In a fresh blow to Westpac, the Federal Court this morning delivered the corporate regulator a win in its appeal against a previous ruling on Westpac’s telephone campaigns. Via Financial Standard.

The full court this morning

said ASIC’s appeal will be allowed with costs, while Westpac-related

companies’ cross-appeal will be dismissed.

In 2014 and 2015, Westpac ran telephone and snail-mail campaigns to encourage customers to roll over external superannuation accounts into their existing accounts with Westpac Securities Administration Limited and BT Funds Management.

ASIC was primarily concerned with the telephone calls.

The

corporate regulator claimed that the two Westpac companies had breached

their FoFA-stipulated best interest duty by advising rollovers to

Westpac-related super funds without a proper comparison of options, as

required by law.

And so, it initially launched civil penalty proceedings against the two Westpac subsidiaries in December, 2016.

The

Federal Court handed down its judgment in January this year, with a

mixed outcome. It decided that ASIC had failed to demonstrate that the

two Westpac companies had provided personal financial product advice to

15 customers in regards to the consolidation of superannuation accounts.

However,

the judge added the Westpac subsidiaries contravened the Corporations

Act in 14 of 15 customer phone calls by implying the rollover of super

funds into a BT account was recommended. This came about through a

“quality monitoring framework” where BT staff were coached in sales

technique.

ASIC appealed the January judgment. Westpac also made a counter appeal.

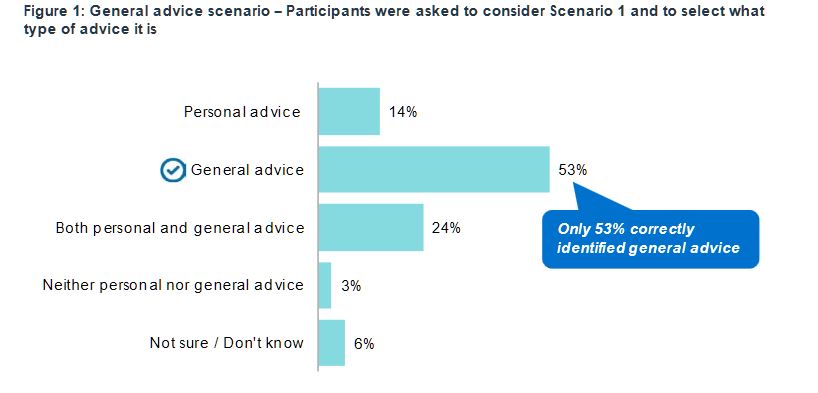

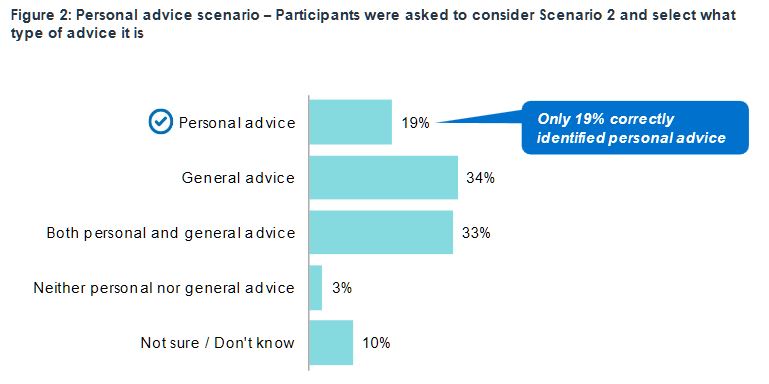

ASIC has released new research revealing many consumers confuse ‘general’ and ‘personal’ advice exposing them to greater risk of poor financial decisions.

The ASIC report, Financial advice: Mind the gap (REP

614), presents new independent research on consumer awareness and

understanding of general and personal financial advice, identifying

substantial gaps in consumer comprehension.

“This disturbing gap in understanding whether the advice they are

getting is personal or not means many consumers are under the false

premise their interests are being prioritised, when no such protection

exists,” said ASIC Deputy Chair, Karen Chester.

Millions of Australians will likely seek financial advice at some

stage in their lives. When they do, it is critical they understand

whether that advice is personal, whether it is tailored to their

circumstances and does the adviser have a legal obligation to act in

their interest.

