Compared with 12 months ago, First Time Buyers are caught in the jaws created by a combination of tighter mortgage underwriting standards and higher property market prices. Together these forces make the prospect of a purchase significantly less likely. This conclusion is drawn from our updated our household surveys. Looking in detail at the survey results:

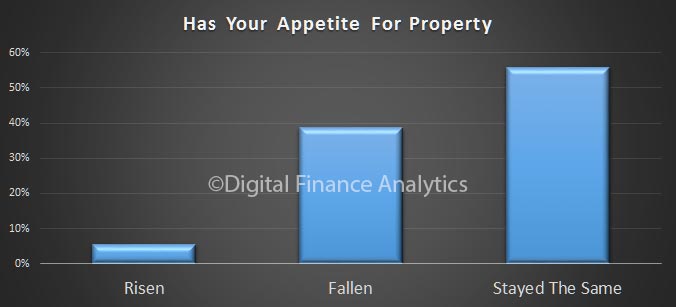

Compared with 12 months ago, 56% of first time buyers still have the same appetite to enter the market, just 5% has a stronger appetite now, whilst 39% have a lower appetite than a year ago.

The fall is driven partly by prices continuing to accelerate out of reach, with 51% saying their target was now more out of reach than a year ago, whilst 43% said there was no real change and 6% said prices has fallen. There were considerable state and regional variations. Prices in WA and areas of QLD are lower, whilst prices in NSW, VIC and ACT are significantly higher.

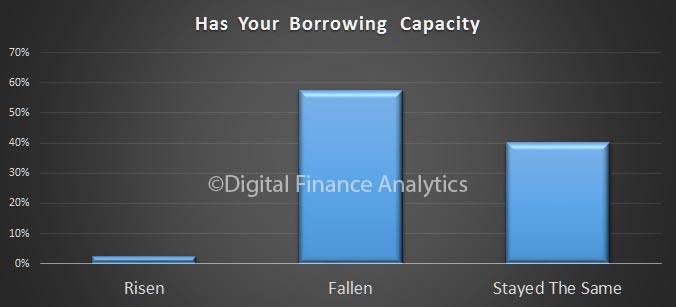

Finally, the combination of flat incomes, and tighter mortgage underwriting standards means that more than half – 58% – said they borrowing capacity had effectively been reduced. Around 40% said there was no change, and just 2% said their borrowing capacity had risen. Once again first time buyers in NSW and VIC were the most under pressure, thanks to high prices, and static incomes.

No surprise therefore that the latest ABS statistics shows the number of first time buyers continuing to languish.

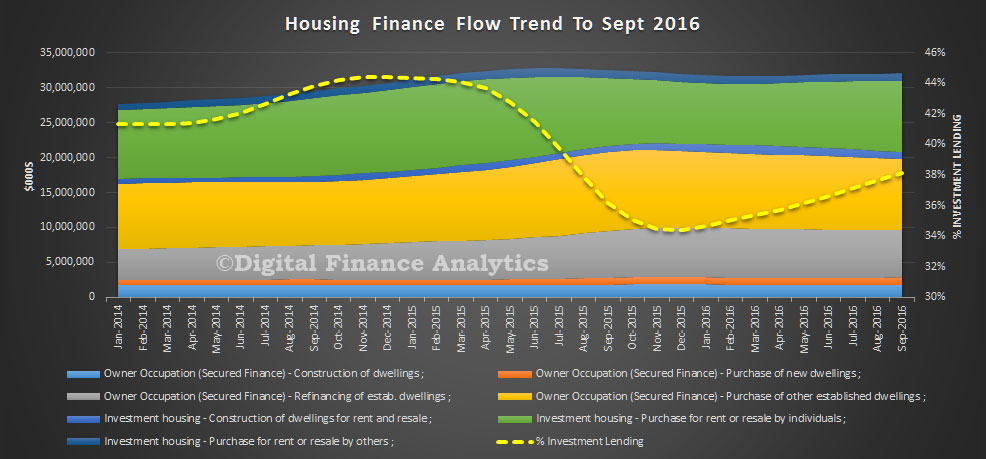

The latest data from the ABS showing housing lending to September 2016 should make the RBA reconsider its stance on housing. This is because, whilst lending for owner occupation fell slightly, property investors were strongly active again. As a result more than 38% of all new loans in September were for investment purposes. This is too high, and will continue to drive debt and home prices ever higher.

As normal we look at the trend series, which irons out monthly variations. Overall new loans worth $32bn were written, up 0.19% on the previous month. However, of that $12.2bn were for investment housing purposes, up 1.32%, whilst loans for the purchase of owner occupied established dwellings were $10.3bn, down 0.77%. Owner occupied refinance was down 0.46%, to 8bn but comprising 21% of all transactions and 34% of all owner occupied transactions. Loans for new dwellings and construction were $2.8bn, up 0.4%.

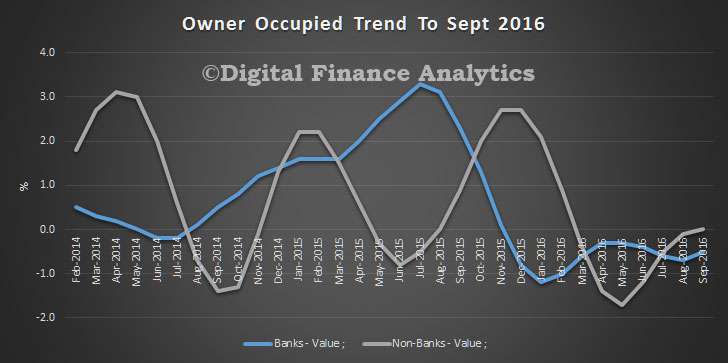

We also saw the mix between banks and non banks continue to shift, with the non-bank lenders higher.

