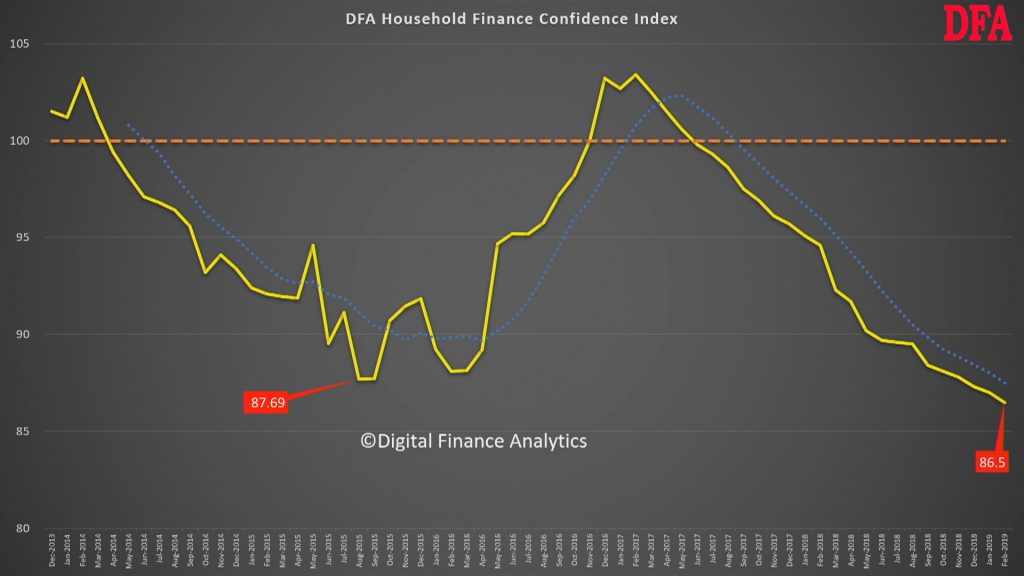

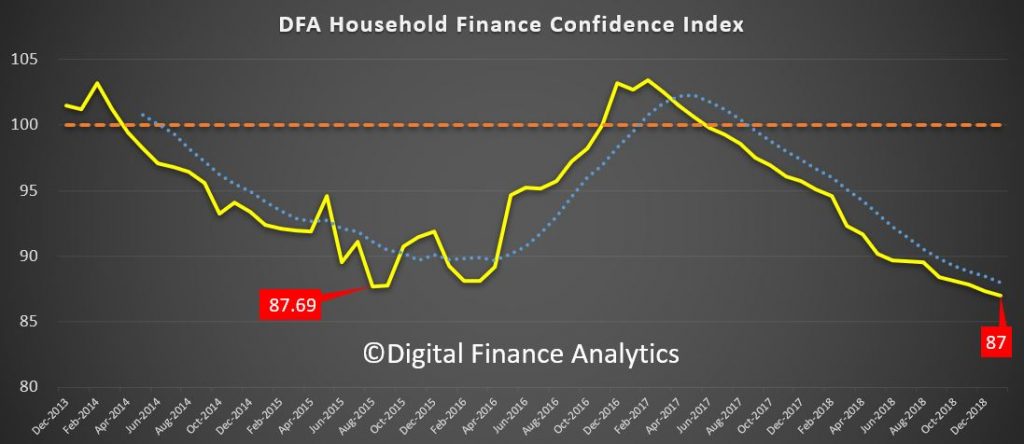

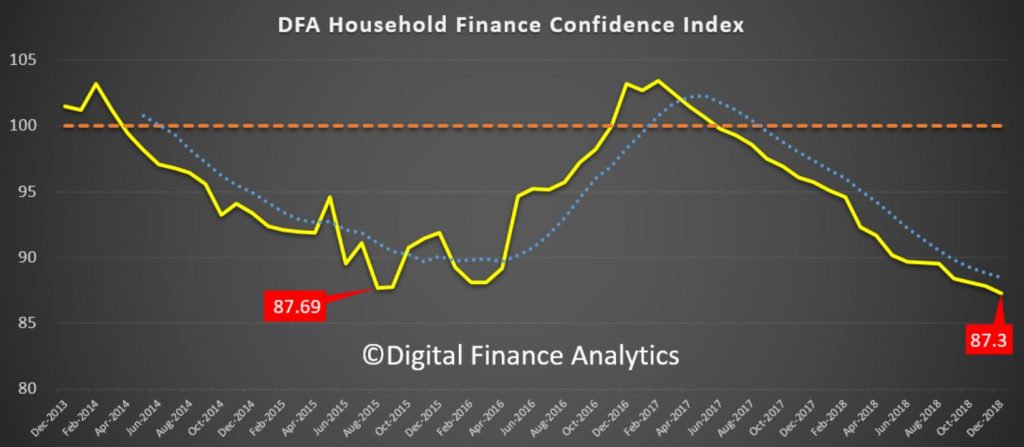

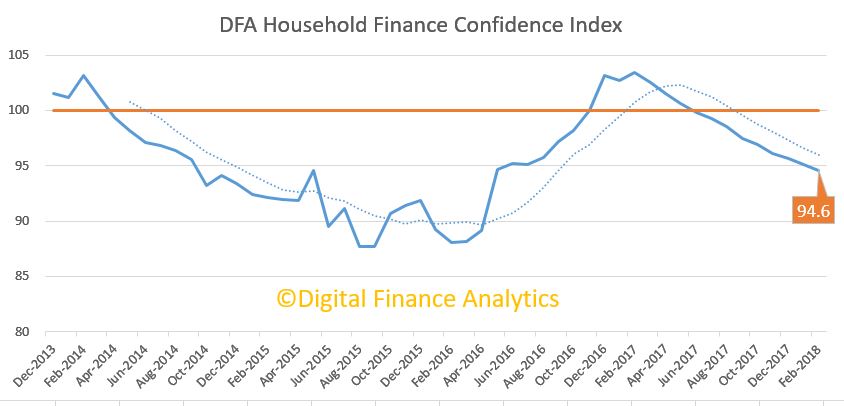

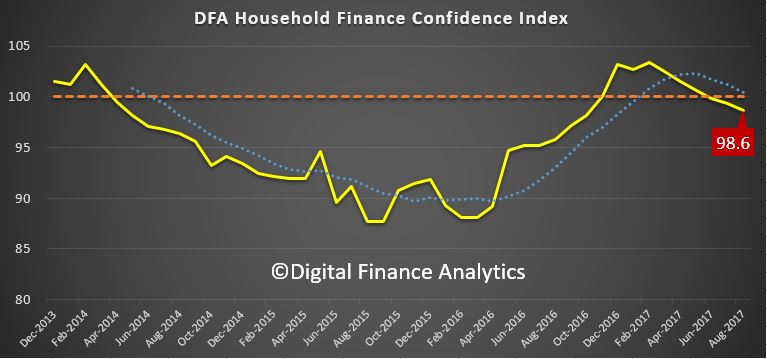

The latest from our household surveys reveals a further fall in household confidence, with the data to end February 2019.

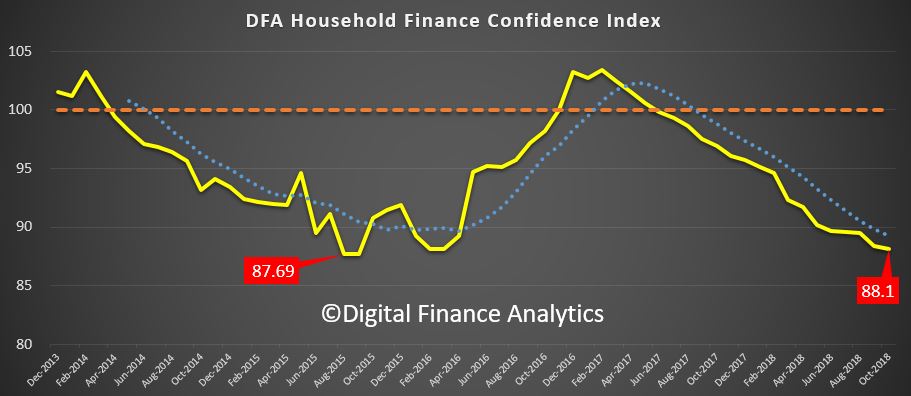

The overall index fell to 86.5, the lowest since we have run the series.

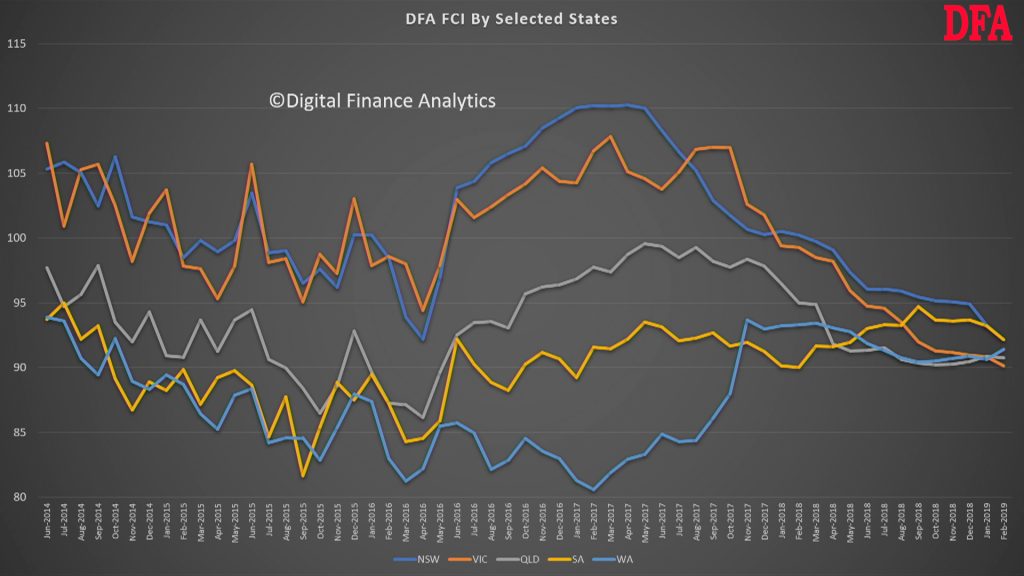

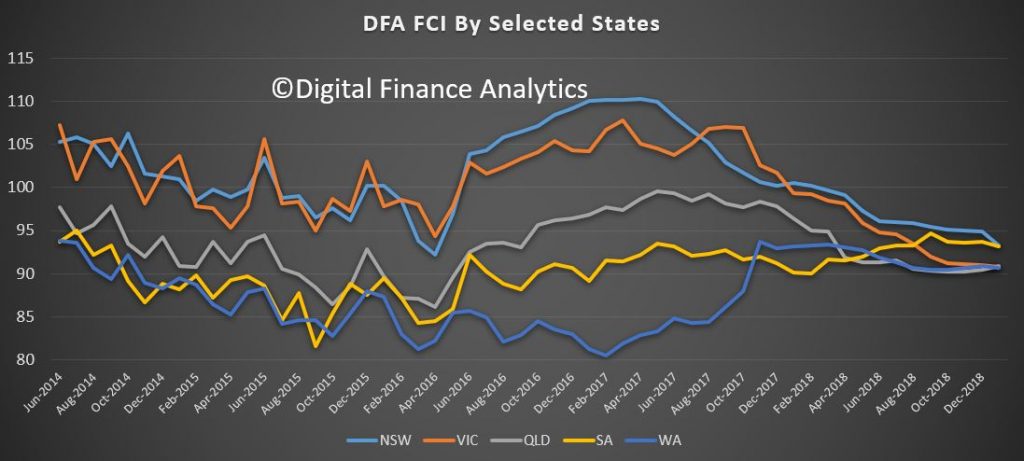

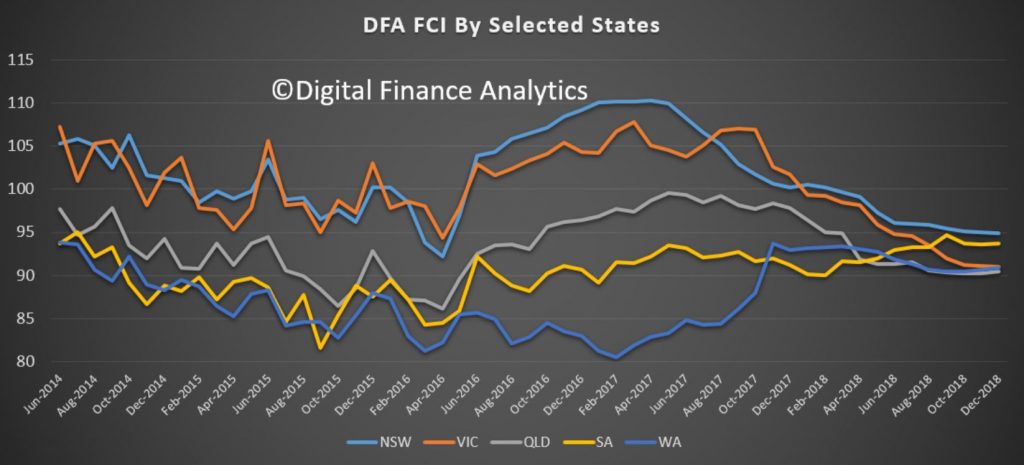

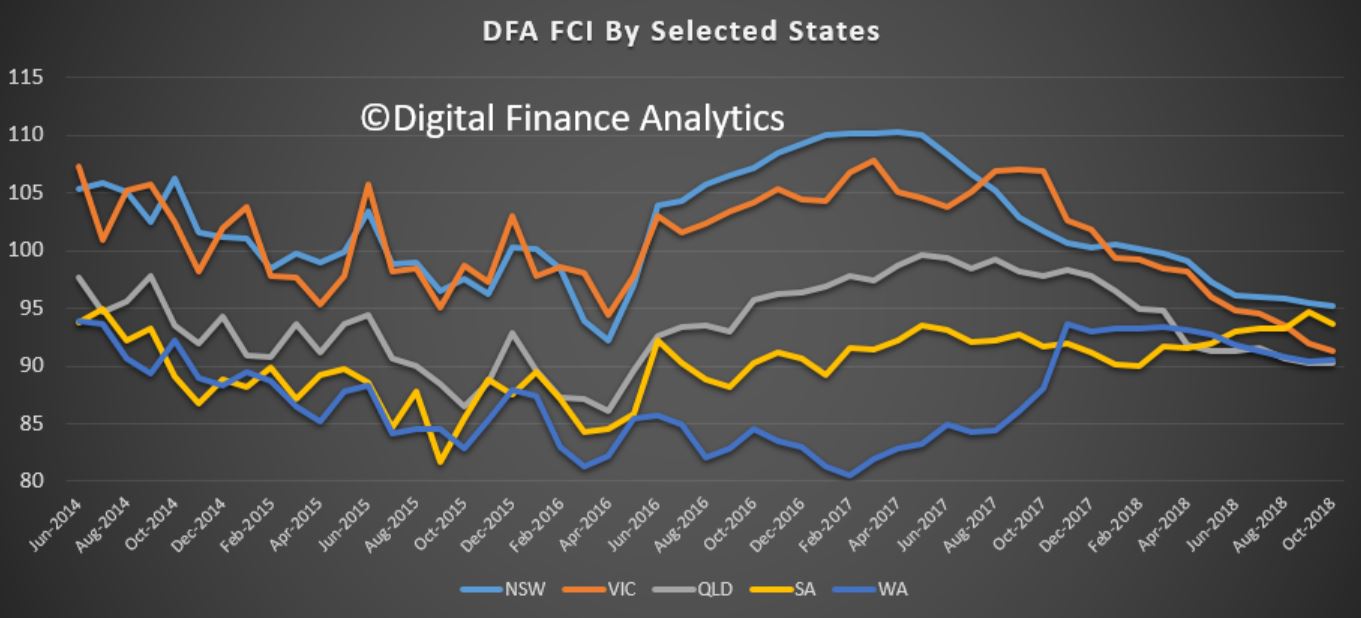

The state indices have converged at a level below the neutral setting.