“The survey not only revealed consumers are not familiar with the concepts of general and personal advice, but only 53 per cent of those surveyed correctly identified ‘general’ advice. And even when provided the general advice warning, nearly 40 per cent of those surveyed wrongly believed the adviser had an obligation to take their personal circumstances into account,” Ms Chester said.

The report highlights the importance of consumer awareness and

understanding of the distinction between personal and general advice

with the Future of Financial Advice (FOFA) protections only applying

when personal advice is provided. These include obligations for advisers

to act in their client’s best interests, to provide advice that is

appropriate to their client’s personal circumstances and to prioritise

their client’s interests. These obligations do not apply when general

advice is provided.

“The survey also revealed that the responsibilities of financial

advisers, when providing general advice, is not well understood. Nearly

40 per cent of those surveyed were unaware that advisers were not required by law to act in their clients’ best interests,” Ms Chester said.

ASIC anticipates the need for financial advice to grow, reflecting an

ageing population and many financial products, especially retirement

products, becoming more complex. ASIC reports that much of the advice is

likely to be general advice, and while appropriate in some

circumstances, it is inevitably of limited use.

“ASIC is seeing increased sales of complex financial products under

general advice models – so not tailored to personal circumstances –

leaving many consumers, especially retirees, exposed to the potential

risk of financial loss. And whilst the Financial Services Royal

Commission, and the Government’s response, dealt with the most egregious

risks of hawking of complex financial products, consumer confusion

about what is personal and general advice needs to be addressed,” Ms

Chester said.

The report’s findings reinforce those of the Murray Financial System

Inquiry and the Productivity Commission reports on the financial and

superannuation systems. Those reports made recommendations about the use

of the term ‘general advice’, which is likely to lead to false consumer

expectations as to the value of and protections afforded advice

received.

Ms Chester said, “This consumer research is timely. It comes as the

Government is considering policy recommendations on financial advice

from the Productivity Commission’s twin reports on Australia’s financial

and superannuation systems. And at a time when the financial system

itself undergoes much change, following the intense scrutiny of the

Financial Services Royal Commission, including considering new financial

advice and distribution business models”.

The report includes quantitative and qualitative research

commissioned by ASIC and undertaken by independent market research

agency, Whereto Research. The research used hypothetical advice

scenarios to test consumer recognition of when general and personal

advice was being provided, and awareness of adviser responsibilities

when being given each type of advice.

Report 614 Financial advice: Mind the gap is the first stage

in ASIC’s broader research project into consumer experiences with and

perceptions of the financial advice sector. Additional research by ASIC

will get underway in 2019 to identify a more appropriate label for

general advice and consumer-test the effectiveness of different versions

of the general advice warning.

The Royal Commission into Financial Services Misconduct has now uncovered evidence of poor industry practice from both the lending camp, including from mortgage brokers, and the financial advice camp. In both cases their forensic analysis revealed cases of consumers being put in the wrong products, charged for services they never received and on fee structures which were hardly transparent.

In addition, some advisers and brokers were restricted by the product portfolios available via their organisations, and ties back to the big banks and other large players were often not adequately disclosed.

