Fitch Ratings forecasts subdued home price growth around the globe over the next couple of years due to a combination of stretched affordability, more challenging macro-economic conditions and macro-prudential measures restricting mortgage eligibility. This is despite falling or very low mortgage rates, insufficient supply in major cities and stable or improved employment levels in most countries.

Political

risks and their impact on economic growth and policy decisions are also

affecting our housing outlooks with lingering US-China trade

uncertainty, despite the recent easing in tensions, and China’s

de-risking drive, Brexit, and developments around mortgage and housing

policy beginning to take a toll.

The US-China trade dispute and

China’s de-risking drive are weighing on global and national growth

prospects, not only for the US and China, but also for their closest

trading partners (such as Australia and Canada) and areas like the EU

that are exposed to global trade.

“Weaker economic growth is a

key driver of more modest home price growth forecasts. UK home price

growth will continue to be affected by lingering trade ‘cliff edge’

risks until the new UK-EU relationship is negotiated. Although the newly

elected Conservative government is expected to pursue a formal exit

next month, there is more uncertainty about its ability to negotiate a

UK-EU Free Trade Agreement by the end of 2020,” said Suzanne Albers,

Senior Director of Structured Finance at Fitch.

In some

countries, there is also uncertainty around mortgage and housing policy.

The US and Canada are reducing the government’s role in mortgage

funding while in Mexico and Colombia new national housing plans may

increase government participation.

Of the 24 countries covered

in the report we expect a nominal price fall only in Italy and Japan,

due to Italy’s sluggish economy and Japan’s post-Olympics hangover and a

decline in real prices in Brazil, Canada, China and the UK. We also

forecast accelerating growth in Australia and Sweden, where prices are

recovering from recent falls, as well as in New Zealand and Colombia.

We

forecast low arrears levels for most countries covered in the report in

light of flat or falling policy rates. However, we also have concerns

about long-term low rates. Under a market stress, the limited scope for

further policy rate cuts would mean that home prices would not benefit

from substantial rate cuts as per recent downturns.

In this low

interest-rate environment, lenders are also struggling to originate the

volumes needed to defend profits, which has resulted in higher

loan-to-values (LTVs) and longer maturities being offered in several

European countries. Household debt levels remain the highest in

Australia, Canada, Denmark, the Netherlands and Norway, making their

economies more exposed to shocks and borrowers more vulnerable to

downturns.

Longer-term, the push towards ESG investments may change housing investment and mortgage funding.

“Fitch

expects climate change will permanently affect housing demand in areas

that are already or could become more exposed to natural disasters, if

they fail to attract new buyers or affordable insurance. Population

redistribution to cities will continue, which will support cities’

higher price dynamism, but conversely ageing populations and

developments in remote working and self-driving vehicles are likely to

also drive regional prices,” adds Albers.

Global macroeconomic challenges are likely to increase pressure on the short-term earnings prospects of investment-grade banks in the Asia-Pacific, Fitch Ratings says in a new report. The report addresses the main questions asked by US and Canada-based investors during a recent tour by Fitch analysts to discuss mainly investment-grade rated banking systems, with particular focus on Australia, New Zealand, mainland China and Hong Kong, Japan, Korea and Singapore.

Banks

in most markets face several challenges to operating performance,

including increased costs related to regulation, slower trade and

economic growth, subdued loan growth, low interest rates and acute

competition. These factors are squeezing net interest margins and

overall profitability. However, while many banks are likely to report

weaker financial results (or less improvement) in 2020 than in 2019, we

do not expect significant deterioration, and there is unlikely to be any

immediate impact on ratings. Consequently, the majority of bank ratings

remain on Stable Outlook. Nevertheless, some banks in Australia (in

particular, the major banks and their New Zealand subsidiaries) and in

Japan are more exposed to negative rating pressure. Where this is the

case, ratings are on Negative Outlook.

To combat these pressures,

banks are increasingly competing for fee income as part of less

asset-intensive (or risk-weighted asset-intensive) growth strategies,

including boosting total income from key relationships. However, many

banks have resorted to taking additional risk, typically credit risk, in

search of greater revenue and margin drivers.

Increased risk

appetite is appearing in various channels. These include expansion into

banking systems in overseas markets where Fitch regards the operating

environment as weaker; moving down the credit curve to support

loan-yields (through SME lending and unsecured personal lending, for

example); holding higher-yielding investment securities; and higher loan

concentrations in certain sectors such as property. The latter has been

attractive to banks from a risk-adjusted return perspective, but higher

concentrations increase the risk of faster deterioration in less-benign

operating conditions.