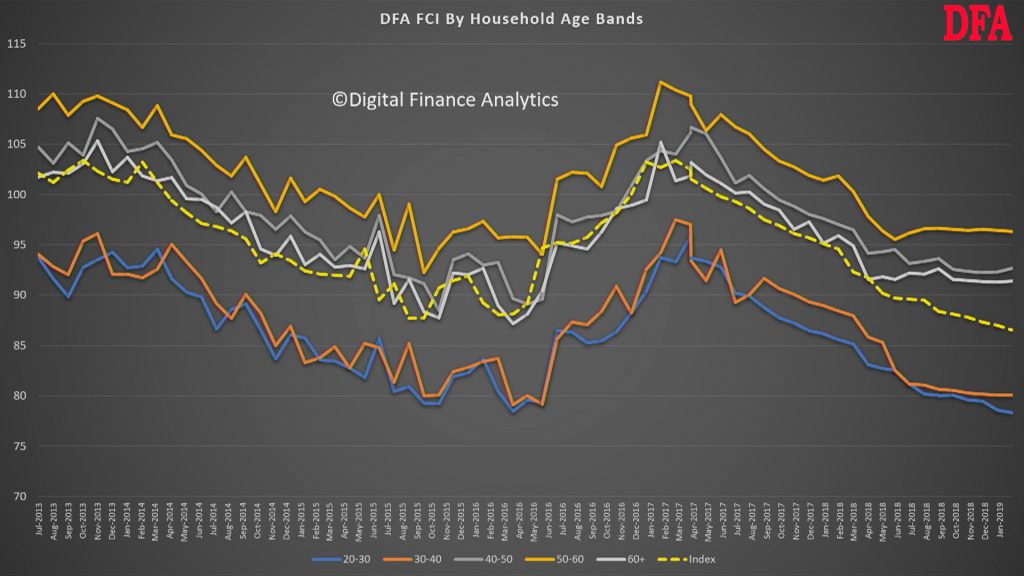

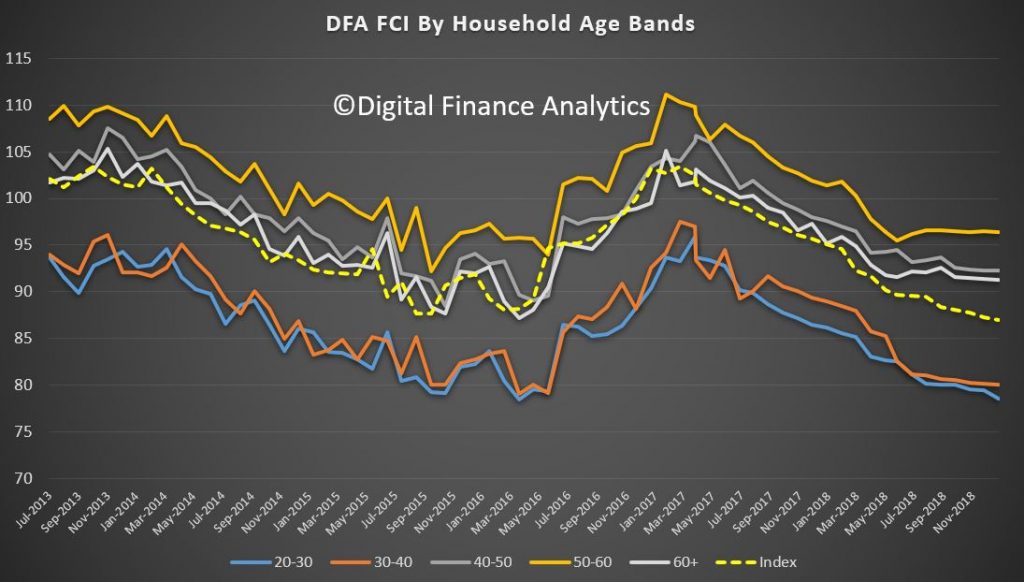

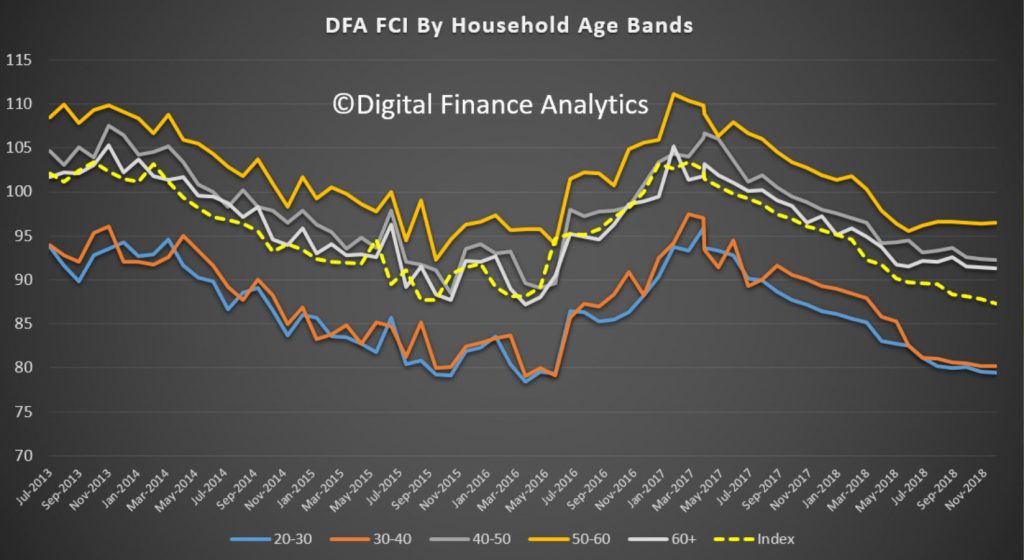

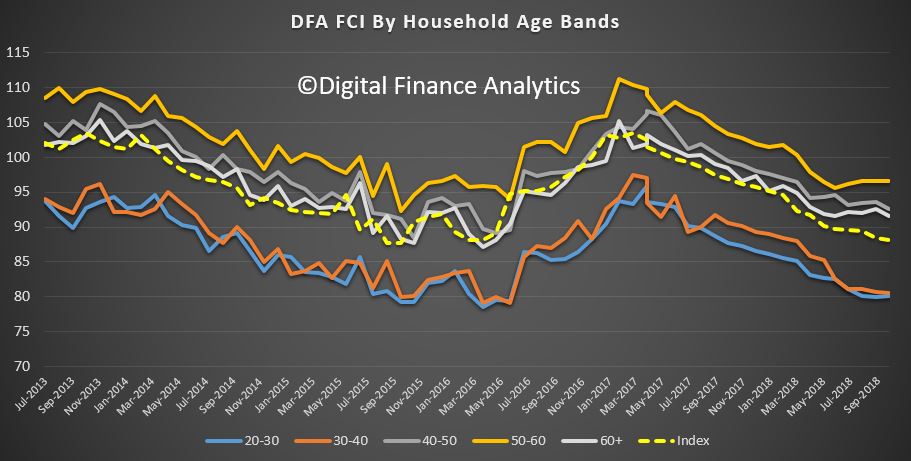

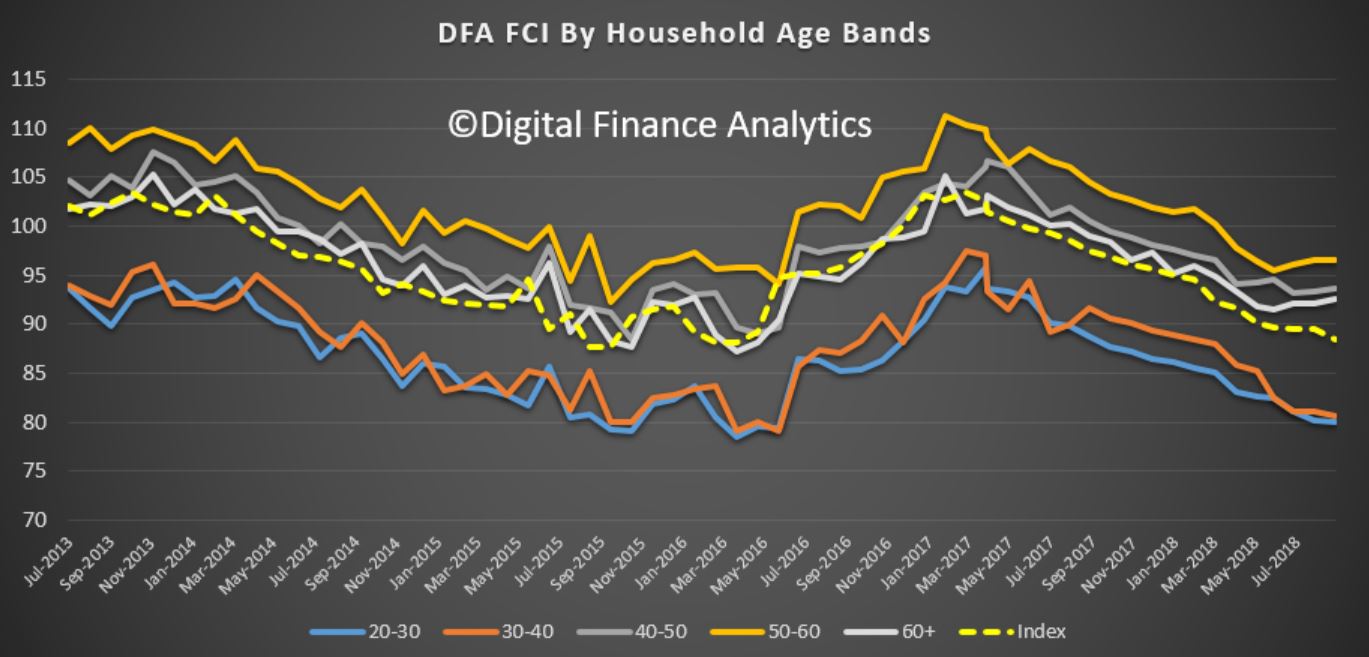

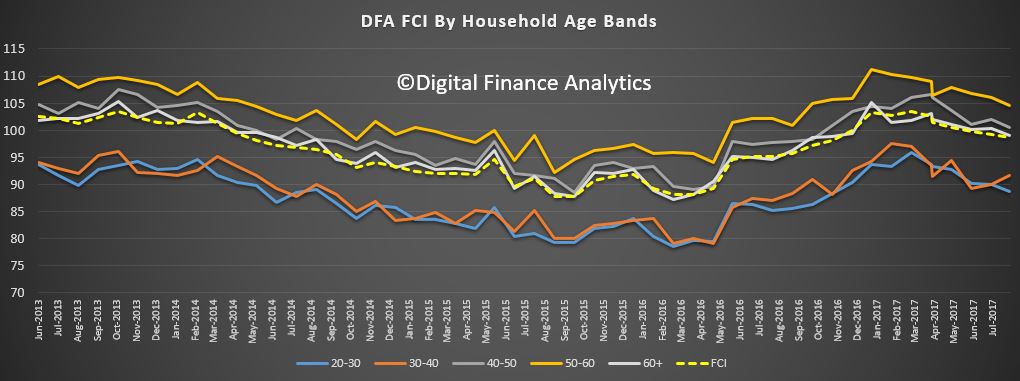

The age groups continue to show younger households are less confident, thanks to low wages growth, high costs and rents or mortgage repayments. Some older groups remain more confident.