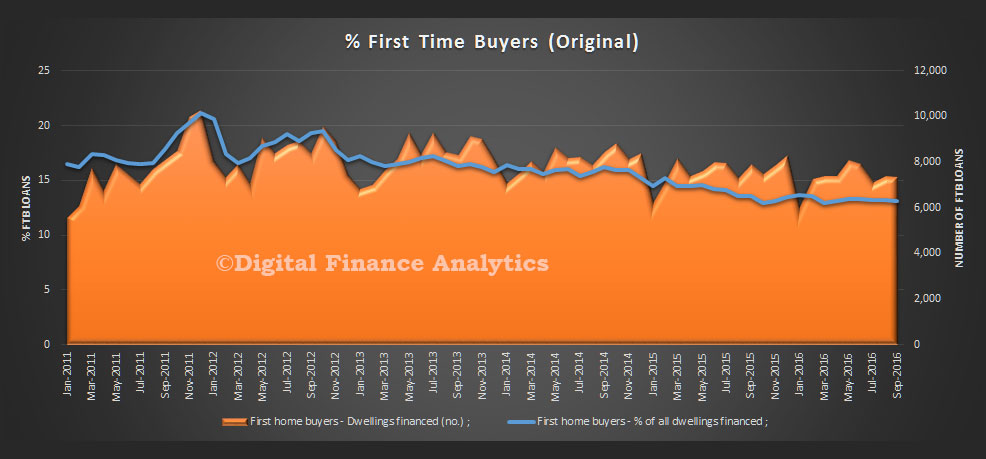

Looking at first time buyers, we see that the number of first time buyers fell again 0.5%, to 7,334 (original), which is 13.1% of all owner occupied loans. The average first time buyer loan was $324k, up 1.9%. The data also shows the proportion of fixed loan fell to 11.2%.

The DFA household survey identified an additional 4,000 first time buyers who whet direct to the investment sector – these are not caught in the ABS first time buyer stats.

All this explains the high auction clearance rates, and short listing times current observed, especially in the eastern states.

A leading financial services expert has described the rise in interest-only mortgages among first home buyers as “disturbing” and likely to trigger higher loan defaults in the future.

Data published by the Australian Prudential Regulation Authority shows that more first home buyers are resorting to interest-only loans to get a foothold in the property market.

The official statistics show that the total value of interest-only loans made by Australian banks rose by $10 billion to $481 billion in the June quarter.

Historically, interest-only loans have been popular among investment borrowers, but the latest data shows that owner-occupiers now account for a larger proportion of interest-only mortgages compared to June 2015.

Dr Adrian Raftery, a senior lecturer in financial planning at Deakin University, believes the trend in the official data indicates that a time bomb might be ticking for thousands of low-income borrowers who bought into the booming property market in the last 12 months.

“There’s been a lot of brainwashing from the operators of get-rich-quick schemes encouraging investors and owner occupiers to take out interest-only loans,” Dr Raftery told The New Daily

“Brokers are also contributing to the growth of interest-only mortgages because they get bigger trail commissions from banks when borrowers take longer to reduce the principal”.

“This is a disturbing trend.”

The problem with interest-only loans is that borrowers do not build equity in their homes until their mortgage contract requires them to start reducing the principal.

However the ABS still fails to pick up the substantial number of FTBs going direct to the investment sector. They should. We run our own series using data from the household surveys.

The ABS publishes monthly statistics relating to first home buyers in Housing Finance, Australia (cat. no. 5609.0): Table 9a (Australia) and Table 9b (State) on the downloads tab; and in Table 9 in the PDF document. First home buyer and other ABS lending statistics are collected on behalf of the ABS by the Australian Prudential Regulation Authority (APRA).

First home buyers are defined as persons entering the home ownership market for the first time as owner occupiers. First time investors are not included.

This paper provides details on the changes to previously published first home buyer statistics as a result of improved reporting by lenders.

BACKGROUND

In 2014, it was established that some lenders were reporting only loans extended to first home buyers who had also received a First Home Owner Grant instead of all first home buyers. As this would have resulted in an underestimation of the number of first home buyers, the ABS adjusted the estimates to account for the under-reporting. The methodology used to adjust the estimates to account for the under-reporting was published in the Information paper: Changes to the method of estimating loan commitments to first home buyers, 2015 (cat. no. 5609.0.55.003) which was released on 4 February 2015.

REVISIONS TO FIRST HOME BUYER STATISTICS

The ABS and APRA worked successfully with lenders to ensure that, in the future, all loans to first home buyers are reported, regardless of whether or not they received a First Home Owner Grant. As a result, from August 2016, the number of first home buyers will no longer require adjustment as most lenders will be reporting correctly.

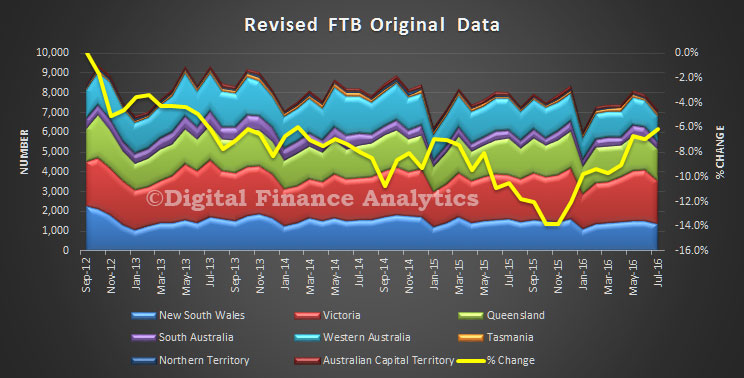

In the process of working with lenders, corrected historical data has been reported by some lenders and this improved data has been used to re-estimate the first home buyer statistics back to October 2012. This has resulted in revisions to the number of first home buyers for the period October 2012 to July 2016. These revisions impact on estimates for the number of first home buyers, the first home buyer ratio and the average loan size for first home buyers.

While the revised estimates show fewer first home buyers than previously reported over the period October 2012 to July 2016, the month to month movements are broadly consistent with the previously published series. For the most recent month (i.e. July 2016) the number of first home buyers in Australia has been revised down by 465 from 7,586 to 7,121.

