CBA has decided to remove SMSF lending from its services. Commonwealth Bank of Australia (CBA) has said it is “streamlining” its product offering and as such will no longer offer the ability for self-managed super fund (SMSF) trusts purchase investment property with their fund. Via Australian Broker.

In July, Westpac announced it would be removing its SMSF product. CBA also announced it would be removing low-doc loan products.

CBA’s SuperGear product currently available will cease at close of business on 12 October. New applications and refinancing applications will not be accepted after this date.

Any approvals before 12 October have the condition they must be settled and approved by 28 December 2018.

A CBA spokesperson said in a statement, “As part of our strategy to become a simpler, better bank, we are streamlining our product portfolio and have made the decision to discontinue our ‘SuperGear’ lending product which enabled investment in residential and commercial property through self-managed super funds.

“This change will be effective from close of business on 12 October 2018. We will continue to support our existing customers who have these loans with us.”

For brokers, commission payments will continue as per existing agreements.

The Hayne royal commission has learned that the corporate watchdog allowed CBA to pay a substantially reduced fine despite misleading customers in its advertising, via InvestorDaily.

The royal commission has heard that ASIC not only gave CBA a severe discount for the misleading conduct but also let Australia’s biggest bank draft the media release regarding the action.

Senior counsel assisting Rowena Orr, QC opened Thursday’s hearing by questioning Helen Troup, the executive general manager of CBA’s insurance business CommInsure.

Ms Troup was taken through four pieces of advertising for CommInsure’s life and trauma insurance policy to determine how they discussed coverage for a heart attack.

Ms Troup accepted that in every case someone reading the adverts would believe the trauma policy covered all heart attacks.

The royal commission heard that CommInsure made a $300,000 voluntary community benefit payment as part of its agreement with ASIC to resolve the issue of misleading advertising.

Ms Orr pointed out to the commission that the maximum penalty for misleading conduct was 10,000 penalty units or almost $2 million per contravention.

In this instance, as Ms Troup had agreed to four adverts being misleading, it could have led to a fine of $8 million. But CommInsure only had to pay $300,000 as part of its agreement with ASIC to resolve the issue.

ASIC in fact seemed to have asked CBA if they thought the $300,000 was appropriate as Ms Orr read out to the commission a letter from the senior executive of ASIC, Tim Mullaly, addressed to CBA:

Could you please consider and let us know whether this is sufficient for CommInsure to resolve the matter, including by way of payment of the community benefit payment, in absence of infringement notices.

This provoked commissioner Hayne to ask if it was a case of the bank stipulating the terms of the punishment.

“The regulator asking the regulated whether the proposal was sufficient in the eyes of the party alleged to have broken the law, is that right?” he asked.

“We could have taken the approach of continuing to defend our position, so this was the alternative,” Ms Troup said.

Commissioner Hayne continued and asked Ms Troup if CommInsure viewed the community payment as a form of punishment.

“The $300,000 community benefit payment was a form of punishment,” she said.

Up until today’s hearing, CBA had not acknowledged the misleading adverts and had even advised ASIC on what language to use in their press release, said Ms Orr.

Ms Orr concluded by summarising that ASIC had given CommInsure notice of its findings, took no enforceable action and gave CommInsure the opportunity to make changes to the media release.

CBA’s life insurance business CommInsure has admitted to not following recommendations from the corporate regulator to update its medical definition of a heart attack so it could deny the payout of a trauma claim to one of its customers, via InvestorDaily.

On Wednesday, the royal commission heard that ASIC had sent a letter to CommInsure flagging its concerns that its reliance on outdated medical definitions in assessing claims – while not in breach of the duty of utmost good faith in Section 13 of the Insurance Contracts Act – fell significantly short of consumer expectations.

The counsel assisting Rowena Orr cited a letter from 22 March 2017 from the ASIC deputy chair at the time, Peter Kell, who noted that in, 2012, the European Society of Cardiology, the American College of Cardiology, the American Heart Association and the World Health Federation published an expert consensus document about the definition of heart attacks.

Sitting in the witness box, CommInsure managing director Helen Troup was questioned by Ms Orr on whether she was aware that this had been reached at the time.“Yes,” Ms Troup said.

“And that report endorsed the use of troponin as a means of detecting heart attacks?” Ms Orr continued.

“Yes,” Ms Troup responded.

“And the report said that laboratories should use a cut-off value of the 99th percentile of a normal reference population to determine whether there had been a heart attack?” Ms Orr said.