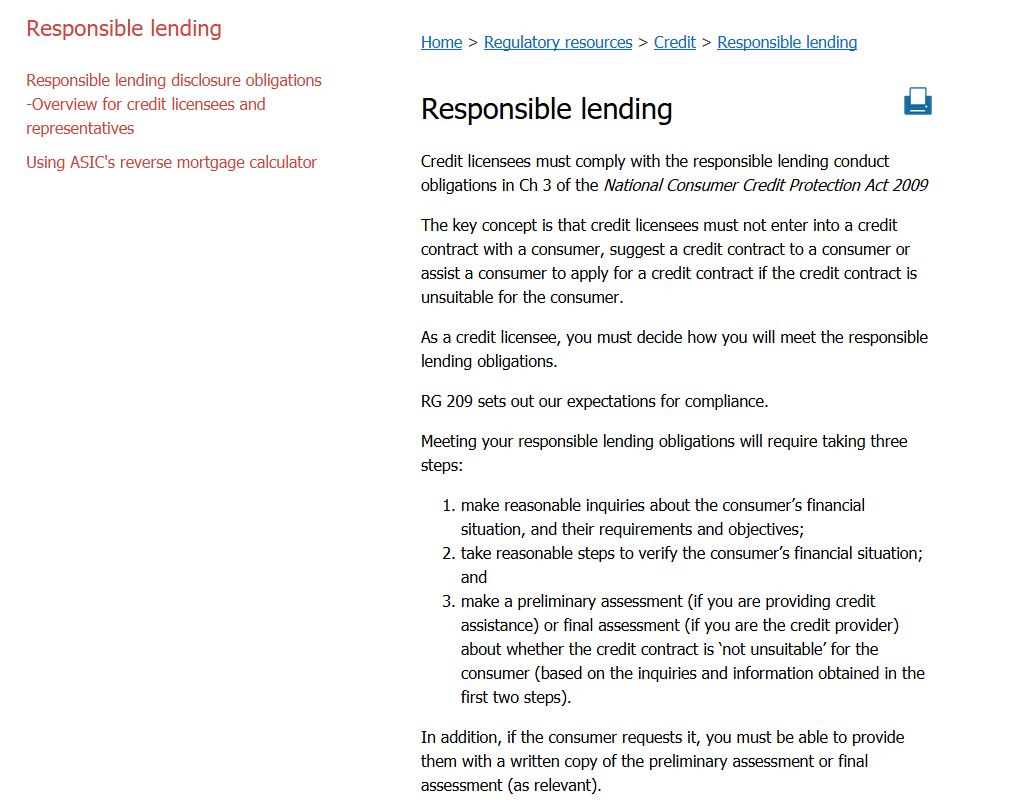

But here’s the thing. There are two distinct flavours of regulation in play, despite both being within ASIC’s bailiwick. I believe it is time to move to a unified common set of regulatory standards to cover both credit and wealth domains.

Lending and credit are based on ASIC’s regulations for responsible lending, which requires both a lender, and intermediary – like a broker – to ensure the loan is “not unsuitable”.

This looking at the purpose of the loan, making an assessment of the ability of the consumer to repay, and ensuring it is fit for purpose. What warrants as appropriate steps depends on the nature of the transaction and og the individual capabilities of the customers involved, so it is “scalable”. But that said, they are not obliged to act in the best interests of their client, and fee disclosure is at best rudimentary. Trailing commissions for example are not disclosed. The precise meaning and definition of what is suitable is still subject to case law. But overall, this is weak protection, and as we have seen from the Commission has failed to protect many borrowers. There is nothing here about the best or most appropriate product and it does not include any reference to whole of market analysis. Just, at best “Not Unsuitable”.

On the financial advice side of the house, as is being explored by the Commission currently, under the FOFA rules, advisers must work in the best interests of their clients, disclose remuneration, and their relationship with product manufacturers if appropriate.

This is a whole different set of rules, again regulated by ASIC. Note again, this does not include finding the best product, or providing whole of market advice. So the rules are slightly stronger, but still incomplete.

Now consider this scenario. I am a property investor who is seeking a mortgage as part of a strategy to build wealth. I will need a life insurance policy also. Who do I talk to? A mortgage broker can assist me with finding a mortgage, but cannot help with life insurance. But if I go and talk to a financial adviser unless they are also a mortgage broker, they cannot assist with the mortgage. And if I find an adviser qualified in both regimes, which rules do they work under?

And that’s the point. The regulations, which by the way are an accident of history in that the responsible lending laws evolved from earlier state legislation, get in the way of providing holistic unified advice. A consumer has both credit AND other wealth management requirements as part of a single issue. Indeed, there are trade-offs, for example between holding more or less investment properties, versus investing in other market related investment products. Indeed, it is feasible to wrap property investments into an overall wealth strategy.

So I suggest that now is the time to create a new unified set of rules to apply to all financial advisers, whether they are advising on credit or wealth products. They should be crafted around best interests of their clients, and should mean offering whole of market advice. That means creating an advice plan which spans both investments and lending. The plan should be based on a fee for service, and the advisers’ remuneration should not be in any way linked to a commission or revenue flow from the products they suggest.

Indeed, we should break apart the advice element from the product sale, and application. I suggest that individual product application could be completed by the adviser as part of a fee for service, but they should not receive any additional remuneration related to successful product sales.

This also has implications for ASIC, as it would reshape the advice landscape, but potentially could both simplify the regulatory regime, and strengthen the protection for customers, and help facilitate better customer outcomes. Down the track, advisers would require one set of qualifications, and would be become more recognised professionals.