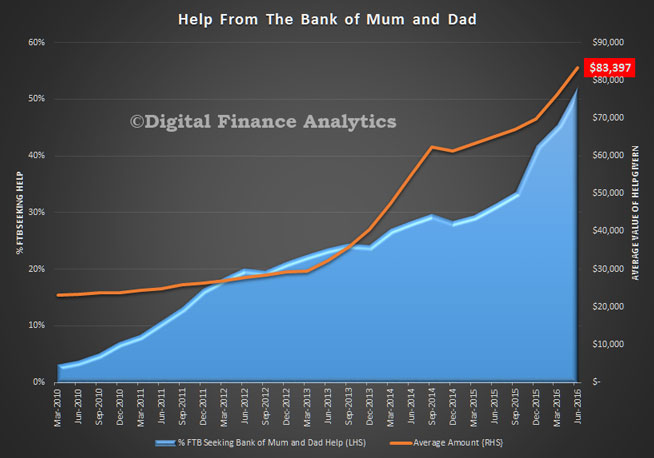

One significant factor in the mix is the extent of help to purchase from parents or other family members – the proverbial “Bank of Mum and Dad”. More than half of first time buyers are now seeking such help, and the average value has lifted to more than $83,000. The trend since 2010 is pretty stark. Those without access to family money are at a significant disadvantage.

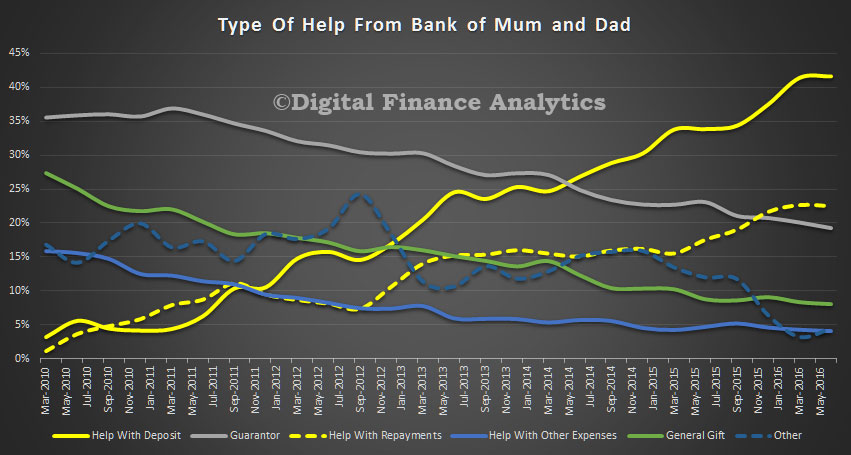

Looking in more detail at the type of help, direct assistance with a deposit now accounts for more than 40%, whilst around 20% of first time buyers receive some help to meet ongoing mortgage repayments. In contrast, the proportion of families offering a bank guarantee is falling, along with making general gifts. Others get help with general expenses, especially child care costs, or purchase transaction costs.

This inter generational shift of wealth is enabled by the accumulated value gained by older households as they ride the property price boom. Some will refinance to draw capital out for their kids. Sometimes this is used to help these first time buyers to purchase an investment property.

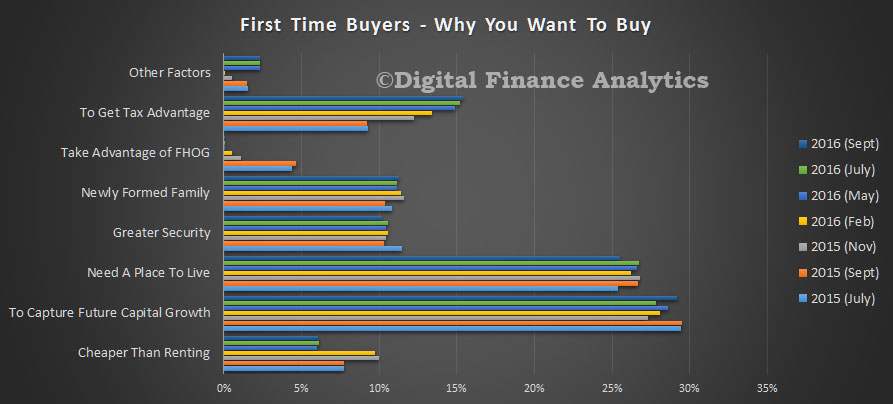

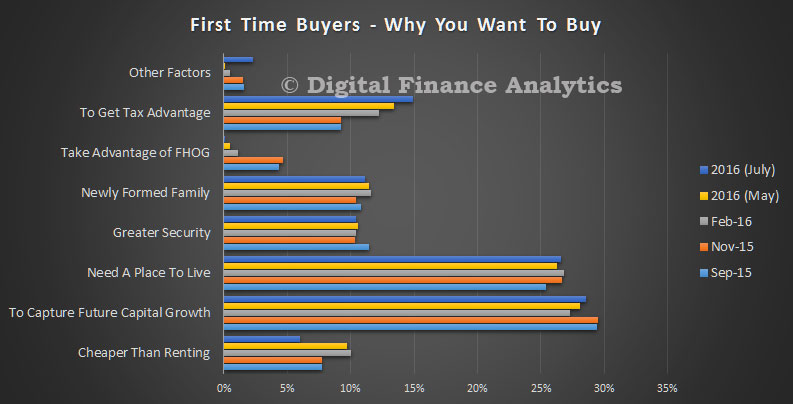

From our surveys we also find that as many first time buyers are being driven by the expectation of future capital growth as finding a place to live. They are also aware of the tax advantages, and the relative costs of renting.

