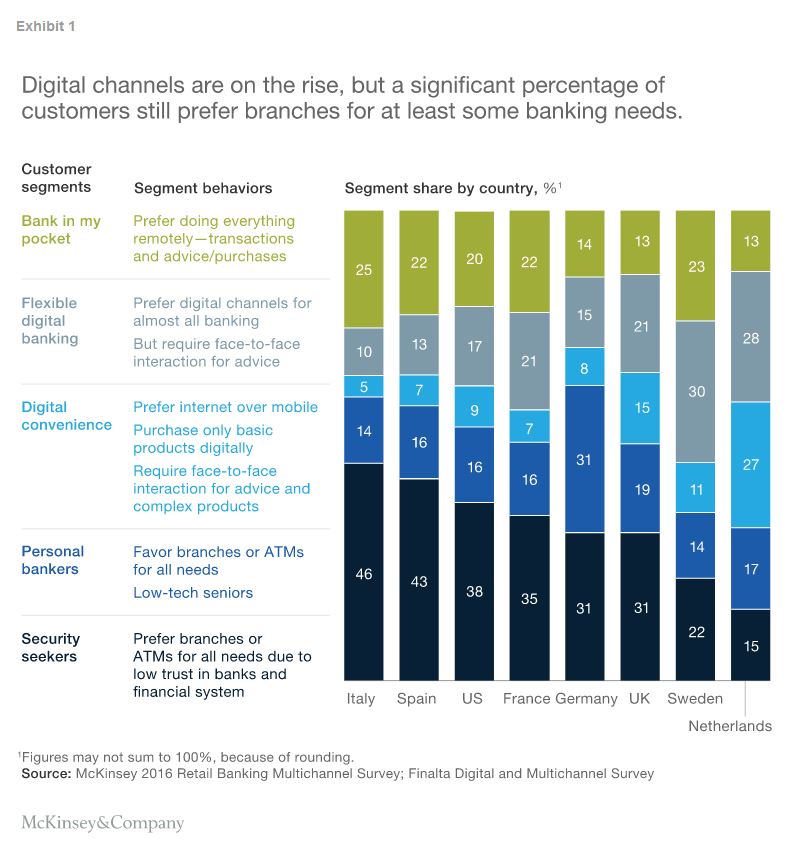

As we discussed this week, the writing is on the wall for bank branches, and more will be closed in the months ahead as the digital revolution continues. You can read our latest research in our “Quiet Revolution” report.

Bankwest announced the closure of a significant number of branches on the east coast, as discussed in this segment.

In it, they argue that digital technology could be harnessed within the branch to enhance customer experience there, and that there is still a role for bank real estate. We are less convinced, as in Australia at least, the digital revolution is well advanced, and brokers provide an alternative face to face sales channel. But in-branch tech may give branches some extra utility, for a short while.

Far from rendering the bank branch obsolete, digital technology holds the key to the branch of the future.

The bank branch as we know it, with tellers behind windows and bankers huddled in cubicles with desktop computers, needs reinvention. Most customers now carry a bank in their pockets in the form of a smartphone and only visit an actual branch to get cash or, occasionally, advice. Globally, financial institutions now process far more transactions digitally than in branches, and since the financial crisis of the late 2000s, more than 10,000 US bank branches have closed—an average of three a day.1

Despite such systemic changes, branches remain an essential part of banks’ operations and customer-advisory functions. Brick-and-mortar locations are still one of the leading sales channels. Even in digitally advanced European nations, between 30 and 60 percent of customers prefer doing at least some of their banking at branches, according to McKinsey research.

Changing customer behavior and the emergence of new technologies spell not the end of the branch but rather the advent of the “smart branch.” Smart branches use technology to boost sales and improve customer experience significantly. When done right, applying the concept transforms the way a bank branch operates (reduced staffing), significantly lowers real-estate requirements, and alters customer interaction (targeted, relevant sales and service-to-sales programs)—with a resulting 60 to 70 percent improvement in branch effectiveness, as measured by cost savings and increased sales.

Our research shows that although many banks have started to adopt elements of the smart-branch model, most are not extracting the full value potential. Making branches smart is not a matter of simply installing new machines or buying a suite of tablet computers. Smart-branch transformation builds on three pillars: the seamless integration of cutting-edge branch technology, which has become cheaper, more reliable, and more accessible; the adoption of radically new, teller- and desk-free branch formats at every location; and the use of digital technology and advanced analytics to improve the operating model in branches, including personalized, data-driven sales and real-time performance management and skill development.

An excellent article from Mckinsey which makes the point that if Digital Transformation this isn’t on your agenda, then you’ve got the wrong agenda! Its not about new shiny tech things. Rather, all value chains will be disrupted, it is revolutionary. The benefits are breathtaking.