We expect Australia’s major banks to face

further earnings pressure in 2020. Falling interest rates and slow

credit growth are putting pressure on net interest income, while the

sale of parts of the banks’ wealth management operations and a reduction

in fees and commissions will hit non-interest income. We expect a

modest uptick in impairment charges in the weaker operating environment,

with households remaining susceptible to shocks in light of their high

leverage, while remediation programmes and system investments will weigh

on costs. Furthermore, higher prudential standards in Australia and New

Zealand will weigh on overall returns on capital, even though they will

support the intrinsic strength of the banks. Australia’s economy is

stable but growth is subdued, with downside risk stemming mainly from a

weaker global economy and the US-China trade dispute.

Bank

ratings in China, Hong Kong, Korea and Singapore remain stable,

reflecting either external support (sovereign or institutional) or the

banks’ intrinsic financial profiles having adequate buffers at current

rating levels to weather expected deterioration in 2020. Nevertheless,

downside risks exist, due to external challenges and, in Hong Kong’s

case, an economy hit hard by social unrest. Increasing exposure to

faster-growing emerging markets is likely to add to pressure, but this

may only become more evident when the operating environment is less

benign. This is also the case for Japanese banks, and comes on top of

structural challenges to their domestic operations, which are likely to

continue dragging on earnings and internal capital generation.

Slowing global economic growth, trade tensions and geopolitical risks will lead to subdued demand growth in global shipping in 2020, Fitch Ratings says in a new report. The sector outlook remains negative. Although all shipping segments have demonstrated more prudent capacity growth in recent years, which supported a better supply-demand balance, a longer record of responsive capacity management is needed to improve the sector’s resilience.

Free global trade is vital for shipping

as about 80% of world trade in goods is carried by the international

shipping industry. The main sector risk is that protectionist measures

may escalate into a protracted trade war and damage the prospects for

global trade and GDP growth. While some upside is possible if the trade

tensions between the US and China ease, the downside risks, including

expected slower GDP growth in China, soft trade growth and Brexit

uncertainty, will continue to weigh on demand.

The sector will

also need to cope with rising costs related to new regulation capping

sulphur content in marine fuel (International Maritime Organisation

(IMO) 2020), which is likely to negatively affect shippers’ credit

metrics. This regulation will probably increase operating costs (if

shippers choose to use more expensive low-sulphur fuel) and/or capex (if

they install scrubbers that remove sulphur from the exhaust or purchase

new LNG-fuelled vessels). Shippers are unlikely to fully pass through

all the associated costs to customers due to their limited bargaining

power in the oversupplied market. We expect most shipping companies to

use low-sulphur fuel.

We forecast global container volumes to

grow by about 2.5% in 2020. While this represents a small increase from

2019, it is well below the average growth rate of about 4.5% over the

past eight years. Trade restrictions, if they remain unresolved, are

likely to have a negative impact on global container volumes of about 1%

in 2020, according to AP Moller-Maersk. We expect better capacity

management in global container shipping with fleet capacity increasing

by 3.3% in 2020, slower than 3.6% in 2019. Container freight rates in

2020 are likely to remain at levels similar to those in 2019.

We

expect dry-bulk trading volumes to grow by 3% in 2020, up by more than

1.5pp on 2019. This improvement will be driven by higher iron ore and

other commodities volumes. Iron ore volumes are expected to slowly

recover following the Vale dam incident in Brazil and challenging

weather at Australian ports in 2019. Fleet additions are likely to match

this growth in volumes, and freight rates are likely to increase as

dry-bulk shippers will be better positioned to pass on some of the

higher fuel costs.

Global tankers’ supply and demand are likely

to grow by 2.5% and 3.5%, respectively, in 2020, supporting a better

supply-demand balance. This will help freight rates to stay at levels

comparable to annual averages in 2019, which represents a recovery from

their troughs in the middle of 2018. The impact of IMO 2020 on tanker

shipping companies is likely to be mixed, as rising compliance costs may

be mitigated by increased tanker demand to transport compliant fuel.

However, lingering trade and geopolitical tensions and political risk

may depress long-term tanker demand

Reverse factoring, a form of financial engineering, is on the rise. This is a technique used by a number of companies to dress their financial results.

Australian engineering group UGL, which is working on large

infrastructure projects such as Brisbane’s Cross River Rail and

Melbourne’s Metro Trains, recently sent a letter

to suppliers and sub-contractors informing them that as of October 15,

they will be paid 65 days after the end of the month in which their

invoices are issued. The company’s policy had been, until then, to

settle invoices within 30 days.