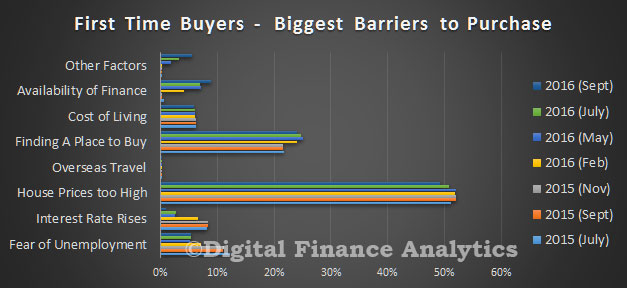

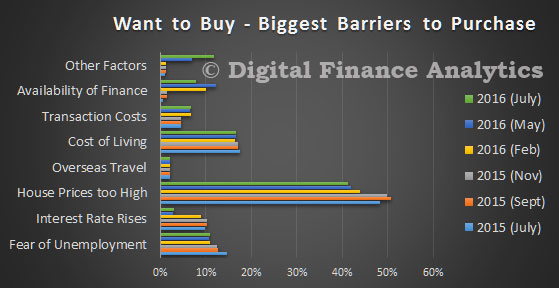

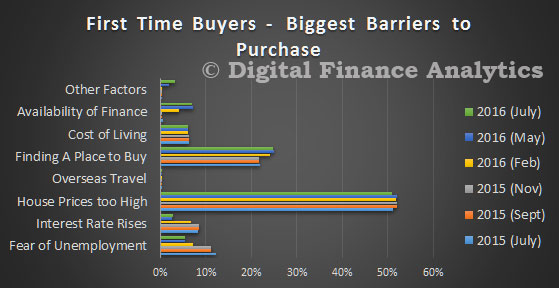

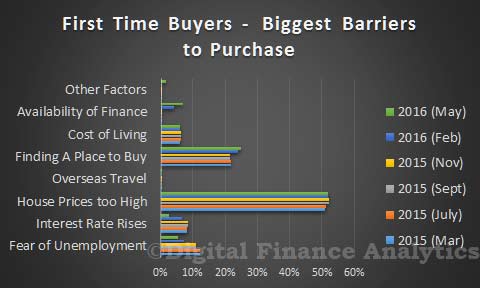

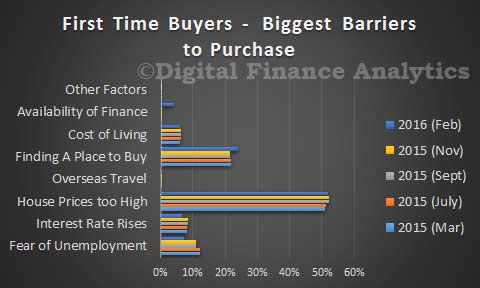

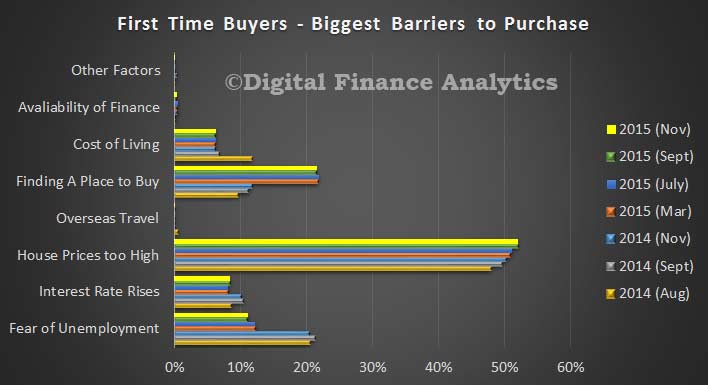

No surprise then the biggest barriers to purchase are high home prices (more than 50%) and finding a place to buy (24%).

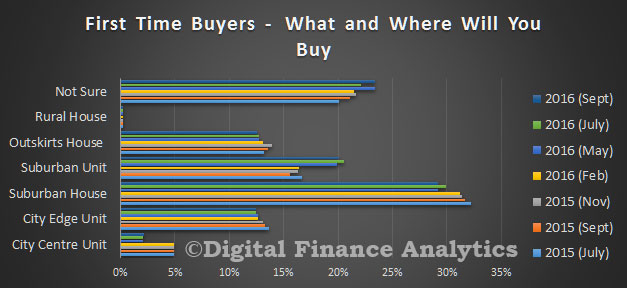

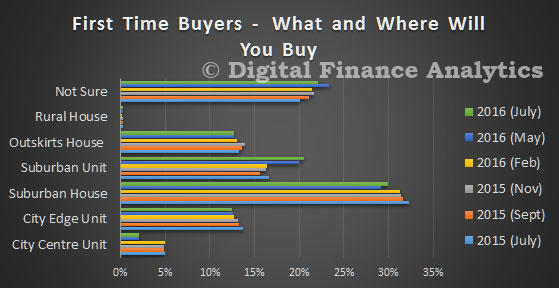

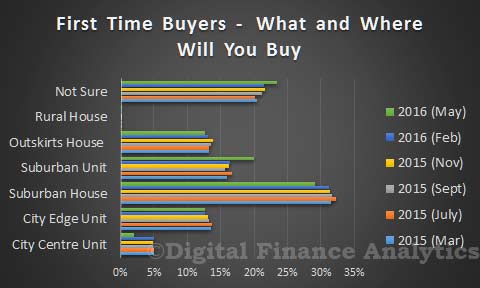

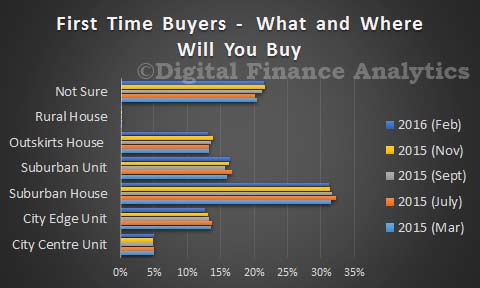

More than 23% say they are not sure where they will buy, though nationally a suburban house is still the first choice.

However, in the eastern states, high prices lead to more households going for a unit, or to purchase an investment property.

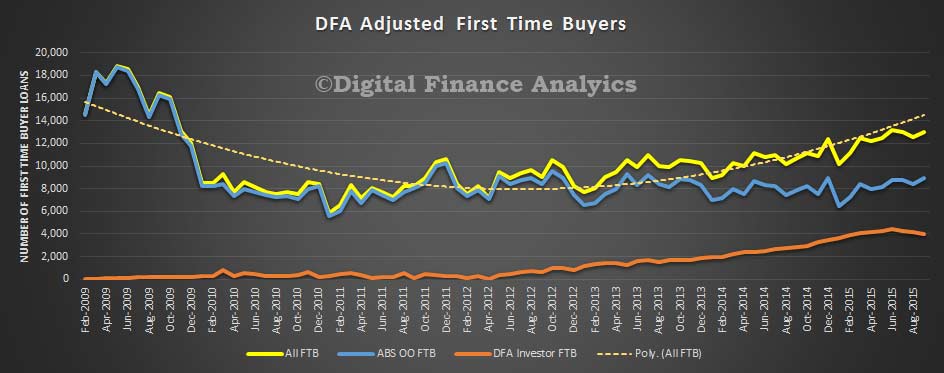

Our first time buyer tracker shows that a significant proportion of first time buyers are going direct to the investment sector. The ABS reported the number of OO first time buyers fell last month. In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 14.1% in July 2016 from 14.3% in June 2016. The number fell from 8,486 to 7,586, down more than 10%. The average loan size was $335,600, 0.2% higher than last month.