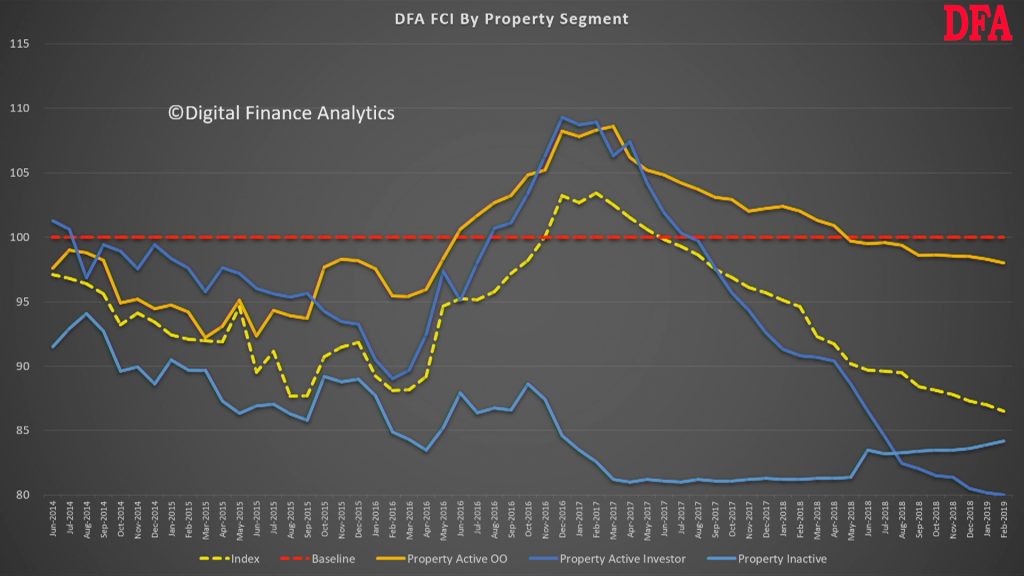

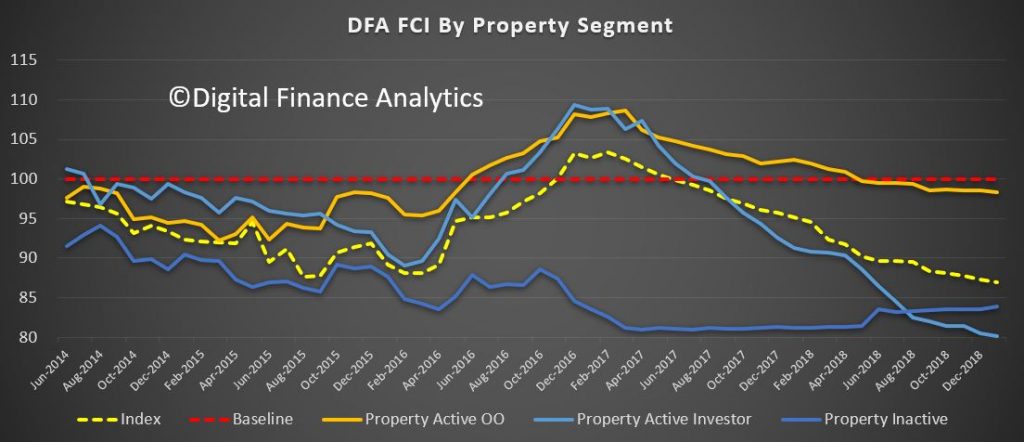

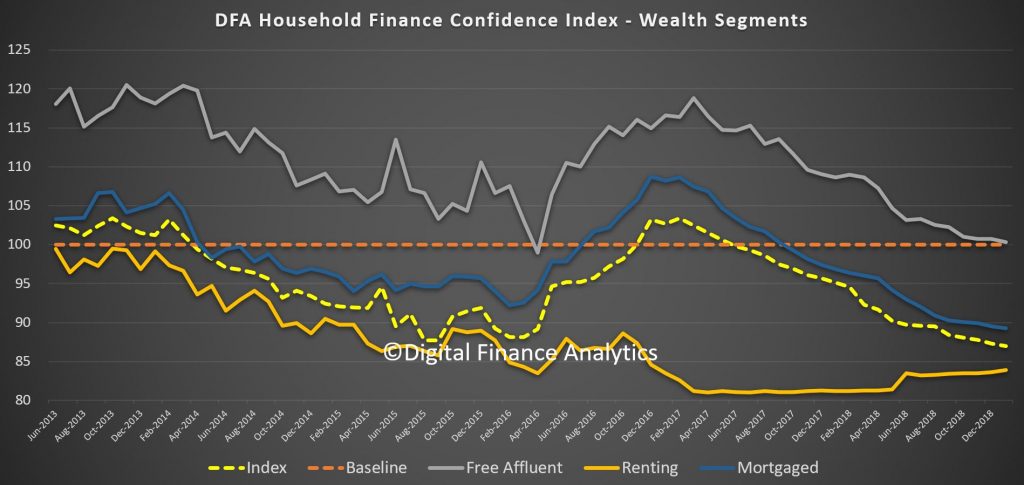

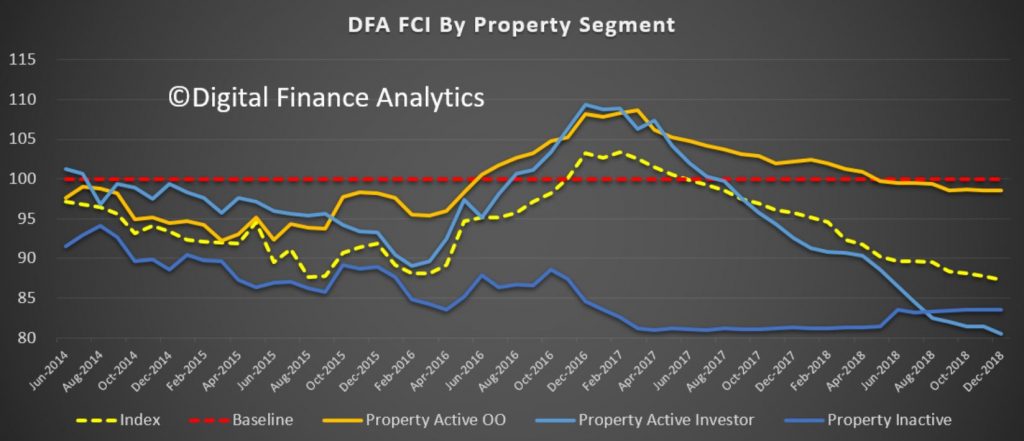

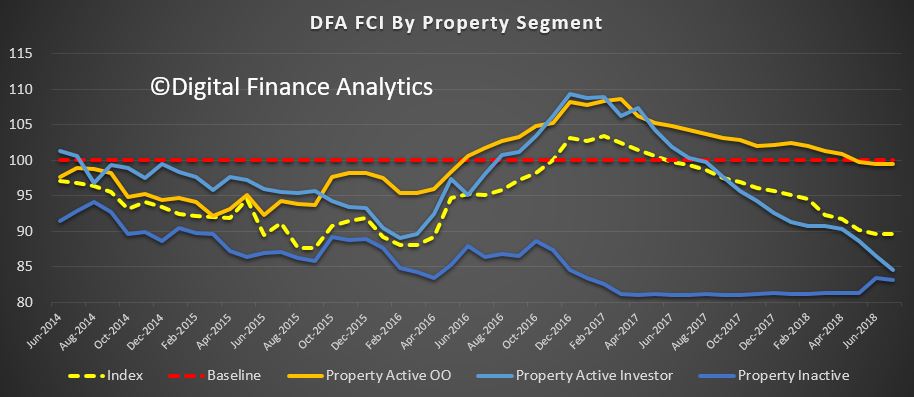

Property investors continue to struggle, though owner occupied owners are relatively more confident, even if below the neutral setting.

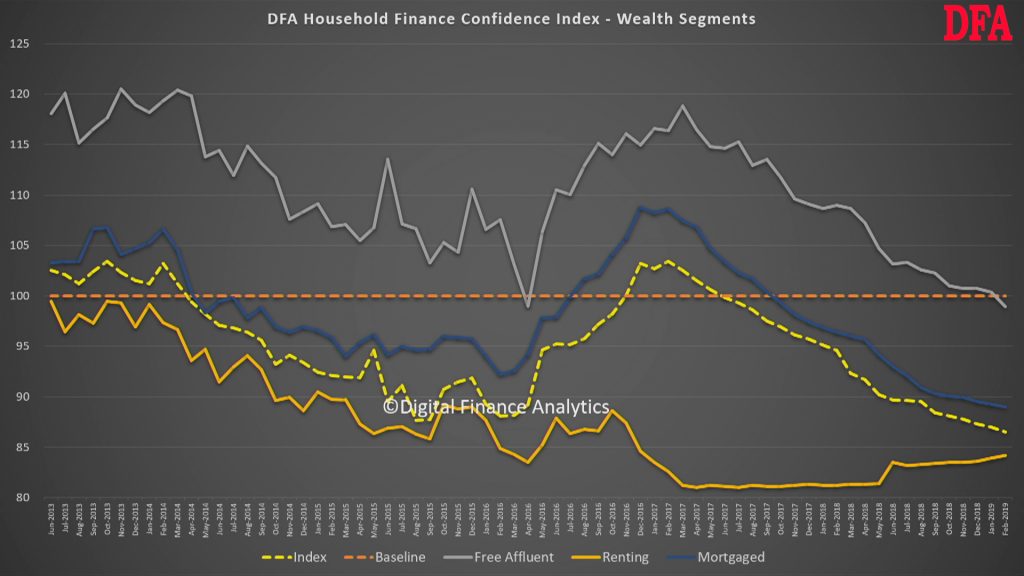

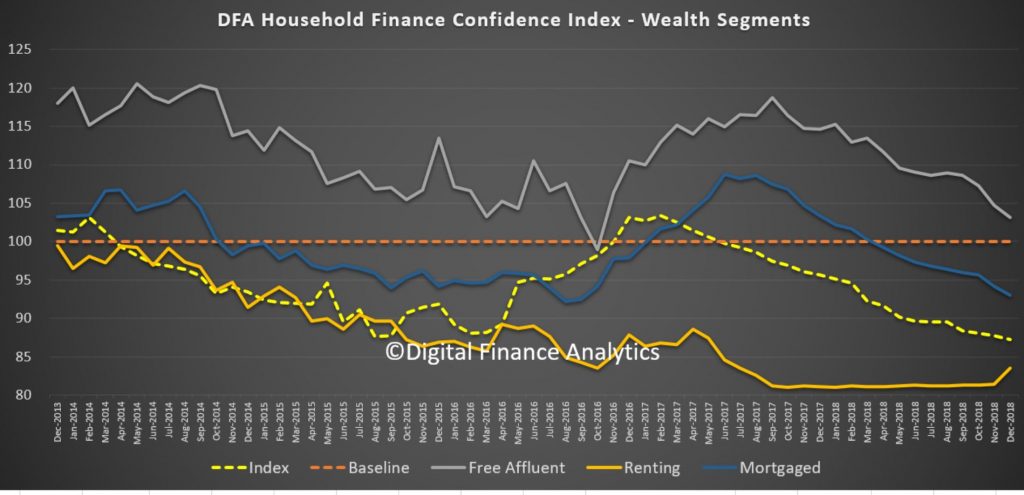

And all wealth segments are now in negative territory.

We review the moving parts in the index in the video above.

This is starting to look serious as the latest DFA household financial confidence index results for January 2019 reveals a further decline in levels of confidence.

The index fell to 87 in January, down from 87.3 in December, the lowest its been since the survey commenced, well below the neutral setting of 100.

By way of background, these results are derived from our household

surveys, averaged across Australia. We have 52,000 households in our

sample at any one time. We include detailed questions covering various

aspects of a household’s financial footprint. The index measures how

households are feeling about their financial health. To calculate the

index we ask questions which cover a number of different dimensions. We

start by asking households how confident they are feeling about their

job security, whether their real income has risen or fallen in the past

year, their view on their costs of living over the same period, whether

they have increased their loans and other outstanding debts including

credit cards and whether they are saving more than last year. Finally we

ask about their overall change in net worth over the past 12 months –

by net worth we mean net assets less outstanding debts.

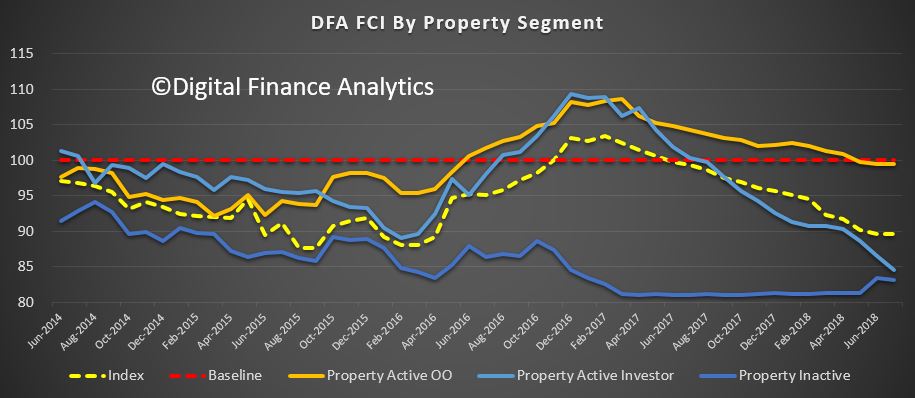

Looking at the results by property segments, we see a fall in confidence among property investors, as home prices and rental yields continue to fall, and reflecting concerns about potential changes to negative gearing and capital gains ahead. That said, purchase interest has risen a little. We will discuss this later.

Owner occupied borrowers are also feeling the heat, reflecting some mortgage price pain, as well as the basic affordability issues. Those renting however are a little more positive relatively speaking, thanks to rents being lower now and a greater choice of property for rent being available, especially in Sydney. Overall investors are the least confident now, a considerable switch from a year or so ago!

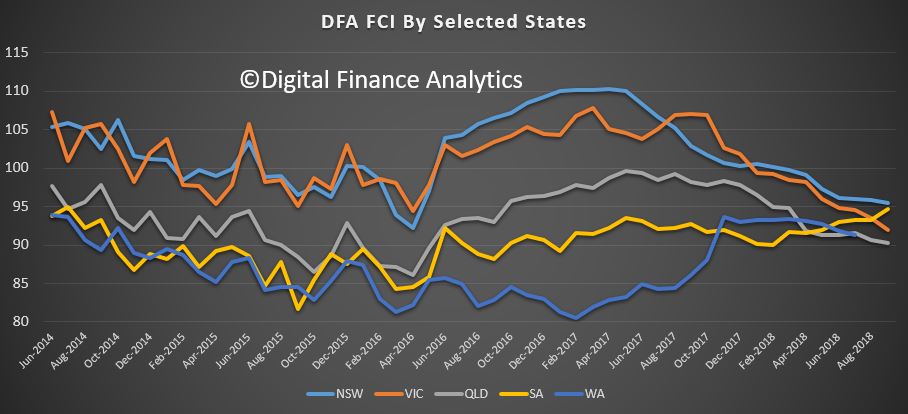

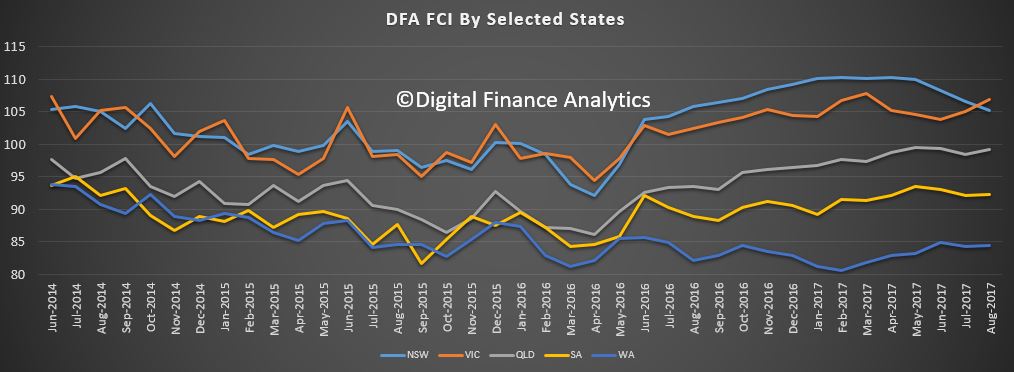

Cutting the data by states, we see that the bunching continues as property price falls in Sydney and Melbourne erode confidence there, relative to the other states. The most significant fall was in NSW, as home prices fall – and the fall out from Opal Tower had an impact more broadly on new purchases, and off the plan commitments.

Across the age ranges we continue to see weakness, with younger households more exposed, although those older households with share market investments saw a rebound in January, which boosted their confidence a little.

Turning to our wealth segments, we continue to see property owners without a mortgage the most confidence, though falling close to the long term neutral benchmark, while those with mortgages (either investor or owner occupied) continue to decline. Renters remain the least confident. This could become an important indicator in the run up to the next election, in that even those heartland voters supporting the incumbent Government are less positive than usual.