I believe the current chaotic regulatory environments, which were crafted to appease the finance industry, are in appropriate and the time has come to create a single unified set of regulations. This would assist customers, but would also help the industry on its journey towards professionalism.

ASIC says the first civil penalty has been imposed on a financial services licensee for breaches of the best interests duty under the Future of Financial Advice (FOFA) reforms. The focus on the matter was on the “best interest” provisions and the remuneration model. This is a significant development.

The Federal Court has imposed a civil penalty of $1 million against Melbourne-based financial advice firm NSG Services Pty Ltd (currently named Golden Financial Group Pty Ltd) (NSG) for breaches of the best interests duty introduced under the Future of Financial Advice (FOFA) reforms.

The penalty relates to financial advice provided to retail clients by NSG advisers on eight occasions between July 2013 and August 2015. The clients were commonly sold insurance and advised to roll over superannuation accounts that committed them to costly, unsuitable and unnecessary financial arrangements.

The Court found that the failures by NSG to ensure compliance by its representatives were systemic in nature and in his reasons, Justice Moshinsky said, “I regard the contraventions as very serious ones”.

In March 2017 NSG consented to the making of declarations against it and after a hearing on 30 March 2017 the Court was satisfied that declarations ought to be made.

The Court found that NSG’s representatives breached:

s961B of the Act by failing to take reasonable steps to ensure that they provided advice that complied with the best interests obligations; and

s961G of the Act by failing to take reasonable steps to ensure that they provided advice that was appropriate to its clients.

Those breaches formed the basis of 20 contraventions in total by NSG of s961K(2) or s961L of the Act, which provides that a financial services licensee must take reasonable steps to ensure its representatives comply with the above sections of the Act.

The Court made the declarations based on a number of deficiencies in NSG’s processes and procedures, including the following:

NSG’s training on legal and regulatory obligations was insufficient to ensure clients received advice which was in their best interests;

NSG did not conduct regular or substantive performance reviews of its representatives;

NSG’s compliance policies were inadequate, and did not address its representatives’ legal or regulatory duties, and in any event, were not followed or enforced by NSG;

There was an absence of regular internal audits, and the external audits conducted identified issues which were not adequately addressed nor recommended changes implemented; and

NSG had a “commission only” remuneration model, which meant that representatives would be paid by way of commission for sales of personal risk insurance products and superannuation rollovers.

ASIC Deputy Chairman Peter Kell said, “This outcome makes clear to the industry the serious consequences of financial services licensees failing to comply with their FOFA obligations. ASIC will continue to pursue licensees who fail to do so.”

NSG, who agreed with ASIC on the amount of the penalty immediately prior to the hearing on penalty, and made joint submissions as to the orders, was also ordered to pay $50,000 in costs to ASIC, and will also pay $50,000 towards ASIC’s costs of its investigation into NSG under s91 of the ASIC Act.

The industry super lobby has accused the major banks of attempting to evade the FOFA regulation within their superannuation products.

Industry Super Australia (ISA) recently posted a submission to the Productivity Commission’s inquiry into the efficiency and competitiveness of Australia’s superannuation system.

ISA called for a crackdown on big banks and other for-profit entities who, it said, have been allowed to exploit superannuation fund members in the name of increasing sales.

The lobby group said the current superannuation system is like FOFA – where for-profit companies like the big four banks have been able to circumnavigate or “work around” legislation and exploit consumers for increased sales and insurance commissions.

“From inception, FOFA has been subject to substantial lobbying efforts that seek to weaken it, and for-profit entities have immediately sought to ‘work around’ and adapt to FOFA in a way that maintains as much of their lucrative businesses as possible,” ISA said in the submission.

“For so long as the superannuation system allows participation by entities that have a strong culture of prioritising themselves rather than serving others, this will happen. The inquiry’s proposed default [superannuation] models will certainly be subject to the same dynamic.”

ISA pointed to exemptions in FOFA which currently “allow bank staff to earn volume-related bonus for selling superannuation under general advice”.

FOFA also “allows the payment of commissions on individual life and income protection insurance on policies paid for out of choice superannuation products which provides strong financial incentives for advisers to switch members out of default superannuation products,” ISA said.

ISA pointed to research from the Roy Morgan Superannuation and Wealth Management in Australia 2011 and 2015 reports which showed the big banks shifting away from selling products via financial advisers and an increase in direct sales to consumers instead.