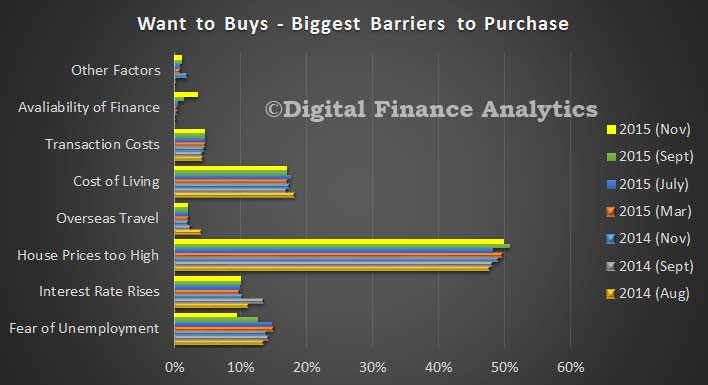

Looking briefly at those wanting to buy, but are not able to at the moment (about 1.1 million households, down from 1.3 million last year), whilst fear of unemployment and interest rate rises continue to dissipate, home prices are just too high relative to their income, to consider market entry. This is also influenced by their costs of living, and an inability to get finance. We also note a rise in “other factors”, which include needing to get finance help from family or friends.

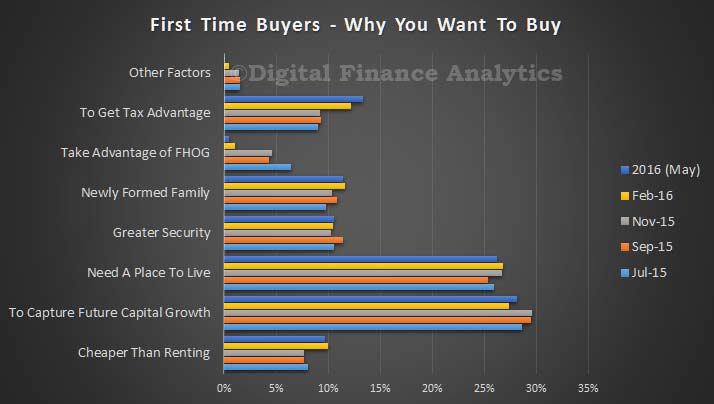

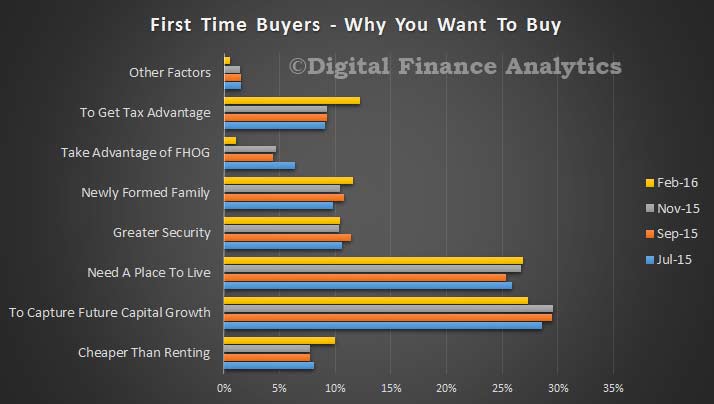

Turning to those actively seeking to enter the market in the next year for the first time (about 312,000 households), we see that more are motivated by potential future capital growth than needing a place to live. In addition, tax advantage was cited by around 15 per cent of first time buyers as a key driver, whilst access to the first home owner grant has become ever less important.

Looking at the barriers to purchase, first time buyers say that high home prices remains the most significant barrier, and as a result just finding a place to purchase is a challenge. Whilst fear of unemployment and the impact of rising interest rates have reduced, more are saying that availability of finance is an issue now as lending criteria are tightened.

Well over 20 per cent of first time buyers are not sure what, or where they will buy. More are likely to buy a unit than a year ago, and less likely to buy a house.

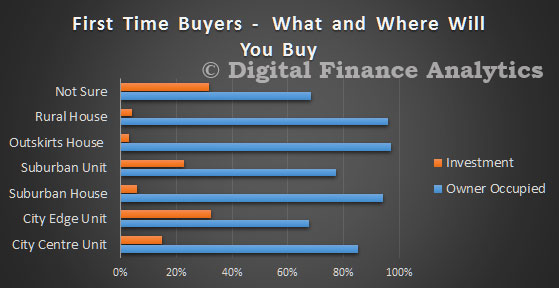

We also continue to see a proportion considering buying an investment property, perhaps a cheaper property in an area they do not want to live in, as a way to enter the market, and participate in potential capital growth. This may be the key to an owner occupied purchase later.