Ms Troup replied in the affirmative.

Ms Orr then noted Mr Kell’s comments in the letter that CommInsure’s decision to select the 11 May 2014 as the effective date of the change had no robust rationale, given the joint report was published in 2012.

She then noted the letter said CommInsure’s conduct was unreasonably slow in responding to the changes in medical practice, that it was on notice that the standard was to be updated and had not done that even three years after the joint report was published, and that seven other insurers had updated their definition by 11 May 2014.

“While this is not contrary to the law, it is ASIC’s view that this has unfairly impacted on some consumers and better practice would be to select an earlier date,” Ms Orr said.

Slater and Gordon has taken aim at Australia’s biggest bank as it prepares to take on the retail super funds in a historic class action lawsuit, via InvestorDaily.

The national law firm this week announced the launch of its ‘Get Your Super Back’ campaign and said it will involve a series of class actions with Commonwealth Bank-owned Colonial First State and AMP super likely to be their first targets.

“The firm will allege the big bank-backed super funds failed to obtain for members competitive cash interest rates on cash option funds, and charged exorbitant fees, affecting millions of members who held part or all of their superannuation in bank owned funds,” they said in a statement.

Senior associate Nathan Rapoport from Slater and Gordon told Investor Daily that the firm chose AMP and Colonial to be first as they were good examples of wrongdoing by superannuation trustees.

“The evidence at the royal commission really highlighted how in our view the trustee companies are letting down members and not acting in accordance with quite elementary trust law in Australia,” he said.

Mr Rapoport said that their case against Colonial First State was to be focused on the way that trustees invested members cash.

“Colonial invests that cash with Commonwealth Bank always and it doesn’t shop around and get the best return for members and we believe that’s a very clear and simple case of the trustee not acting in the best interest of its member,” he said.

The case against the AMP is similar but is also focusing on the fees charged by the bank, said Mr Rapoport.

“The evidence we have looked at indicates that AMP funds are charging as much as half a percent per annum than other comparable funds and even though that may not sound like a lot, over a lifetime it really adds up to quite an enormous amount,” he said.

AMP refuted the claims and said any issues with their business had already been fixed.

“We’re committed to acting in the best interests of our superannuation members at all times and acting in accordance with our legal and regulatory obligations.”

AMP said that they were already working with customers to benefit any affected members and to improve member outcomes.

“We have reduced the administration fees on some of our cash investment options to address the issue of negative returns in the small number of funds impacted by this issue. We are also compensating affected customers for lost earnings,” they said.

Commonwealth Bank also released a statement confirming it was aware of the announcement but that they had “not been served with any legal proceedings”.

The case would not end at those two banks; Slater and Gordon are looking to see what other funds had not acted in the best interest of members, said Mr Rapoport.

“There seems to be a trend in the way they [retail funds] invest the cash with their parent banks so there is a good chance that we will be launching a case against many others as well,” he said.

If the class action is broadened, it has the potential to be the largest class action law suit ever undertaken in Australia.

“We estimate that there could be in the order around 5 million Australians that have at least one account with a retail super fund so if we do broaden the case and launch cases against most of the retail funds then that’s the kind of number we are looking at,” he said.

The allegations arise from evidence given to the royal commission into the banking industry and information released in the Productivity Commission report.

The Productivity Commission report released in May found that retail super funds only brought in members 4.9 per cent per annum in contrast to the 6.8 per cent per annum brought in by industry funds.

In fact, the Productivity Commission report found that retail funds frequently underperformed and charged more fees than industry funds.

Sportsbet is currently tipping Commonwealth Bank to pay back the largest compensation with odds of $1.65, followed by ANZ $4.00, Westpac $7.00 and NAB $8.00.

The Australian Prudential Regulation Authority and the FSC declined to comment and, at time of writing, Colonial First State had not responded to media requests.

Commonwealth Bank of Australia has today announced it will increase its variable home loan rates, following a sustained increase in funding costs. All variable home loan rates will increase by 15 basis points from 4 October 2018.

For owner occupiers, the standard variable home loan rate will increase to 5.37% per annum for customers with principal and interest repayments, and 5.92% per annum for customers with interest only repayments.

For investors, the standard variable home loan rate will increase to 5.95% per annum for customers with principal and interest repayments, and 6.39% per annum for customers with interest only repayments.