The letter also mentioned that if the suppliers want to get paid

sooner than the new 65-day period, they can get their money from UGL’s

new finance partner, Greensill Capital, one of the biggest players in

the fast growing supply chain financing industry, in an arrangement

known as “reverse factoring”. But it will cost them.

Reverse factoring is a controversial financing technique that played a major role in the collapse of UK construction giant Carillion,

enabling it to conceal from investors, auditors and regulators the true

magnitude of its debt until it was too late. Here’s how it works: a

company hires a financial intermediary, such as a bank or a specialist

firm such as Greensill, to pay a supplier promptly (e.g. 15 days after

invoicing), in return for a discount on their invoices. The company

repays the intermediary at a later date.

In its letter to suppliers UGL trumpeted that the payment changes would “benefit both our businesses,” though many suppliers struggled to see how. One subcontractor interviewed byThe Australian Financial Review complained that the changes were “outrageous” and put small suppliers at a huge disadvantage since they did not have the power to challenge UGL. Some subcontractors contacted by AFR refused to be quoted out of fear of reprisal from UGL.

CIMIC is one of Australia’s largest construction and infrastructure

groups. It is majority owned by the German company Hochtief, which in

turn is majority owned by the Spanish consortium ACS. In August ACS, the

world’s seventh largest construction company, admitted

it is making “extensive use” of both conventional factoring and reverse

factoring “across the group,” to “more efficiently manage cash flows

and match revenues and costs over the course of the year.”

Conventional factoring is a perfectly legitimate, albeit expensive,

way for cash-strapped companies to speed up their cash flow. It involves

selling accounts receivable — the amounts a company has billed to its

customers and expects to be paid in due time — at a discount to a third

party, which then collects the money from the customers.

Reverse factoring, by contrast, is a much more pernicious yet

increasingly prevalent form of supply chain financing that is being used

by large companies to effectively transform their supply chain into a

bank. Put simply, if suppliers want to get paid in a reasonable period

of time, they must pay an intermediary for the privilege.

More importantly, in most countries there is no explicit accounting

requirement to disclose reverse factoring transactions. The companies

can effectively borrow the money from the third party lender — thus

incurring a debt — without having to disclose it as debt, meaning it

expand its borrowing while maintaining its leverage ratios. This process

causes the debt to be understated.

Credit rating agency Fitch warned last year that reverse factoring effectively served as a “debt loophole” and that use of the instrument had ballooned, though no one knows by exactly how much since there is so little disclosure.

The use of an accounting loophole allowing companies to extend ‘payables days’ by the use of third-party supply chain financing without classifying this as debt may be on the rise, according to Fitch Ratings. We believe the magnitude of this unreported debt-like financing could be considerable in individual cases and may have negative credit implications.

Supply chain financing continues to be actively marketed by banks and other institutions in the burgeoning supply chain finance industry. A technique commonly referred to as reverse factoring was a key contributor to Carillion’s liquidation as it allowed the outsourcer to show an estimated GBP400 million to GBP500 million of debt to financial institutions as ‘other payables’ compared to reported net debt of GBP219 million.

The debt classified as ‘other payables’ was unnoticed by most market participants due to the near complete lack of disclosure about these practices and the effect on financial statements. Whether these programmes require disclosure under accounting standards depends greatly on their construction, which in practice allows many companies not to disclose them.

In the six months to June, CIMIC used reverse factoring and other

supply chain financing techniques to increase its total days payable to

159 days from 135 days in the previous six months, according to New Zealand investment bank, Jarden. By the end of June, its total factoring level was almost $2 billion.

More and more Australian companies are following the same playbook.

Rail group Pacific National told suppliers in May that it was using

global financial group C2FO‘s services to facilitate what it calls “accelerated payment of approved supplier invoices.”

Telecoms giant Telstra has ramped

up its exposure to “reverse factoring” more than 14-fold in the space

of just one year, from $42 million to almost $600 million. This $551

million increase, which is also reportedly being provided at least in

part by Greensill, represents a staggering 18% of Telstra’s 2019 free

cashflow, according to a report by governance firm Ownership Matters.

Yet the company’s credit is still rated A- by S&P Global, making it

one of Australia’s highest rated industrial corporations.

A Telstra spokesman said the company strongly denies that its

accounts “are not an accurate reflection of our business,” adding for

good measure that “supply chain financing is a practice commonly used

worldwide – it provides our suppliers the option of getting paid upfront

while at the same time getting the benefit of Telstra’s strong credit

rating.” Once again, it’s a win-win for both company and suppliers.