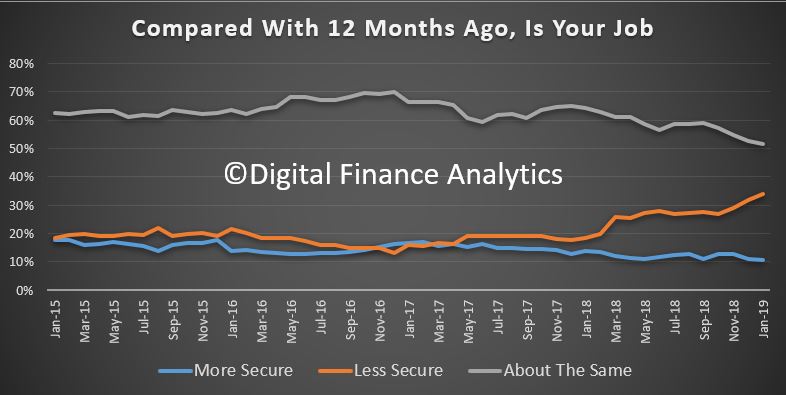

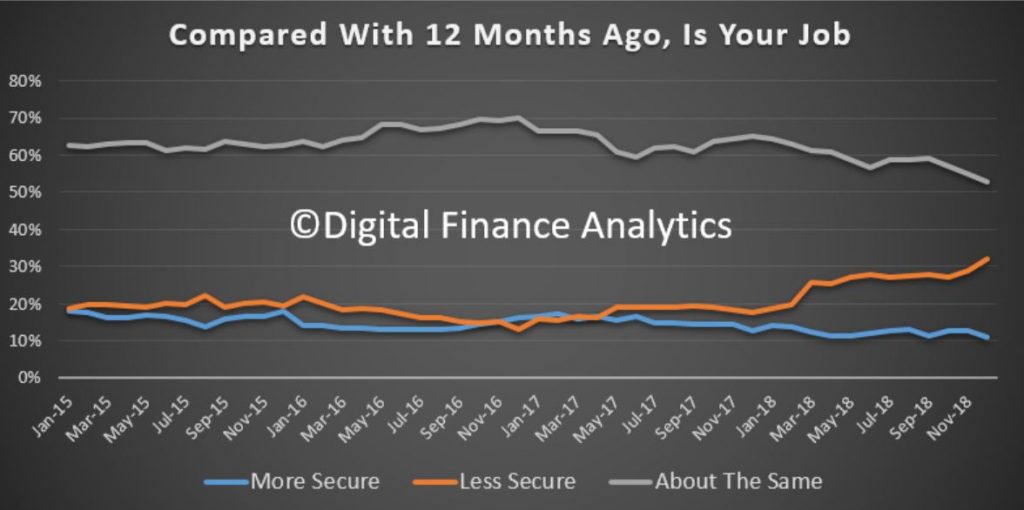

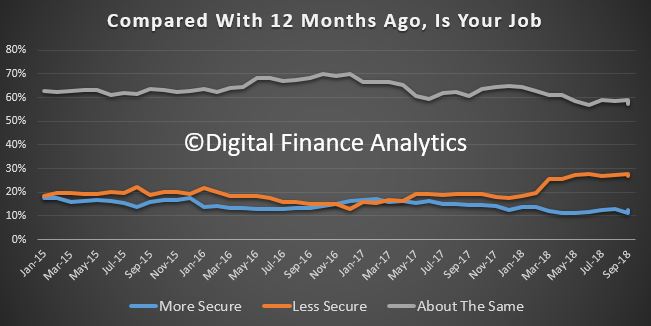

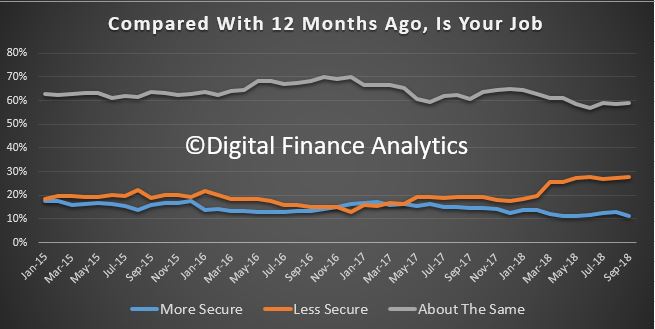

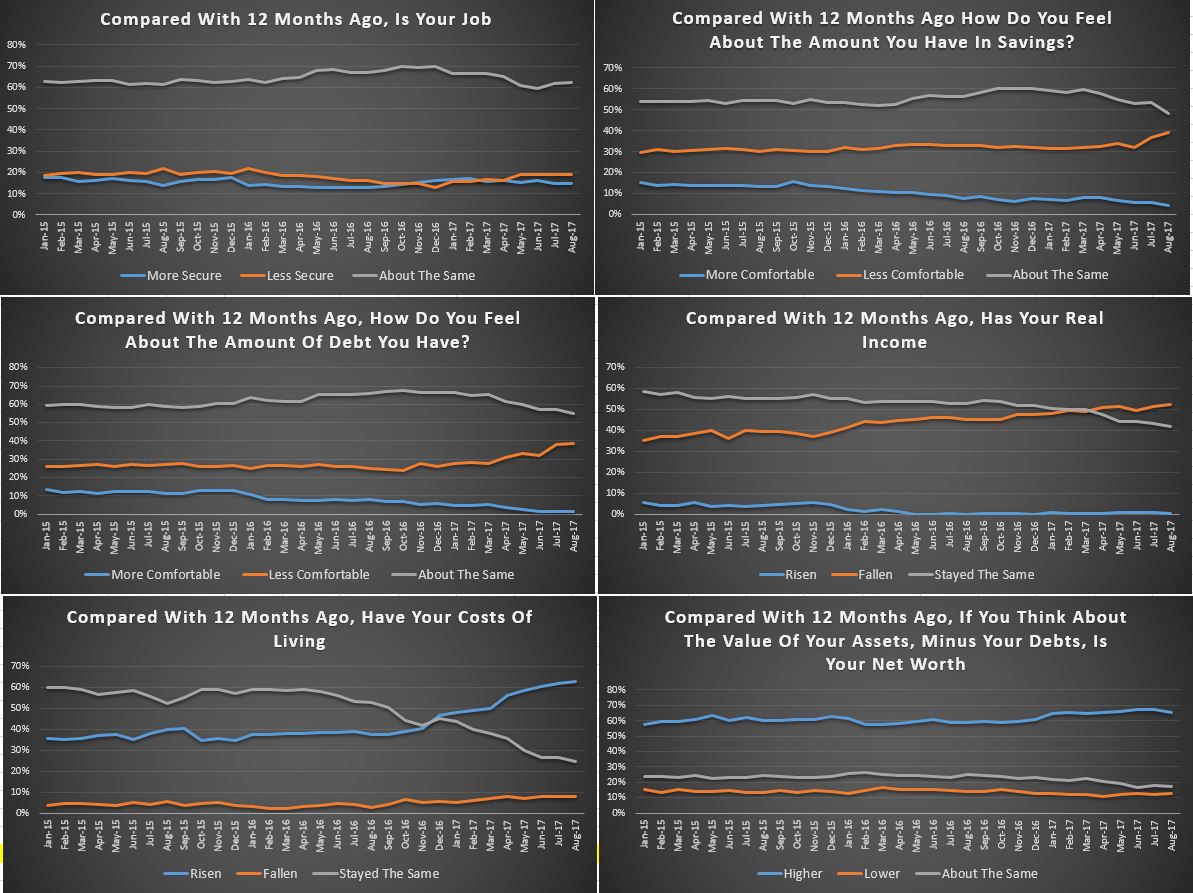

We can then examine the moving parts within the index. We start with job confidence. Those feeling more secure about their job prospects fell 2.19% to 10.57%, while those feeling less confident rose 4.84% to 33.85%. 51.68% saw no change, but that fell by 3.30%. There was a noticeable rise of concerns in the construction sector as building approval momentum falls.

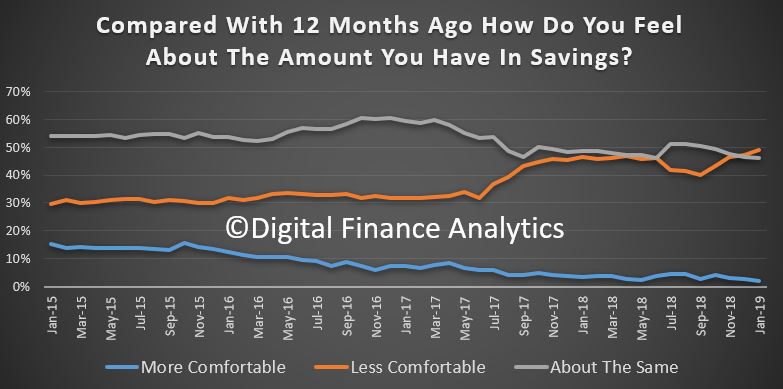

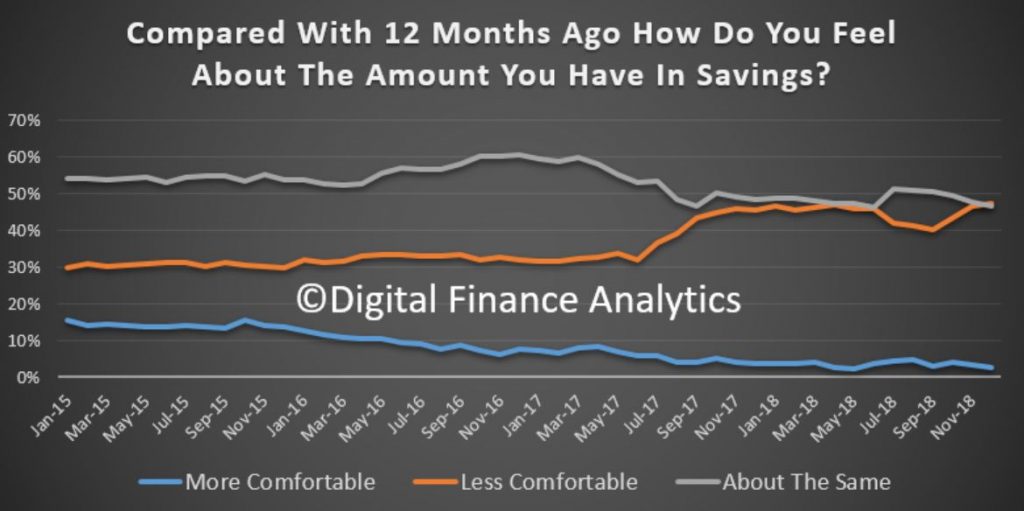

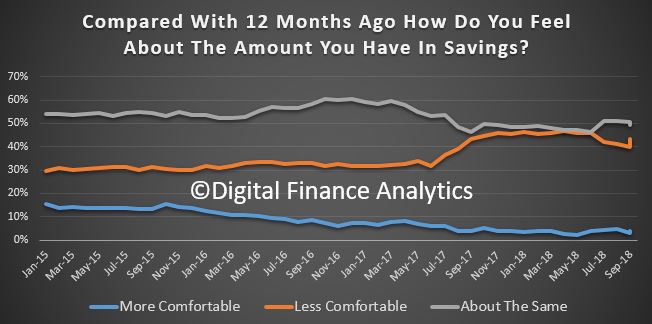

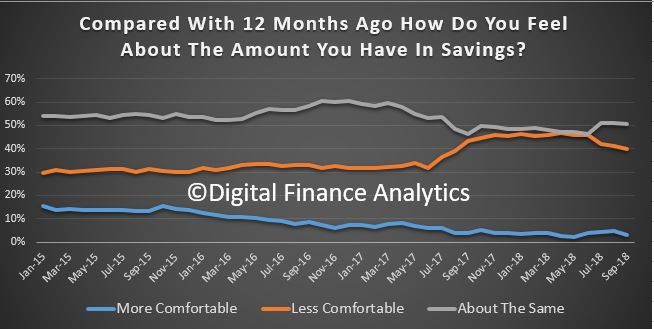

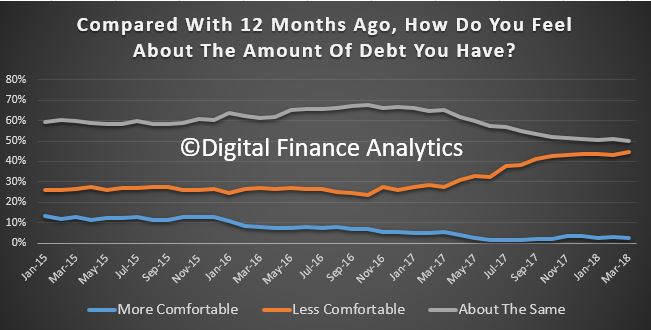

Savings rates continue to fall for many, and others are raiding what savings they have to maintain their lifestyles – something which of course cannot continue indefinably – one reason why the savings ratio continues to fall. June 1.98% of households were more comfortable than a year ago, down 1.28%, while 48.96% were less comfortable, a rise of 2.52%. 46.24% were about the same, down 1.56%.

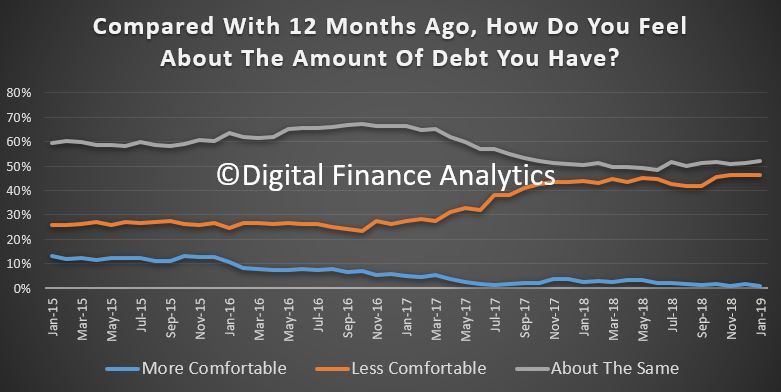

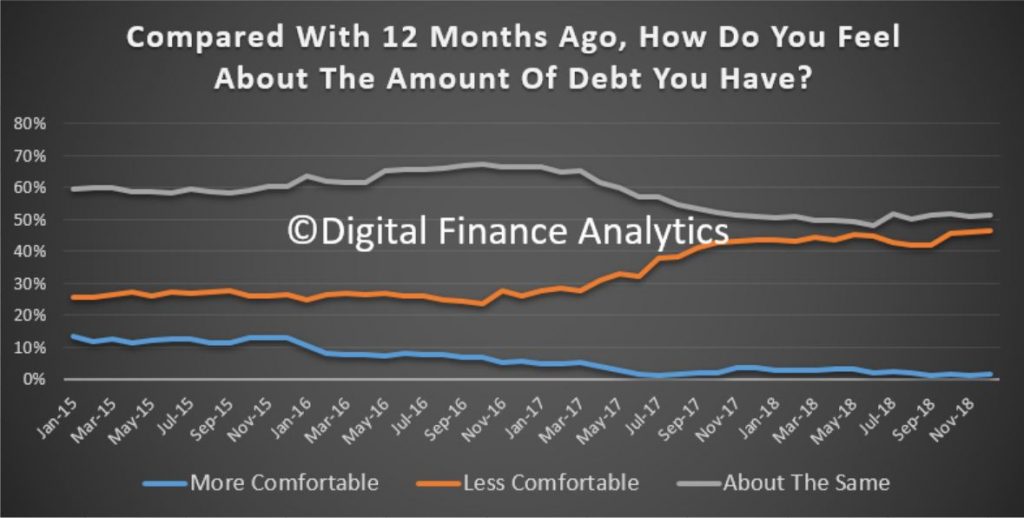

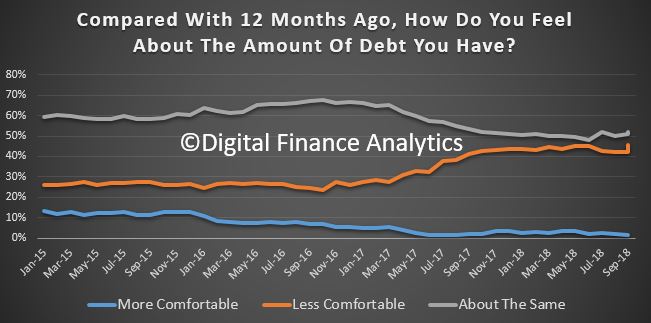

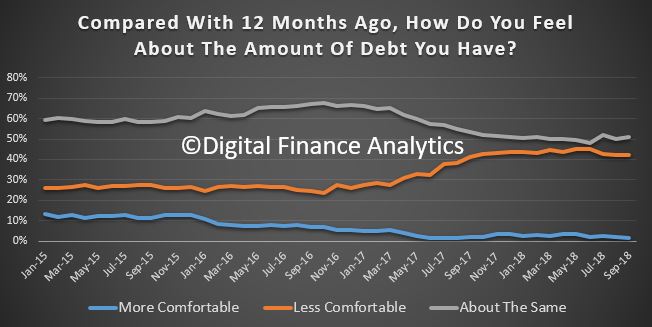

Turning to debt, 1.11% of households are more comfortable than a year ago, and 52% are about the same. 46% are less comfortable than a year back, thanks to rising rates, switches to interest and principal from interest only loans and problems in servicing the repayments. We also continue to see growth in quasi credit such as Afterpay, as well as other forms of short term credit. Household debt of course continues to rise faster than incomes or inflation.