Angus Sullivan, Group Executive Retail Banking Services Commonwealth Bank, said: “We have made this decision after careful consideration. We are very conscious of the impact that increasing interest rates will have on our customers, however it is important that we price our home loan products in a way that reflects underlying costs.

“Over the past six months, we have seen funding costs increase significantly, driven primarily by a rise in the 90 day Bank Bill Swap Rate. These changes have increased the cost of providing loans to our customers.

“We have absorbed these higher funding costs over the past six months in the hope that they would ease. Unfortunately, the costs have remained high and it is now expected that they will remain elevated for the foreseeable future.

“As a result of this, we have made the decision to raise our variable home loan rates to partially offset the increased costs. We understand this will have an impact on household budgets. To allow our customers time to prepare, this change will not take effect for four weeks, giving homeowners an opportunity to look at their options.

“For customers looking for more certainty around their mortgage repayments, we continue to offer a range of fixed rate options that may be suitable. These include a 3.79% per annum two year fixed rate for owner occupier customers, with principal and interest repayments, on our wealth package.

“We also encourage customers with interest only repayments to consider whether a lower rate principal and interest home loan would better meet their needs. Customers can switch online, in-branch or over the phone at no cost.

“Our customers can speak with one of our home lending specialists, who can review their home loan options free of charge, to ensure that their arrangements remain appropriate for their circumstances.”

The increase to our variable home loan rates will come into effect on 4 October 2018

CBA has rejected claims it broke the law, pointing to an obscure loophole in the Criminal Code and stating that it was “genuinely of the belief” that it was doing the right thing.

Great legal minds are trying to find ways to explain the banks conduct and avoid the worst potential consequences! This from InvestorDaily:

Earlier this month, Colonial First State (CFS) executive general manager Linda Elkins faced the royal commission, where she was questioned about CBA’s handling of the MySuper transition.

From 1 January 2014, employers could only make default contributions to a registrable superannuation entity (RSE) offering a MySuper product.

Counsel assisting Michael Hodge established in his questions to Ms Elkins that CBA had breached the law 15,000 times by receiving default contributions into high-fee-paying accounts after 1 January 2014.

RSEs were also given a deadline of 1 July 2017 to transfer existing accrued default accounts (ADAs) to an approved MySuper product.

Mr Hodge noted that the contravention of s.29WA of the SIS Act is a strict liability offence, a point that was highlighted by CBA in its latest submission to the Hayne inquiry.

“However, it should be noted that in determining whether or not an offence has actually occurred, consideration would need to be given to the defence of mistake of fact available in section 6.1 of the Criminal Code in respect of strict liability offences,” the bank said.

“This is particularly the case here where CFSIL was genuinely of the belief that the members for whom the s.29WA breach occurred were in fact ‘choice’ members who fell outside the requirements of s.29WA and that it was only after engagement with APRA that it understood that the regulator was of a different view.”

In June 2014, the board of CFS was told by management that APRA had requested it accelerate the transition for 60,000 ADA members, the royal commission heard.

Moving the 60,000 into lower-fee MySuper products would have the effect of turning off grandfathered commissions for advisers, the royal commission heard.

CFS, like other retail super providers, was eager to have ADA clients make an “investment decision” so that they would be considered a ‘choice’ member and therefore ineligible for transfer to a MySuper product.

In Mr Hodge’s submission to the commission following the fifth round of hearings, he stated that it is open to the commission to find that additional breaches occurred.

In response, CBA has stated that “there is no evidence before the commission to suggest that the failure to pay contributions of a subset of FirstChoice Personal members into a MySuper product was anything other than a genuine misunderstanding about the scope of s.29WA and its impact on particular cohorts of members, which CFSIL came to learn APRA did not agree with.”

“CFSIL believed that these members of FirstChoice Personal were choice members, to whom s.29WA did not apply.

“That honest mistake does not excuse CFSIL’s breach of the SIS Act provisions and s.912A(1)(c) of the Corporations Act as it has properly conceded, but it does tell against a finding of a failure to do all things necessary to provide services efficiently, honestly and fairly.”

On 10 August, the International Bank for Reconstruction and Development said it has mandated the Commonwealth Bank of Australia (CBA) as the exclusive arranger of the world’s first bond issuance solely using blockchain technology, via Moody’s.

This is credit positive for CBA because it shows the bank is making headway with significant fintech initiatives, which can help improve its operating efficiency and fend off new competition.