Yet in its last financial report, Telstra disclosed that it had extended payment terms to suppliers from 30 to 45 days to 30 to 90 days. This is part of “a persistent trend” that is hurting the cash flows of small and family businesses across Australia, revealed a review of payment terms released in March by the Australian small business and family enterprise ombudsman.

There is a persistent trend in Australia of payment times being extended beyond usual industry standards. Late payment, where businesses get paid beyond contract terms, adds to the cash flow problem faced by suppliers. It appears as though large Australian companies and multinationals apply these policies to improve their own working capital efficiencies at the expense of their suppliers. While the average days to get paid is declining, it is still above 30 days at an average of 36.74 days

This average obscures the imbalance between large and small business as large business are the worst for late payments and small business the fastest.

This imbalance intensifies cash flow pressure for small and family businesses. Scottish Pacific, a large independent finance provider, estimates the cost is $234.6 billion in lost revenue. That is, SMEs would have generated more revenue if cash flow was improved, as late payments accounted for a 43% downturn in cash flow.

Small and family businesses must find other ways to finance the short fall in their working capital. This places stress on smaller businesses with significant ramifications for solvency and mental health.

The outcome; small businesses cannot invest in growth and cannot increase employment.Since the Hayne Royal Commission, banks have tightened responsible lending standards across the board which has caused a ‘credit crunch’ for small businesses. They are finding it increasingly difficult to demonstrate ‘employee-like’ cash flow like a consumer. A high growth, entrepreneurial SME is highly unlikely to demonstrate cash flow in this way.

The increased bank focus on ‘employee-like’ cash flow means more needs to be done by large corporations paying their suppliers on time. Where large corporations delay payment to their small business suppliers beyond the contracted payment time, small business cash flow is unpredictable and presents significant difficulties in their ability to access and service finance.

Not only that, it’s also making it more likely that Australia will sooner or later have a Carillion of its own on its hands.

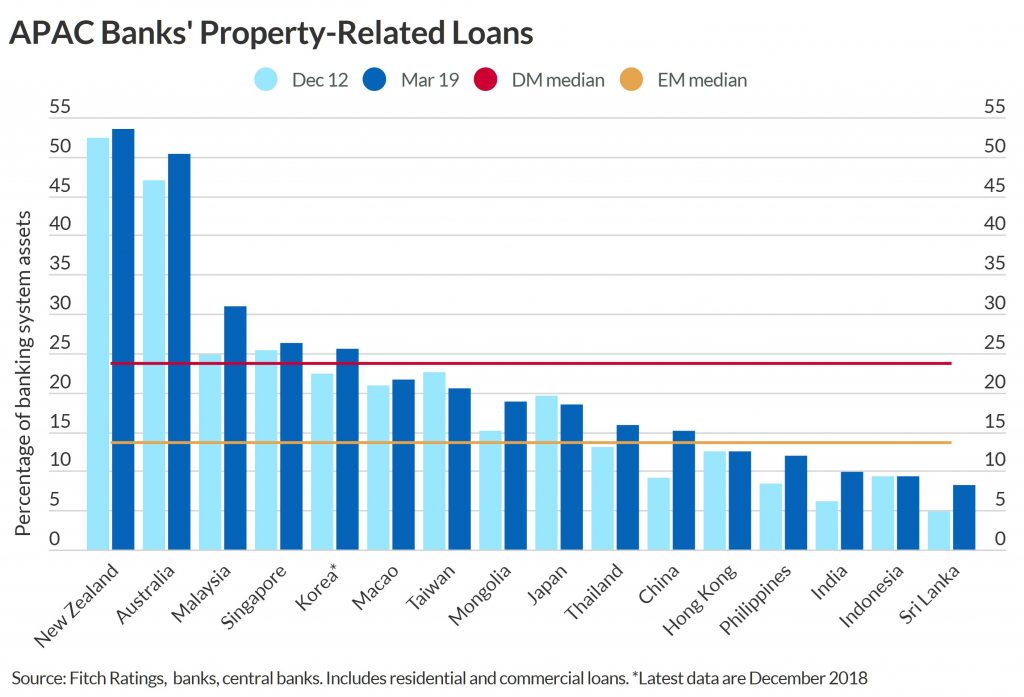

Banks in the Asia-Pacific region are increasingly exposed to property-related risks, Fitch Ratings says in a new report. The Australian and New Zealand banking sectors have the greatest exposure to property market stress, while banks in Sri Lanka, Mongolia and Vietnam have the least protection from loss-absorption buffers. We believe that regulatory oversight and macro-prudential policies should contain the direct effect of a residential property downturn on banks, especially in developed markets where loss-absorption buffers tend to be higher. However, accommodative monetary and economic policies could aggravate leverage.

