ASIC is warning credit providers and debt management firms that strong, targeted action against predatory lending, high-cost credit and misconduct impacting consumers experiencing financial difficulty is expected in the coming months as part of its continuing focus on protecting consumers.

Timely, given the high cost of debt, and the pressure many households and businesses are under. Remember more debt is not necessarily the answer!

NAB has updated its mortgage serviceability assessment policy, becoming the final big four bank to amend its policy in response to APRA’s new guidance. Via The Adviser.

It has lowered its interest rate floor to 5.5 per cent and increased its interest rate buffer to 2.5 per cent, effective for all new home loan applications from 5 August.

The revisions have come in response to the Australian Prudential Regulation Authority’s (APRA) changes to

its home lending guidance, in which it scrapped the 7 per cent interest

rate floor for mortgage assessments and increased the buffer rate to

2.5 per cent.

Commenting on the

changes, NAB’s chief customer officer, consumer banking, Mike Baird

said: “NAB welcomes the updated APRA guidelines on home lending

serviceability.

“We believe now is the

right time to change the approach to how the affordability rate floor is

determined, given the continuing low interest rate environment.”

He

added: “As a responsible lender, serviceability is assessed using a

number of factors and we consider all lending applications on a

case-by-case basis.”

NAB

has matched ANZ’s rate floor of 5.5 per cent, and has undercut CBA and

Westpac, who dropped their floor rates to 5.75 per cent.

However, as

it stands, Macquarie has the lowest floor rate (5.3 per cent), with

MyState on the opposite side of the spectrum, dropping its floor rate to

just 6.2 per cent.

All the aforementioned lenders have also increased their buffer rates to 2.5 per cent.

Other

lenders are expected to follow suit, including non-banks, with Resimac,

which, along with the rest of the non-bank sector is not formally bound

by APRA’s guidance, also confirming that it is reviewing its policy.

The lending landscape has changed dramatically over the past year, with near-prime lending becoming the fastest-growing sector and lenders beginning to see the rise of “super prime” borrowers; via The Adviser.

Given

the reduced risk appetites from the banks following the banking royal

commission and an increasing trend from the majors to “simplify” their offerings, the non-bank lenders have taken a growing proportion of market share

as more borrowers fall outside of the credit policies and brokers turn

to non-banks for more specialised products for their clients.

Speaking on The Adviser Live webcast yesterday (21 March) for the Leadership Series – the Changing Lending Landscape,

leading non-bank representatives outlined how the lending market was

changing and what brokers can do to ensure they are across all the

changes and offering solutions to their clients.

One

of the themes from the webcast was the rapid rise of near-prime

borrowers, given the reduced number of exceptions that some banks are

willing to accept.

Aaron

Milburn, director of sales and distribution at Pepper, revealed that the

fastest-growing segment of the lending market was near-prime borrowers.

Mr

Milburn said: “Near-prime lending in our industry is the

fastest-growing sector of it. A lot of near-prime [deals] used to be a

major bank deal with a credit exception on it, effectively, [but] that’s

all tightened up now.

“So

the near-prime space is our fastest-growing sector of lending at Pepper

and as an industry. We see that only growing because we see no

relaxation of credit policy at the majors… You think about the gig

economy, you think about people that are Uber drivers, or they do

Airtasker jobs at the weekend and they have been doing that for a

prolonged period of time and they can prove that. Why shouldn’t they use

that income? We see that sort of area growing and that is our

fastest-growing area.”

Mr

Milburn noted that the growing near-prime category was not just

expanding in the residential space but in the commercial space too.

, and Mal Withers has come in to run it for us, and the

near-prime sector of that credit policy, or that product, is growing

substantially fast as well.”

Mr

Milburn elaborated that the near-prime commercial borrower may be a

commercial client who has “a small default” or a “bump in the road in

the past and is trying to get back on their feet”.

“We

think that customer base is bankable, as we do in the near-prime

residential space, and we don’t think they should miss out, so that is

an area of growth for us as well,” he said.

Building

on this, Cory Bannister, VP-chief lending officer at La Trobe

Financial, said that the lender had to “re-categorise” its borrower

segments in the current environment, given the changing borrower

make-up.

He elaborated:

“We’ve even had to re-categorise almost how we determine what’s prime

and near-prime. Now, when we look at it, we look at ‘super prime’, which

we would say is probably what the banks are looking at now.

“Prime,

which is probably the loans that would have been bankable all day,

every day, which have probably slipped out [of major bank’s appetites]

and near-prime is the old traditional space, and specialist sits at the

end of that.”

Mr Bannister

concurred that the near-prime sector was a “growing sector” but added

that these were not necessarily applications that have serious credit

defaults or infringements, but instead borrowers who may have had a

“change of circumstances” such as a variable income or variable

employment.

