CoreLogic reported that their national Home Value Index (HVI) rose 8.1% in 2023, a significant turnaround from the 4.9% drop seen in 2022, but well below the 24.5% surge recorded in 2021. December’s 0.4% increase saw 2023 finish with a relatively soft monthly rise in home values.

Despite the annual 8.1% increase, the year was punctuated by diversity , with the annual change in housing values ranging from a 15.2% surge in Perth to a 1.6% fall across regional Victoria.

So now of course, the question is what will happen in 2024. Last week I made two shows for the channel, one on the top 5 elements supporting home price growth in 2024 and the other on the top five elements which could drive prices lower.

If you take, low supply, high demand, easing lending, Government support and RBA/APRA stability concerns, the potential for home prices, especially houses to rise in 2024 seems pretty strong. On the other hand, the risks from higher unemployment or a recession, the exit of property investors, higher delinquency and defaults, higher mortgage rates for longer, and dire housing affordability are all reasons why prices could fall in 2024.

To make an assessment of what will play out, you then have to do is to weigh the relative influence of each of these forces, against an unstable local and global economic environment.

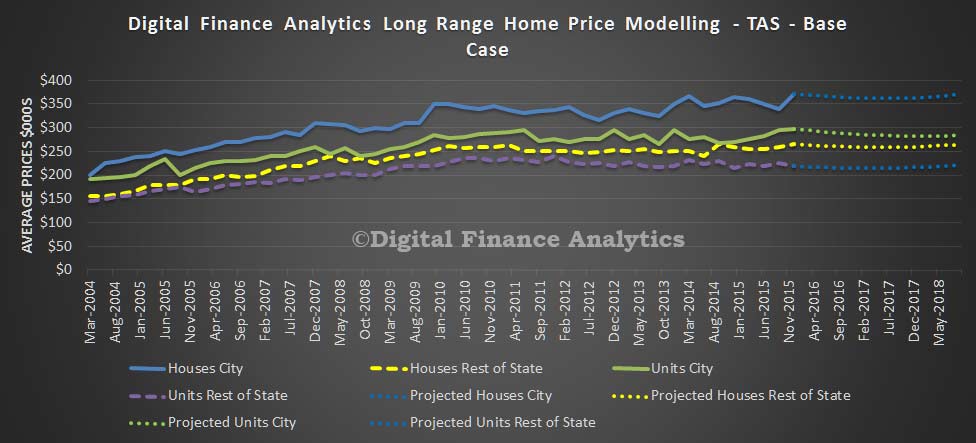

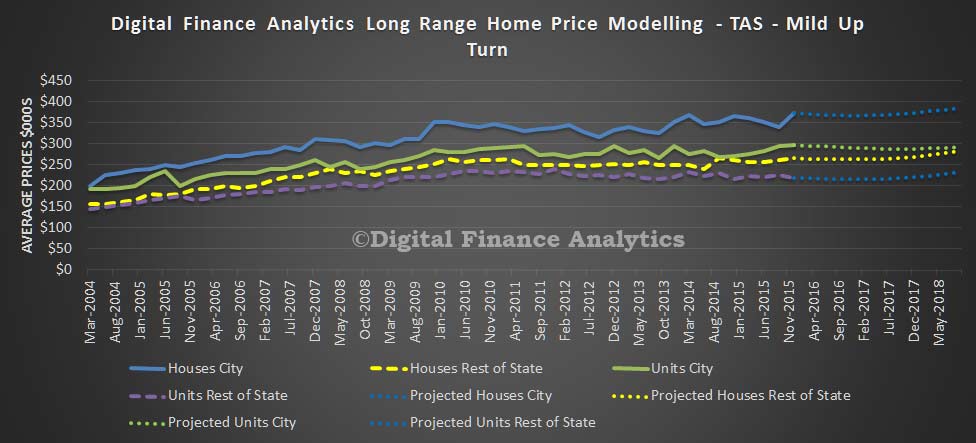

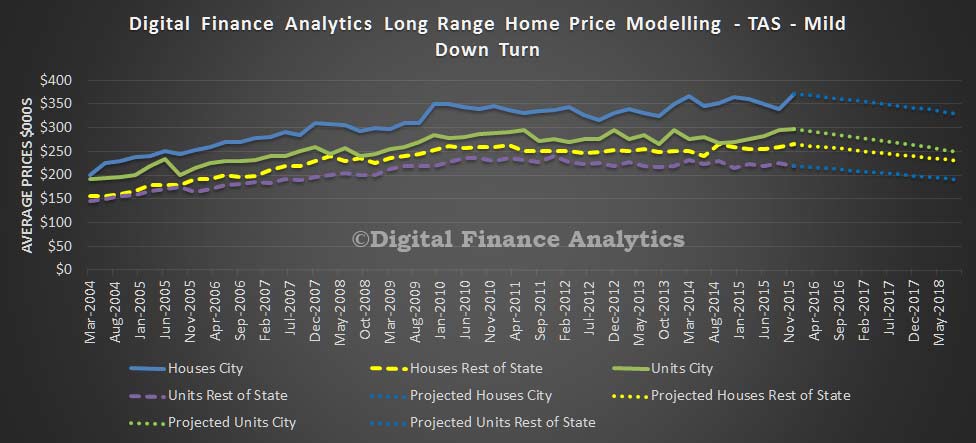

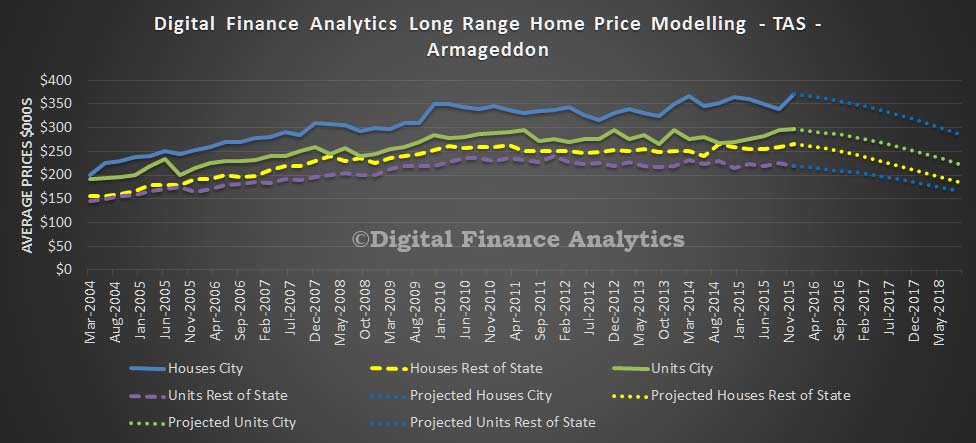

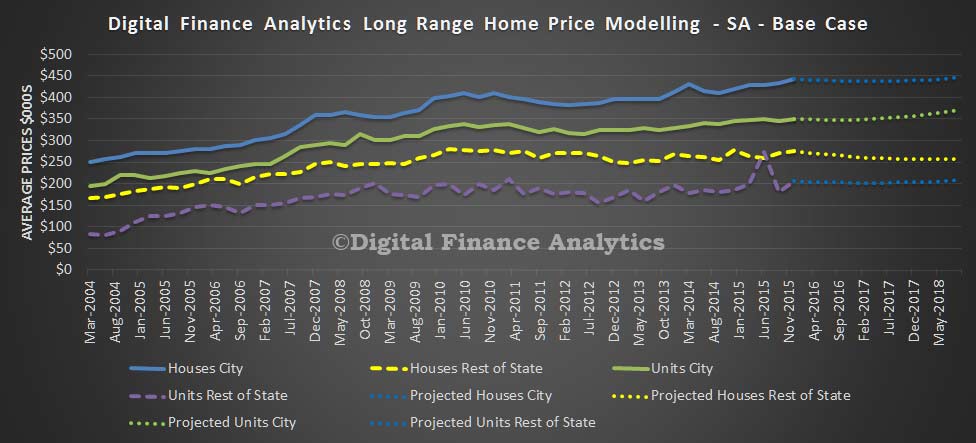

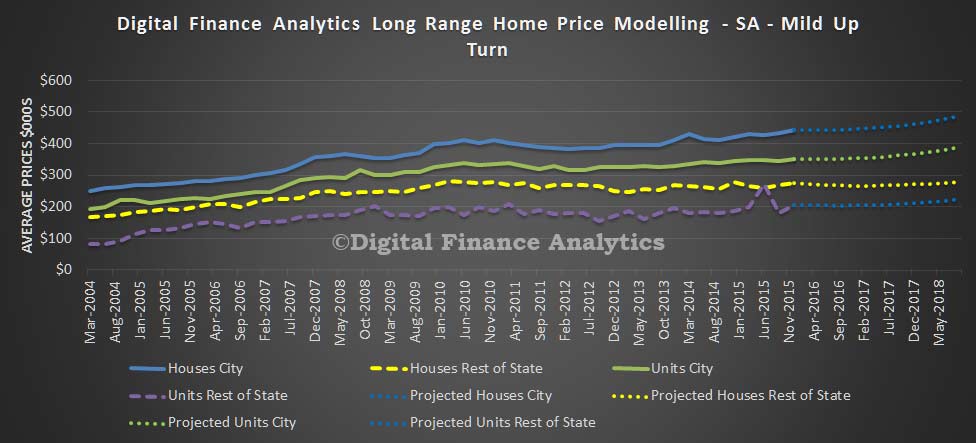

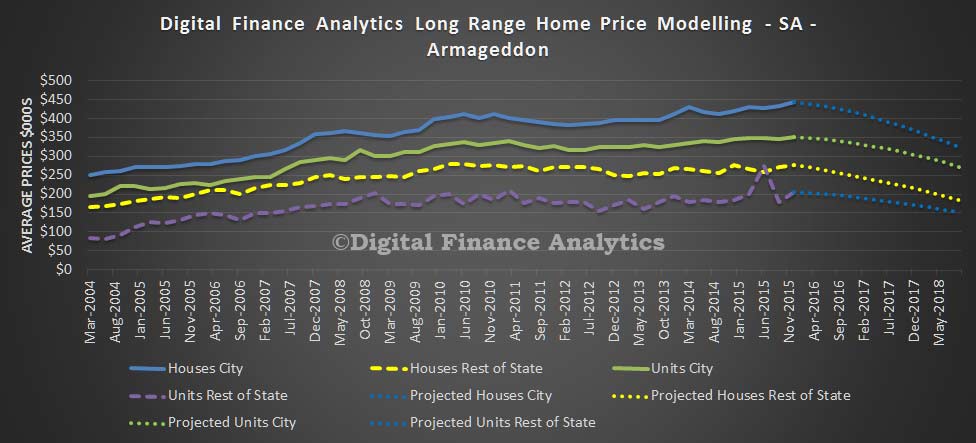