Rising household debt increases risks for banks as borrowers’ debt-servicing capacity becomes more sensitive to economic factors, and a high reliance on property to collateralise loans exposes banks in a property market downturn. Regulators in most of the region’s developed markets have introduced macro-prudential measures to stem property-sector risks and to strengthen banking-sector resilience to potential property stress. We believe that policymakers will remain focused on measures that support stability and prevent risks of overheating, despite recent macro-prudential loosening in Australia, New Zealand and Taiwan to support their economies. We expect Hong Kong, Singapore and South Korea to maintain the tighter bias in their policy settings.

In general, developed economies in Asia have higher banking-sector exposure to property and more indebted household sectors than emerging countries. Australia and New Zealand are two stand-out cases, with household debt-to-GDP ratios of 129% and 94%, respectively, at end-2018. However, banking systems in developed markets have more experience of managing property cycles and stronger loss-absorption buffers, and the authorities’ proactive approach should cushion the impact on banks from a property market stress.

In emerging countries, banks’ exposure to the property sector tends to be lower, but risks are building in light of their strong property lending in recent years, due in part to governments relying increasingly on property to support their economies. Rapid credit growth often masks asset-quality issues, and rising property exposure makes banks more vulnerable to a property downturn, particularly where loss-absorption buffers are lowest (Mongolia, Sri Lanka and Vietnam). Property-related risks in India and Sri Lanka may be understated due to indirect exposures and limited data transparency.

Vietnamese banks appear susceptible in light of rapid consumer loan growth coupled with large legacy bad-debt issues and thin capital buffers. That said, a significant deterioration in Vietnam’s property market seems remote amid strong economic prospects.

In China, banks’ property

exposure has increased significantly over the past decade, but only to

15% of banking sector assets at end-March 2019, while household

debt-to-GDP had risen to 53% by end-2018 from 30% at end-2012. The risks

may be partly mitigated by macro-prudential and other measures, but the

Chinese authorities frequently intervene to manage the housing sector.

However, rising household debt adds to the challenges for domestic

consumption and the financial sector.

Fitch Ratings says residential mortgage loans in Scandinavia, the Netherlands and Switzerland have seen exceptionally strong performance despite high loan-to-value (LTV) ratios and significant household debt. This reflects generous social security systems and large household wealth, which are a common denominator of these ‘AAA’ rated jurisdictions with strong public finances.

The growth of housing

debt in Scandinavia, the Netherlands and Switzerland can be explained

by a combination of tax deductibility, low interest rates, and unique

features of each respective mortgage market. These include long

contractual tenors and interest-only periods. Limited repayment has made

borrowers more sensitive to house price decreases. However,

macro-prudential requirements in each country are helping to address the

risk that high household debt could jeopardise financial stability.

Macro-prudential

measures were originally focused on maximum LTV and stressed

affordability at origination, but lower mortgage rates continued to

stimulate mortgage growth. Banking authorities therefore imposed minimum

mortgage loan amortisation as well as maximum loan-to-income (LTI) or

debt-to-income ratios. Such restrictions have contributed to the recent

adjustment in Norwegian and Swedish house prices and limited lending

growth in Denmark. Swiss regulators have tightened capital requirements

for banks and promoted self-regulation, which established minimum

amortisation for mortgages above 66% LTV. Gradual changes to tax

incentives and underwriting standards were introduced by the Dutch

authorities, especially since 2013, which have made the mortgage market

more resilient.