Digital transformation is about sweeping change. It changes everything about how products are designed, manufactured, sold, delivered, and serviced—and it forces CEOs to rethink how companies execute, with new business processes, management practices, and information systems, as well as everything about the nature of customer relationships. I’m seeing leaders who get this. They’re all over it: they want to launch five transformation initiatives right now; they’re talking to me and every digital leader they know about where the technology threats are coming from; and they’re hiring the best people to advise them. Yet I’m shocked by—even fearful for—the many CEOs I know who seem to be asleep at the switch. They just don’t see the massive disruption headed their way from digital threats, seen or unseen, and they don’t seem to understand it will happen very quickly.

So when I see CEOs who may be experimenting here and there with AI or the cloud, I tell them that’s not enough. It’s not about shiny objects. Tinkering is insufficient. My advice is that they should be talking about this all the time, with their boards, in the C-suite—and mobilizing the entire company. The threat is existential. For boards, if this isn’t on your agenda, then you’ve got the wrong agenda. If your CEO isn’t talking about how to ensure the survival of the enterprise amid digital disruption, well, maybe you’ve got the wrong person in the job. This may sound extreme, but it’s not.

It’s increasingly clear that we’re entering a highly disruptive extinction event. Many enterprises that fail to transform themselves will disappear. But as in evolutionary speciation, many new and unanticipated enterprises will emerge, and existing ones will be transformed with new business models. The existential threat is exceeded only by the opportunity.

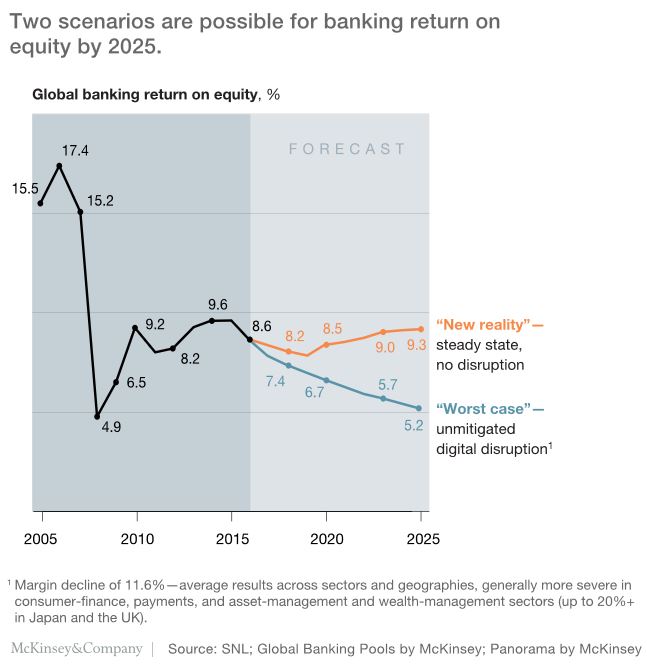

Looking across the world of banking, there is one striking trend according to the latest Mckinsey Global Banking Report. Profit remains elusive as margins are crushed. Return on equity is stuck in a range of 8 to 10 per cent (though we note Australian Banks’ are higher!, but are still falling). Recovery from the 2007 banking crisis has, they say, been tepid.

Underlying this is a slowing in revenue growth, currently as low as 3%, half that of the previous five years – so margins are down 35 basis points in China and 46 basis points in the USA. They suggest that in a fully disrupted world ROE could fall to around 5%, compared with around 9.3% without disruption.

They claim the biggest contribution to profitability is not geography, but a bank’s business model.

We found that “manufacturing”—the core businesses of financing and lending that pivot off the bank’s balance sheet—generated 53.0 percent of industry revenues, but only 35.0 percent of profits, with an ROE of 4.4 percent. “Distribution,” on the other hand—the origination and sales side of banking—produced 47 percent of revenues and 65 percent of profits, with an ROE of 20 percent.

Now new digital platform players are threatening customer relationships and stealing margin. But Fintechs, which were seen as an outright threat initially, are now collaborating with major players, for example Standard Chartered and GlobalTrade, Royal Bank of Scotland and Taulia, and Barclays and Wave.

“digital pioneers are bridging the value chains of various industries to create “ecosystems” that reduce customers’ costs, increase convenience, provide them with new experiences, and whet their appetites for more.”

So they argue, banks are at a cross roads. Should banks participate in this new digital ecosystem or resit it? To participate, banks will have to deploy a vast digital toolkit. This offers a path to sustainable higher ROE, perhaps. This is a substantive digital transformation, designed from customer centricity.