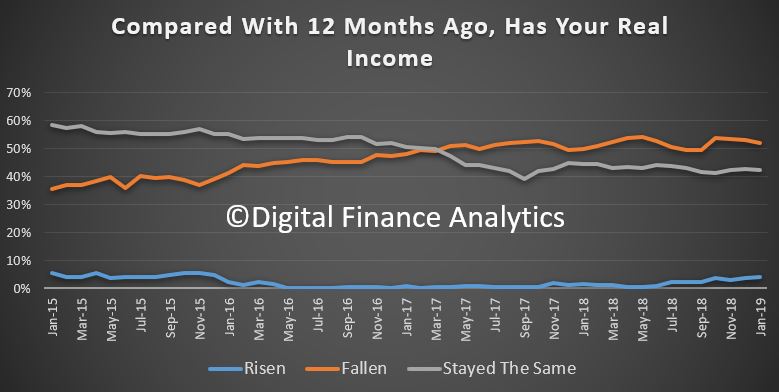

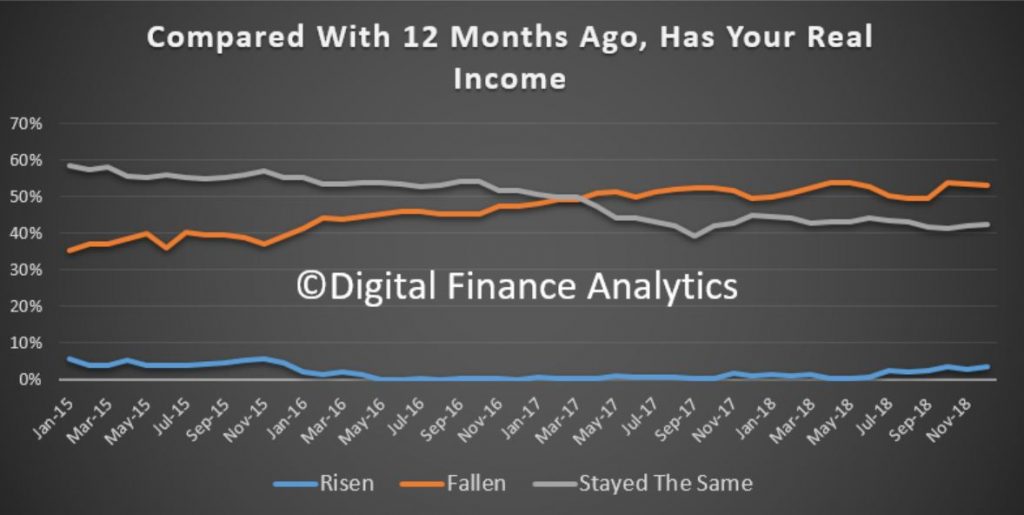

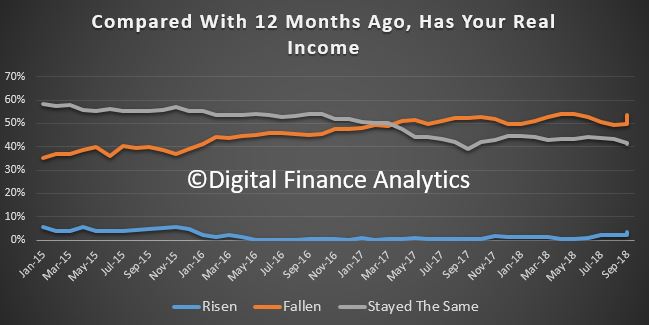

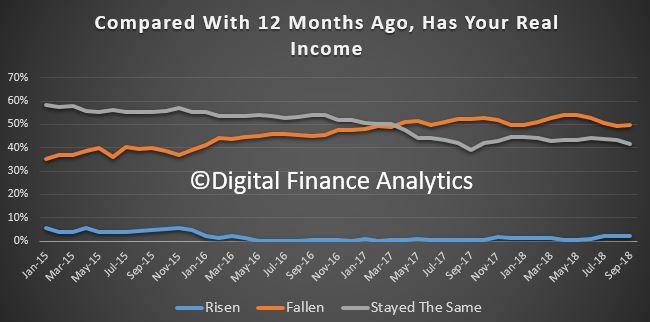

Income growth remains a real concern for many households (in real terms many have seen falls in recent years). 3.88% of households reported their real incomes had grown in the past year, 51.99% said incomes had fallen in real terms, and 42.5% said there had been no change. We continue to observe pressure on the income side of household balance sheets, despite the RBA’s expectation that wages will rise eventually. One bright spot was dividend payments which were higher, but this failed to offset the total picture.

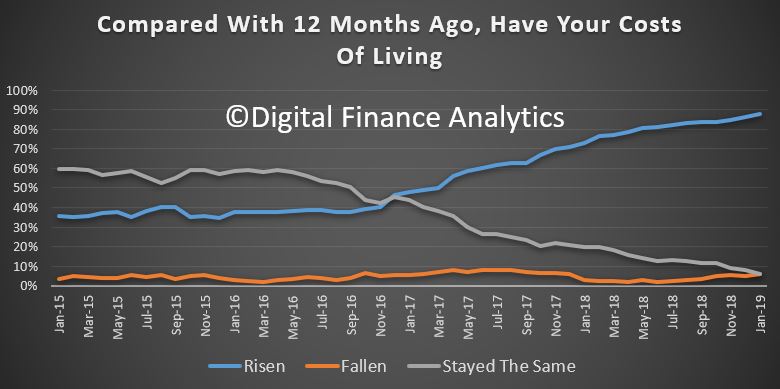

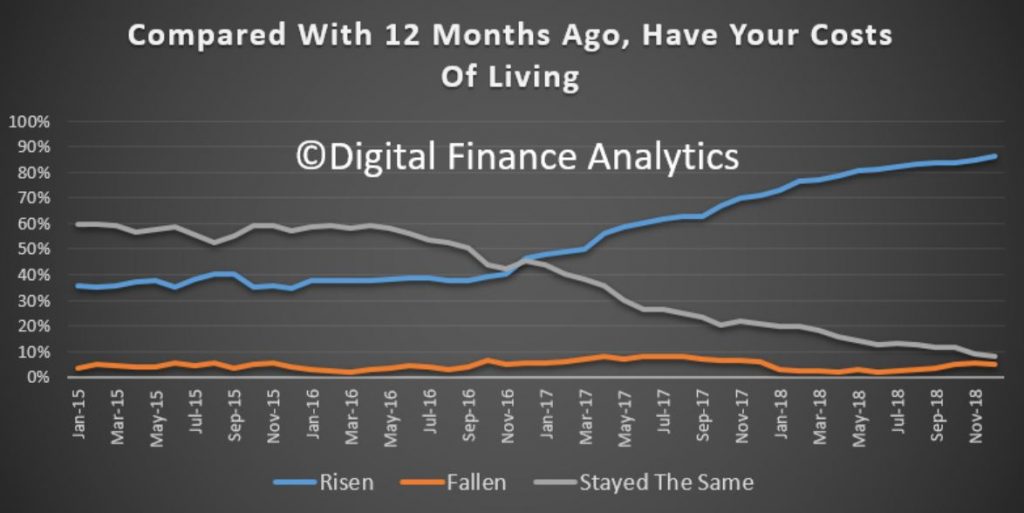

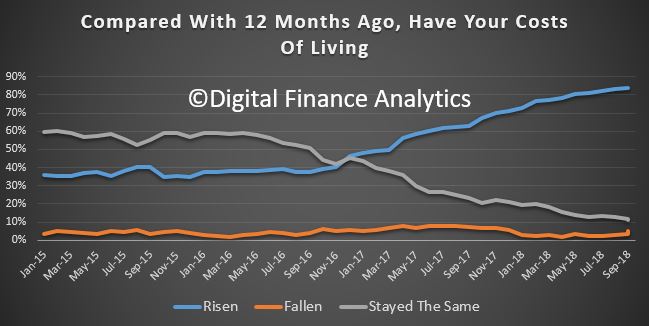

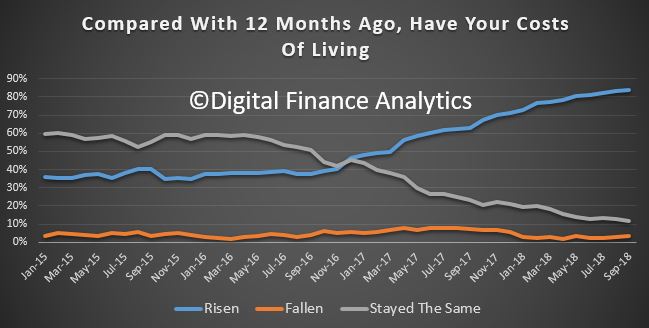

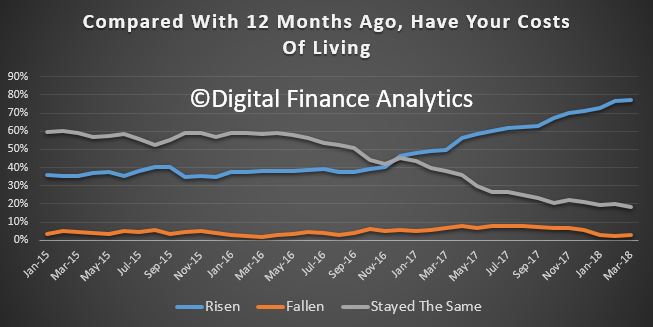

One of the killer categories is the costs of living. Once again we think the CPI figures just do not reflect the lived experience of many households. 87.75% said their costs had risen over the past year, up 3.2%. This includes the old favorites, electricity, child care, health care, and household staples, despite a fall in costs of fuel at the bowser.

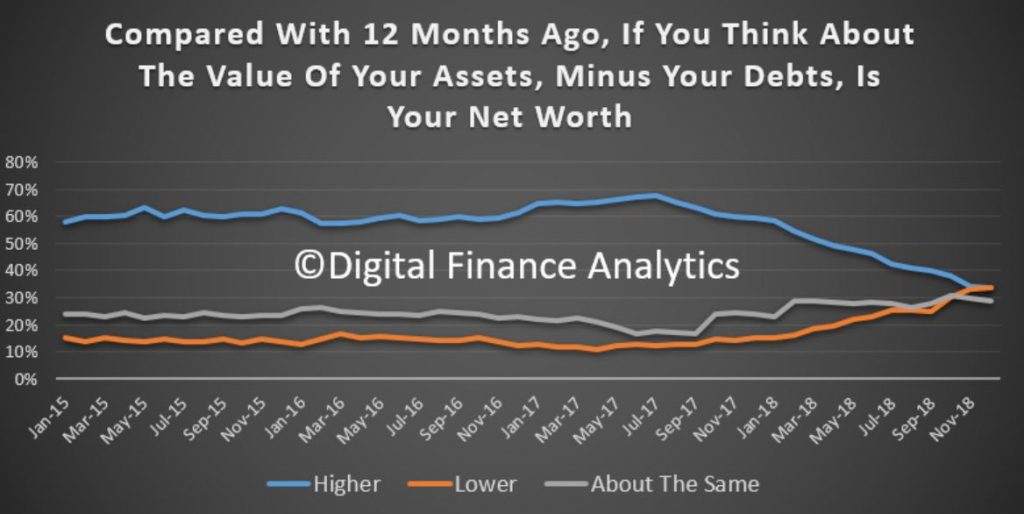

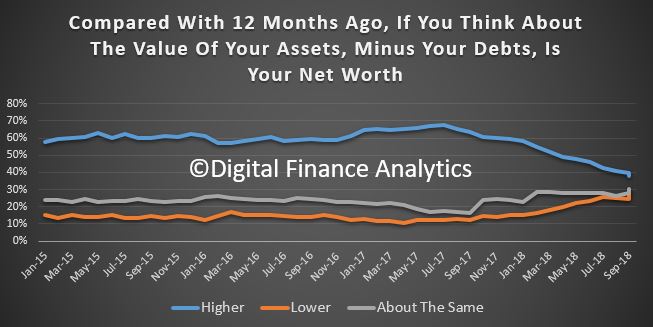

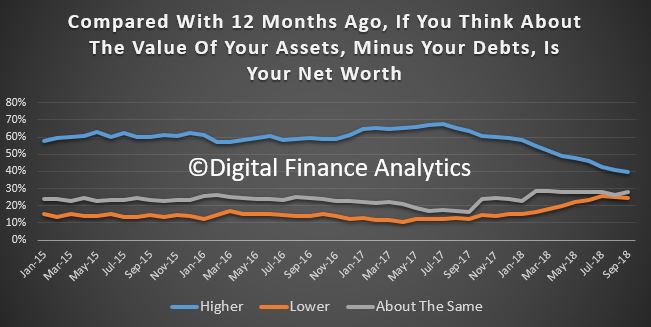

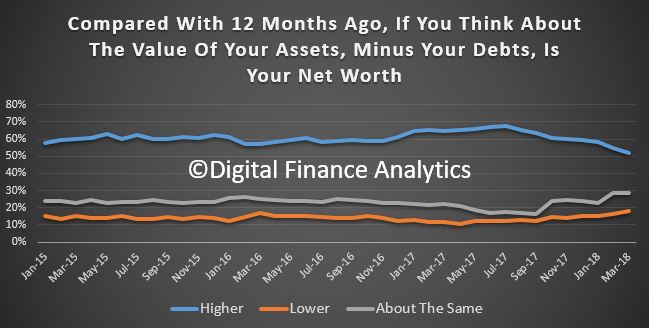

And finally, household net worth continues to take a dive thanks for falling home prices – this despite recent positive share price moves. Overall 32.18% of households sand their net worth had improved, down 1.82% from last month, 37.28% said their net worth had fallen, up 4.05% and 27.42% said there had been no change, down 2.52%.

One other interesting point which came out from the analysis is that potential property investors are more active now, thanks to the falls in asking prices, and importantly, the burning fuse with regards to ending negative gearing should Labor win the next election. Thus we have seen a rise in investors considering transacting. Some lenders are offering “special” fixed rate offers, in the light of APRA’s hands off approach, and of course Hayne did not do anything on responsible lending. The tighter underwriting standards are still in play of course – for now – but I would not bee surprise to see a kick up in new investor lending in the weeks ahead, despite the lower levels of financial confidence.