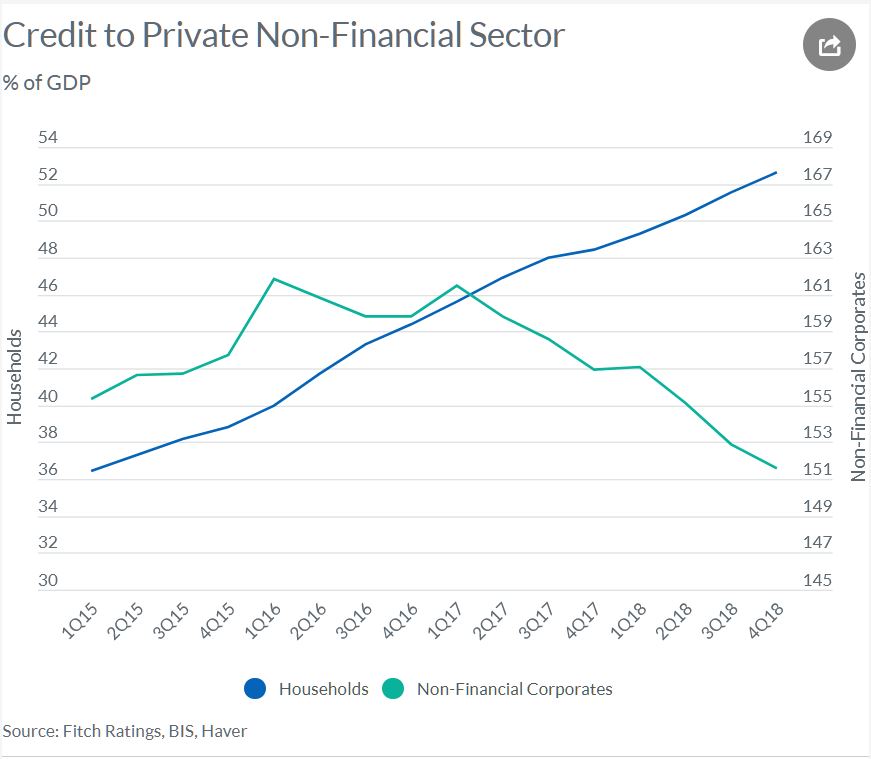

Chinese household debt has continued to rise rapidly, reaching 85% of disposable income at end-2018, Fitch Ratings says in a report published today. Rising debt servicing costs do not pose near-term risks to financial stability, but will weigh on economic growth in the medium term and this is reflected in our latest GDP forecasts.

Chinese household debt grew by 18.2% last year, slightly slower than in 2017 but still nearly double the rate of nominal GDP growth. They estimate that household debt rose to about 53% of GDP last year, up from just 18% a decade earlier. This increase was largely driven by mortgage borrowing, but has spread to other products such as credit cards, where the outstanding balance of debt was similar to the US, at about USD1 trillion at end-2018.

The household debt-to-disposable income

ratio is lower than most developed markets. But the gap will narrow

rapidly, with the ratio rising to close to 100% at the end of this

decade if growth rates remain unchecked.

The rapid pace of household debt growth is more of a concern than the level. Closing the gap with international peers would add considerably to China’s macroeconomic vulnerabilities, given its already high corporate debt burden. Rising consumer credit could support economic growth and rebalancing towards consumption in the near term. In their latest Global Economic Outlook published on 17 June, they increased our forecast for annual real GDP growth this year slightly, by 0.1pp to 6.2%, as earlier policy easing appeared to have gained traction. But consumer indicators have been relatively soft.

2Q19’s yoy growth rate of 6.2%, released by the National Bureau of Statistics on 15 July and in line with our GEO forecast, is consistent with their view that following a stronger-than-expected first quarter, growth would slow before stabilising. Rising household debt may lead to overleveraging by individual borrowers, eventually becoming a headwind to growth as debt service costs rise at the expense of other discretionary spending. They reduced their 2020 growth forecast by 0.1pp to 6.0% in the GEO, and see growth slowing to 5.8% in our 2021 forecast. A sharp correction in property prices is a downside risk, given households’ significant exposure to housing loans.

Household debt accounts for just 18% of banks’ assets in China, lower than many other APAC jurisdictions. But several medium-sized banks have aggressively expanded their lending in the segment, given continued corporate deleveraging efforts. Ping An Bank stands out, with 84% of its loan increase in 2017-2018 in retail loans, especially credit cards.

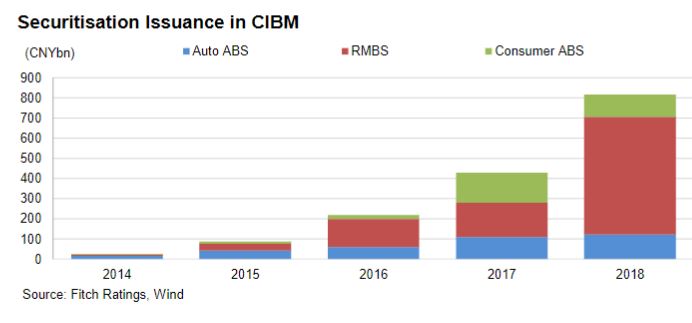

Among securitised assets in Chinese consumer ABS deals, unsecured consumer lending, which is less regulated than secured lending, exhibits a worse performance. Secured loans, like housing mortgages and auto loans, have been robust despite rising household debt because they benefit from stringent underwriting guidelines stipulated by regulators, and low average loan-to-values provide significant buffers against declines in collateral market value.