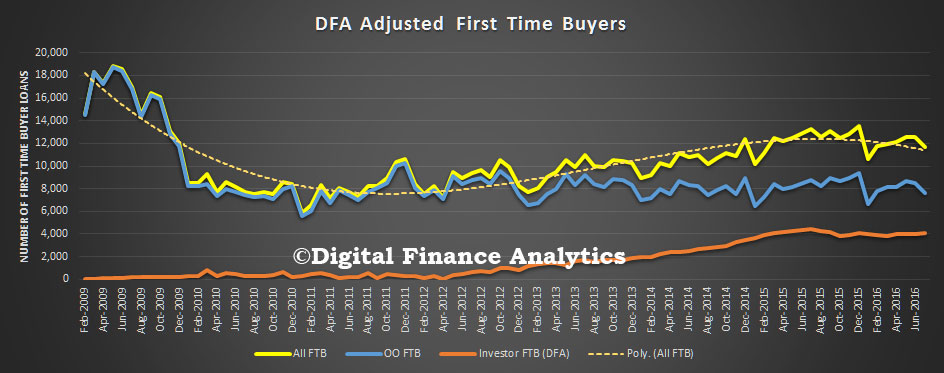

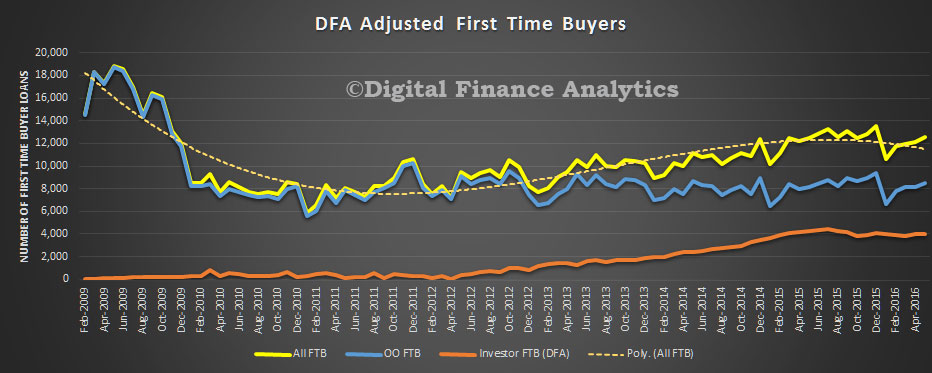

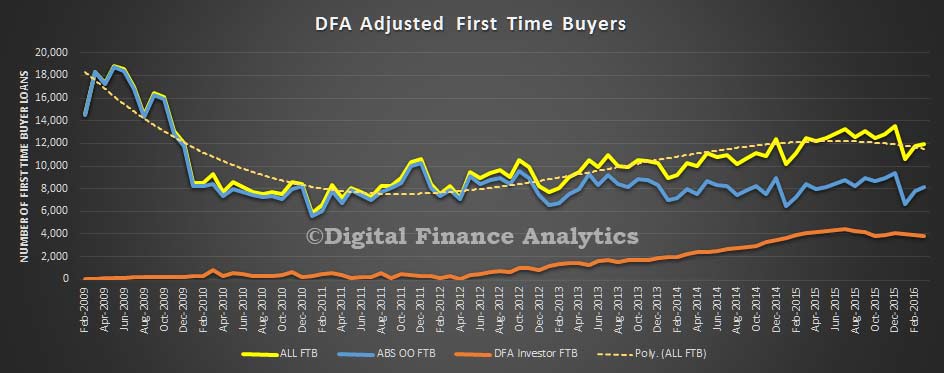

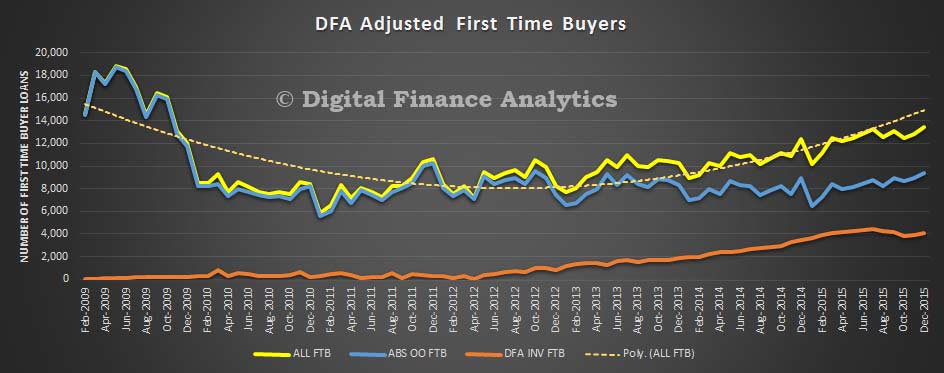

We publish monthly data on the number of first time buyers who go direct to the investment sector from our surveys and overlay this on the ABS data. Around 4,000 are buying each month. The ABS data also shows the number of first time buyers is rising, to May 2016, though still well below the peak.

Next time we will do a deep dive on the investment property sector.

Rounding out our survey findings, we look briefly at the first time buyer market segment. We noted in the summary that there was still demand – and we see this translated into both owner occupied and investment property purchases. The “Bank of Mum and Dad” is becoming an important factor, with more than half of first time buyers saying they had some financial help from the wider family. In some cases this translated into a deposit, in other transaction costs, but the most common mode appears to be a loan – often at cheap rates. We also know that banks look for a savings behaviour, so a windfall gift is not necessarily the most successful mode of assistance.

The latest data shows that first time buyers are as interested in capital gains, and tax advantage as meeting a need for a place to live. The tax advantage benefit registered more strongly this time around (thanks to all the recent publicity around negative gearing and capital gains benefits). On the other hand, the first home owner grant structures have largely been dismantled, and in any case they simply pushed prices higher, so were an expensive and ultimately ineffective lever.

The barriers to purchase – which vary by state to some extent – centre on the fact that simply house prices are too high. As a result finding a place to buy, especially competing with investors (who we saw yesterday are back in the game) is hard. We also see a spike in households unable to find finance, as lending criteria have tightened. Lower interest rates do not translate automatically to a larger loan, as the banks are using a floor of 7.25% or more for serviceability assessment – and this has not changed since the recent rate cut. Our modelleing shows that there are much deeper rate discounts for existing buyers wanting to refinance, compared with first time buyers. In addition, the maximum LVR has lowered, so larger deposits are needed – at a time when interest rates on deposits continue to grind lower. Thus first time buyers are squeezed, at a time when incomes are static in real terms.

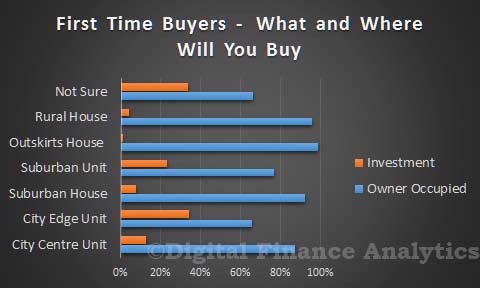

Looking at the types of property first time buyers are considering, we see that 23% are simply not sure what to go for. Our surveys show that price is the main determinate, and the style, or location of property is somewhat secondary. They simply want to “get on the ladder” – despite the fact we are probably close to peak house prices, and peak household debt! Nationally, the suburban house remains the most attractive option, though more are now having to settle for a suburban unit (20%).