The point, we would add from our Quiet Revolution banking channel analysis, is that customers are already ahead of banks, demanding more and better digital services, so first in best dressed!

Financial institutions have embarked on a “broad-based retreat” from cross-border activities in the decade since the global financial crisis, according to management consultancy McKinsey & Co.

Reflecting on the past decade for a McKinsey Global Institute podcast, Washington, DC-based partner Susan Lund said there has been a clear change in behaviour from global banks since the downturn.

“In the 10 years since the global financial crisis began, cross-border capital flows have fallen by 65 per cent, from over $12 trillion to just over $4 trillion in 2016,” Ms Lund said. “Half of that decline is coming from a decline in cross-border lending and other types of banking activity.”

The decline is symptomatic of decisions by bank boardrooms to reduce foreign exposure, the management consultant said, retreating to an inward-looking focus on national interests.

“[Global banks are] selling foreign businesses,” she said. “They’re allowing loans to expire without renewing them, and they’re selling different types of foreign assets. Overall, there’s been a broad-based retreat toward more domestic activity.”

The first key driver of the trend has been the need for some institutions – particularly those adversely affected by the GFC – to “rebuild capital and recoup losses”, minimising risks and costs associated with offshore ventures.

The second has been increasing regulatory requirements post-GFC, which have forced a greater focus on domestic compliance.

Speaking on the same podcast, Frankfurt-based MGI partner Eckart Windhagen said the retreat has been particularly advanced among eurozone banks, many of which were bullish on cross-border activity before 2008.

While Western and European banks have retreated, some Asia-Pacific financial institutions – including those domiciled in China – have been expanding their global reach over the past decade, especially in emerging markets such as economies in Africa and Latin America.

However, despite this trend, only 9 per cent of total assets of Chinese banks are held outside of China, the McKinsey partners clarified.

Asked whether the retreat of global banks from cross-border activity spells “the end of financial globalisation”, Mr Windhagen responded emphatically in the negative.

“Financial globalisation is surprisingly robust,” he said.

“Financial markets remain deeply interconnected, but with a different profile.

“The global value of foreign investment as a percentage of GDP has been steady since 2007, at around 180 per cent, and now stands as an absolute figure at more than $130 trillion.”

In Australia, we have seen ANZ retreat from part of its Asia-Pacific expansion strategy and NAB divest from its UK banking assets.

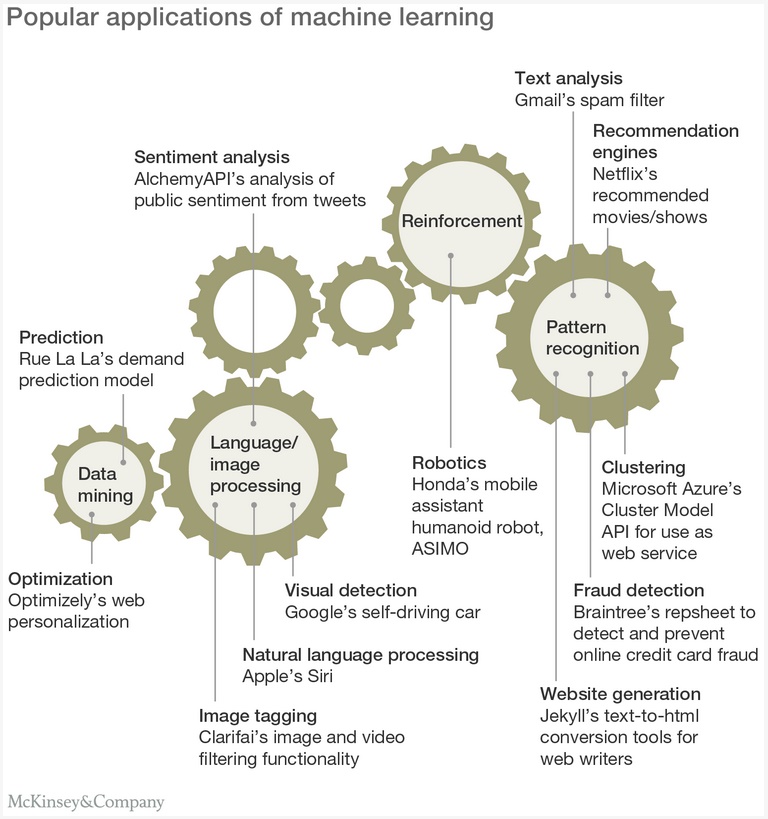

Good article from McKinsey on the revolution catalysed by the combination of machine learning and new payment systems as part of big data. The outline some of the opportunities to expand the use of machine learning in payments range from using Web-sourced data to more accurately predict borrower delinquency to using virtual assistants to improve customer service.

