We examine the market in Perth suburb Rockingham 6168, on the day of the WA election. Is property booming, and if you had bought int 2014, would you be ahead or behind?

Another deep dive into a property location, about 100k from Brisbane. Palmwoods is a rural town and locality in the Sunshine Coast Region, Queensland, Australia. In the 2016 census, Palmwoods had a population of 5,676 people.

It is situated close to popular family tourist attractions such as The Big Pineapple. Pineapple growing remains the most important primary industry in the area. Palmwoods is located 15 minutes from the beach and the Blackall Range.

In the latest in our property spotlight series, we examine the fast changing suburb south of Sydney, where just 22 percent of homes are now houses, as the rise of the high rise continues. This may not bode well for the myriad of property investors in the area.

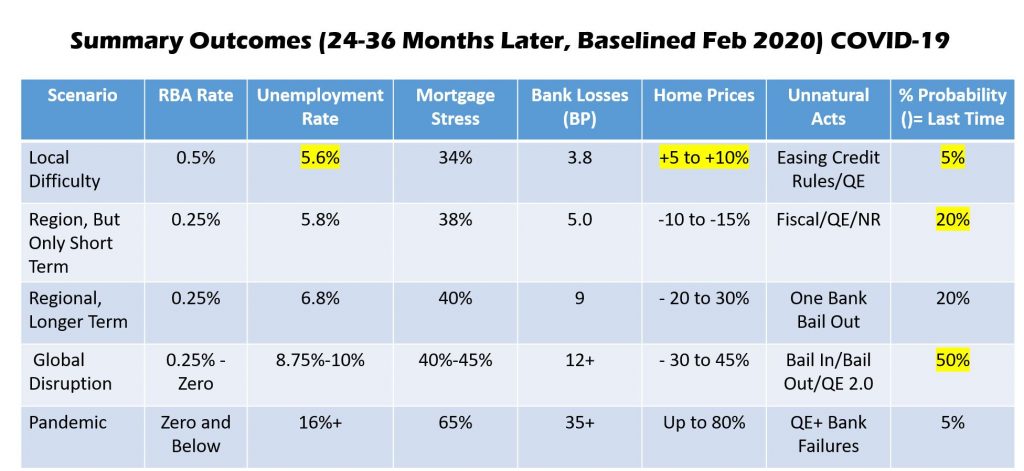

Last week we ran our latest live event, and discussed a range of potential scenarios relating to the virus. If the virus is localised and of short duration, there was still a path to higher prices, but as its severity and reach grows, prices would turn negative. This is a simple (actually complex) set of relationships between economics, human behavior and property.

Here is a summary of the various scenarios from our modelling. We weighted the greatest probability at 30-45% fall in the months ahead, assuming global disruption, financials market falls and reinfection. All of which is coming true.

Begs the question, how soon will prices turn south unequivocally?