ABC Lateline carried a segment featuring BrickX, which can either be seen as an innovative way to facilitate housing affordability, or the ultimate in the financialisation of property. You decide!

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

ABC Lateline carried a segment featuring BrickX, which can either be seen as an innovative way to facilitate housing affordability, or the ultimate in the financialisation of property. You decide!

Solving the affordable housing crisis is a high priority for state governments around Australia.

This is understandable given the hyper-inflated property markets in many Australian capital cities. Rising concerns that interest rates will increase over coming years also fuel the unaffordability fires.

Proposed solutions to this crisis often focus on opening up new greenfield areas of land in the outer suburbs to develop lower-cost housing. Hence the solution to the affordable housing process is often thought to lie in creating housing with a low purchase price. This approach incentivises developers and housing suppliers to keep the price of new housing stock as low as possible.

This leads to houses that are more costly to own and maintain. Construction savings on features such as insulation, passive solar design, and heating and cooling systems mean such houses have high energy demands. That, in turn, means ongoing living costs such as the cost of air conditioning remain high for the life of the house.

Such houses are also constructed to the minimum standards dictated by the building codes. Poorer design and lower-quality materials can lead to large deferred maintenance costs and lower resilience to natural hazards.

In addition, housing in the outer suburbs has poorer prospects for capital growth, effectively trapping poorer households on the fringes of our cities. The residents of these suburbs also generally face higher transport costs to get to work and services.

Exposed to future risks

We are, in effect, encouraging new home owners to take on larger future risks and costs just so they can buy a house. This keeps government happy by increasing the number of new home owners – a proxy for affordable housing.

But this approach ignores the issue that home owners increasingly cannot afford to continue to own a home, not just buy one.

Increasingly, the first cost-saving action for struggling home owners is to be uninsured or underinsured. About 14% per cent of people have no home or contents insurance whatsoever.

Of those who are insured, many know they are not adequately covered. Back in 2012 it was identified that around one-quarter of home owners and renters had no insurance cover for house contents. Other estimates suggest that nearly one-third of households in Australia remain uninsured. Other studies more recently concluded that 41% of tenants do not have contents insurance.

Events like the recent Cyclone Debbie remind us just how exposed many families are to natural hazards, including physical damage to assets and the associated emotional hardship.

In many cases, families have been financially wiped out as a result of their lack of insurance coverage. These families then go back onto the long waiting list for affordable social housing.

Therefore, by defining affordable housing in terms of only purchase price of housing and number of new home owners, we are dramatically understating the problem of housing affordability.

By facilitating families to invest in houses that require high energy demands to be liveable, and which are located in areas increasingly exposed to natural hazards while households are uninsured or underinsured, we are simply mismanaging the affordable housing challenge.

Reframing affordability

A key action that can be taken is to frame housing affordability in terms of whole-of-ownership-life costs. This means we move away from defining affordable housing in terms of the initial capital cost and instead consider the total cost of owning a house over the term of ownership.

This approach explicitly encapsulates the risks of under-insurance and higher interest rates.

This is the approach used when funding infrastructure and major utilities assets. When planning major infrastructure, cost-benefit analyses must now consider the whole-of-life costs. This is to account for enthusiastic infrastructure advocates deferring costs through to increased maintenance obligations so the capital costs remains low, and hence the project becomes more attractive.

It’s the same for housing development. Therefore, the same approach needs to be adopted for home ownership.

So the latest pivot from the Government is a focus on the “good and bad debt” as an apparent key to growth, with housing affordability now becoming more of a side show as the realisation dawns that they cannot solve that equation. This segment discusses the issue, and includes a contribution from DFA.

From Mortgage Professional Australia.

Moody’s report shows regulatory crackdowns and low-interest rates will not protect affordability, putting pressure on Government to take action in the Budget

![]()

Housing affordability is deteriorating in Australia despite the impact of regulatory crackdowns and low interest rates, a report by international ratings agency Moody investors Service has found.

Affordability worsened in the year to March 2017, with interest repayments requiring for 27.9% of household income on average, compared with 27.6% in March 2016. Affordability declined steeply in Sydney, Melbourne and Adelaide, according to the report, although it improved in Brisbane and Perth, which is currently the most affordable city in Australia, with the proportion of income going to repayments at 19.9%.