Looking to the

future, both Mr Milburn and Mr Bannister, as well as Matt Bauld, general

manager, sales and business development at Prospa, agreed that the

non-bank sector would continue to flourish with the support of the

broker space.

Mr Bannister

concluded that he believed broker market share could reach 66 per cent

in the next year, adding: “I think we will see the non-bank market share

continue to grow… I think you’re seeing more of the bank simplification

strategies playing out, more products being exited, [so] non-banks are

doing more of the lifting now to try and provide more solutions.

“The overall credit tightening, I don’t see that being retraced any time soon, that zero exceptions policy is starting to bite.”

“I

think it will be some time before we see the major banks’ credit

policies change. I think it’s going to increase the broker market share

and increase the non-bank market share,” he said.

Mr

Milburn agreed, stating: “I think non-bank share will continue to grow…

the near-prime market, whether that be residential or CRE, is going to

continue to grow out because the major banks aren’t moving their credit

policy in line with the changing world… The number of exceptions to that

major bank policy now are reducing. So near-prime, near near-prime or

super prime, those sections will continue to grow out because the majors

aren’t willing to see individuals as individuals.”

Mr

Milburn continued to suggest that several banks “do not have a

near-prime product, they do not have a specialist product and they are

not there for when customers go into times of hardship. We are. And

that’s the beauty of the non-bank space, we are there for Australians

who are undervalued and underserved by the major banks, and we will

continue to grow that out.”

Speaking

from an SME lender perspective, Mr Bauld added that non-banks would

also grow in this space as brokers continue to diversify into this

space.

Mr Bauld said: “We

have literally scratched the service of a $20-billion-plus market, so

there is massive room for continued growth, that’s why we absolutely

implore brokers to look at this space and think ‘OK, how do we get

involved?’ We will absolutely help them get involved…

“[So],

there is a massive opportunity for the intermediated market, but they

have to seize it. They really have to future-proof their business. And

if they do, there is a huge and massive opportunity ahead,” he said.

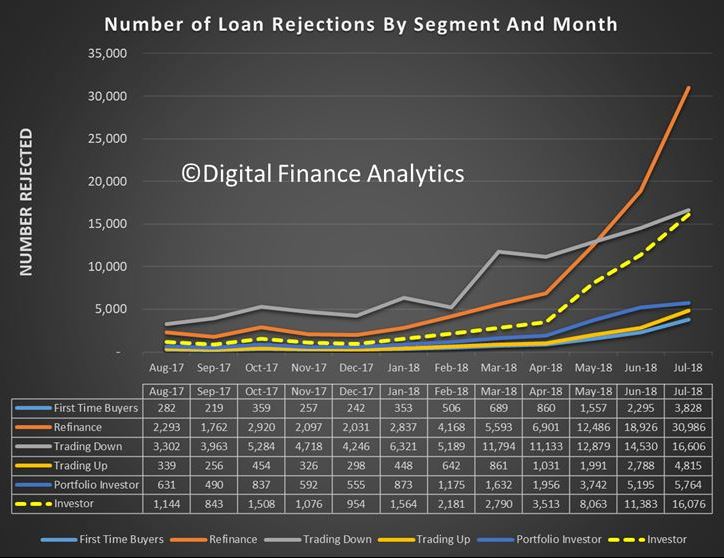

DFA research was featured in a number of the weekend papers, discussing the rising number of mortgage loan applications which are being rejected by lenders due to tighter lending standards, meaning that many households are unable to access the low refinance rates currently on offer.

NEARLY half of all homeowners are now shackled to their mortgage, with refinance rejections up significantly cent in less than a year as banks rattled by the royal commission drastically tighten borrowing rules.

Loan sizes are being slashed by 30 per cent, trapping many financially stressed customers including some who have been slugged with “out of cycle” interest rate rises. House hunters are also being hit by the credit crunch, with dramatic implications for property markets. The crunch stems from two big shifts in the way banks judge borrowers.

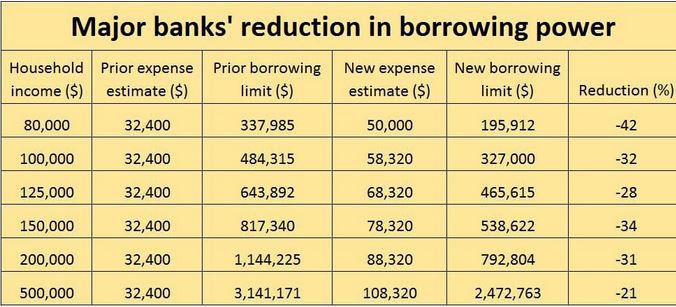

Expense estimates have been raised substantially — the minimum outgoings for an average household are now assumed to be a third higher, according to bank analysts UBS.

On top of this, granular cost breakdowns must be provided. After the royal commission revealed in March that expense checks were so lax as to be borderline illegal, new tests have been imposed requiring in some cases detail of weekly, fortnightly, monthly, quarterly and annual spending in as many as 37 categories from alcohol and haircare to shoes and pets, as well as doctor visits.