In summary then, interesting times as household finances are squeezed, yet the fixation on property for many Australians remains strong. There is still a belief that falls will be limited, and they will bounce back. We are not so sure!

Following on from our mortgage stress report for December 2018, which we released yesterday, we complete our monthly data series with the release of the December Household Financial Confidence Index, our gauge of how households are feeling about their financial situation.

The overall index fell again in December to an all-time low of 87.3 (which is strange given the Government’s assertion the economy is in fine fettle!

The DFA index can be segmented a number of different ways, to home in on which households are most concerned about the state of their finances. A significant factor is whether households are property owning, and whether they are mortgaged. Households who hold property, but no mortgage are the most confident and above the 100 neutral setting, although confidence in this group is falling. Those with a mortgage are well below the neutral measure, and confidence for this group continues to fall. Those in the rental sector, or living with friends or family are less confident, though recent wage rises and falling rents have had a slightly positive impact this month.

Within the property holding segment, we can also separate property investors from owner occupied households. Significantly property investors have gone very negative now, thanks to falling property prices, rising mortgage costs and issues with mortgage refinancing. The threats to negative gearing are also in play. Concerns about rising mortgage rates are building (Bank of Queensland moved yesterday!). Owner occupied property holders are more positive, those with mortgages and those mortgage free are both within this segment. Property inactive households – those with no exposure to property – are slightly more confident than property investors.

We can also examine the data across the main states. When we do that we find a “bunching” of scores, as NSW and VIC come off their highs (the main centres in which property prices are falling).

South Australian households have remained more positive, while Victorian households have taken something of a dive -as prices are moving south at a faster clip. And we can also look at the age band data.

Here, younger households remain the least confident, and the general slide continues across the age bands, other than those aged 50-60 – who are less likely to hold mortgages, so more likely to reside in the “Free Affluent” segment.

We can then look at the data drivers for the index.

Job security shows a spike in those feeling less secure, up 3% – and workers in the construction and real estate sectors have become more concerned. There was a fall of 1.7% in those feeling more secure than a year ago, at 11%. 53% of households reported no change than a year ago, down 2%.

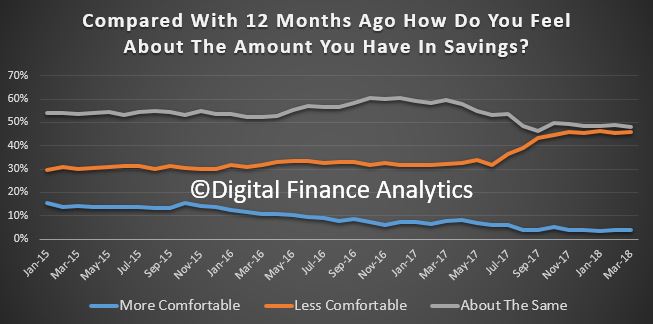

Savings are taking a beating, with more households tapping to savings to sustain their budgets, and also being hit by falls in interest rates on deposits and falls/volatility in the share markets. 2% only, are more comfortable than a year ago, 46% less comfortable, and 51% about the same.

Debt remains a major source of concern for many households. Whilst overall personal credit (other than for mortgages) is falling there are credit hot spots where households under pressure are putting more on credit cards, using staged repayment products like Afterpay, or even Payday loans. Many households are finding their large mortgages more difficult to handle (as reflected in our stress reports). Around 1.5% of households are feeling more comfortable than a year ago, 46% less comfortable and 51% about the same.

Household income remains under pressure, with many reporting no increase in real incomes in the past 5 years. Many households are working multiple jobs, and are still underemployed. In addition, the interest on deposits held with the banks have fallen significantly, as they trim their interest rates to protect their margins. 4% said their income in real terms had risen, 53% said it had fallen and 43% said there was no change.

Households reported continued rising living costs in December with and additional 1.5%, or a total of 86% saying costs, in real terms had risen. 5% said they had fallen and 8% said there was no change. As well as the usual suspects – higher electricity costs, health care, child care and some food costs, a number of households reported rises in land tax as a concern. Once again the official CPI seems disconnected from the true experiences of many households, costs continue to rise and fast!

Finally, we look at Net Worth – Assets less loans owning. We see a rise in those reporting a fall, directly associated with the fall in home prices, 34% said their net worth had dropped in the past year, 33% said it had improved, and 29% said it was about the same. So whilst for some the “wealth effect” is intact, one third are feeling the effects of a reduction in wealth on paper, and as a result they are more cautious on their planned spending. This is sufficient to slow consumption ahead, and may well impact GDP as a result.

In summary then, we continue to see the same forces in play, in that as home prices slide and costs rise, household finances are under pressure. But the effects are not uniform, those with mortgages, and younger are most impacted. But the recent stock market ructions and lower returns on deposits are also biting.

By way of background, these results are derived from our household

surveys, averaged across Australia. We have 52,000 households in our

sample at any one time. We include detailed questions covering various

aspects of a household’s financial footprint. The index measures how

households are feeling about their financial health. To calculate the

index we ask questions which cover a number of different dimensions. We

start by asking households how confident they are feeling about their

job security, whether their real income has risen or fallen in the past

year, their view on their costs of living over the same period, whether

they have increased their loans and other outstanding debts including

credit cards and whether they are saving more than last year. Finally we

ask about their overall change in net worth over the past 12 months –

by net worth we mean net assets less outstanding debts.

The results from the DFA household surveys to the end of October 2018 are out today. The index measures households overall comfort level with their finances across a number of key dimensions. Recent home price trends, lower returns on deposits and share market gyrations have combined to take the index lower, despite strong employment trends. The wealth effect is now working in reverse, with a potential impact on future consumption.

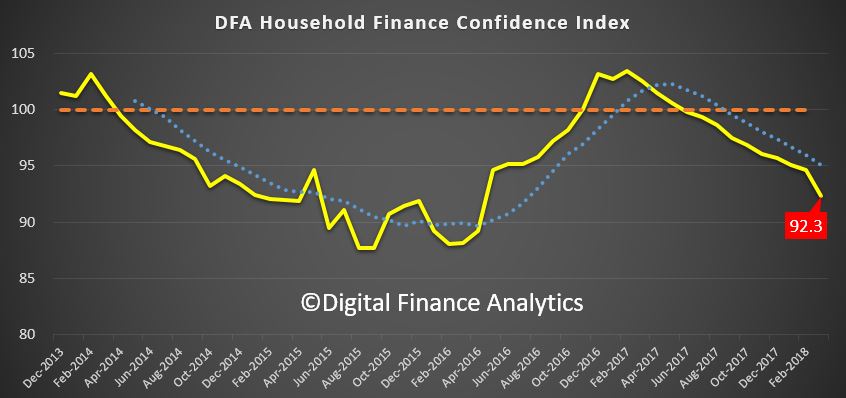

The index returned a result of 88.1, down from 88.4 last month. This continues the decline since late 2016, and is now approaching the lowest ratings from 2015.

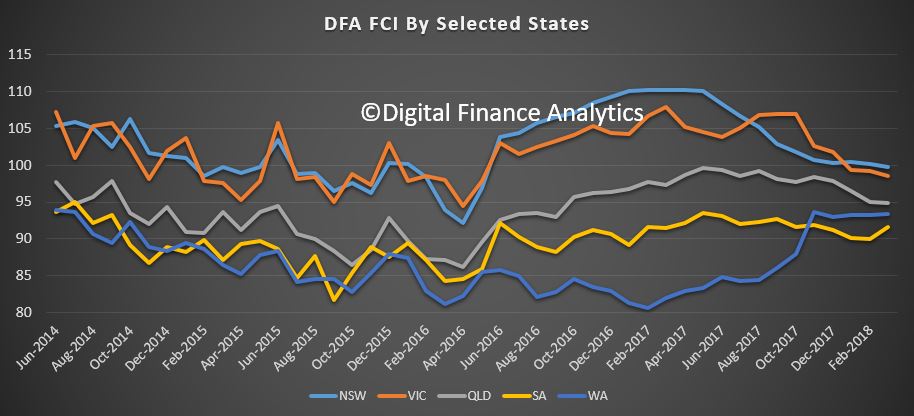

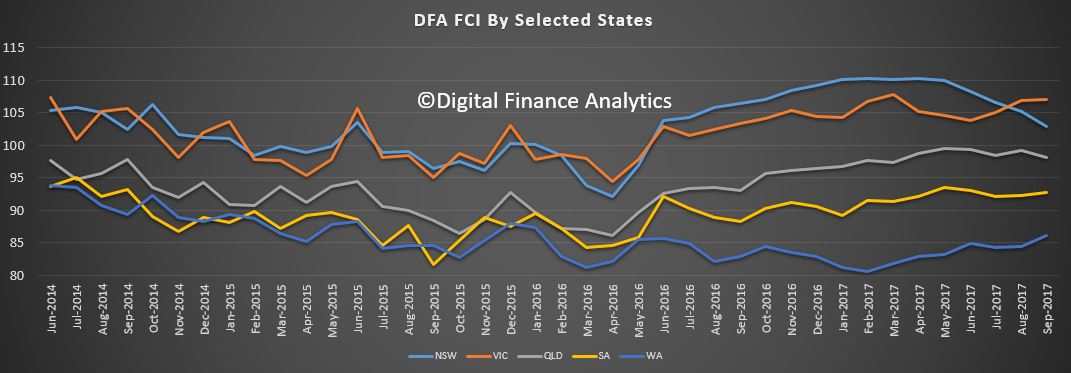

The convergence across the states continue as home price falls in NSW and VIC take a toll, with the southern state showing a significant slide. WA and QLD appear to be tracking quite closely.

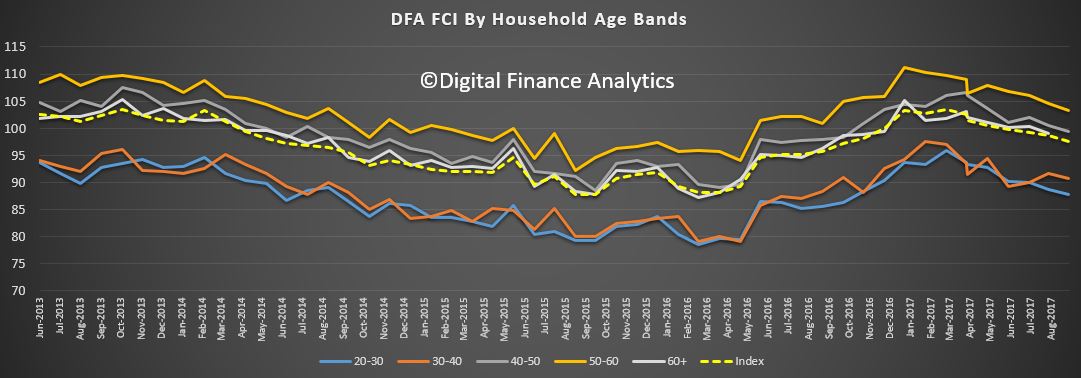

Across the age bands, younger households are under the most pressure (thanks to large mortgages, or renting) while those aged 50-60 years remain the most confident, thanks to lower net borrowing, and more savings and investments. For those aged 40-50 recent falls in property prices swamp any benefit from stock market performance.

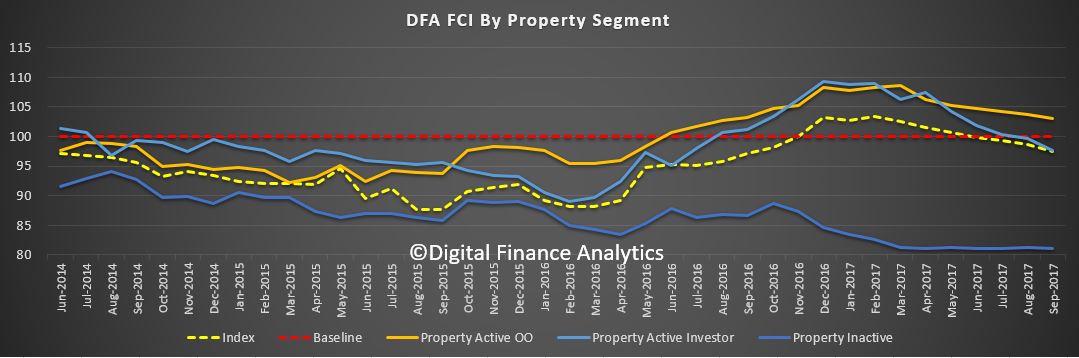

Those holding property for owner occupation remain the most positive, despite falls in paper values of their homes, but property investors are now registering significant concerns, thanks to flat or falling net income from rentals, falling capital values and concerns about the future of negative gearing and capital gains tax relief. More property investors signalled an intention to seek to sell property, as the switch from interest only to principal and interest loans continues. More than 41% of mortgage applications were rejected, compared with 5% last year, as more rigorous underwriting standards bare down. In fact those renting are in many cases more confident than property investors, significant turn around. The great property investor decade in passing.

Turning to the moving parts within the index, there was a small fall in those feeling more insecure about their job prospects, down 0.71% to 26.99%. There was a rise of 1.53% in those feeling more secure to 12.68%, and as a result those saying there was no change dropped a little, down 1.91% to 57.14%. We continue to see the spread of more precarious employment, including gig economy jobs, zero hours contracts, and growth in low paid ancillary healthcare jobs. We also saw a significant fall in employment in the finance, construction and real estate sectors, as the property sector eases.

Savings have been hit by recent stock market ructions, plus lower deposit rates on call accounts. As a result, there was a 3.38% rise in those less comfortable with their savings, to 43.39%. 49.28% said there was no change.

On debt, 45.47% of households were more concerned about their debt holdings, up 3.48%, thanks to some higher interest rates, rejected loan applications, and falling property values eating into equity, so reducing loan to value ratios. That said, those seeing no change stood at 51.87%, so more than half of households do not see any significant change.

Looking at household cash flow, income growth remains anemic in real terms. Just 3.69% said they had real income growth in the past year, up 1.32%, partly thanks to recent wage awards. However, 53.71% said their incomes had fallen over the same period, up 4.01%, and 41.33% said there was no change. Those in the public sector (especially in Canberra) appear to be fairing the best.

On the costs side of the equation, recent oil price falls have yet to translate into the results, so households said that overwhelmingly their costs of living has risen in the past year – at 83.66%. 4.88% said their costs had fallen, up 1.50% and 11.33% said there was no change. We see find households discussing power bills, fuel, health care costs and child care expenses, but they also highlighted recent rises in some food staples and council charges.

So finally, we can look at net worth (assets minus debts). Around 30% of households reported no change compared with a year ago, but 30.6% reported a net fall, up 5.27% and directly associated with the fall in property values and share values. 37.92% said their net worth was higher, down 1.89% from last month. So the fall in values is now hitting home, and as a result more households are experiencing a negative wealth effect.

This may well be deadly to household consumption (the engine of growth from the RBA’s perspective). This all goes to show that tracking employment growth as a leading indicator of the economy is not telling the whole story.

Slow wages growth, falling home prices and rising costs are combining to drag wealth and household confidence lower, and there is no end in sight. Another reason why we think the RBA will not be lifting the cash rate any time soon.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

In the final post relating to our latest household surveys this month, we turning to our household financial confidence index.