Machine learning is one of many tools in the advanced analytics toolbox, one with a long history in the worlds of academia and supercomputing. Recent developments, however, are opening the doors to its broad-scale applicability. Companies, institutions, and governments now capture vast amounts of data as consumer interactions and transactions increasingly go digital. At the same time, high-performance computing is becoming more affordable and widely accessible. Together, these factors are having a powerful impact on workforce automation. McKinsey Global Institute estimates that by 2030 47 percent of the US workforce will be automated.

Payments providers are already familiar with machine learning, primarily as it pertains to credit card transaction monitoring, where learning algorithms play important roles in near real-time authorization of transactions. Given today’s rapid growth of data capture and affordable high-performance computing, McKinsey sees many near- and long-term opportunities to expand the use of machine learning in payments. These include everything from using Web-sourced data to more accurately predict borrower delinquency to using virtual assistants to improve customer service performance.

Machine learning: Major opportunities in payments

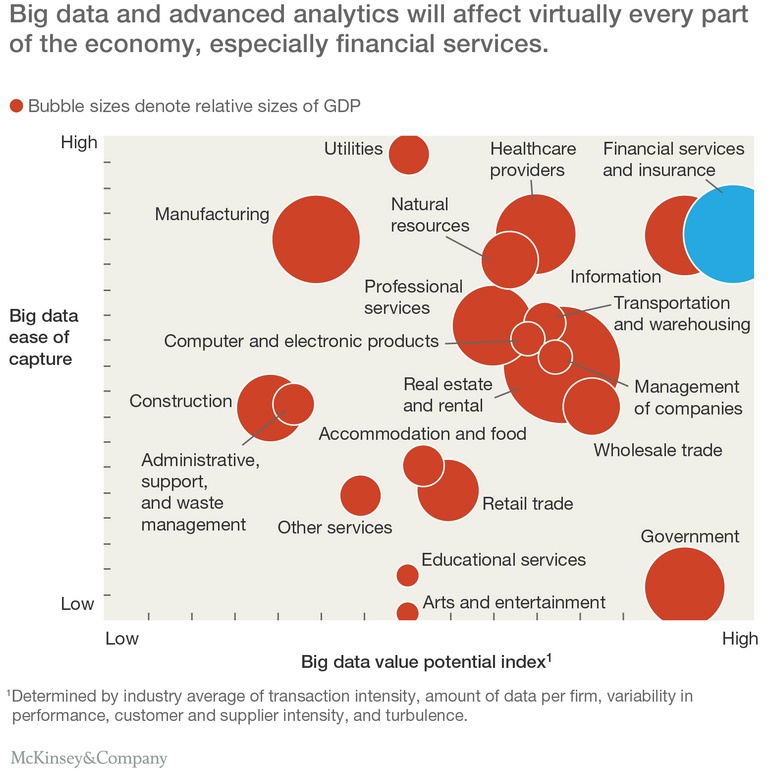

Rapid growth in the availability of big data and advanced analytics, including machine learning, will have a significant impact on virtually every part of the economy, including financial services (exhibit). Machine learning can be especially effective in cases involving large dynamic data sets, such as those that track consumer behavior. When behaviors change, it can detect subtle shifts in the underlying data, and then revise algorithms accordingly. Machine learning can even identify data anomalies and treat them as directed, thereby significantly improving predictability. These unique capabilities make it relevant for a broad range of payments applications.

What is machine learning?

Machine learning is the area of computer science that uses large-scale data analytics to create dynamic, predictive computer models. Powerful computers are programmed to analyze massive data sets in an attempt to identify certain patterns, and then use those patterns to create predictive algorithms (exhibit). Machine learning programs can also be designed to dynamically update predictive models whenever changes occur in the underlying data sources. Because machine learning can extract information from exceptionally large data sets, recognize both anomalies and patterns within them, and adjust to changes in the source data, its predictive power is superior to that of classical methods.

Machine learning has already established a strong foothold in credit cards, particularly in fraud management. PayPal’s Braintree Auth payments tool, for example, uses PayPal’s consumer transaction data in conjunction with software developer Kount’s fraud detection capabilities to authorize high volumes of transactions and verifications in near real-time. Each credit card transaction or verification is analyzed in milliseconds using hundreds of fraud detection tests.

There are several other areas in the payments value chain where machine learning is adding significant value:

Product sales: Machine learning can be a powerful tool for developing deeper insights about customers and sales prospects because it can draw upon a wider variety of internal and external data than marketers have traditionally used. It can more accurately cluster customers and prospects into segments according to their profiles and probable needs. This deeper insight can reveal new opportunities for cross-selling and up-selling among both customers and prospects. McKinsey finds that with machine learning payments providers can increase revenue from existing customers by 10 to 15 percent.