As a result, we think that now four in 10 households would now have difficulty refinancing. That means you are basically a prisoner in the loan you’ve currently go. This is based on our 52,000 household surveys plus data from a range of official sources. We estimate that 31,000 households’ refinance applications were rejected in July versus 2,300 in August last year.

Comparison service Mozo’s lending expert Steve Jovcevsk said . “There’s such a huge pool of people who are in that boat.” The most common motivation among those seeking to refinance was to save money by finding a better deal. Many were feeling the pinch because living costs were rising faster than wages and rates on interest-only or investment loans had increased.

The main issue these households are facing in seeking a new deal was banks’ definition of a “suitable loan now is different to six months ago because of the royal commission” and a clampdown by the Australian Prudential Regulation Authority. So there has been a big rise in loan rejections, particularly refinancing.

The borrowing power of hosueholds are being crimped, as shown on the banks website mortgage calculators. Those calculators, compared to a year or 18 months ago, are now on average showing a 30 per cent lower number. For some, the reduction in borrowing power is even greater. The head of UBS’s bank analysis team Jon Mott said that for a household with pre-tax income of $80,000 would get 42 per cent less from a bank; for a $150,000-a-year household, would get 34 per cent less.

Mozo’s Mr Jovcevski said in one example he was personally aware of, a person pre-approved to borrow $630,000 last year was recently offered just $480,000. The would-be borrower’s job and income hadn’t changed.

The implications for property markets were severe, Mr Jovcevski said. “There are fewer qualified buyers,” Reduced borrowing power would drag down selling prices and eventually cut valuations.

“It’s a double whammy for those mortgage prisoners,” Mr Jovcevski said. “Their valuations come in lower so their equity may end up being less than 20 per cents so they have to pay lenders mortgage insurance again” if they refinance.

Australian Banking Association CEO Anna Bligh said banks had to make reasonable inquiries to satisfy APRA’s strengthened mortgage lending standards but she said the term ‘home loan prisoners’ does not represent the facts of a fiercely competitive home loan market where everyday banks are seeking to attract new customers.

Mozo’ Jovcevski said homeowners seeking to give themselves the best chance of successfully refinancing should reduce their expenses in the months prior to applying and ensure all bills have been paid on time.

Mark Hewitt — general manager of broker and residential at AFG which arranges 10,000 home loans a month — said would-be borrowers whose budgets were at breaking point or beyond could still get a loan if they had equity, a clean repayments history and the ability to ditch key expenses such as fees for private school if under the pump.

Some people seeking their first home loan are signing documents in which they promise to cut their spending if a new loan is approved.

“When you get a mortgage you make sacrifices — you continue some of your discretionary spending but not all of it,” said Brett Spencer, head of Opica Group, which sells software to brokers that works out how much a prospective customer can cut back.

A figure is agreed between the broker and the would-be borrower which is then provided to the bank, which would otherwise rely on the higher, raw expense figures.

This makes in interesting point, mortgage brokers will be diving into household expenses more than ever before, but of course, household saying they will cut their expenses to get a loan is not the same a clear cash flow.

Thus even in this tighter market, the industry is still trying to find ways to bend the affordability rules. And it’s worth remembering that according to the latest figures from APRA more than 5% of new loans currently being written are outside standard assessment criteria.

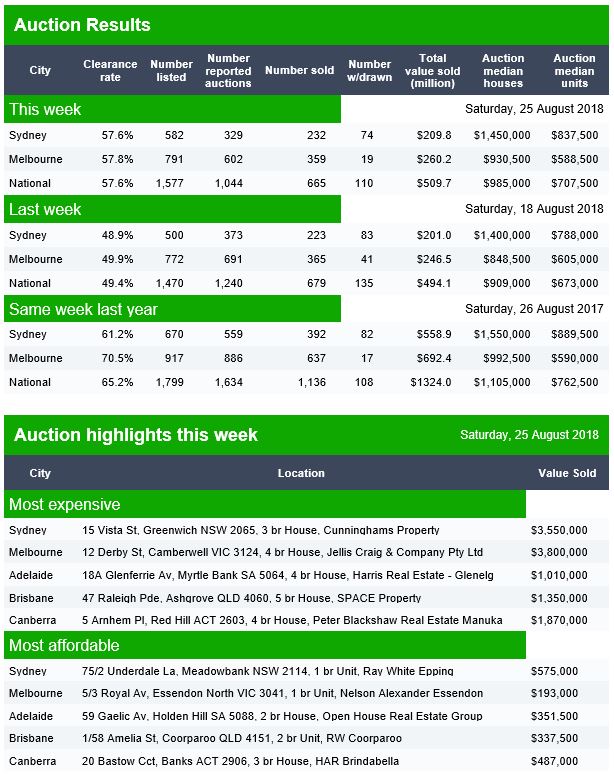

This suggests that even now; bank lending standards are still too lose. All this points to more home prices falls ahead. This is reinforced by the latest Domain auction clearance rate data which was released yesterday, and shows that the final auction clearance rate last week in Sydney, Melbourne and Nationally ended up below 50% way lower on both volume and clearance rates than a year ago.