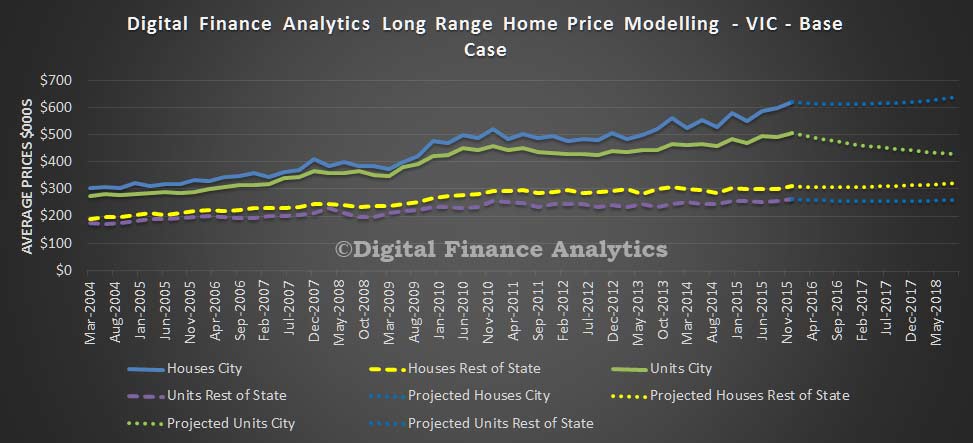

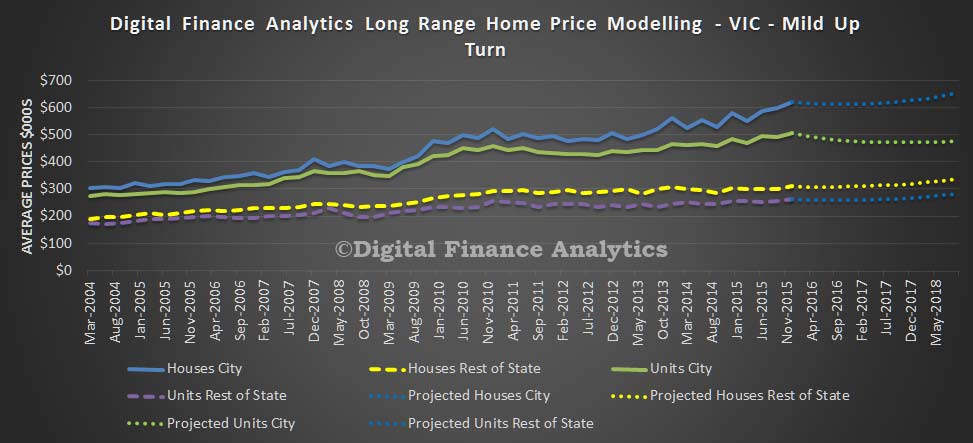

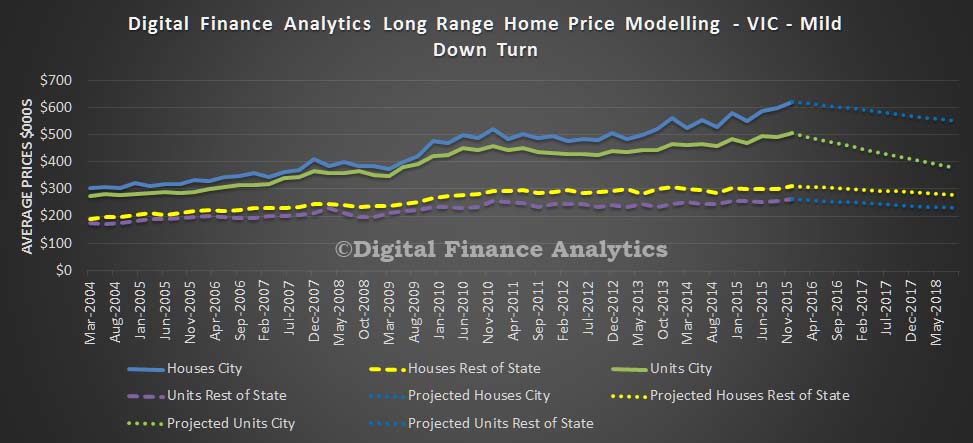

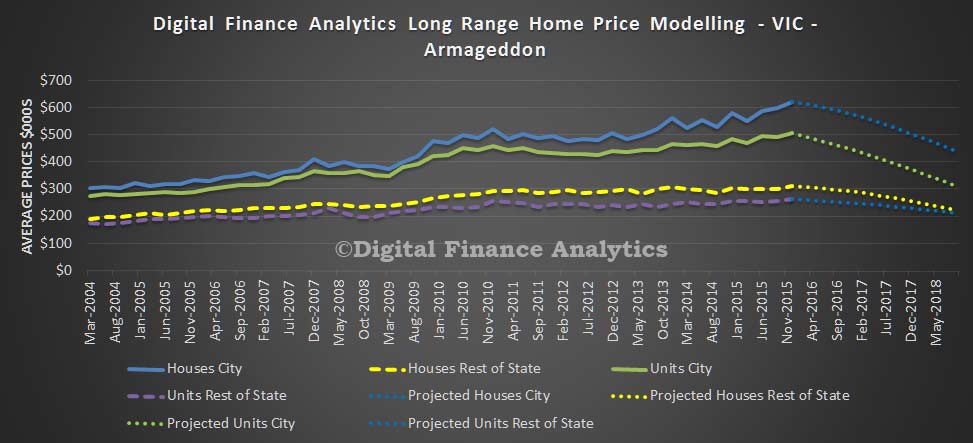

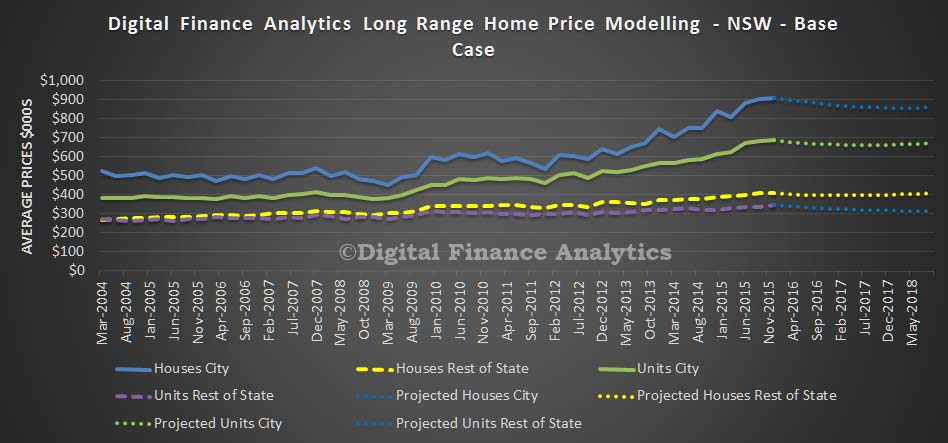

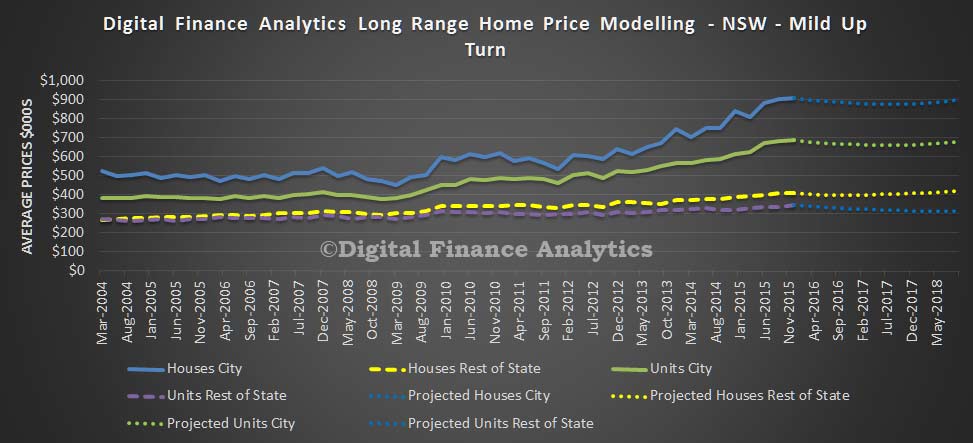

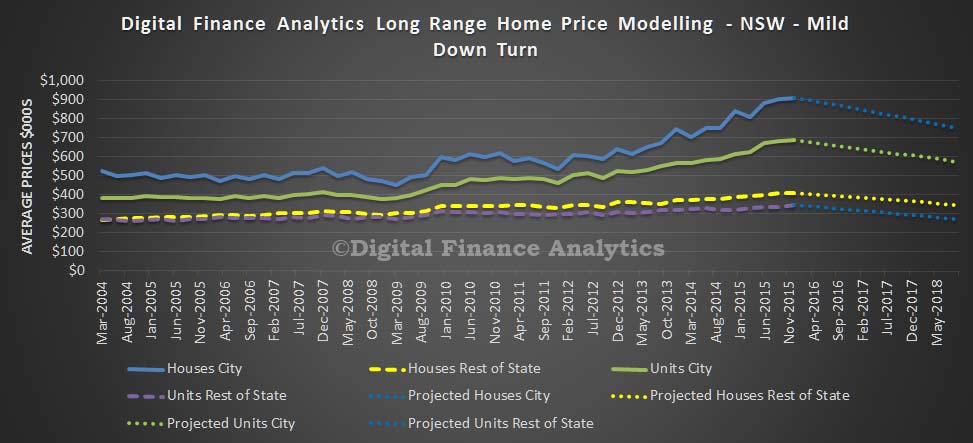

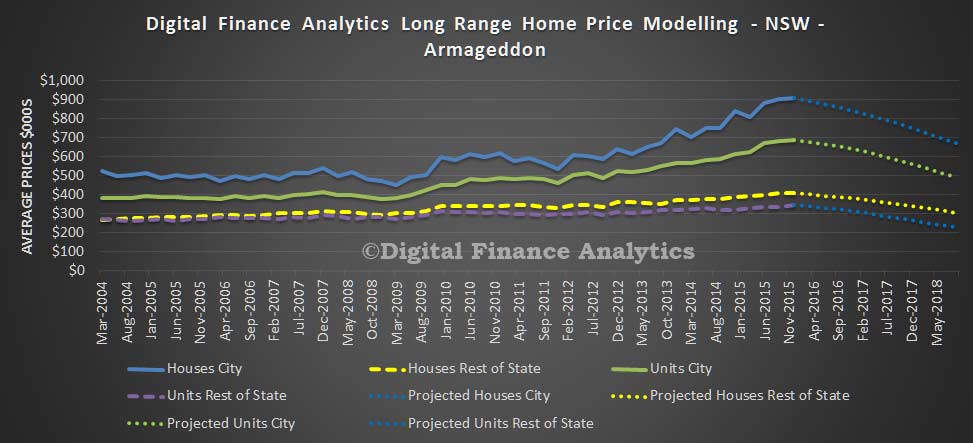

This is something we model dynamically, in our Core Market Model, which incorporates all these elements and delivers scenarios at a post code level for houses and units.

In comparison, the AFR published estimates from a panel of 10 property market experts and economists. Overall, they take a more sober view on growth prospects for the housing market, with most tipping gains of somewhere between 1 and 5 per cent. The most optimistic prediction is for house price gains of up to 8 per cent, while the most bearish forecast is for prices to fall nationally by as much 5 per cent.

Last year’s “very unusual supply and demand dynamics” are expected to normalise in 2024, according to Barrenjoey chief economist Jo Masters, who is tipping 4.8 per cent growth nationally. Sydney house prices could rise by 3.8 per cent, with Melbourne up 3.2 per cent and Brisbane 5.9 per cent.

“Importantly, we think borrowing capacity will re-emerge as a key constraint on demand,” she told AFR Weekend in a quarterly property survey.

Trying to pin the tail on the property price donkey, is fraught with difficulty, because of the uncertainty in the system – one reason why I run scenarios, and why the specific tale you prefer will influence your expectation of price movements.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

Blog")