Moody’s expect that housing affordability will continue to deteriorate, blaming “rising housing prices, which outstripped the positive effects of lower interest rates and moderate income growth”. Whilst APRA’s restrictions on interest-only mortgage lending could dampen demand for apartments they could also reduce affordability, Moody’s claims: “the new regulatory measures have prompted some lenders to raise interest rates on interest-only and housing investment loans, which will make such loans less affordable.”

Proportion of joint-income required to meet interest repayments, March 2016:

- Sydney 37.5%

- Melbourne 30.3%

- Brisbane 23.9%

- Adelaide 23%

- Perth 19.9%

- Australia: 27.9%

Coming just weeks ahead of the 2017-18 Federal Budget, Moody’s report indicates the Government cannot rely on regulators and the RBA if it wants to improve affordability. In March Treasurer Scott Morrison said repayment affordability would play a major part in the Budget and was a bigger issue then the difficulty of first home buyers, whilst ruling out any changes to negative gearing.

In a series of sensitivity tests, Moody’s demonstrated the risks faced by Australian homeowners. Looking at the effect of house prices continuing to rise, income decreasing and interest rates increasing, Moody’s found Sydney homeowners were particularly vulnerable. A 10% rise in property values – far from unknown in the harbour city – meant an extra 3.8% of income needed to meet mortgage repayments.

Moody’s report did find that affordability was unchanged for apartments. Apartment owners spent an average of 24.5% of their income on repayments, compared to 29.3% for house owners. This is a national average: affordability of apartments did decline in Sydney and Melbourne.

Almost nothing is to be seen of Australia’s housing crisis in the latest inflation figures.

Wednesday’s Consumer Price Index (CPI) from the Australian Bureau of Statistics showed just a 0.5 per cent increase in inflation this quarter, up 2.1 per cent over the past 12 months.

Over the same period, house prices grew 1.4 per cent, and by 75 per cent over the past five years.

The biggest increases in the CPI were in fuel, healthcare, power and, yes, housing.

However, as pointed out recently by Commonwealth Bank senior economist Gareth Aird, this ‘housing’ figure, which accounts for 22 per cent of the CPI calculation, does not truly reflect the struggle of many Australians to get onto the property ladder.

“The CPI is a poor barometer of changes in the cost of living for people who don’t own a dwelling and aspire to purchase one,” Mr Aird wrote.

That’s because the CPI measure of ‘housing’ only counts rents, utilities and the cost of building a new dwelling. It doesn’t include the cost of the land the dwelling sits on. And it doesn’t include the interest costs of repaying a mortgage.

If the full cost of housing was factored in, Mr Aird estimated it would add roughly 55 percentage points to headline inflation.

As mentioned above, the CPI ‘housing’ measure also doesn’t include interest charges. It used to, but they were removed in 1998 after lobbying from the Reserve Bank, which argued that rising mortgage interest rates would push up inflation, thereby requiring official cash rate rises, which would then push mortgage rates even higher, in a vicious loop.

The RBA said then that “excluding interest charges would in no way distort the outcome over the long run”.

Australia Institute senior research fellow David Richardson said if the CPI were to include land prices, the inflation rate would be pulled too hard by almost out of control house prices.

“Imagine if things went up 15 per cent a year in price,” Mr Richardson told The New Daily.

“Lots of contracts in Australia are indexed against the CPI. If they’re sort of fiddled then you’re talking billions and billions in consequences.”

Marcel van Kints, program manager with the Prices Branch of the ABS Macroeconomic Statistics Division, told The New Daily: “The ABS CPI aligns with international standards, an international respected measure of inflation.”

The ABS also published a FAQ with Wednesday’s release in which they pointed to their reasoning behind the exclusion of land from the CPI.

They said that housing is included in the Selected Living Cost Indexes, which are “particularly suited to assessing whether or not the disposable incomes of households have kept pace with price changes”.

Inflation outpaces wages

All of this is seeing many Australians left behind as both housing and the prices of popular consumer goods rise while wages stagnate.

Over the past 12 months, the CPI rose 2.1 per cent while wages grew by only 1.9 per cent, according to the latest ABS data.

The Australia Institute’s David Richardson said this is leaving many Australians worse off.

“I suspect that as professionals and skilled white collar workers, we’re all in the same boat,” he said.

“What we’re seeing now is a symptom of structural change that’s been creeping up on us for a long time.”