Yet despite all this, some are still sprooking the market, saying it’s a great time to buy. We do not agree.

Investment guru Warren Buffet wasn’t commenting on the Australian mortgage market when he said, “Only when the tide goes out do you discover who has been swimming naked”, but it is no less relevant.

Key points:

42 per cent of home loan customers told banks they had incomes in excess of $500,000 last year

Westpac is the first bank to face ASIC court action over irresponsible lending allegations

Mortgage contracts can be voided if the bank provides credit to someone who cannot afford it

When interest rates start rising and/or if property prices fall, the market’s vulnerabilities will be exposed.

The prospect of higher interest rates is considered a distant threat because inflationary pressures will take time to build.

We also know households are sitting on a mountain of property debt and one false interest rate move by the RBA could trigger a collapse with far-reaching consequences.

That isn’t the only trigger.

Overstated income

The banks’ Achilles heel — irresponsible lending — is shaping up as a major threat to the banks and financial system, depending on the outcome of the banking royal commission and a low-profile battle currently being waged in courts.

“Irresponsible lending is endemic in Australia,” Digital Finance Analytics director Martin North said.

“More than 900,000 households are already in mortgage stress.

“We’re seeing a lot of households who are actually getting loans that are five, six, seven, eight, nine times income and that is astronomically high and in my mind will lead to grief later.”

Even though customers of the big four banks are representative of the Australian population, their claims about the incomes of those customers are not.

“The free and loose lending standards that banks have demonstrated, particularly over the last decade through the use of benchmarking tools and interest only loans, has the potential to be catastrophic for the Australian economy,” Maurice Blackburn lawyer Josh Mennen said.

Financial planning crisis, money laundering scandals, market manipulation … you ain’t seen nothing yet.

CBA has today revealed a raft of changes including LVR caps and restrictions to rental income for serviceability that will impact mortgage brokers and their clients from next week.

On Saturday (2 December) CBA will introducing a new Home Loan Written Assessment document called the Credit Assessment Summary (CAS) for all owner occupied and investment home loan and line of credit applications solely involving personal borrowers.

“These changes further strengthen our responsible lending commitments related to the capture and documentation of customer information,” the bank said.

“The CAS will present a summary of the information you provided on behalf of your borrower(s) and / or that the Bank has verified (where relevant) and used to complete its credit assessment.”

It will include a summary of loan requirements and objectives, personal details and financial information, total monthly living expenses at a household level and information about the credit applied for.

CBA said the CAS will form part of the loan offer document packs for all owner occupied and investment home loan and line of credit applications.

“The CAS will not be issued for Short Form Top Up applications or applications involving non-person applicants (i.e. Trust or Company). The Document Checklist, which is on the last page of the Covering Letter to Borrower (Full Pack), will indicate when a CAS has been issued,” the group said.

“An application exception will be raised if the CAS is not returned or not signed by all personal borrowers. The application will not progress to funding until the exception is resolved.”

LVR and postcode restrictions

Meanwhile, CBA confirmed that it will introduce credit policy changes for certain property types in selected postcodes from Monday 4 December.

The changes include reducing the maximum LVR without LMI from 80 per cent to 70 per cent, reducing the amount of rental income and negative gearing eligible for servicing and changing eligibility for LMI waivers including all Professional Packages and LMI offers for customers financing security types in some postcodes.

“We continue to lend in all postcodes across Australia,” CBA said.

However, on Monday the bank will also introduce what it has called the Postcode Lookup Tool, which will be available under the Tools and Calculators section on CommBroker.

“This tool will provide you with detail on policies that may apply in certain areas. You should use this tool during your customer discussions to understand policies that may apply to postcodes in which they have expressed a home lending need. If policies apply, you should discuss these with your customers,” the bank said.

The chairman of the prudential regulator has called on the finance industry to “devote more effort to the collection of realistic living expense estimates from borrowers” and give “greater thought” to the appropriate use and construct of benchmarks.

Speaking at the Australian Securitisation Forum 2017 on Tuesday (21 November), the chairman of the Australian Prudential Regulation Authority said that the regulator had been “increasingly focused on actual lending practices” and “confirmed there is more to do… to improve serviceability measures, particularly in relation to the assessment of living expenses and the identification of a borrower’s existing debts” to ensure that borrowers can afford their mortgages.