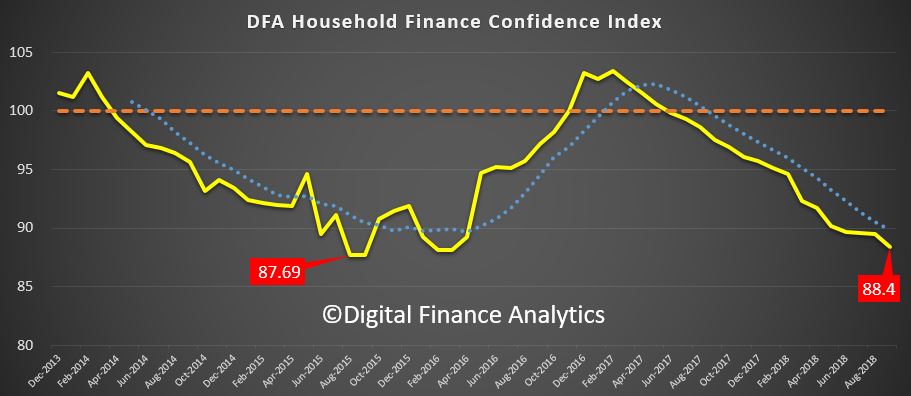

The latest read, to end September shows a further fall, and continues the trend which started to bite in 2017. The current score is 88.4, just a bit above the all-time low point of 87.69 which was back in 2015. Last month – August – it stood at 89.5.

Looking across our property segments, both property investors and owner occupiers were lower, reacting to the falls in home prices, and the difficulty of refinancing many are experiencing. Mortgage rate increases are also putting more pressure on many budgets. Despite this, those renting remain less confident, though investors have really turned sour now.

Across the states, we see a bunching of results, though Victoria appears to be heading south, while South Australian households are a little more positive than last month.

The falling levels of confidence are evident across many of the age bands, older households are still relatively more positively, largely thanks to historic capital growth in their property, and strong stock market performance in recent times. Younger households are more concerned and many are now seeing their property values fall, at least on paper.

Looking at the moving parts which drive our index, those who felt more confident about their job security than 12 months ago fell 1.8% to 11%. 59% saw no change.

There was a fall in those confident with regards to their savings, with a fall of 1.7% in those feeling more comfortable than a year ago, and 50% feeling about the same. The falling savings rates that many have experienced is part of the story, but so is the fact that more are raiding savings to make ends meet. This of course is not a sustainable position.

There was a fall of 1.3% in those who are comfortable with the amount of debt they hold, and 42% are less comfortable than a year ago, reflecting recent mortgage rate increases, and problems with getting an appropriate refinance deal.

Overall income remains an issue for many, with 42% saying there had been no increase in the past year, and 50% saying there had been a decrease in real income. Many households are relying on multiple jobs to pay the bills, and some of these are zero hours and uncertain in terms of income. We still see high levels of under employment, suggesting that many households want more work than they can get.

The costs of living remain a significant issue with 84% saying their costs have risen in the past year. It is the normal story, higher electricity and fuel bills, rising medical costs and child care as well as school fees. The standard reported CPI measure does not appear to align with many households current experience.

Putting all this together, 39% say their net worth is higher now than a year ago, mainly thanks to the strong stock market, 28% say they see no change and 25% say their net worth has dropped. The most significant factor here is the fall in property values over the past 12 months.

We expect to see the index continuing to track lower ahead, because the elements which drive the outcomes are unlikely to change. Home prices will continue to move lower, the stock markets are off their highs, wages are hardly growing and costs of living are rising. Household financial confidence is set to remain in the doldrums.

Finally, despite the attractor mortgage rates on offer from the banks continues, (in an attempt to keep mortgage volumes up), our research shows that many households cannot access them in the new tighter lending environment. 40% of applications are being rejected.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

The latest Digital Finance Analytics Household Finance Confidence Index for March 2018 shows a further slide in confidence compared with the previous month.

The current score is 92.3, down from 94. 6 in February, and it has continued to drop since October 2016. The trend is firmly lower.

Across the states, confidence is continuing to fall in NSW and VIC, was little changes in SA and QLD, but rose in WA.

Across the age bands, there were falls in all age groups.

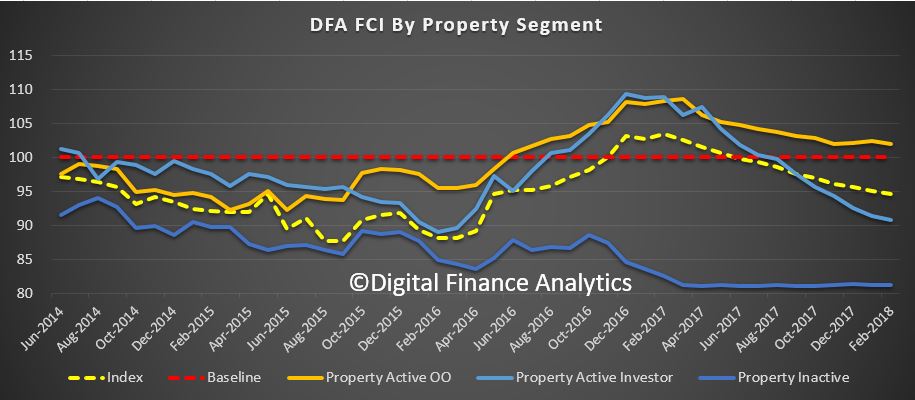

Turning to the property-based segmentation, owner occupied householders remain the most confident, while property investors continue to become more concerned about the market. Those who are property inactive – renting, or living with parents or friends remain the least confident. Nevertheless those who are property owners remain more confident relative to property inactive households.

We can look at the various drivers which underpin the finance confidence index.

We start with job security. This month, there was a rise 6% in households who are less confident about their job security compared with last month, up to 25.8%. Those who felt more secure fell by 1.5% to 12.1% while 61% saw no change. Availability of work was a primary concern, but the security concerns were more around job terms and conditions, and the requirement to work unsocial hours and weekends.

Turning to concerns about levels of debt, 44.5% of households were more concerned about their outstanding loans, up 1.5% from last month. Under 3% of households were more comfortable with the debt they hold. 49% reported no change this month. Those who were more concerned about debt highlighted concerns about higher interest rates, and the ability to service their current loans in a flat income environment.

52% of households reported their incomes had fallen in the past month, in real terms. This is up 1.5% this month. Just over 1% of households reported a pay rise, and 43% reported no change in real incomes. More households comprise of members who are working multiple jobs to maintain income.

In contrast, cost of living continues to rise faster than incomes for many households. 77% of households said their costs had indeed risen, up slightly from last month. 18% of households said costs had stayed the same and 3% said costs had fallen. Households said the costs of electricity, petrol, school fees and child care costs all hit home. Health care costs, and especially the costs of private health care cover also figured in their responses. More households are seriously considering terminating their health insurance cover due to the rising expense.

Turning to savings, 46% of households were less comfortable with their savings a rise of 1.5% compared with last month. 4% were more comfortable. 50% were about the same. There were ongoing concerns about further falls in interest rates on deposit accounts, and the need to continue to raid savings to support ongoing household budgets.

Finally, we look at household overall net worth. Despite the volatility seen in the financial markets, the main concern captured in answers to this question related to potential falls in property values. 52% said their total net worth was higher, down 3% from last month. 18% said their net worth was lower, a rise of 2% compared with last month. 28% remained the same. Both those with higher levels of education, and males tended to report more of a rise in net worth. Women were considerable more concerned about the current trajectory of home prices, and the risks relating to future falls. Households in regional centres remained more concerned about their net worth, not least because in many areas home prices have risen less strongly in recent years.

So in conclusion, based on the latest results, we see little on the horizon to suggest that household financial confidence will improve. We expect wages growth to remain contained, and home prices to slide, while costs of living pressures continue to grow. There will also be more pressure on mortgage interest rates as funding costs rise, and lower rates on deposits as banks trim these rates to protect their net margins.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

The latest edition of the Digital Finance Analytics Household Finance Confidence Index shows a further drift lower, remaining below the 100 neutral benchmark. It fell to 94.6 in February, down from 95.1 the previous month. This is in stark contrast to improved levels of business confidence as some have reported. Our latest video blog covered the results.

The slide was more significant among those households with investment properties, thanks to higher mortgage rates, concerns about interest only loan resets and lower home prices. In additional net rentals are lower. Owner occupied households also fell just a small amount, mainly because of rising living costs against flat incomes. Those renting, or otherwise excluded from property are the least confident. This continues the long term trend, indicating that property ownership still bolsters confidence to some extent.

The slide was pretty consistent across the states, other than a small lift in WA. Compared with a year ago, confidence levels in NSW and VIC are significantly lower.

We also see a similar story across all the age bands, suggesting the decline in confidence is similarly widely spread.

To understand the reasons for the falls we can look to the index scorecard. Overall, there was a rise of 1.2% in households feeling less secure about their jobs, compared with this time last year, and a small reduction in those feeling more secure.

Those with savings were less comfortable, thanks to continued falls in deposit rates, and recent discussions about deposit bail-in following passage of the recent APRA Act. More significantly, more are dipping into their savings, to maintain lifestyle, and so balances are reducing. Many realise this is not a sustainable position.

Just under half of households remain uncomfortable with the amount of debt they hold, around half saw no change over the past year. Concerns related to rising interest charges which are working through, and also ability to maintain mortgage repayments. Some households have resorted to obtain additional credit, either on a card, or separate loan, to maintain their finances. Again many realise this is not a sustainable position.

Costs of living concerns rose, with 76.7%, up 3.84% on last month, households saying that costs of electricity, fuel, rates, child care and school fees all impacting. Only 2.5% of households said their costs had fallen.

Finally, we saw a fall of 3.7% of households who said their net worth had improved, down to 54.6%, mainly explained by changes in the value of property on one hand, and of share prices on the other. 16% said their net worth had fallen. 28.9% said there had been no change.

Based on our research, we see little on the horizon to suggest that household financial confidence will improve. We expect wages growth to remain contained, and home prices to slide, while costs of living pressures continue to grow. There will also be more pressure on mortgage interest rates as funding costs rise, and lower rates on deposits as banks trim these rates to protect their net margins.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

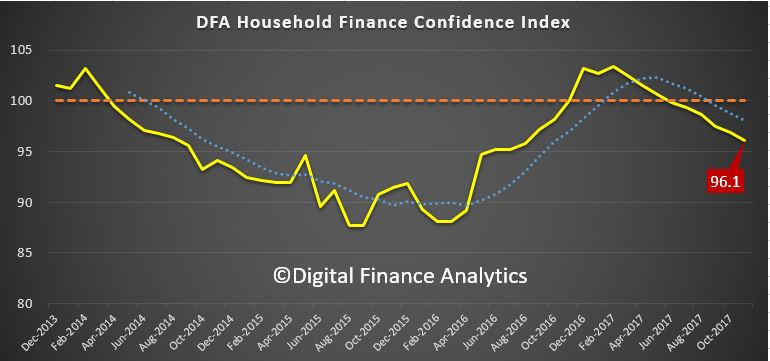

Digital Finance Analytics has released the November 2017 results from our Household Financial Security Index. The index uses data from our household surveys to assess households level of financial comfort.

The index fell to 96.1, which is below the 100 neutral metric, down from 96.9 in October 2017. This is the sixth month in succession the index has been below the neutral point.

Watch the video or read the transcript.

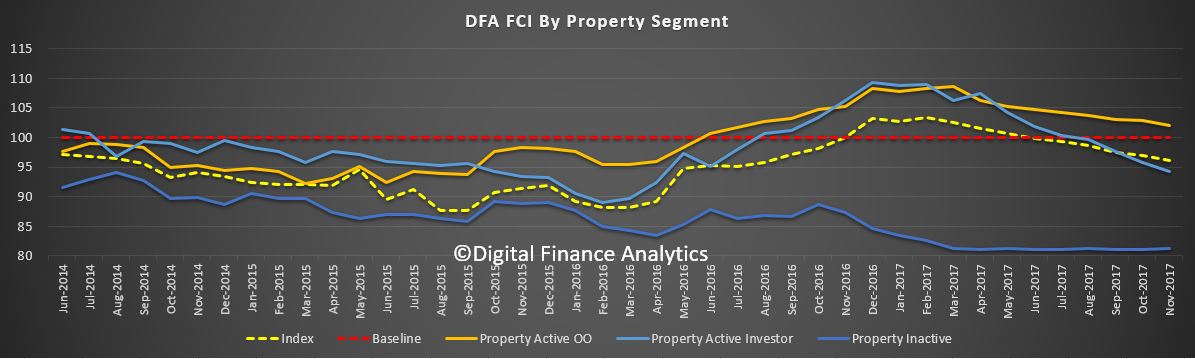

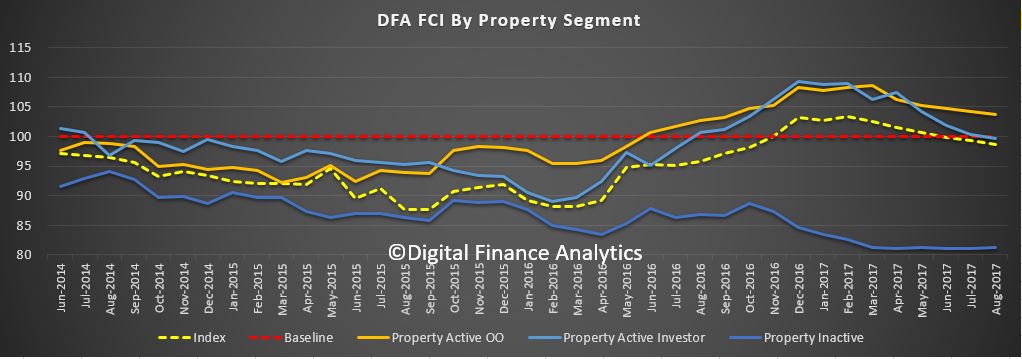

Owner Occupied households are the most positive, scoring 102, whilst those with investment property are at 94.3, as they react to higher mortgage repayments (rate rises and switching from interest only mortgages), while rental yields fall, and capital growth is stalling, especially in Sydney). Households who are not holding property – our Property Inactive segment – will be renting or living with friends or family, and they scored 81.2. So those with property are still more positive overall.

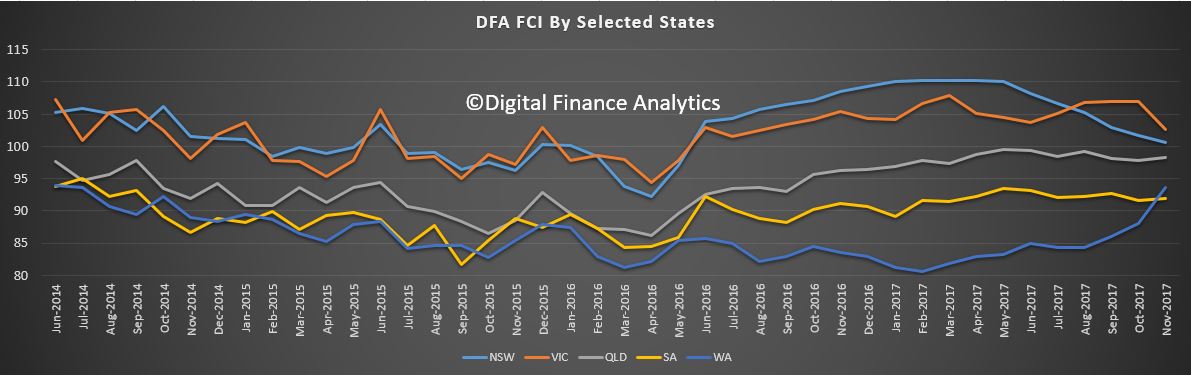

Looking across the states, households in NSW and VIC are just above the neutral setting, but continue to slipping lower. Households in QLD are below the 100, but up a little, as are those in SA and WA. Western Australian households are the least positive, but somewhat improved.