The HIA makes some good points about the need for a credible land planning body to provide national monitoring and forecasting of future land release and housing requirements to address housing affordability; but ignores the important point that supply is actually NOT the key issue, because average number of people per property has remained the same as the mortgage loan growth and house prices have risen. Other factors are at work.

Australia needs supply not demand focused solutions to address our national affordability challenges, said the Housing Industry Association.

“Attempts to remove demand for new housing will reduce supply, affordability and jobs,” said HIA’s Deputy Managing Director, Graham Wolfe.

“While several measures announced today by Labor to address Australia’s housing affordability challenges provide a sensible approach to increasing supply of new homes, others targeting demand will have an adverse impact on affordability now and into the future,” said Mr Wolfe.

“We can’t address housing affordability nationally with both eyes solely on Sydney and Melbourne,” said Mr Wolfe. “Sydney house price increases have been driven by many factors, including significant population growth, a ten-year supply recession, low interest rates and the impact of extremely high stamp duty costs on sales in the established housing market.”

“The dynamics in Perth, Adelaide, Northern Queensland and Darwin are very different. Foreign investors and self-managed superannuation fund investors cannot be blamed for the recent fall in house prices in Perth and Darwin, or the slower level of new housing activity in Adelaide. Inflicting demand side measures on these capital cities ignores the significant negative impact on housing supply, jobs and economic growth in these economies.“Right now, if foreign capital investment in Australia helped bring significant residential development projects to commencement in Perth, creating jobs and production, the Western Australian economy would be much better for it.

“Australia needs a credible land planning body to provide national monitoring and forecasting of future land release and housing requirements. The body would help to inform government policy on financing, infrastructure and demographics.“Other policies to address housing affordability must include a reduction in the imbedded taxation on new housing, government funding to support infrastructure and reforms to address unnecessary planning delays in bringing new residential developments to market.

“Our national housing affordability challenge is complex, and necessitates a national ‘cost of housing’ inquiry to identify impediments to the supply of new housing. Such an inquiry would bring together the overlapping impact of regulations, taxes and barriers imposed by all three levels of government, and importantly, inform governments in developing cohesive, integrated and responsible housing reforms, measures and programs,” concluded Mr Wolfe.

Labor will promise to ban direct borrowing by self-managed superannuation funds, as part of a housing affordability policy released on Friday to pre-empt the government’s package in next month’s budget.

This “limited recourse borrowing” – where a creditor has limited claims on the loan if there is a default – has increased from about A$2.5 billion in 2012 to more than $24 billion. Almost all of it is in residential or commercial property.

The Murray Financial System Inquiry in 2014 recommended restoring the prohibition that had been lifted in 2007. It warned that “further growth in superannuation funds’ direct borrowing would, over time, increase risk in the financial system”.

Among other measures, a Shorten government would double the screening fees on foreign investment and financial penalties that apply to foreign investment in residential real estate. Foreign investment purchases nearly tripled over the three years to 2014-15. The ALP says the higher fees and penalties would “help level the playing field between first home buyers and property speculators”.

The centrepiece of the ALP housing policy remains the changes to negative gearing and the capital gains tax discount that Labor took to the election, but the latest package surrounds those with several other initiatives.

The opposition announcement comes as the government’s expenditure review committee struggles to stitch together a credible package, and after a much-publicised split among ministers over whether first home buyers should be able to use their superannuation for housing. Malcolm Turnbull last week apparently ruled that option out.

Labor says its package would see the construction of more than 55,000 new homes over three years and increase employment by 25,000 new jobs a year.

The ALP would establish a Council of Australian Governments process to achieve a more efficient and uniform vacant property tax across the main cities.

It would provide $88 million over two years for a new Safe Housing Fund for transitional accommodation for victims of domestic violence, vulnerable young people and older women at risk of homelessness. This would restore cuts made by the Coalition in the 2014 budget.

It would also work with state governments to get better outcomes in the National Affordable Housing Agreement. And it would establish a bond aggregator to increase investment in affordable housing – something the government is moving towards.

Labor would also re-establish the national Housing Supply Council and re-instate a minister for housing, the policy says.

It says that “any housing affordability package that doesn’t involve reforms to negative gearing and the capital gains tax discount is a sham”.

“Demand for housing is being turbo-charged by unfair, unsustainable and distortionary tax concessions for investors.” The ALP’s long standing policy is to limit future negative gearing to new housing and reduce the capital gains tax discount from 50% to 25%.