Chairman Wayne Byres told delegates that it was “no secret” that the regulator had been “actively monitoring housing lending by the Australian banking sector over the past few years” in a bid to “reinforc[e] sound lending standards in the face of strong competition that… was producing an erosion in lending quality just at a time when standards should be going in the other direction”.

Noting that mortgages represent more than 60 per cent of total lending within the banking sector, My Byres said that APRA’s goal is to ensure that regulated lenders are “making sound credit decisions which are appropriate, individually and in aggregate, in the context of broader housing market and economic trends”.

The chairman said: “We have consistently called out a number of factors that are contributing to an environment of heightened risk, many of which have been with us for quite some time now. Household indebtedness is high; perhaps more importantly, the trajectory is clearly for it to rise further.”

Mr Byres pointed to figures that show that the housing debt-to-income ratio is near 200 per cent — an all-time high.

“This trend is underpinned by a sustained period of historically low interest rates, subdued income growth and high house prices,” Mr Byres warned. “Combined, they describe an environment in which lenders need to be vigilant to ensure that their policies and practices are both prudent and responsible.

“In short, heightened risk requires heightened vigilance: certainly by APRA, but also — and preferably — by lenders (and borrowers) themselves.”

The APRA chairman said that while APRA’s crackdown on interest-only loans has been helping moderate this type of lending, he warned that there were still metrics that continue to “track higher than [what] intuitively feels comfortable”.

Question of reliability of HEM as a ‘realistic’ benchmark

One such metric was non-performing loans, which Mr Byres said were growing at an overall rate that was “drifting up towards post-crisis highs, without any sign of crisis”.

As such, the regulator is paying “particular attention” to lending to those with a low net income surplus (NIS), those who are “vulnerable to shocks”. According to APRA, NIS lending relies on the lender’s assessment of the surplus income borrowers would likely have left over each month, after taking into account living expenses, debt repayments and adding in some buffers.

“Over recent years, we have been challenging lenders to ensure that their serviceability methodology is robust, and includes adequate conservatism to ensure that borrowers are not unduly exposed if their circumstances were to change,” the chairman said.

Mr Byres went on to state that while the upward trend in low NIS lending “appears to have moderated over the past few quarters”, there is still a “reasonable proportion of new borrowers [who] have limited surplus funds each month to cover unanticipated expenses or put aside as savings”.

He therefore highlighted that as measures of NIS are dependent on the quality of the lenders’ assessment of borrower living expenses, if those expenses are “understated”, then measures of NIS are “overstated”.

Touching on the fact that many banks use the Household Expenditure Measure (HEM) as a benchmark of living expenses, Mr Byres echoed thoughts from the broking industry that this benchmark actually paints a “modest level of weekly household expenditure”.

He called on lenders to do more to ascertain a borrower’s expenses, saying: “It is open to question whether, even if it is higher than a borrower’s own estimate, such a benchmark always provides a realistic assessment of a borrower’s genuine expenditure needs.

“From APRA’s perspective, we would like to see the industry devote more effort to the collection of realistic living expense estimates from borrowers and give greater thought to the appropriate use and construct of benchmarks in instances where those estimates are deemed insufficient.”

Several banks have already introduced tighter policies around expenditure, with AMP announcing that it would not progress loan applications if it did not include a new monthly living expenses form, which covers both basic living and discretionary living expenses.