“This activity has almost doubled across the four major banking groups from 10 per cent in the 2011 Report, compared to 19 per cent for the three years to December 2015,” ISA said.

“[This takes] advantage of the lower levels of consumer protection outside personal advice to aggressively sell super directly.”

ISA said regulation and further competition are not the answers for cracking down on misconduct from for-profit entities in the superannuation sector.

“Regulation alone has never been enough to ensure good behaviour. Regulation is particularly unreliable in relation to the finance sector because that sector is especially vigorous in its efforts to influence policy makers,” ISA said.

There is a concern that “each of the inquiry’s proposals seeks to remove superannuation from the industrial system, and envisions private sector, for-profit financial institutions bidding for and winning pools of default superannuation members,” the submission said.

“Such an outcome will deliver to the for-profit part of the super system a ready-made, government-sanctioned, and generally disengaged customer base at a very low acquisition cost.”

Instead there needs to be a focus on culture and values within organisations ISA said.

“The reason why some funds tend to consistently perform well, and prioritise members, is an amalgam of culture, values, institutional objectives, and governance.”

For the first time we get a read on how the Future of Financial Advice (FOFA) reforms will be interpreted by the courts.

ASIC says the Federal Court has found that Melbourne-based financial advice firm NSG Services Pty Ltd (formerly National Sterling Group Pty Ltd) (NSG) breached the best interests obligations of the Corporations Act introduced under the Future of Financial Advice (FOFA) reforms.

This is the first finding of liability against a licensee for a breach of the FOFA reforms.

This matter relates to financial advice provided by NSG advisers on eight specific occasions between July 2013 and August 2015. On these occasions, clients were sold insurance and/or advised to rollover superannuation accounts that committed them to costly, unsuitable, and unnecessary financial arrangements.

NSG consented to the making of declarations against it and after a hearing on 30 March 2017 the Court was satisfied that declarations ought to be made.

The Court found that NSG’s representatives:

breached s 961B of the Corporations Act by failing to take reasonable steps to ensure that they provided advice that complied with the best interests obligations; and

breached s 961G of the Corporations Act by failing to take reasonable steps to ensure that they provided advice that was appropriate to its clients.

Those breaches amounted to a contravention by NSG of s 961L of the Corporations Act, which provides that a financial services licensee must ensure its representatives are compliant with the above sections of the Act.

The Court made the declarations based on the following deficiencies in NSG’s processes and procedures:

NSG’s new client advice process was insufficient to ensure that all necessary information was obtained from, and given to, the client;

NSG’s training on legal and regulatory obligations was insufficient to ensure clients received advice which was in their best interests;

NSG did not routinely monitor its representatives nor identify deficiencies in the knowledge or skills of individual representatives;

NSG did not conduct regular or substantive performance reviews of its representatives;

NSG’s compliance policies were inadequate, and did not address its representatives’ legal or regulatory duties, and in any event, were not followed or enforced by NSG;

there was an absence of regular internal audits, and the external audits conducted identified issues which were not adequately addressed nor recommended changes implemented; and

NSG had a “commission only” remuneration model, which meant that representatives would only be compensated by way of commission for sales of life insurance products and superannuation rollovers.

ASIC Deputy Chairman Peter Kell said, “This finding, the first of its kind, provides guidance to the industry about what is required of licensees to ensure representatives comply with their obligations to act in the best interests of clients and provide advice that is appropriate”.

ASIC has sought orders that NSG pay pecuniary penalties in relation to the declarations made. A date for the hearing on penalty will be fixed by the Court.

Background

On 3 June 2016, ASIC commenced proceedings against NSG in the Federal Court (refer: 16-187MR).

ASIC has banned Mr Adrian Chenh and Mr Bill El-Helou from providing financial services for a period of five years each following an ASIC investigation.

ASIC’s investigation found that Mr Chenh and Mr El-Helou provided advice to clients that was in breach of the best interests duty introduced under the Future of Financial Advice (FOFA) reforms.

ASIC found that Mr Chenh and Mr El-Helou had:

failed to act in the best interests of clients in that the advice provided did not leave them in a better position;

failed to provide advice that was appropriate to the clients; and

failed to provide financial services guides, product disclosure statements and statements of advice.

An additional finding was made that Mr El-Helou was not adequately trained, or not competent, to provide financial services.

ASIC deputy Chairman Peter Kell said, ‘Financial advisers must act in the best interests of their clients and provide advice that is appropriate. ASIC is committed to raising standards in the financial advice industry.’