Customer retention: Companies typically monitor and forecast customer churn based on changes in account status; when churn rates rise they take steps to address the problem. Now, through machine learning, they can identify those customers they are at risk of losing and act quickly to retain valuable customers. For example, 47Lining, an Amazon Web Services partner, uses a combination of site behavior, demographics, and media-sentiment measures to predict customer churn with 71 percent accuracy. Companies using machine learning to address customer churn have achieved reductions of as much as 25 percent.

Collections: Collection practices and debt restructuring work best when closely aligned with borrowers’ changing circumstances and propensity to pay. Machine learning can help companies build robust dynamic models that are better able to segment delinquent borrowers, and even identify self-cure customers (that is, customers that proactively take action to improve their standing). This enables them to better tailor their collection strategies and improve their on-time payment rates. TrueAccord’s HeartBeat, for instance, is a machine learning tool that helps lenders customize personal interactions in real time, based on its ability to detect why a customer’s payments are late. Companies using machine learning have been able to reduce their bad debt provision by 35 to 40 percent.

Treasury pricing: In commercial payments, companies can capture 10 to 15 percent more revenue through optimized treasury pricing. In the near term, advanced analytics can identify quick-win opportunities to reduce price leakage (such as discounts exceeding authorized limits) and billing errors. Over the long term, clustering techniques built on machine learning can significantly improve customer segmentation and lead to more appropriate pricing models.

Customer care: Over time, McKinsey expects to see a gradual increase in the automation of many customer services. This is an area in which the cognitive intelligence capabilities of machine learning are particularly well suited. Among the benefits are: lower servicing costs, enhanced agent performance, more efficient capacity management, improved digital customer experience, reduced risk, and elimination of waiting times. A variety of relevant applications are already available, including virtual assistants that use natural language processing, deep insight tools like IBM’s Watson, and cognitive engines that can do things presently handled by humans, such as IPSoft’s Amelia, which can understand and interact with people (see sidebar, “Cognitive agents”).

Machine learning in the card collection environment

Cognitive agents

Cognitive agents like IPSoft’s Amelia combine natural language and deep insight technologies to complete tasks typically handled by humans. Using a three-step process, they help companies intelligently automate a variety of tasks:

Understand: Cognitive agents can rapidly absorb and comprehend a diverse range of data sets, from complex manuals to call logs and flow charts.

Learn: Cognitive agents absorb data from the customer language they process, and can refer the customer to a live agent language they process, and can refer the customer to a live agent when uncertain about how to react. They also learn from cases they refer to agents, further improving effectiveness as they continue to record interactions and data.

Resolve: Finally, cognitive agents can directly resolve customer inquiries received through online chat, mobile, and voice channels. Alternatively, when connected to a backend system they can support live agents in resolving customer issues.

Service automation tools can help payments providers increase customer satisfaction, enhance financial performance, and improve compliance.

In card issuing, machine learning is already having a valuable impact. This is especially true in collections, where McKinsey has seen 10 to 15 percent improvements in recovery rates and 30 to 40 percent increases in collections efficiency. To minimize delinquencies, issuers can use individual-account pattern recognition technologies, and develop contact guidelines and strategies for accounts that are already delinquent. Following an account delinquency, issuers allow a brief time window (usually 90 days) before they write off the receivables and turn collection over to third-party providers. This brief period is an ideal time for issuers to apply collection strategies that draw heavily on the capabilities of machine learning.

An excellent article from McKinsey (I may be biased, but analytics used right are very very powerful!).

More than 90 percent of the top 50 banks around the world are using advanced analytics. Most are having one-off successes but can’t scale up. Nonetheless, some leaders are emerging. Such banks invest in talent through graduate programs. They partner with firms that specialize in analytics and have committed themselves to making strategic investments to bolster their analytics capabilities. Within a couple of years, these leaders may be able develop a critical advantage. Where they go, others must follow—and the sooner the better because success will come, more than anything else, from real-world experience.

By establishing analytics as a true business discipline, banks can grasp the enormous potential. Consider three recent examples of the power of analytics in banking:

To counter a shrinking customer base, a European bank tried a number of retention techniques focusing on inactive customers, but without significant results. Then it turned to machine-learning algorithms that predict which currently active customers are likely to reduce their business with the bank. This new understanding gave rise to a targeted campaign that reduced churn by 15 percent.

A US bank used machine learning to study the discounts its private bankers were offering to customers. Bankers claimed that they offered them only to valuable ones and more than made up for them with other, high-margin business. The analytics showed something different: patterns of unnecessary discounts that could easily be corrected. After the unit adopted the changes, revenues rose by 8 percent within a few months.