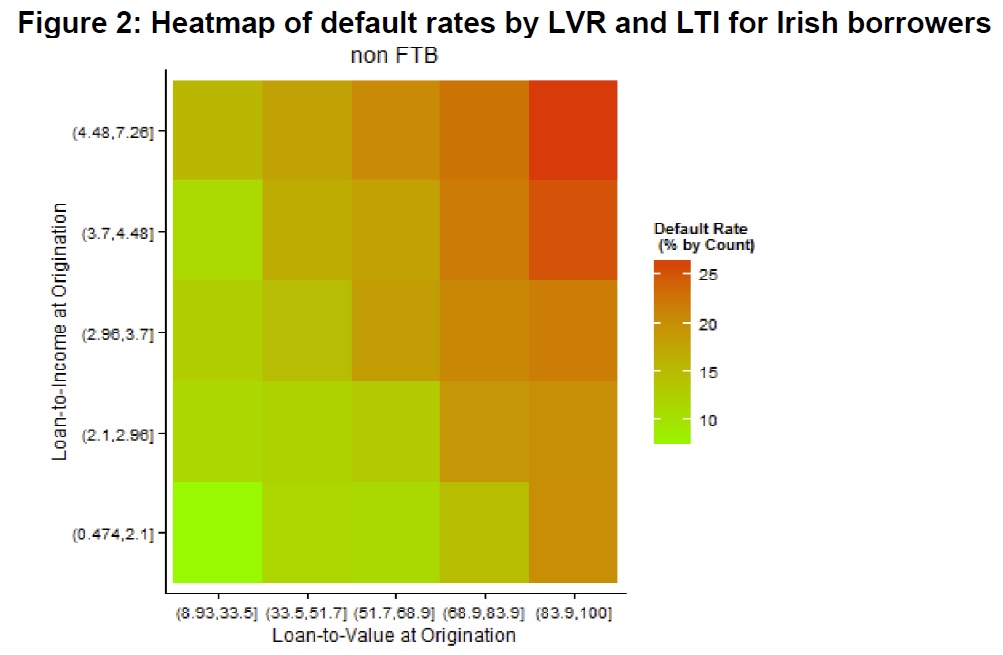

The APRA chairman also called out the fact that there had only been a “slight moderation” in the proportion of borrowers being granted loans that represent more than six times their income (which would require borrowers to commit more than half of their net income to repayments if interest rates return to their long-term average of just over 7 per cent). He also warned that “high LTI lending is well north of what has been permitted in other jurisdictions grappling with high house prices and low interest rates, such as the UK and Ireland”.

Lastly, Mr Byres highlighted that while lenders utilise a loan-to-income ratio to understand the extent to which a borrower is leveraged, he said that this can be problematic as it does not capture a borrower’s total debt level.

He therefore outlined his belief that the introduction of mandatory comprehensive credit reporting (CCR) from next year will help “strengthen credit assessment and risk management” as it will enable lenders to see a borrower’s full financial commitments, including those from others financial institutions (which has previously been “something of a blind spot” for lenders).

The APRA chairman said: “[T]he government’s recent announcement of mandatory comprehensive credit reporting beginning from next year will facilitate a switch from LTI to debt-to-income (DTI) metrics and strengthen credit assessments and risk management. This will undoubtedly be a positive development for the quality of credit decisions.”

APRA will ‘devote a large portion of supervisory resources to housing’ in 2018

Mr Byres conceded that APRA has “certainly been more interventionist than [it]would normally wish to be”, but added that as risk within the lending environment has increased, he believed the regulator’s actions have “helped to strengthen lending standards to compensate”.

He said: “We will need to continue to devote a large portion of our supervisory resources to housing in 2018. The broader environment of high and rising leverage, encouraged by historically low interest rates, requires ongoing prudence. It is easy to run up debt, but far harder to pay it back down when circumstances change.

“It is in everyone’s long-term interest to maintain sound standards when times are good – that is, after all, when most bad loans are made. Moreover, sound lending standards are an essential foundation on which the health of the Australian financial system is built, regardless of whether the loans are held on balance sheet, or securitised and sold.”

The NZ Reserve Bank has released its consultation paper on possible DTI restrictions. The 36+ page report is worth reading as it sets out the risks ensuring from high risk lending, leveraging experience from countries such as Ireland.

Interestingly they build a cost benefit analysis, trading off a reduction in the costs of a housing and financial crisis with a reduction in the near-term level of economic activity as a result of the DTI initiative and the cost to some potential homebuyers of having to delay their house purchase.

Submissions on this Consultation Paper are due by 18 August 2017.

In 2013, the Reserve Bank introduced macroprudential policy measures in the form of loan to-value ratio (LVR) restrictions to mitigate the risks to financial system stability posed by a growing proportion of residential mortgage loans with high LVRs (i.e. low deposit or low equity loans). This increase in borrower leverage had gone hand-in-hand with significant increases in house prices, particularly in Auckland. The Reserve Bank’s concern was the possibility of a sharp fall in house prices, in adverse economic circumstances where some borrowers had trouble servicing loans. Such an event had the potential to undermine bank asset quality given the limited equity held by some borrowers.

The Reserve Bank believes LVR restrictions have been effective in reducing the risk to financial system stability that can arise due to a build-up of highly-leveraged housing loans on bank balance sheets. However, LVRs relate mainly to one dimension of housing loan risk. The other key component of risk relates to the borrower’s capacity to service a loan, one measure of which is the debt-to-income ratio (DTI). All else equal, high DTI ratios increase the probability of loan defaults in the event of a sharp rise in interest rates or a negative shock to borrowers’ incomes. As a rule, borrowers with high DTIs will have less ability to deal with these events than those who borrow at more moderate DTIs. Even if they avoid default, their actions (e.g. selling properties because they are having difficulty servicing their mortgage) can increase the risk and potential severity of a housing related economic crisis.

While the full macroprudential framework will be reviewed in 2018, the Reserve Bank has elected to consult the public prior to the review. This consultation concerns the potential value of a policy instrument that could be used to limit the extent to which banks are able to provide loans to borrowers that are a high multiple of the borrower’s income (a DTI limit). A number of other countries have introduced DTI limits in recent years, often in association with LVR restrictions. In 2013, the Bank and the Minister of Finance agreed that direct, cyclical controls of this sort would not be imposed without the tool being listed in the Memorandum of Understanding on Macroprudential Policy (the MoU). Hence, cyclical DTI limits will only be possible in the future if an amended MoU is agreed.