Mr Chenh and Mr El-Helou both have a right to appeal to the Administrative Appeals Tribunal for a review of ASIC’s decisions. Mr Chenh has exercised his right of appeal and filed an application for review on 21 March 2017.

Background

ASIC has commenced proceedings against NSG Services Pty Ltd (formerly National Sterling Group Pty Ltd) (NSG) for breaches of the “best interests obligations” contained in the Corporations Act, and is seeking declarations of breaches and financial penalties (refer: 16-187MR). A hearing on liability occurred on 30 March 2017.

Both Mr Chenh and Mr El-Helou, previously representatives at NSG, gave financial product advice, particularly in relation to superannuation and insurance.

ASIC says it has commenced proceedings in the Federal Court of Australia against Wealth and Risk Management Pty Ltd (WRM), and related companies Yes FP Pty Ltd (Yes FP) and Jeca Pty Ltd (trading as Yes FS) (Yes FS), in relation to various alleged breaches of the Corporations Act 2001 and the Australian Securities and Investments Commission Act 2001, including alleged breaches of best interests obligations. ASIC is seeking injunctive relief, declarations of contraventions and financial penalties.

WRM is licensed to advise retail clients about, and deal in, life risk insurance and superannuation products. WRM authorises advisers, generally employed by WRM’s corporate authorised representative Yes FP, who provide personal financial advice to retail clients referred to them by Yes FS, via the website yesfs.com.au.

ASIC alleges that:

on numerous occasions since December 2015, WRM Advisers have provided advice that is conflicted and in breach of the best interests obligations contained in the Corporations Act;

WRM has breached s912A(1) of the Corporations Act by not:

doing all things necessary to ensure that the financial services covered by its licence are provided efficiently, honestly and fairly; and

has not taken reasonable steps to ensure that its representatives comply with financial services laws;

Yes FS has contravened s911A and/or s911B of the Corporations Act by carrying on a financial services business without holding an AFSL;

Yes FS has contravened s1041H of the Corporations Act 2001 and s12DA of the ASIC Act by engaging in misleading and deceptive conduct; and

WRM, Yes FS and Yes FP contravened s12CB of the ASIC Act by engaging in unconscionable conduct in connection with the supply or possible supply of financial services.

The first hearing of the matter is listed before the Federal Court of Australia at 9:30am on 31 March 2017.