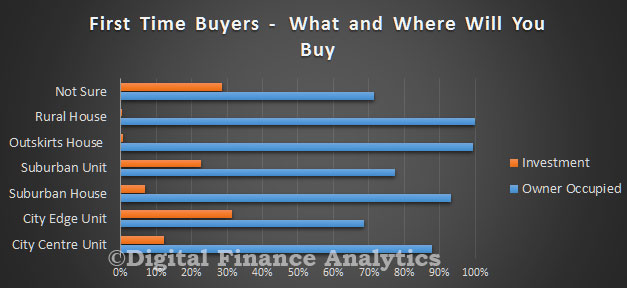

If we ask about whether they will go for an investment property or an owner occupied property, we see that most of those going the investment route are considering a unit, on the fringe of the City. About one third of first time buyers will likely end up as an investor, not living in their own owner occupied home.

Continuing our series on the results from our latest household surveys, today we look at first time buyers. Data from our surveys, combined with recently released ABS data, highlights that first time buyers are more active now compared with last year. Whilst many first time buyers are seeking to buy a place to call home, an increasing number are looking to go direct to the investment sector to buy a cheaper place as a means of getting on the property ladder, assisted by tax breaks and negative gearing. This trend continues to build.

So, looking at first time buyer motivations, we find that prospective capital growth is the strongest driver (27%), compared with needing a place to live (26%). Significantly, tax advantage figures as a decision driver (12%), up from 9% last year. This is worth noting in the context of the current quasi-discussion about negative gearing! The fact that buying is cheaper than renting (10%), up from 8% last year influences the decision, as does forming a family (12%). The potential to access first home owner grants (FHOG) has reduced in importance as their availability has diminished (and that is a good think, because FHOG’s simply are another market distortion).

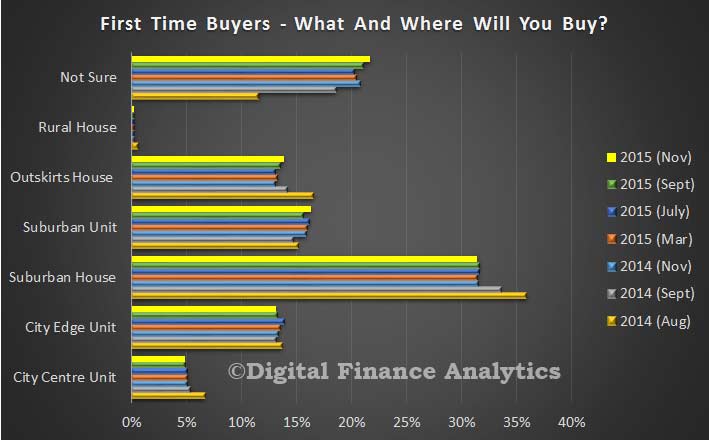

Many first time buyers are not all that sure where to buy, with a high 21% saying there is no simple choice. A significant proportion (33%) will look for a unit whilst nearly 60% still want to buy a house.

Most prospective first time buyers going direct to the investment sector are seeking to buy a unit, as the purchase price will be significantly lower. Purchasing preference is spread from CBD (12%), city fringe (35%) and suburban outskirts/regional centres (23%). Underlying this is a strong motivation to get onto the housing escalator anyway they can. We also noted that around 35% of prospective first time buyers were expecting to get help from the wider family to assist in the purchase, so the “bank of mum and dad” remains an important factor in the first time buyer equation. Yesterday we highlighted that more than half of prospective first time buyers believe house prices will continue to rise – so they wish to transact to avoid seeing prices move further against them and to enjoy capital appreciation at a time when interest rates are really low. Property purchase is hard wired into the Australian psyche.

Finally, there are a number of barriers first time buyers are encountering. More than half think property prices are too high (this has been pretty constant in recent surveys), 22% said they were having difficulty finding a place to buy (lack of supply, and competition with investors – both local and overseas) and around 5% said that they are finding it difficult to get finance. This reflects tightening lending criteria and flat incomes in real terms and is a marked change from last year. More than 60% of first time buyers will be consulting a mortgage broker to assist with finding a loan.

Next time we will do a deep dive on the refinancing sector.

Continuing our analysis of the latest DFA household survey of property drivers and expectations, today we look at the First Time Buyer segment. For those wanting to buy, but are unable to do so, the main barriers remain high house prices, and costs of living (no surprise given static real income growth). However, we also see a spike in availability of funding as a barrier, compared with a couple of months ago. Lending criteria may be getting tighter for some. We also see fears of unemployment receding in the eastern states, though it was a little higher this time in WA.

So then, looking at those who are actively seeking to buy for the first time, more than 20% are unsure of the type of property they can find. Overall houses, are preferred but we see units very much in the frame, especially in the eastern states, in and around the main urban centres. There are more units available (resale and new construction) than houses in these areas, and prices for units will be a little lower.

For those actively seeking to buy for the first time, prices are the major barrier, most seem able still to get finance if they do find a place to buy.

One final perspective, from our earlier research, we are seeing some reduction in the absolute number of first time buyers going direct to the investment sector (the red line), but it is still a very significant factor. It is still a logical approach for some, to gain access to the housing market, perhaps by buying a cheaper place to rent and hoping for capital gains and tax breaks, though of course interest rates have risen in the investment mortgage sector, and prospective buyers are likely to be buying into very full (some would say precarious) prices. For many it is a dilemma, will prices continue to rise (in which case they need to get in now) or will prices begin to correct (in which case it is better to wait, to avoid the pitfalls of negative equity)? Given yesterday’s comments, waiting a bit may be the more sensible path as the property worm is turning, especially in the eastern states.

More next time on the other segments in our surveys. You can read our last Property Imperative Report which summaries the state of play as at September 2015. This post updates some of the data in that report.

Allowing first homebuyers to cash out their super to buy a home is a seductive idea with a long history. Like the nine-headed Hydra, which replaced each severed head with two more, each time the idea is cut down it seems to return even stronger.

Both sides of federal politics took proposals to the 1993 election to let Australians draw down their super. After re-election, then Prime Minister Paul Keating scrapped it amid widespread criticism. Former Treasurer Joe Hockey raised the idea again in March and was roundly criticised by academics and the media. This month the Committee for Economic Development of Australia (CEDA) has again resurrected the idea.