Labor says the super funds’ ban “will prevent the unnecessary buildup of risk in Australia’s superannuation system, reduce future calls on the aged pension as a result of a less diversified superannuation system and make the financial system more resilient in the face of potential economic shocks”.

It says that although foreign purchases in residential real estate account for a relatively small amount of overall annual purchases, the amount has grown by 275% in the three years to 2014-15.

Under the Labor policy, from July 1 2019 the foreign investment application fee would go from $5000 to $10,000 for a property up to $1 million; from $10,100 to $20,200 for one between $1 million and $2 million, and from $20,300 to $40,600 for one between $2 million and $3 million.

For foreign buyers who acquired dwellings without approval, the criminal penalty would be increased to $270,000, and $1.35 million for a company.

Author: Michelle Grattan, Professorial Fellow, University of Canberra

From The Real Estate Conversation.

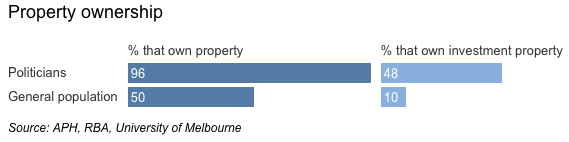

Many of the federal politicians tasked with fixing Australia’s intractable housing affordability problems are significant property investors themselves, according to findings from an investigation by the ABC.

The study, which looked at data from Parliament’s registers of interests, shows that at least 95 per cent of our elected federal members own at least one property; this compares with a home ownership rate for the general population of around 50 per cent, according to the ABC.

Source: the ABC.

Many of the politicians deciding if property investment should be tax advantaged are significant property investors themselves. Of our 226 federal politicians, approximately half own at least one investment property – and a number owning significantly more. Only approximately 10 percent of the general population are property investors.

National Party senator Barry O’Sullivan has the largest portfolio, with 33 properties.

And which party owns the greatest number of properties? The Coalition, with 295 properties, compared with Labor’s 193 properties.

Source: the ABC.

The study didn’t include properties wholly owned by politician’s spouses.

Deloitte Access Economics’ Chris Richardson recently suggested that young Australians would be better off renting than trying to buy a house. He argued:

… rents today make a lot more sense than housing prices.

This may be true. However, the situation for renters is far from clear-cut. Rents continue to increase in Australian cities, and are out of reach for low- and very-low-income earners.

Renters also face substantial housing insecurity. In Australia, 50% of renters are on a fixed-term one-year lease; 20% are on a month-to-month “rolling” lease.

For renting to become a truly viable, long-term alternative to home ownership, greater rental affordability and security is needed.

Longer-term structural changes to tackle housing affordability, including boosting the supply of social housing and increasing tenure diversity, will be essential. There are some promising moves, including the recently announced proposal for a bond aggregator model to fund social and affordable housing.

Failing a substantial increase in affordable housing, there will be a need to increase rent assistance payments, particularly in high-cost regions.

This acknowledges that housing costs differ across the country and that many low-income earners need to remain in high-cost regions. This includes older people whose social and family networks are in these regions, and people who work in these areas.

Many industries in high-cost cities are dependent on people who earn low and very-low incomes. These people have a right – and need – for affordable, secure housing – and a house that is a home.

For renting to become a true alternative to home ownership, greater rental security is needed.

To move toward secure rentals we need to reward long-term investment. One example might include encouraging institutional investors, including superannuation companies and other businesses that invest in large amounts of rental housing, who are in it for the long haul.

However, there is no reason to assume that institutional investors will offer more affordable rental properties, or be any better landlords than so-called “mum and dad” investors. We therefore need to pursue changes to rental laws to ensure renters, including the growing generation of long-term renters, can experience a secure sense of home. Specific changes include:

Removing no-grounds eviction. The perceived risk of eviction leads to stress for renters. And the right to no-grounds eviction can lead to retaliatory eviction by landlords when tenants exercise their rights, including rights to maintenance and repairs.

The Tenants’ Union of NSW has called for a balancing of landlord and tenant interests through tenancy laws that specify reasonable grounds for termination.

Such laws could follow the German example. In Germany, rental laws ensure security of tenancy while retaining the right of landlords to terminate a lease in certain circumstances, such as if a tenant violates the lease agreement (for example, by not paying rent) or if the landlord requires the property for personal use.