The purpose of this consultation is for the Reserve Bank, Treasury and the Minister of Finance to gather feedback from the public on the prospect of including DTI limits in the Reserve Bank’s macroprudential toolkit.

Throughout the remainder of the document we have listed a number of questions, but feedback can cover other relevant issues. Information provided will be used by the Reserve Bank and Treasury in discussing the potential amendment of the MoU with the Minister of Finance. We present evidence that a DTI limit would reduce credit growth during the upswing and reduce the risk of a significant rise in mortgage defaults during a subsequent severe economic downturn. A DTI limit could also reduce the severity of the decline in house prices and economic growth in that severe downturn (since fewer households would be forced to sharply constrain their consumption or sell their house, even if they avoided actual default). The strongest evidence that these channels could materially worsen an economic downturn tends to come from countries that have experienced a housing crisis in recent history (including the UK and Ireland). The Reserve Bank believes that the use of DTI limits in appropriate circumstances would contribute to financial system resilience in several ways:

– By reducing household financial distress in adverse economic circumstances, including those involving a sharp fall in house prices;

– by reducing the magnitude of the economic downturn, which would otherwise serve to weaken bank loan portfolios (including in sectors broader than just housing); and

– by helping to constrain the credit-asset price cycle in a manner that most other macroprudential tools would not, thereby assisting in alleviating the build-up in risk accompanying such cycles.

The policy would not eliminate the need for lenders and borrowers to undertake their own due diligence in determining that the scale and terms of a mortgage are suitable for a particular borrower. The focus would be systemic: on reducing the risk of the overall mortgage and housing markets becoming dysfunctional in a severe downturn, rather than attempting to protect individual borrowers. The consultation paper notes that DTIs on loans to New Zealand borrowers have risen sharply over the past 30 or so years, with further increases evident since 2014. This partly

reflects the downward trend in interest rates over the period. However, interest rates may rise in the future. While the Reserve Bank is continuing to work with banks to improve this data, the available data also show that average DTIs in New Zealand are quite high on an international basis, as are New Zealand house prices relative to incomes.

Other policies (such as boosting required capital buffers for banks, or tightening LVR restrictions further) could be used to target the risks created by high-DTI lending. The Bank does not rule out these alternative policies (indeed, we are currently undertaking a broader review of capital requirements in New Zealand) but consider that they would not target our concerns around mortgage lending as directly or effectively. For example, while higher capital buffers would provide banks with more capacity to withstand elevated housing loan defaults, they would do little to mitigate the feedback effects between falling house prices, forced sales and economic stress.

The Reserve Bank has stated that it would not employ a DTI limit today if the tool was already in the MoU (especially given recent evidence of a cooling in the housing market and borrower activity), it believes a DTI instrument could be the best tool to employ if house prices prove resurgent and if the resurgence is accompanied by further substantial volumes of high DTI lending by the banking system. The Reserve Bank considers that the current global environment, with low interest rates expected in many countries over the next few years, tends to exacerbate the risk of asset price cycles arising from ‘search for yield’ behaviour, making the potential value of a DTI tool greater.

The exact nature of any limit applied would depend on the circumstances and further policy development. However, the Reserve Bank’s current thinking is that the policy would take a similar form to LVR restrictions. This would involve the use of a “speed limit”, under which banks would still be permitted to undertake a proportion of loans at DTIs above the chosen threshold. By adopting a speed limit approach, rather than imposing strict limits on DTI ratios, there would be less risk of moral hazard issues arising from a particular ratio being seen as “officially safe”. Exemptions similar to those available within the LVR restriction policy would also be likely to apply.

Most Australian banks are facing a one or two notch rating downgrade over the next two years as rising residential property prices put financial institutions at risk.

In a commentary on Australian banks entitled Rising Economic Risks Could Cut Ratings on Most Australian Financial Institutions by One Notch, S&P Global Ratings has examined the dangers of Australia’s hot housing market.

Rising economic imbalances are increasing the risk of a sharp correction in property prices, analysts at the global ratings agency said.

If such a scenario occurs, S&P highlighted eight financial institutions (including six banks) which would incur large credit losses and a subsequent credit rating downgrade.

S&P makes these ratings adjustments by focusing on the Risk Adjusted Capital (RAC) Framework.

“Our risk weights applicable to a bank’s loans are calibrated to the economic risk we see in the country. Consequently, as economic risks in a country rise in our opinion, we increase the risk weights, and that pushes down the capital ratios,” Sharad Jain, director at S&P Global Ratings, told Australian Broker.

“This in turn, could have an additional downward impact on bank ratings. This is because our risk adjusted capital ratios are a key driver of our capital and earnings assessment – which is an analytical factor in our assessment of a bank’s rating.”

In the event of rising economic risks facing banks in a particular country, this by itself would be enough to place pressure on bank ratings within that country, he said.