CBA will use the private Ethereum blockchain platform to create, allocate, transfer and manage a new debt instrument debt, dubbed “bond-i.” The transaction will provide a platform for future debt-security issuance using blockchain technology. The use of blockchain for bond issuance can offer efficiency benefits for both issuers and arrangers by simplifying the settlement processes. The technology can be used for both registry and payment systems, consolidating payments by investors and title transfers by issuers into single, instant transactions.

Prior to this transaction, CBA experimented blockchain-based bond issuance with government entity Queensland Treasury Corporation (State of Queensland, Aa1 stable). In January 2017, the bank arranged the issuance of a so-called cryptobond for Queensland, by utilizing blockchain technology. It was a trial transaction carrying no debt obligation, with Queensland acting as both the issuer and investor to test the process.

As discussed in our Bank of the Future report, fintech innovations such as these will help traditional banks reduce operating costs and also mitigate the risk of disruption by new fintech firms

CBA defied a request from APRA to accelerate the transfer of 60,000 members to MySuper in order to placate the bank’s aligned advisers, the royal commission has heard, via InvestorDaily.

Appearing before the royal commission hearings into superannuation yesterday, Colonial First State (CFS) executive general manager Linda Elkins was questioned about CBA’s handling of the MySuper transition.

From 1 January 2014, employers could only make default contributions to a registrable superannuation entity (RSE) offering a MySuper product.

Counsel assisting Michael Hodge established in his questions to Ms Elkins that CBA had breached the law 15,000 times by receiving default contributions into high-fee-paying accounts after 1 January 2014.

RSEs were also given a deadline of 1 July 2017 to transfer existing accrued default accounts (ADAs) to an approved MySuper product.

In June 2014, Mr Hodge established, the board of CFS was told by management that “APRA has requested that you accelerate the transition for 60,000 [ADA] members”.

“This suggestion has significant business implications as the original transition date is 2016,” the CFS board was told in June 2014.

Mr Hodge asked Ms Elkins: “Was one of the issues of which you were aware that immediately moving these ADAs over to MySuper would affect the relationship between Colonial and its advisers?”

“I was aware that advisers were impacted by this, yes,” Ms Elkins replied. “I don’t know that it follows it would affect our relationship with the advisers but we were aware that advisers were – were concerned, yes.”

Moving the 60,000 into lower-fee MySuper products would have the effect of turning off grandfathered commissions for advisers, the royal commission has heard.

CFS, like other retail super providers, was eager to have ADA clients make an “investment decision” so that they would be considered a ‘Choice’ member and therefore ineligible for transfer to a MySuper product.

“And that was why you were taking active steps for the benefit of advisers to obtain investment directions from members?” asked Mr Hodge.

“We were taking active steps to ensure the members had information to – to assist them with the choices they had,” replied Ms Elkins.

Hodge continued: “The purpose of obtaining those investment directions, or a purpose, I’m sorry, for obtaining those investment directions was to benefit advisers?