A top consumer bank in Asia enjoyed a large market share but lagged behind its competitors in products per customer. It used advanced analytics to explore several sets of big data: customer demographics and key characteristics, products held, credit-card statements, transaction and point-of-sale data, online and mobile transfers and payments, and credit-bureau data. The bank discovered unsuspected similarities that allowed it to define 15,000 microsegments in its customer base. It then built a next-product-to-buy model that increased the likelihood to buy three times over.

Results like these are the good news about analytics. But they are also the bad news. While many such projects generate eye-popping returns on investment, banks find it difficult to scale them up; the financial impact from even several great analytics efforts is often insignificant for the enterprise P&L. Some executives are even concluding that while analytics may be a welcome addition to certain activities, the difficulties in scaling it up mean that, at best, it will be only a sideline to the traditional businesses of financing, investments, and transactions and payments.

In our view, that’s shortsighted. Analytics can involve much more than just a set of discrete projects. If banks put their considerable strategic and organizational muscle into analytics, it can and should become a true business discipline. Business leaders today may only faintly remember what banking was like before marketing and sales, for example, became a business discipline, sometime in the 1970s. They can more easily recall the days when information technology was just six guys in the basement with an IBM mainframe. A look around banks today—at all the businesses and processes powered by extraordinary IT—is a strong reminder of the way a new discipline can radically reshape the old patterns of work. Analytics has that potential.

Tactically, we see banks making unforced errors such as these:

not quantifying the potential of analytics at a detailed level

not engaging business leaders early and to develop models that really solve their problems and that they trust and will use—not a “black box”

falling into the “pilot trap”: continually trying new experiments but not following through by fully industrializing and adopting them

investing too much up front in data infrastructure and data quality, without a clear view of the planned use or the expected returns

not seeking cooperation from businesses that protect rather than share their data

undershooting the potential—some banks just put a technical infrastructure in place and hire some data scientists, and then execute analytics on a project-by-project basis

not asking the right questions, so algorithms don’t deliver actionable insights

Research from McKinsey shows that despite all the hype surrounding digital transformation, there is a long way to go for many organisations, and the rate of transformation varies across industries. Yet already there is already profound economic fallout.

This finding confirms what many executives may already suspect: by reducing economic friction, digitization enables competition that pressures revenue and profit growth. Current levels of digitization have already taken out, on average, up to six points of annual revenue and 4.5 points of growth in earnings before interest and taxes (EBIT). And there’s more pressure ahead, our research suggests, as digital penetration deepens

At the current level of digitization, median companies, which secure three additional points of revenue and EBIT growth, do better than average ones, presumably because the long tail of companies hit hard by digitization pulls down the mean. But our survey results suggest that as digital increases economic pressure, all companies, no matter what their position on the performance curve may be, will be affected.

Mckinsey says that Consumer adoption of digital banking channels is growing steadily across Asia–Pacific, making digital increasingly important for driving new sales and reducing costs. The branch-centric model is gradually but unmistakably giving way to the mobile-centric one.

Deferring the development and refinement of a digital offering leaves a bank exposed to the risk of weakened relationships and lower profitability. Now is a critical moment to draw retail-banking customers toward Internet and mobile-banking channels, regardless of the general level of network connectivity in a given market.

Our annual study, the Asia–Pacific Digital and Multichannel Banking Benchmark 2016, was led by Finalta, a McKinsey Solution, and examined digital consumer-banking data collected between July 2015 and July 2016 from 41 banks. This article focuses on our findings from Australia and New Zealand, Hong Kong, Malaysia, Singapore, and Taiwan, examining consumer digital engagement, user adoption, and traffic and sales via Internet secure sites, public sites, and mobile applications.1 We detail three counterintuitive findings, and make suggestions for how banks should move forward.

Three counterintuitive findings

Consumer use of digital banking is growing steadily across all five markets (Exhibit 1). In the more developed markets of Australia and New Zealand, Hong Kong, and Singapore, growth in recent years has been concentrated in the mobile channel. Indeed, among some banks use of the secure-site channel has begun to shrink, as some customers enthusiastically shift most of their interactions to mobile banking. In emerging markets, growth is strong in both secure-site and mobile channels.

Exhibit 1

Three counterintuitive findings point to the need for banks to act aggressively to improve their use of digital channels to strengthen customer relationships.