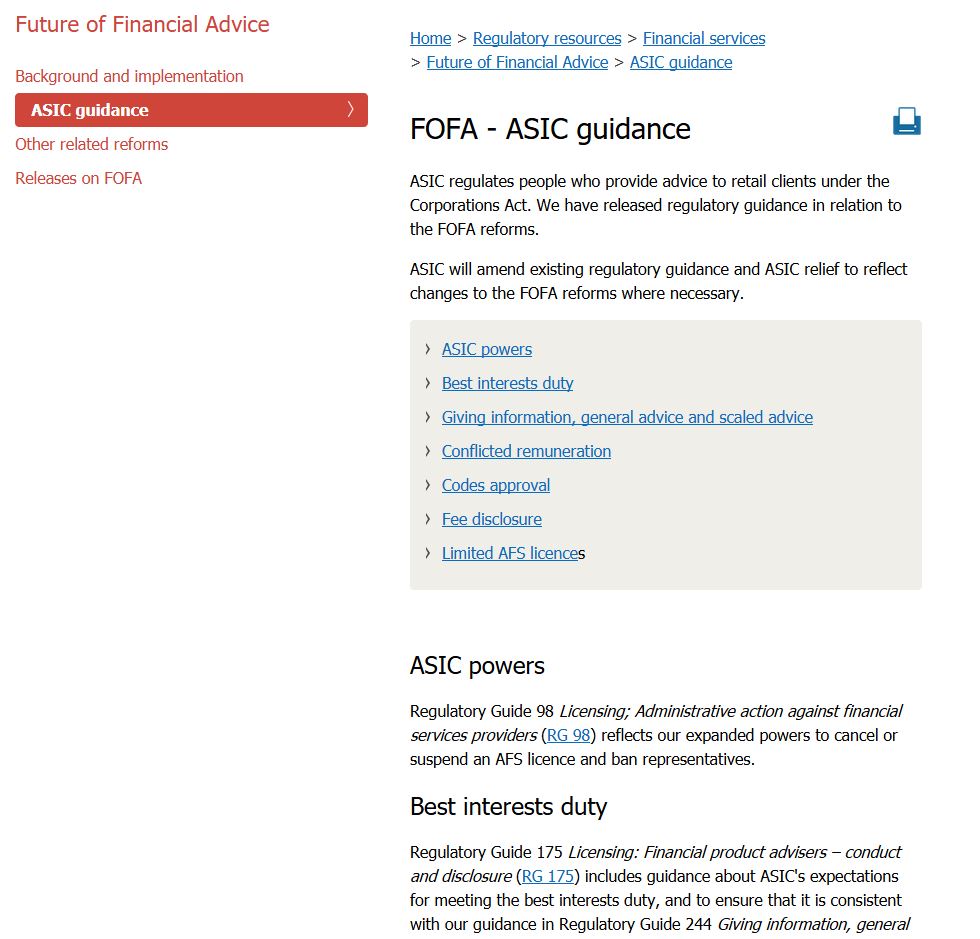

Part 7.7A of the Corporations Act 2001 (Cth) was enacted as part of the “Future of Financial Advice” (FoFA) reforms which are aimed at ensuring that financial advice companies and their advisers act in the best interests of the client. ASIC alleges in this case that WRM has breached s961L of the Corporations Act.

Regulatory Guide 175Licensing: Financial product advisers – conduct and disclosure provides guidance to help licensees understand ASIC’s expectations for meeting the best interests duty, and to ensure that it is consistent with ASIC’s guidance in Regulatory Guide 244Giving information, general advice and scaled advice.

Section 912A of the Corporations Act 2001 sets out the general obligations of Australian Financial Services Licensees.

Section 911A of the Corporations Act 2001 requires any person carrying on a financial services business in Australia and providing financial product advice to hold an AFS licence or be a representative of an AFS licensee. ASIC contends that the conduct that is the subject of this action required Yes FS to have an AFS licence or be an authorised representative of an AFS licensee.

Federal laws which will affect the future of the financial planning industry passed the House of Representatives last night.

The Corporations Amendment (Professional Standards of Financial Advisers) Bill, which was first introduced into Parliament in November 2016 by the Coalition, passed the House on the first sitting day of 2017.

Minister for Revenue and Financial Services Kelly O’Dwyer said the Bill comes in response to the actions of a minority of rogue financial advisers.

“Over time, repeated instances of inappropriate advice have led to a reduction in consumers’ trust in the financial advice industry,” O’Dwyer said during a reading of the Bill.

“Reduced trust acts as a barrier to consumers seeking financial advice, which is a poor outcome for both consumers and the industry.”

O’Dwyer recognised the majority of financial advisers have provided high-quality advice to their clients, adding that the measures debated will help to rebuild confidence in the industry.

Under the legislation, financial advisers will be required to hold a degree or a qualification equivalent to a degree, complete a professional year, pass an exam, and undertake continuous professional development.

A single uniform code of ethics will also set the ethical principles that advisers must comply with.

O’Dwyer hopes that the passing of the Bill means that more Australians will have the confidence to seek financial advice, noting that currently only one in five seek advice.

The new professional standards regime will commence on 1 January 2019, following successful passage through the Senate.

Labor’s last minute amendment

Prior to passing the House, Shadow Assistant Treasurer Andrew Leigh called on the government to apologise to victims of bad financial practice following their vote against Labor’s proposed financial advice measures.

“The house calls on current Liberal and National Party parliamentarians to apologise for the disregard their colleagues in the 43rd parliament showed for the many victims of bad practice in the financial advice sector when they voted against Labor’s Future of Financial Advice measures,” Leigh’s proposed amendment stated.

Leigh offered three additional amendments, drawing attention to the lack of trust consumers have in the financial services industry.

Speaking to Financial Standard this morning, head of policy and government relations for the FPA Benjamin Marshan said that while he feels positive about how the Bill passed the house, he is disappointed with Labor’s response, given that the industry is desperately seeking certainty.

“The amendments that the ALP proposed were trying to play games and show up the Government,” Marshan said.

“It’s disappointing that given that financial planners have been looking for certainty. Consumers are looking for increased trust and passing the Bill through unanimously shows that the ALP didn’t have any philosophical issues with the Bill.”