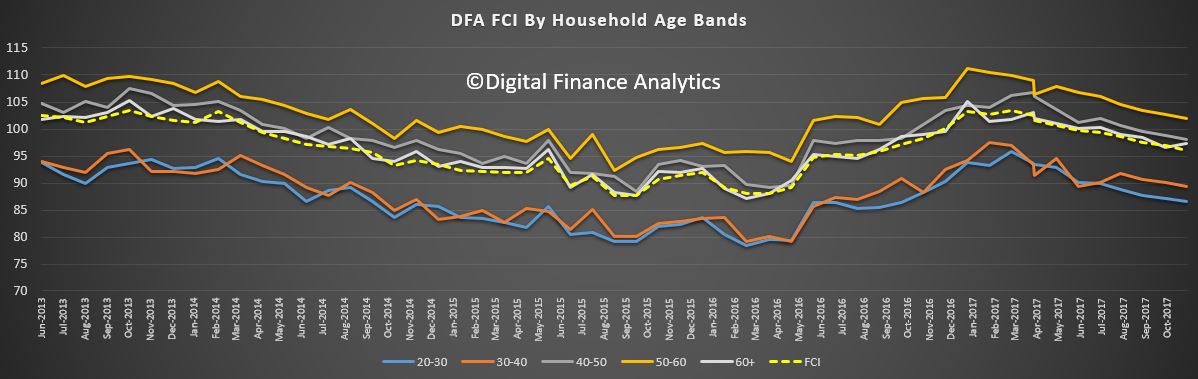

Looking across the age ranges, younger households are the least positive, and all ages banks fell, other than those over 60 years which saw a small rise.

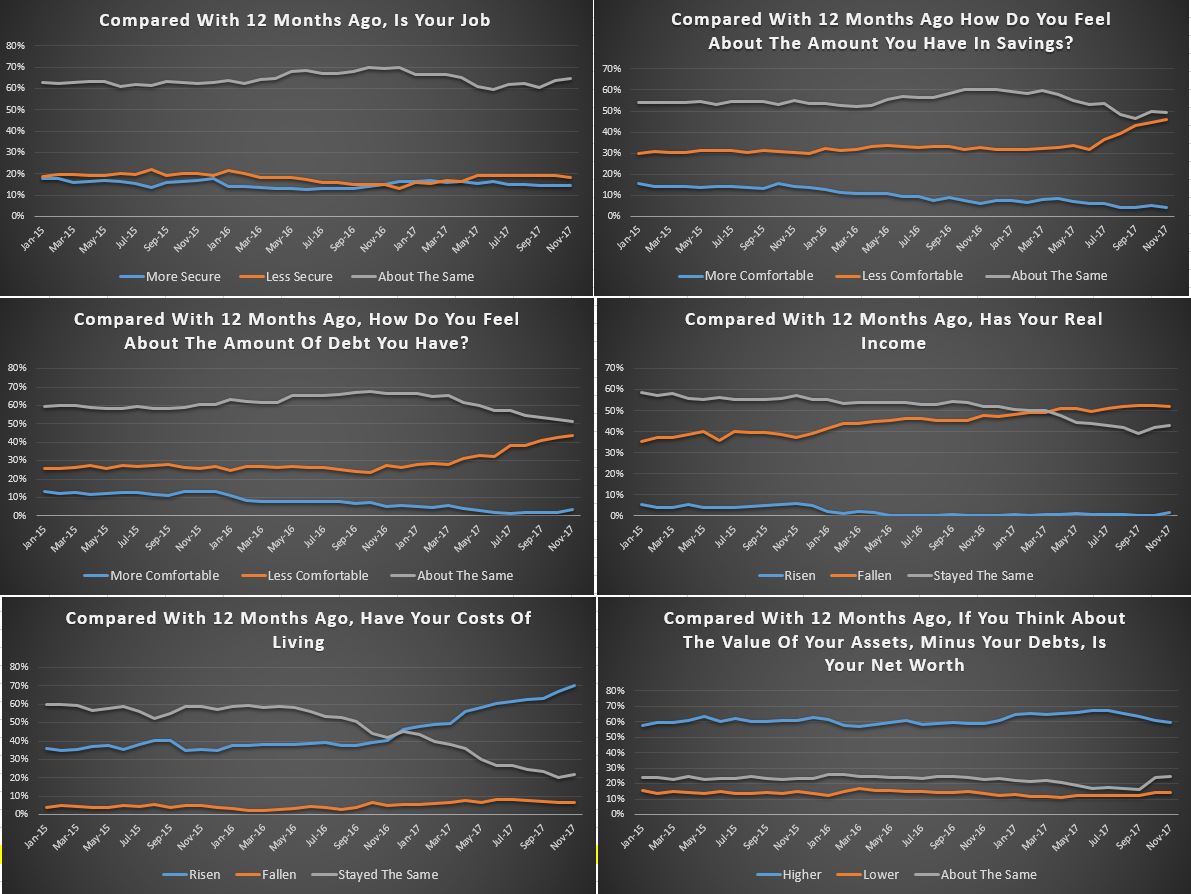

Looking at the FCI score card, job security is on the improve, reflecting rising employment participation, and the lower unemployment rate. Around 20% of households feel less secure, especially those with multiple part time jobs.

Savings are being depleted to fill the gap between income and expenditure – as we see in the falling savings ratio. As a result, nearly 40% of households are less comfortable with the amount they are saving. This is reinforced by the lower returns on deposit accounts as banks seek to protect margins.

More households are uncomfortable with the amount of debt they hold with 40% of households concerned. The pressure of higher interest rates on loans, tighter lending conditions, and low income growth all adds to the discomfort. More households reported their real incomes had fallen in the part year, with 50% seeing a fall, while 40% see no change. Only those on very high incomes reported real income growth.

More households reported a rise in their costs of living, and this month this included higher school fees and child care costs, energy bills and fuel costs. The average cpi of around 2% appears to understate the real life experience of many households.

Finally, household net worth improved for more than 60% of households, but there is a rise in those seeing no growth, mainly as home price growth eases back. Those with share market investments have done quite well in recent months.

Looking ahead, we expect the overall index to trend lower, as incomes remain constrained, and costs of living grow. The property market has a big impact on households level of confidence and the leading indicators are flagging lower outcomes ahead. However, home prices would need to fall significantly to allow many of those currently unable to afford to buy in to the market.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

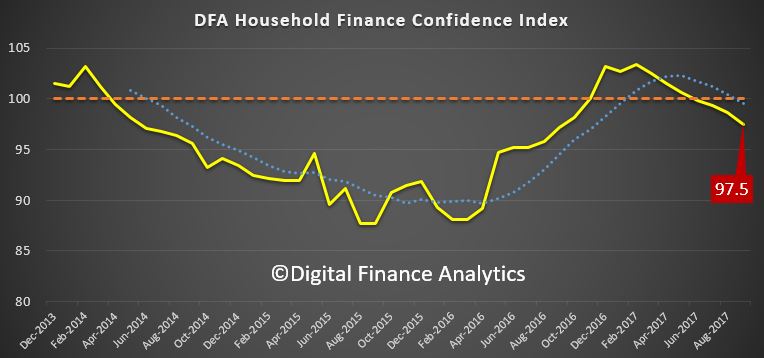

The September update of the Digital Finance Analytics Household Finance Security Index, released today, underscores the growing gap between employment, which remains relatively strong, and the Financial Security of households. We discussed this recently on ABC The Business. The Index fell from 98.6 in August to 97.5 in September.

This is below the 100 neutral setting, and continues the decline since December 2016. Watch the video, or read the transcript.

The state by state view highlights a fall in NSW, while VIC holds higher, and there was a rise in WA from February 2017 lows. This highlights the fact the households across the national are under different levels of pressure.

Tracking by age bands we find younger households are significantly less confident, compared with those aged 50-60 years. But across the board, the general trend is lower.

Property ownership remains a large factor, with those renting still below those owning property. We also see an ongoing decline in property investor confidence, thanks to tighter underwriting standards, higher mortgage rates, and the reduction in interest only loans availability.

Looking at the scorecard, there was a 4% fall in households comfortable with their savings, as they are forced to raid them to cover ongoing expenses (and the low returns on deposit balances as the banks seek to build margin). There was a rise of nearly 3% of households who were uncomfortable with the amount of debt they hold, reflecting higher mortgage rates, especially on investment loans and interest only loans, and concerns about future rate movements. Finally, more households reported their overall net worth has deteriorated as home prices came under pressure.

The disconnect is that while people can, in the main, get some work, their earned income is not rising as fast as costs. We also find more households relying of a larger mix of fragmented part-time jobs, which tend to be less predictable. As a result, we expect the current trends to continue, as momentum in the housing sector ebbs. There is no obvious circuit breaker available in the current low interest rate, low growth environment.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

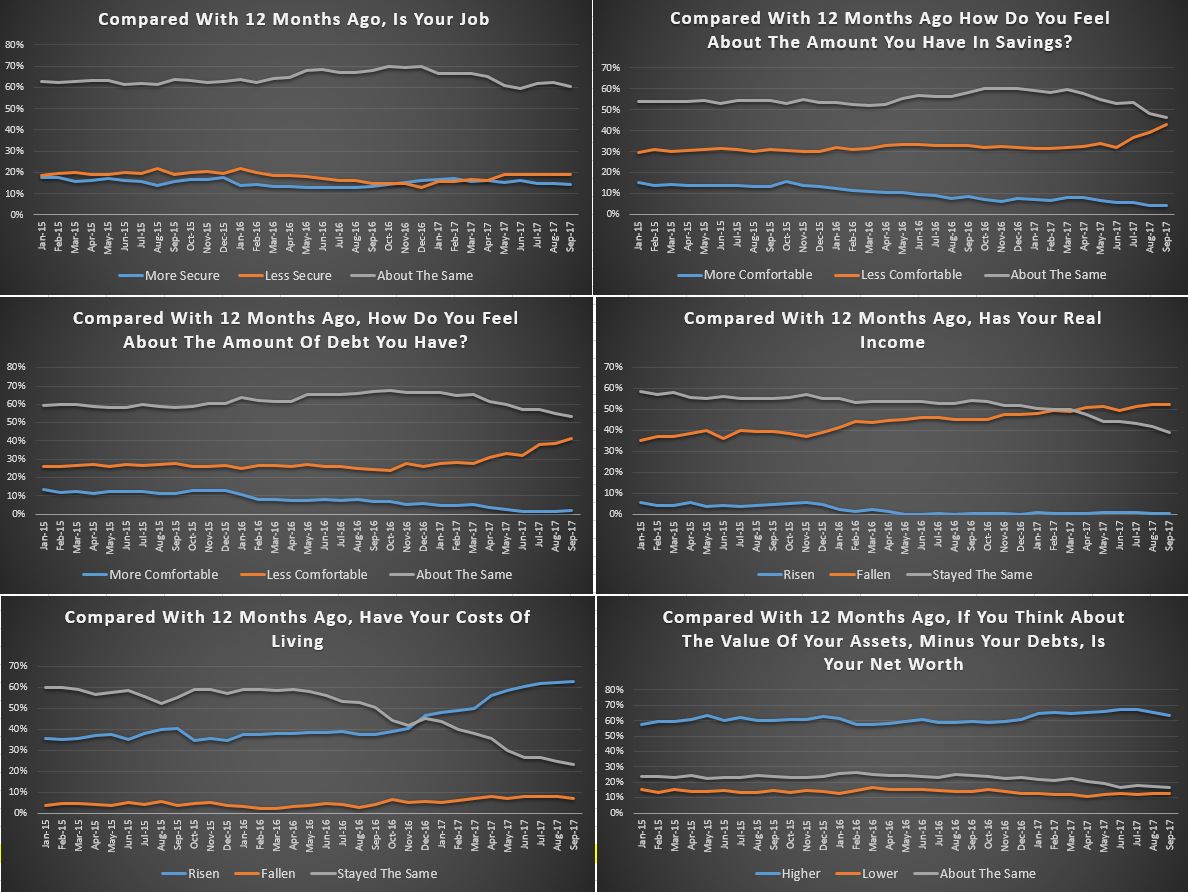

Digital Finance Analytics has released the August 2017 edition of our Household Finance Confidence index, which uses data from our 52,000 household surveys and Core Market Model to examine trends over time. Overall, households scored 98.6, compared with 99.3 last month, and this continues the drift below the neutral measure of 100. This is an average score, and there are significant variations within our various segments.

Watch the video to learn more, or read the transcript below:

Younger households are overall less confident about their financial status, whilst those in the 50-60 years age bands are most confident. This is directly linked to the financial assets held, including property and other investments, and relative incomes. Households over 60 years track quite closely to the national averages.

For the first time in more than a year, households in Victoria are more confident than those in NSW, while there was little relative change across the other states. One of the main reasons for the change in NSW can be traced directly to the state of the Investment Property sector, where we see a significant fall in the number of households intending to purchase in NSW, and more intending to sell. One significant observation is the rising number of investors selling in Sydney to lock in capital growth, and seeking to buy in regional areas or interstate. Adelaide is a particular area of interest.

Consistent with our earlier analysis, a household’s property owing status has a significant impact on their relative financial confidence, with owner occupied households the most confident, ahead of property investors and those renting. That said, low rental growth rates mean more investors are underwater on a cash flow basis, especially in Victoria, where more than half are not covering the borrowing costs of their investment mortgage from rental receipts (but are still hopeful of capital gains, and they can offset the losses thanks to tax breaks). Actually returns are much stronger in QLD and TAS.

Looking at the scorecard, job security remained about the same this month, but there was a 1.7% fall in those more comfortable with their savings and a rise of 2.5% of those less comfortable – thanks to lower interest rates on deposits as banks seek to build margin. The debt burden remained a concern, with a small rise in those worried about meeting repayments on outstanding loans. Incomes are still under pressure, with more saying their incomes in real terms have been devalued, down 1%, to 52% of households. Costs of living continue to rise for 63% of households, and only 7% saw a fall. 65% of households said their overall net worth rose again, thanks mainly, to home prices rising. Some in WA, QLD and WA reported a fall, directly due to house values continuing to slip.

Given the fact that the dynamics of the economy seem to be locked in place with lower income growth, rising costs of living, and the property market adjusting to the new regulatory environment, we expect confidence to continue to drift lower in the months ahead. There is no obvious circuit breaker available in the current low interest rate, low growth environment. The leading indicators suggest that the recent positive momentum in the property market may be short lived.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.