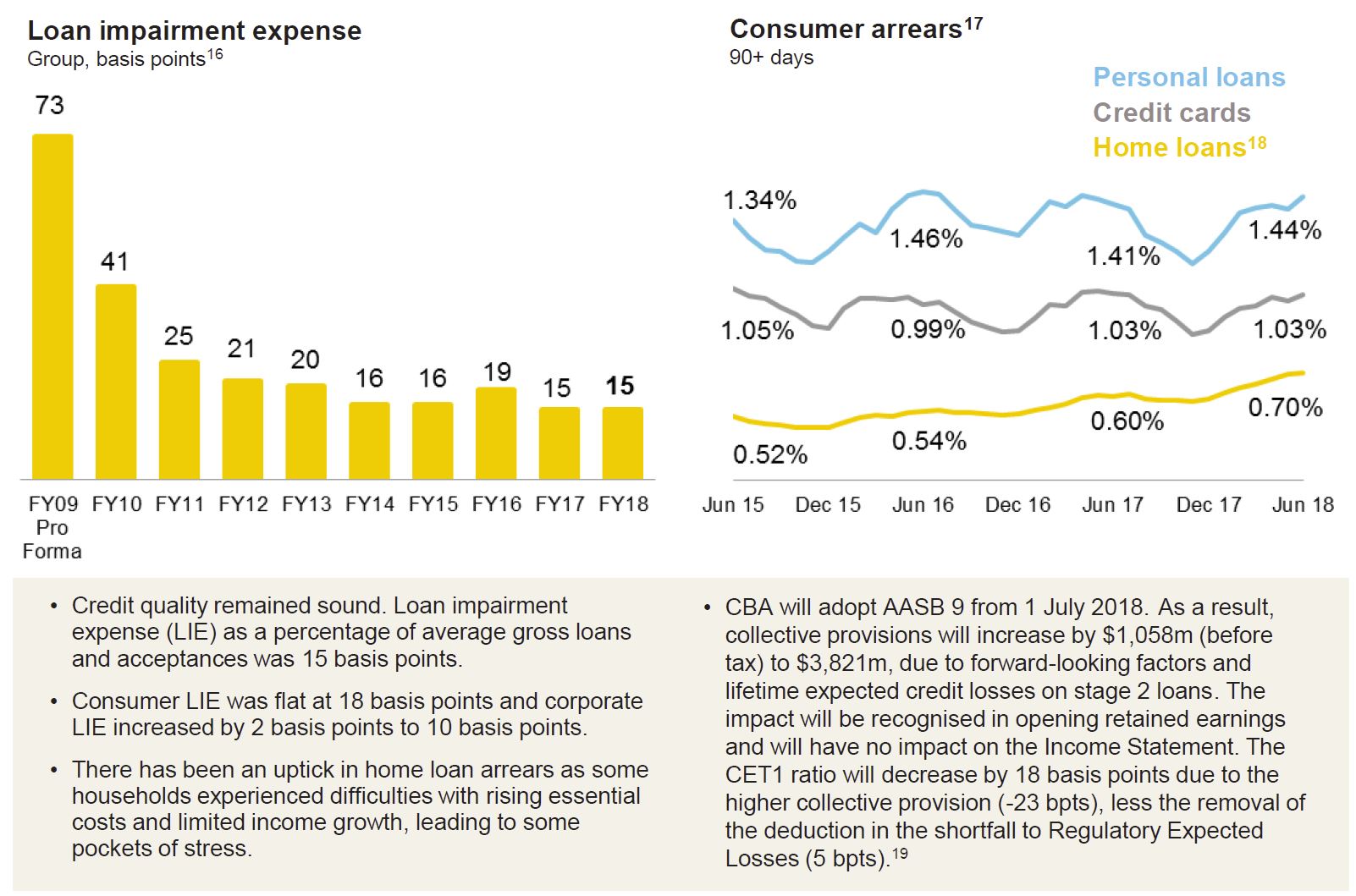

Fitch Ratings says the Commonwealth Bank of Australia’s full-year results to 30 June 2018 (FY18) broadly support the agency’s expectation that earnings pressure would emerge for Australian banks during 2018. An increase in wholesale funding costs led to a reduction in CBA’s net interest margin in 2H18, loan growth continued to slow and continued investment into the business and compliance contributed to higher expenses. Mortgage arrears also trended upwards due to some pockets of stress, and while they have not translated into higher provision charges as yet due to strong security values, continued moderation in Australian house prices may result in higher provisioning charges in future financial periods.

Most of the earnings issues appear applicable across the sector and are likely to remain into 2019, placing pressure on profit growth for all Australian banks. Increased regulatory and public scrutiny of the sector may make it difficult for the larger banks to reprice loans to incorporate the increase in wholesale funding costs, meaning net interest margins are likely to face some downward pressure. Loan growth is likely to further slow as the housing market continues to moderate, while compliance costs continue to rise due to the scrutiny on the sector.

The most prominent scrutiny is the royal commission into misconduct in the banking, superannuation and financial services industry, which has already identified a number of shortcomings within the industry. We expect the release of the interim royal commission report, due to be published by the end of September 2018, to give a better view of how widespread these shortcomings are and what impact they may have on the credit profile of Australian banks.