Marshan added that the FPA is looking forward to the Bill passing quickly through the Senate on Thursday.

“We’re encouraged by the commitment that the government is showing to the industry,” he said.

The Australian Bankers’ Association has today strongly rejected the claim by Industry Super Australia that banks ‘sidestep’ Future of Financial Advice protections when advising customers on superannuation.

The big four banks have been luring people away from industry super funds and into poorer performing super products, an industry super advocacy group claims.

Industry Super Australia says there has been a significant increase in people signing up to bank-owned super funds as the major banks ramp up their over-the-counter superannuation sales advice.

Industry Super’s chief executive David Whiteley says the banks’ super products typically delivered lower investment returns than industry super funds.

“There’s a real risk now of people walking into a bank and ending up as a member of a super fund that is worse than the fund they were already a member of,” he told AAP on Tuesday.

“The implication for the consumer is that they’ll retire with less, or they may have to work longer, or they will become more reliant on the aged pension.”

Mr Whiteley said the group’s analysis of data from Roy Morgan Research found that the big four banks had doubled their over-the-counter super sales advice between 2011 and 2015.

“The figures show direct advice is growing quickly and at the expense of traditional channels including financial advisers,” he said.

The research also found that customers were being switched from funds with higher net satisfaction and performance into funds with lower satisfaction and performance, he said.

And, unlike financial advisers, bank staff, who are often given incentives to sell the super products, don’t have to meet best interest obligations, he said.

“General advice direct from a bank does not need to meet the best interest obligations and it is likely the banks are using this and linked sales incentives to funnel customers into underperforming funds.”

Industry Super Australia wants banks to be required to perform a better-off test to demonstrate a customer would not be worse off if they switched funds.

It also wants a ban on all sales incentives relating to superannuation.

ABA responds:

“It is ridiculous to claim that the increase in major banks’ superannuation market share points to ‘obvious market failure’,” ABA Executive Director – Retail Policy Diane Tate said.

“Banks have made significant investment to change their practices and systems to comply with the Future of Financial Advice laws, banning conflicted remuneration and introducing a best interest duty,” she said.

“We also support new legislation to raise education, ethical and professional standards for all financial advisers.”

Ms Tate said customers want a one-stop-shop for their basic banking and financial services.

“Banks are using technology to make sure their customers have the convenience of being able to access all their products and services in one place, like using their smartphone, and with the confidence their money is secure.

“Banks have raised the competency and ethical standards of financial advisers. For example, just last month the industry announced a new way of hiring financial advisers to stop advisers with poor conduct records moving around the industry.

“We have also established an independent review into how banks pay staff and reward them for selling products and services,” she said.

“Industry super funds are competitors with banks. If only this was a campaign about doing the right thing by customers; but really it is just a competitive play,” Ms Tate said.

ASIC has said it has commenced proceedings against Melbourne-based NSG Services Pty Ltd (formerly National Sterling Group Pty Ltd) (NSG) for breaches of the ‘best interests duty’ introduced under the ‘Future of Financial Advice’ (FOFA) reforms.

This is the first civil penalty action ASIC has taken against a licensee alleging breaches of the best interests duty and is seeking declarations of breaches and financial penalties.

Since 3 April 2008, NSG has been licensed to provide personal advice on risk insurance and superannuation products to retail clients. NSG employs advisers to provide financial services advice on its behalf as its representatives and authorised representatives (NSG advisers).

ASIC alleges that:

NSG failed to take reasonable steps to ensure that its advisers complied with the best interests obligation when providing advice to clients; and

as a result, on numerous occasions, NSG advisers did not act in the best interests of their clients.

In addition, ASIC alleges that:

NSG has not provided appropriate training to its advisers to ensure clients receive advice in their best interests. Instead, ASIC contends that NSG has trained its advisers that it is almost always in a client’s best interest to take out some form of life risk insurance, regardless of a client’s financial situation;

NSG’s written policies relating to legal and regulatory compliance and risk management have been inadequate, and in any event, not followed or enforced;

since 1 July 2013, on eight specific occasions, and because of advice provided by NSG advisers, clients were sold insurance and/or advised to rollover superannuation accounts that committed them to costly, unsuitable, and unnecessary financial arrangements; and

regular and or substantive performance reviews of advisers have not been conducted, and disciplinary action against advisers who do not act in compliance with their obligations under the Corporations Act has not been taken.