First, banks can excel in their digital offering despite limitations in the digital maturity of the markets they serve. One measure of digital maturity is the Networked Readiness Index (NRI), published annually by the World Economic Forum. This scorecard rates how well economies are using information and communication technology. It examines 139 countries using 53 indicators, including the robustness of mobile networks, international Internet bandwidth, household and business use of digital technology, and the adequacy of legal frameworks to support and regulate digital commerce. Comparison of digital-banking adoption with the level of networked readiness reveals that a country’s level of digital maturity does not necessarily promote or inhibit the growth of a bank’s digital channels.

Singapore, for example, has the most highly developed infrastructure for digital commerce in the world. However, when it comes to digital banking, Singaporean banks trail their peers from the less-networked markets of Australia and New Zealand, where banks have been able to draw consumers to digital channels despite gaps or weaknesses in digital connectivity.

Some banks have also been successful in pushing mobile banking regardless of network limitations (Exhibit 2). While Australia and New Zealand have moderately high levels of third-generation (3G) and smartphone penetration (trailing both Hong Kong and Singapore), the banks surveyed have achieved much stronger consumer adoption of mobile channels than their peers in other markets.

Exhibit 2

The second key finding is that having a relatively small base of active users does not necessarily mean low traffic (Exhibit 3). Among all participating banks in our survey, banks in Malaysia report among the smallest share of customers using the secure-site channel; however, these customers tend to log on many times a month, and the typical secure-site customer interacts with the bank more than twice as often as the secure-site banking customers of participating banks in Hong Kong and Singapore.

Exhibit 3

Third, the survey data reveal wide variations in performance across key metrics by country. In Australia and New Zealand, for example, there is wide variation in digital-channel traffic, with customers logging on with 32 percent more frequency at participating banks in the upper quartile than those in the lower quartile. In Hong Kong, digital adoption among upper quartile peers exceeds that of the lower quartile peers by ten percentage points. Participants in Singapore observe a sixteen-percentage-point gap between the upper and lower quartile peers in the proportion of sales through digital channels.2 The wide gap between best and worst in class in multiple markets points to a significant opportunity for banks to beat the competition with compelling digital offers.

What banks should do

Banks in emerging markets have an opportunity to leapfrog to digital banking. Despite gaps in technology and smartphone penetration, a number of banks have tapped into consumer segments eager to adopt digital channels. Banks in emerging markets should prepare for rapid consumer adoption of digital channels. The digital evolution in emerging markets will differ considerably from the trajectory of banks in more developed markets.

Banks in highly developed markets have room to grow their active user base and digital sales. Indeed, the cost and revenue position of banks that do not act to improve their digital offering may weaken relative to peers that shift more business to digital channels. Banks in all markets should plan for this transition, especially through the integration of diverse technology platforms, the consolidation of customer data across multiple channels, and the continuous analysis of customer behavior to identify real-time needs. It is important to build services rapidly and to go live with minimally viable prototypes in order to attract early adopters—these digital enthusiasts eagerly experiment with new features and provide valuable feedback to help developers.

The significant variation of performance among countries shows great potential for banks to boost digital engagement with a dual emphasis on enrollment and cross-selling. Banks should carefully consider four best practices that often bring immediate gains by streamlining the customer’s digital experience:

Deliver credentials instantaneously upon in-app enrollment. The global best practice shows that banks that issue credentials instantaneously through in-app enrollment see their mobile activity rise on average 1.5 times faster. Of the banks that provided data on functionality, more than 50 percent do not have in-app enrollment. This presents a significant value-creation opportunity.

Simplify authentication processes to make them both secure and user friendly. Approximately three in five banks surveyed lack the ability to authenticate a user’s mobile device. In our experience, banks that store device information and allow users to log on simply by entering a personal identification number or fingerprint see three times more digital interaction than banks that require users to enter data via alphanumeric digits each time they log on.

Implement ‘click to call’ routing to improve response times. Instead of using a voice-response system, where customers must listen to a long list of options before selecting the relevant service choice, an increasing number of mobile apps are adopting click-to-call options for each segment, enabling customers to bypass the voice-response menus. Of the banks that provided data on capability, only 30 percent in our Asia–Pacific survey offer authenticated click-to-call options. The improvement in customer service is significant, with global banks able to improve the speed of answering customer calls by up to 40 percent.

Make digital sales processes intuitive and simple. Take credit cards as an example: best-practice global banks achieve average conversion rates (the ratio of page visits to applications) some 1.6 times those of Asia–Pacific banks. They do this by presenting products and features for which a customer has been prequalified through an intuitive, easy-to-read dashboard display or via tailored messages. Application forms are prefilled automatically with customer data. With intuitive and simple applications, banks in the Asia–Pacific region could increase the rate of completed applications by 22 percent, to come up to par with global best-practice banks.