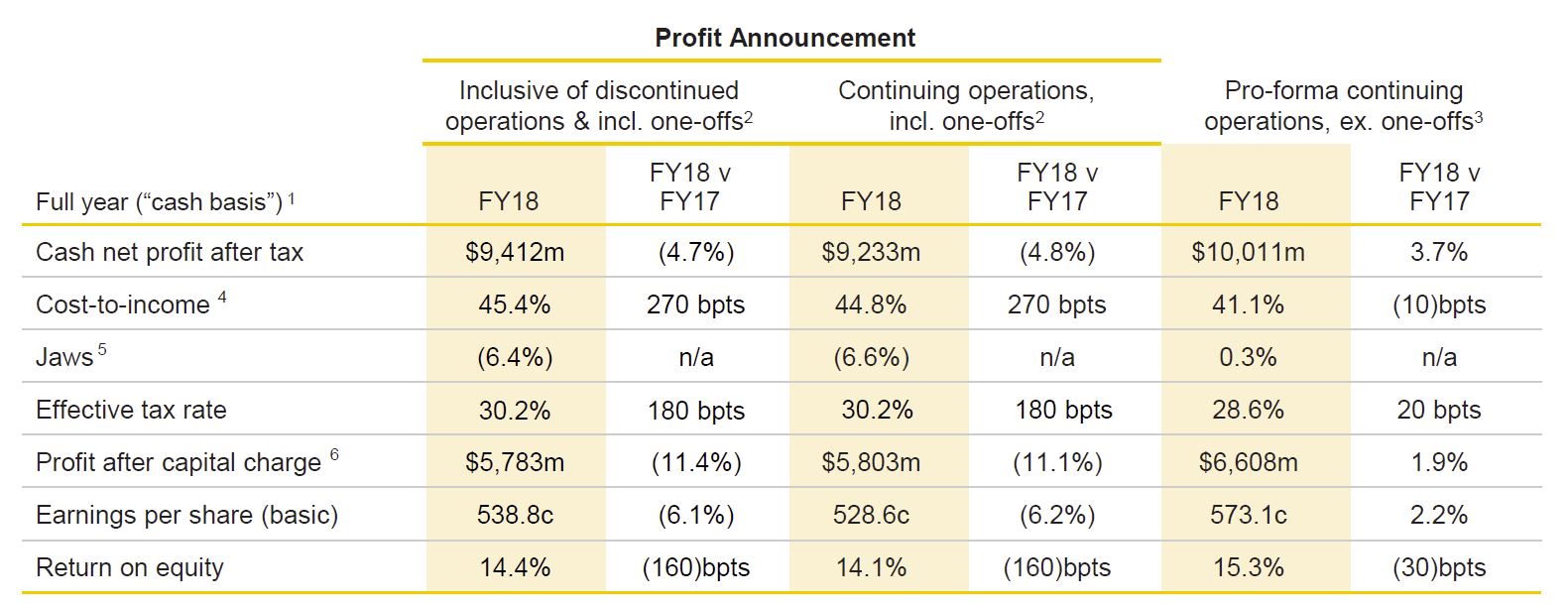

CBA’s FY18 results show a level of resiliency despite these issues. The bank reported cash net profit after tax from continuing operations declined 5% to AUD9.2 billion in FY18, but this was driven by a number of one-off charges, including a AUD700 million fine to settle a civil case in relation to breaches of anti-money laundering and counter-terrorism financing requirements. Cash net profit after tax from continuing operations rose by 4% to AUD10.0 billion when the one-off items were excluded.

Balance-sheet metrics remain consistent with Fitch’s expectations. The bank reported a stable common equity Tier 1 ratio of 10.1%, which incorporates the AUD1 billion additional operational risk charge (essentially an increase of AUD12.5 billion in operational risk-weighted assets) put in place following the publication of the independent prudential inquiry report in May 2018. The divestiture of a number of assets planned for FY19 as well as CBA’s ability to generate capital through retained earnings mean the bank is well-positioned to meet the regulator’s “unquestionably strong” capital requirements ahead of schedule. CBA’s liquidity coverage ratio (131%) and net stable funding ratio (112%) both increased due to an improvement in the bank’s deposit mix towards more stable deposit types and a lengthening in the average term to maturity of its wholesale funding.

Fitch continues to monitor CBA’s progress in remediating shortcomings in its operational risk controls and governance identified in the May 2018 independent prudential inquiry report as risks around this process were a key driver of Fitch’s revision of CBA’s Outlook to Negative. CBA noted in the FY18 results announcement that the remediation program has received approval from the Australian Prudential Regulation Authority and that it aims to make significant progress in implementing the program over FY19. However, CBA also noted that full remediation would be a multiyear process for the bank.