Securitisation accounts for about 2%of Chinese banks’ funding source for household debt. Securitised assets, which have performed better than banks’ overall books, can provide a direct and granular insight about asset-specific performance. The performance of secured loans, like housing mortgages and auto loans, has been robust despite rising household debt because they benefit from good economic environment and stringent underwriting guidelines stipulated by regulators.

The re-election of the Liberal Party-led coalition government (Coalition) in Australian federal elections on 18 May signals broad policy continuity in line with the fiscal priorities announced in April’s pre-election budget, says Fitch Ratings. The Coalition campaigned, among other things, on prudent fiscal management and a goal of achieving an underlying cash surplus next fiscal year, which is consistent with our fiscal assumptions when we affirmed Australia’s ‘AAA’ rating in April.

As

such, Fitch continues to expect a return to an underlying cash surplus

for the fiscal year ending June 2020 (FY20), marking the first time the

federal government has achieved this in 11 years. On a Government

Finance Statistics basis, we forecast a federal government deficit of

0.2% of GDP in FY19 followed by a surplus of 0.1% in FY20. General

government debt/GDP should fall to 40.8% in FY20 after remaining flat at

41.2% of GDP in FY19.

A commitment to fiscal prudence across

the political spectrum is a supporting factor for the country’s ‘AAA’

rating. Nevertheless, a 22pp increase in government debt/GDP since 2010,

due to sustained fiscal deficits, has eroded what was once a strength

for Australia’s credit profile relative to peers.

Slowing growth

remains a key risk to the fiscal outlook. We forecast real GDP growth to

decline to 2.0% in 2019 from 2.8% in 2018 amid spillovers from a

slowing housing market on dwelling investment and consumption, and

sluggish income growth. External risks from rising trade tensions and

the potential indirect effects on commodities demand also remain. A

sharper-than-expected economic slowdown would affect revenues beyond our

current base case and could add to political pressures for more fiscal

stimulus.

Positively, the unemployment rate remains low and the

labour market has proven resilient, though labour market indicators have

softened slightly in recent months in line with our forecasts. A large

pipeline of public infrastructure mitigates risks of a sharper slowdown.

The implementation of limited personal income tax cuts, as included in

the April budget, could also provide some support to growth. However,

using some of the recent upswing in revenues makes the fiscal trajectory

more sensitive to commodity prices, and GDP and wage growth. Commodity

prices have remained buoyant, lifting exports and corporate profits,

despite US-China trade ructions and the slowdown in Chinese economic

growth.

High household debt remains a risk for both the overall

economy and the financial sector. Fitch expects the ongoing house-price

correction to remain orderly, with prices declining 5% in 2019, but a

sharper correction could exacerbate risks from high household debt. Debt

service is low at current interest rates, but households remain

vulnerable to a labour market or interest rate shock, although neither

is expected in Fitch’s base case. We revised our monetary policy

forecast in March and expect the Reserve Bank of Australia to cut its

policy rate by 25bp to 1.25% in 2019. We forecast Australian growth to

rebound to 2.5% in 2020.

The Coalition will likely continue to

require cross-bench support in the Senate to pass legislation, and this

could add to risks to the budget outlook and affect policymaking

capacity particularly with regards to deeper, productivity-enhancing,

medium-term economic reforms.

Australia’s ‘AAA’ rating remains

underpinned by robust structural factors including strong governance,

high income, proven economic resilience and credible policymaking

institutions. The country retains a strong banking sector that is well

positioned to handle shocks and a potential growth rate of 2.4%, which

is above the ‘AAA’ median.

Potential growth projections for the larger emerging market (EMs) economies have deteriorated due mainly to a gloomier outlook for investment, says Fitch Ratings’ Economics team.

“One over-arching

theme from our updated estimates of potential growth is a slowdown in

projected investment growth over the next few years. This feeds through

to lower labour productivity growth as we see less scope for increases

in the capital to labour ratio, or ‘capital deepening'”, said Maxime

Darmet, Associate Director in Fitch Ratings’ Economics team. “Prospects

for a sharp re-acceleration in wider production efficiencies in emerging

markets also still look quite limited.”