House prices have skyrocketed again over the past two years, particularly in Sydney. So politicians are attracted to any policy that appears to help first homebuyers to build a deposit. Unlike the various first homebuyers’ grants that cost billions each year, letting first homebuyers cash out their super would not hurt the budget bottom line – at least, not in the short term. But the change would worsen housing affordability, leave many people with less to retire on, and cost taxpayers in the long run.

It is a bad idea for five reasons.

First, measures to boost demand for housing, without addressing the well-documented restrictions on supply, do not make housing more affordable. Giving prospective first homebuyers access to their superannuation will help them build a house deposit, but it would worsen affordability for buyers overall. Unless supply increases, more people with deposits would simply bid up the price of existing homes, and the biggest winners would be the people who own them already.

Second, the proposal fails the test of superannuation being used solely to fund an adequate living standard in retirement. The government puts tax concessions on super to help workers provide their own retirement incomes. In return, workers can’t access their superannuation until they reach a certain age without incurring tax penalties.

While paying down a home is an investment, owner-occupiers also benefit from having somewhere to live without paying rent. These benefits that a house provides to the owner-occupier – which economists call housing services – are big, accounting for a sixth of total household consumption in Australia. Using super to buy a home they live in would allow people to consume a significant portion of the value of their superannuation savings as housing services well before they reach retirement.

Third, most first homebuyers who cash out their super would end up with lower overall retirement savings, even after accounting for any extra housing assets. Owner-occupiers give up the rent on their investment. With average gross rental yields sitting between 3% and 5% across major Australian cities, the impact on end retirement savings can be very large. Consequently, owner-occupiers will tend to have lower overall lifetime retirement savings than if the funds were left to compound in a superannuation fund

Frugal homebuyers might maintain the value of their retirement savings if they save all the income they no longer have to pay as rent. In reality, few will have such self-discipline. Compulsory savings through superannuation have led many people to save more than they would otherwise. A recent Reserve Bank study found that each dollar of compulsory super savings added between 70 and 90 cents to total household wealth. If first homebuyers can cash out their super savings early to buy a home that they would have saved for anyway, then many will save less overall.

Fourth, the proposal would hurt government budgets in the long run. Superannuation fund balances are included in the Age Pension assets test. The family home is not. If people funnel some of their super savings into the family home, gaining more home equity but reducing their super fund balance, the government will pay more in pensions in the long-term.

Government would be spared this cost if any home purchased using super were included in the Age Pension assets test, but that would be very hard to implement. For example, do you only include the proportion of the home financed by superannuation? Or would the whole home, including principal repayments made from post-tax income, be included in the assets test? The problems go away if all housing were included in the pension assets test, but this would be a very difficult political reform.

Fifth, early access to super for first homebuyers could make the superannuation system even more unequal than it is today. Many first homebuyers are high-income earners. Allowing them to fund home purchases from concessionally-taxed super would simply add to the many tax mitigation strategies that already abound.

Consider the case of a prospective homebuyer earning A$200,000. Their concessional super contributions are taxed at 15%, rather than at their marginal tax rate of 47%. Once they buy a home, any capital gains that accrue as it appreciates are tax-free, as are the stream of housing services that it provides. Such attractive tax treatment of an investment – more generous than the already highly concessional tax treatment of either superannuation or owner occupied housing – would be prone to massive rorting by high-income earners keen to lower their income tax bills.

What, then, should the federal government do to make housing more affordable?

Prime Minister Malcolm Turnbull has tasked Jamie Briggs with rethinking policy for Australia’s cities.Mick Tsikas/AAP

Helping fix our cities

Above all, new federal Minister for Cities Jamie Briggs should support policies to boost housing supply, especially in the inner and middle ring suburbs of major cities where most people want to live, and which have much better access to the centre of cities where most of the new jobs are being created. The federal government has little control over planning rules, which are administered by state and local governments. But it can use transparent performance reporting, rewards and incentives to stimulate state government action, using the same model as the National Competition Policy reforms of the 1990s.

Other reforms, such as reducing the 50% discount on capital gains tax and tightening negative gearing, would also reduce pressure on house prices and could be implemented straight away. Such favourable tax treatment drives up house prices because it increases the after-tax returns to housing investors. The number of negatively geared individuals doubled in the 10 years after the capital gains tax discount was introduced in 1999. More than 1.2 million Australian taxpayers own a negatively geared property, and they claimed A$14 billion in net rental losses in 2011-12.

There are no quick fixes to housing affordability in Australia. Yet any government that can solve the problem by boosting housing supply in inner and middle suburbs, while refraining from further measures to boost demand, will almost certainly find itself rewarded, by voters and by history.

Authors: Brendan Coates, Senior Associate, Grattan Institute; John Dale, John Daley is a Friend of The Conversation, Chief Executive Officer , Grattan Institute.

The fall is driven partly by prices continuing to accelerate out of reach, with 51% saying their target was now more out of reach than a year ago, whilst 43% said there was no real change and 6% said prices has fallen. There were considerable state and regional variations. Prices in WA and areas of QLD are lower, whilst prices in NSW, VIC and ACT are significantly higher.

The fall is driven partly by prices continuing to accelerate out of reach, with 51% saying their target was now more out of reach than a year ago, whilst 43% said there was no real change and 6% said prices has fallen. There were considerable state and regional variations. Prices in WA and areas of QLD are lower, whilst prices in NSW, VIC and ACT are significantly higher. Finally, the combination of flat incomes, and tighter mortgage underwriting standards means that more than half – 58% – said they borrowing capacity had effectively been reduced. Around 40% said there was no change, and just 2% said their borrowing capacity had risen. Once again first time buyers in NSW and VIC were the most under pressure, thanks to high prices, and static incomes.

Finally, the combination of flat incomes, and tighter mortgage underwriting standards means that more than half – 58% – said they borrowing capacity had effectively been reduced. Around 40% said there was no change, and just 2% said their borrowing capacity had risen. Once again first time buyers in NSW and VIC were the most under pressure, thanks to high prices, and static incomes. No surprise therefore that the latest ABS statistics shows the number of first time buyers continuing to languish.

No surprise therefore that the latest ABS statistics shows the number of first time buyers continuing to languish.