Rent increases are sometimes a “backdoor” way of evicting tenants. In a recent survey, 11% of renters reported receiving a “rent hike after requesting a repair and 10% said that their landlord or agent became angry”. We need stronger regulation of rent increases and stronger penalties for unreasonable increases.

There are precedents for this in other jurisdictions. Germany again provides a great example. There, rent increases are allowed less frequently. And they:

… must be based in the rents of three similar dwellings or a database of local reference rents and rents may not increase more than 20% over three years.

Ensuring the right to make a home. Rental laws need to ensure the right of tenants to make their house into a home, including making cosmetic changes to a property, ability to keep pets, and allowing alterations that would allow an older person or person with a disability to live there.

Some older renters I have interviewed recently have had to move after these types of adjustments were rejected by landlords who thought age-related modifications were not attractive.

In New South Wales, the right to make changes that would ensure a property is liveable for people with different housing needs is being considered as part of the current residential tenancy law review. However, the right to make cosmetic changes is excluded.

Popular wisdom often suggests that tenants and landlords have different interests. In fact, they have very similar interests. Both benefit from secure tenancies and a property that is well maintained and cared for.

Failure to ensure rental affordability and security will require a raft of policy changes in other areas, including pension income calculations that assume home ownership. It will also condemn a generation of long-term renters to increasingly unaffordable and insecure housing.

Author: Emma Power, Senior Research Fellow, Geography and Urban Studies, Western Sydney University

From The Sydney Morning Herald.

Deloitte Access Economics’ quarterly business outlook, released today, predicts the official cash rate of 1.5 per cent will climb slowly in 2018 and 2019 to reach 3 per cent in the early 2020s.

The Reserve Bank was well aware “interest rates are now a massively more potent weapon for slowing the Australian economy than they’ve ever been before”, the forecaster said.

![]()

It noted Australian families have overtaken the Danish in recent months to become the world’s second most indebted households after the Swiss, relative to income – a consequence of “dangerously dumb” house prices.

Director Chris Richardson told Fairfax Media a crisis could be averted if, as he predicted, interest rates rose slowly and steadily. But cheap credit and high leverage still posed risks.

“In global terms our housing prices are asking for trouble,” Mr Richardson said, arguing many workers have found their homes make more money each day than they do. “That’s kind of God’s way of saying: this thing’s gonna blow.”

Sydneysiders were particularly vulnerable, Deloitte found, having benefited enormously from low interest rates but now witnessing “silly prices” that continued to grow – a “rather worrying development” in Deloitte’s eyes.

“The seeds of future slowdown are already well and truly sown. The better that NSW looks now, the greater the troubles that this state is storing up for the future,” the outlook warned.

“The joy of rising wealth eventually gives way to the pain of servicing gargantuan mortgages. Interest rates are beginning to rise around the world and although official interest rates in Australia may not follow suit until 2018, that augurs badly for the disposable incomes of Sydneysiders.”

Martin North, principal of Digital Finance Analytics, expressed concern Australia could be heading for a version of the US sub-prime mortgage crisis that preceded the Global Financial Crisis.

The parallels involve spiralling household debt, stalled incomes, rising levels of mortgage stress and interest rates that are on the way up.

Mr North’s modelling shows 669,000 families (or 22 per cent of borrowing households) are in mortgage stress. That would rise to 1 million households, or one third of borrowers, if interest rates rose by 3 percentage points.

But the main factors in Mr North’s reckoning are the static nature of wages and the rising tide of under-employment.

“This falling real income scenario is the thing that people haven’t got their heads around,” he told Fairfax Media.

“Unless we see incomes rising ahead of inflation and under-utilisation dropping, any increase in interest rates is going to have a severe impact on [people’s] wallets and therefore in discretionary spending and therefore on growth.

“I have a feeling we are meandering our way, perhaps a little bit blindly, into a rather similar scenario to the US.”

Mr North said mortgage stress was not only an issue for battlers and people on the urban fringe, but increasingly affected more affluent, highly leveraged households.

He dismissed the possible solutions put forth by Treasurer Scott Morrison as “political theatre” and invoked former prime minister Paul Keating by arguing Australia may be heading for “the correction we have to have”.

“I’m not sure that there are other levers that are available,” he said.

The Deloitte report also poured scorn on cutting immigration to boost housing affordability, an idea backed by former prime minister Tony Abbott among others.