Fitch’s updated

potential supply-side growth estimates over the next five years for the

10 major EMs covered in the agency’s Global Economic Outlook (GEO) show

downward revisions for Turkey, Brazil, Mexico, South Africa and

Indonesia and an upward revision for India. China’s potential growth

estimate remains unchanged at 5.5%.

Tukey’s potential growth is

now estimated at 4.3%, down 0.5pp since our last report. This reflects

the sharp external adjustment since last year’s currency crisis, which

has been achieved partly through a collapse in the investment-to-GDP

ratio. This will result in significantly lower growth in the capital

stock (and hence labour productivity) than previously projected.

Brazil’s

potential growth has been revised down slightly to 1.7% from 1.8%. Even

though we expect trend investment growth to be quite robust over the

next few years, on the fading effects of past large negative shocks, the

very low starting point for the investment-to-GDP ratio means that the

capital stock is unlikely to grow significantly, dampening GDP growth

prospects.

Mexico’s potential growth is now estimated at 2.5%.

This has been revised down by 0.3pp on the back of less favourable

investment prospects – particularly in the energy sector – as the new

government puts the implementation of reforms to the sector on hold.

South

Africa’s potential growth has been revised down by 0.2pp to 1.7%.

Sustained deterioration in business confidence is weighing on

investment, and total factor productivity (TFP) – which captures

improvements in the efficiency of the production process – continues to

decline.

Weaker trend investment growth is also the main reason

why China’s projected potential growth is much lower than recent

historical growth outturns. A declining investment-to-GDP ratio has been

necessary to limit the growth of corporate leverage, but has resulted

in slower growth in the capital stock. However, this rebalancing may

also have helped productivity at the margin: TFP growth has recently

stabilised after falling steadily from 2008.

India is still

estimated to have the highest potential GDP growth, at 7%. This has been

revised up by 0.3pp, in part reflecting the revised national statistics

showing significantly better growth performance in recent years than

previously estimated.

Indonesia’s estimated potential growth is

5.3%, revised down by 0.2pp. Growth outturns since 2015 have been

remarkably stable at around 5%, reflecting that potential growth has

ratcheted down.

TFP growth has not been particularly impressive

historically in most large EMs. Moreover, it has weakened substantially

over the past 10 years or so in virtually all countries – with the

notable exceptions of Indonesia and India. This may reflect waning

momentum in structural reform and a decline in manufacturing as a share

of GDP since the late 1990s, a sector that has traditionally exhibited

higher productivity growth.

Australia’s major banks will continue to face heightened regulatory scrutiny following recent public inquiries, including the Royal Commission, that identified shortcomings in conduct, governance and compliance, and will all be engaged in remediation that could distract management from day-to-day business, says Fitch Ratings. These challenges come amid other near-term pressures on earnings from a generally tougher operating environment.

The four major banks –

ANZ, CBA, NAB, Westpac – have large market shares across most products

in Australia and New Zealand, which support strong earnings and balance

sheets and help moderate risk appetite compared with many international

peers. However, it may be difficult for the banks to exercise these

advantages fully in an environment of increased public and regulatory

scrutiny, and pressure to increase their focus on customers rather than

shareholders.

In the longer term, there is a risk that the

findings of the inquiries may erode the market position of the four

major banks, either by reducing management focus on revenue growth or

through reputational damage – of which there is so far little evidence.

CBA

and NAB were found to have the most significant weaknesses in their

operational and compliance risk frameworks, and therefore face larger

risks from the remediation process. This is reflected in the Negative

Outlooks Fitch has assigned to these banks’ Long-Term Issuer Default

Ratings. Shortcomings that allowed misconduct issues to arise were

particularly evident at CBA, which is the only bank that will go through

to a formal remediation process and face increased capital

requirements.

Addressing conduct, culture and governance

problems should improve the soundness of the system in the longer term,

but will exacerbate banks’ short-term challenges. Fitch maintains a

negative outlook on the sector as earnings are likely to remain under

pressure in 2019 due to slower loan growth, especially in the

residential-mortgage segment, falling net interest margins, rising

wholesale funding costs, and increasing impairment charges, albeit from a

low level.

The main downside risks to bank performance continue

to stem from the housing market, where prices continue to decline after

large increases up to mid-2017. A sharp drop may result in negative

wealth effects for consumers and could undermine banks’ asset quality.

However, our central scenario is that house prices will fall by only

around 5% in 2019, which would represent a gradual easing of housing

market risks. Moreover, regulatory intervention in the mortgage sector,

including more stringent underwriting measures, has helped to reduce

risks in newer vintages of loans, and should make the major banks more

resilient to any downturn.