Across the five markets we focused on, the branch-centric model is gradually but unmistakably giving way to the mobile-centric one. Looking at how digital-channel adoption and usage is evolving, along with the diversity of scenarios, banks have ample room to win in their target markets with a carefully tailored digital offering. Digital-savvy consumers warm quickly to well-designed and easy-to-use digital-banking channels, often shifting to the new channel in a matter of days. Banks need to act quickly to improve their customers’ digital experience or risk being left behind.

Mckinsey in a new report “A brave new world for global banking“, says three formidable forces—a weak global economy, digitization, and regulation—threaten to significantly lower profits for the global banking industry over the next three years. Developed-market banks are most affected, with $90 billion, or 25 percent, of profits at risk, but emerging-market banks are also vulnerable, especially to the credit cycle. Countering these forces will require most banks to undertake a fundamental transformation centered on resilience, reorientation, and renewal.

Our report, A brave new world for global banking: McKinsey global banking annual review 2016, finds that of the major developed markets, the United States banking industry seems to be best positioned to face these headwinds, and the outcome of the recent presidential election has raised industry hopes of a more benign regulatory environment. Japanese and US banks have between $1 billion and $45 billion in profits at risk by 2020, depending on the extent of digital disruption. Yet after mitigation, their profitability would drop by only one percentage point to 8 percent for US banks and 5 percent in Japan. Banks in Europe and the United Kingdom have $35 billion, or 31 percent, of profits at risk; more severe digital disruption could further cut their profits from $110 billion today to $50 billion in 2020, and slice returns on equity (ROEs) in half to 1 to 2 percent by 2020, even after some mitigation efforts (see exhibit for how digitization may reduce fees and margins across different businesses).

Exhibit

Emerging-market banks face a different challenge. They are structurally more profitable than their developed-market counterparts, with ROEs well above the 10 percent cost of capital in most cases but vulnerable to the credit cycle. Brazil, China, and Russia could have $50 billion in profits at risk, with China comprising $47 billion. A slower growth scenario could result in additional credit losses of up to $250 billion, of which $220 billion would be in China, our report finds, but with their current high profitability of $320 billion, Chinese banks should be able to withstand these losses.

Three formidable challenges

Banks must adapt to the reality of a macroeconomic environment that offers a number of risks and limited upside potential. Along with stagnating growth, banks face enormous challenges to digest the wave of postfinancial-crisis regulation, despite industry hopes of a more benign regulatory environment in the United States. Control costs in risk, finance, legal, and compliance have shot up in recent years. And additional proposals, termed “Basel IV,” are likely to include stricter capital requirements, more stress testing, and new guidelines for conduct and compliance risk.

Meanwhile the pressures of digitization, which boosts competition and compresses margins, are growing. Some emerging-market banks are managing well, offering innovative mobile services to customers. But our report finds that in the largest emerging markets, China and India, banks are losing ground to digital-commerce firms that have moved rapidly into banking.

In developed economies, digitization is impacting banks in three major ways. First, regulators, who were initially more conservative about the entry of nonbanks into financial services, are now gradually opening up. Over time, huge tech companies may be able to insert themselves between banks and their customers, capturing the vital customer relationship and presenting an existential threat. On the positive front, a number of banks are teaming up with fintech and digital firms, using big data and analytics to sharpen risk assessment and drive revenue growth. Lastly, many banks have been able to digitize processes and dramatically lower costs in their middle and back offices (although digitization can sometimes add costs).

A fundamental transformation

Countering the headwinds now gathering force means most banks will need to embark on a fundamental transformation that exceeds their previous efforts. Tinkering around the edges, as many banks have done for years, is not adequate to the scale of the task and will only exacerbate the sense of fatigue that comes from years of one-off restructurings.

This transformation is centered on three themes:

Resilience. Banks must ensure the short-term viability of their business through tactical measures to restore revenues, cut costs, and improve the health of the balance sheet. They need to protect revenues through repricing and greater intermediation, reduce short-term costs, manage capital and risk, and protect core business assets. Our report found that digitization is only the start of the answer on costs, with radical reductions in functional costs needed to fundamentally rebase the cost structure.

Reorientation. While the resilience agenda is defensive in nature, in reorientation, banks go on offense. They must reorient their business models to the customer and the new digital environment by establishing the bank as a platform for data and digital analytics and processes, and aggressively linking up with fintechs, platform providers, and other banks to share costs through industry utilities. They also need to streamline their operating models and IT structure and move toward a proactive regulatory strategy.

Renewal. The industry must move beyond traditional restructuring and renew the bank via new technological capabilities, as well as new organizational structures. Any new business model that banks design will likely require new technology and data skills, a different form of organization to support the frenetic pace of innovation, and shared vision and values across the organization to motivate, support, and enable this profound transformation.