S&P expects property price growth to moderate and then remain at relatively low levels during the next 12 to 18 months.

However, analysts warned there is a one-in-three chance of a ‘downside scenario’ occurring in which property prices spiked. The resultant rise in risk would weaken the capital ratios of all banks in Australia.

For most banks, this movement would not be enough to put further pressure on their credit profiles. Thus, most financial institutions would only be downgraded by one notch.

However, S&P Global gave a warning about eight Australian financial institutions, highlighting two banks – Auswide Bank and MyState Bank – as being at greatest risk in this ‘downside scenario’.

“It is important to point out that, if our downside scenario materialises, to review our ratings on these institutions, we would make an assessment of their position and plans in relation to capital, business, and broader financial profile,” Jain said.

“A two-notch downgrade would be only one of the three likely outcomes in that scenario. The other two likely outcomes are a one-notch downgrade with stable outlook or a one-notch downgrade with a negative outlook.”

S&P Global also warned about the risks posed for AMP Bank, HSBC Bank Australia, ME Bank and P&N Bank in these circumstances although the agency admitted that parent support from these institutions is highly likely to prevent a two notch downgrade.

As reported by the ABC, ASIC says it has been investigating up to 11 banks over their home lending practices, amid concerns loans are being given to people that cannot afford to repay them.

Appearing before Senate Estimates, the Australian Security and Investments Commission (ASIC) was questioned about its Federal Court action against Westpac, announced yesterday.

ASIC’s senior executive responsible for banking, Michael Saadat, said the inquiries have been underway for a couple of years.

“It started really when we conducted our review of interest only loans in 2015,” he said.

“We looked at the conduct of 11 lenders.

“We have announced action against Westpac but we have been in discussions with other lenders and we hope to make an announcement about the work that we’ve been doing with other lenders in the next few weeks.”

Mr Saadat added that Westpac had changed its lending practices after the regulator made its concerns known in 2015.

“Despite the fact that they stopped the practice … we’ve decided to bring this action because of the importance of the issues that it raises,” he said.

Westpac not alone

It’s a fair bet all four major banks are facing ASIC scrutiny over poor home loan approval practices.

In a statement yesterday, Westpac said the loans identified by ASIC are all meeting or ahead on repayments.

However, ASIC said its action is intended to head-off possible future risks for consumers and the financial system.

“One of the aims of the responsible lending legislation is to enable ASIC to take action before the problems manifest themselves,” explained the regulator’s deputy chairman Peter Kell.

ASIC’s chairman Greg Medcraft said a key motivation for the regulator was to get other banks to change their ways.

“The issues is deterrence, and when you lodge a case it’s not just for that party, it’s to send a message to the broader sector,” he said.

ASIC said the maximum civil penalty that a court could award for breaches of the responsible lending laws is $1.7 million per contravention.

Westpac currently stands accused of seven contraventions of the law.

Westpac will defend Federal Court proceedings commenced by ASIC in relation to a number of home loans entered into between December 2011 and March 2015, including specific allegations made by ASIC regarding seven loans. The court action does not concern Westpac’s current lending policies or practices.

Of the seven specific loan applications ASIC references in its proceedings, all loans are currently meeting or ahead in repayments.

Westpac Group, Chief Executive, Consumer Bank, George Frazis said Westpac takes its responsible lending obligations seriously and has confidence in its lending standards and processes. Our objective is to help more Australian families into their homes in a responsible way.

“It is not in the bank’s or customers’ interests to put people into loans that they cannot afford to repay. It goes hand in hand that we have robust credit approval processes while helping customers purchase their home.

“Our credit policies are informed by our deep experience and understanding of the mortgage market.

“They include a consideration of customers’ specific circumstances, including income and expenditure, previous repayments history and the overall customer relationship. We build into our processes a range of conservative inputs, including the addition of buffers to take into account possible future interest rate increases.”

Mr Frazis said Westpac uses sophisticated systems as part of its rigorous credit approval process. This includes utilising benchmarks such as the Household Expenditure Measure (HEM), published by the Melbourne Institute for Social and Economic Research, which provides broad analysis of customer expenditure based on demographic criteria.

“In our experience this survey is a useful input into our loan assessment process, in combination with our understanding of customers’ circumstances.”

Westpac disputes ASIC’s claims that Westpac relied solely on the HEM benchmark and did not have regard to a customer’s declared expenses in its unsuitability assessment.

“The Australian residential market is dynamic and we are constantly reviewing and refining our credit policies.”

“Importantly, interest-only mortgages were assessed in the same way as a standard principal and interest loan, and did not increase how much a customer could borrow.

“We are committed to meeting our responsible lending obligations and servicing the needs of customers, including prompt credit approval, which enables our customers to responsibly purchase their home with confidence,” Mr Frazis said.

Blog")