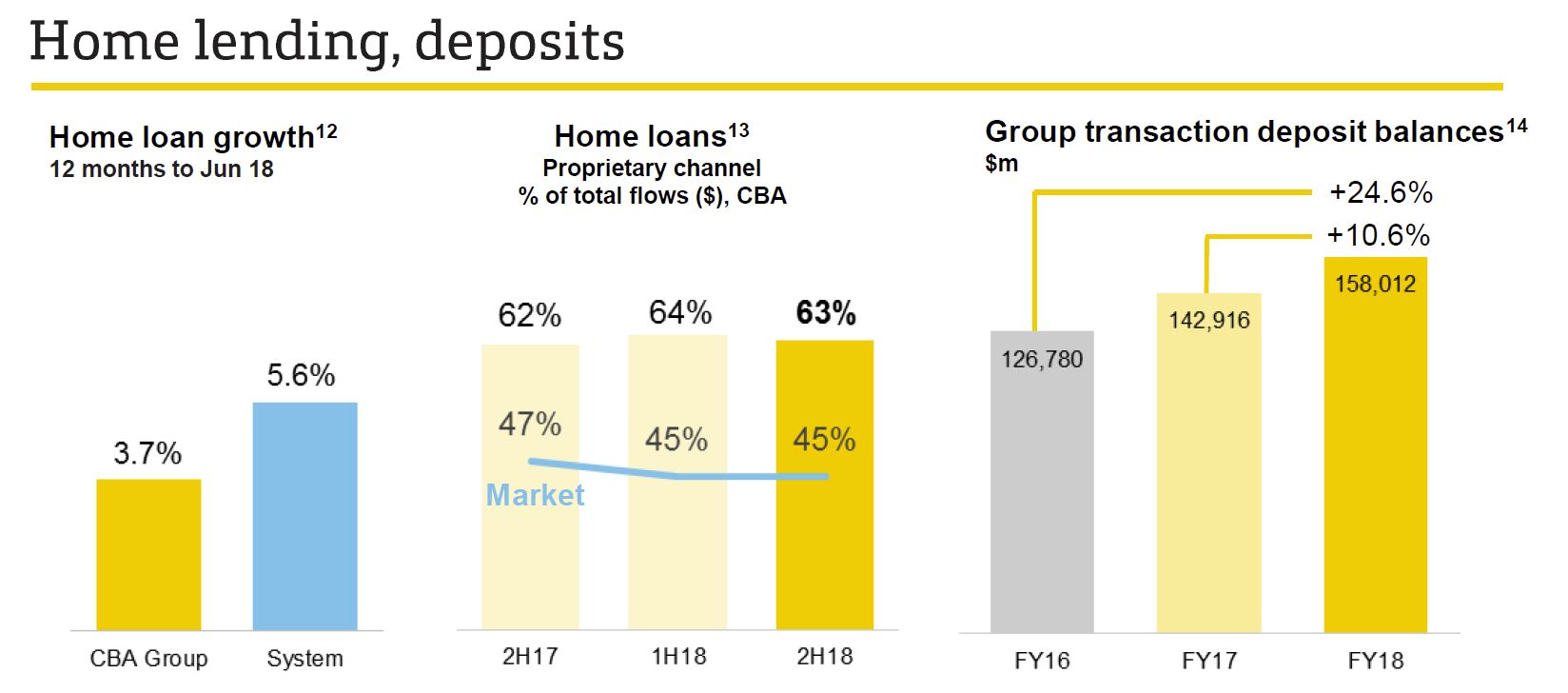

In the CBA’s full-year 2018 (FY19) financial results, released yesterday, the share of new home loans originated by brokers dropped from 43 per cent in FY17 to 41 per cent in FY18, as they focus on “their core market”.

CBA’s net profit after tax (NPAT) also took a hit over FY18, falling by 4.8 per cent to $9.23 billion, the first profit decline in 9 years. NIM was lower in the second half.

They warned of higher home loan defaults “as some households experienced difficulties with rising essential costs and limited income, leading to some pockets of stress”.

CEO Matt Comyn attributed the decline in profit growth to “one-off” payments, which included CBA’s $700 million AUSTRAC penalty, the $20 million settlement paid to ASIC for alleged bank bill swap rate (BBSW) rigging, and $155 million in regulatory costs incurred from the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

“There has been a number of one-off items that have impacted the result, including a couple of large penalties that we have resolved. If you strip some of those out, actually the result looks more from an underlying perspective up 3.7 per cent,” Mr Comyn said.

The number of broker-originated loans as a proportion of all new business settled by the major bank has dropped alongside a fall in residential lending.

Over the same period, the total number of home loans settled by CBA also dropped from $49 billion in FY17 to $45 billion in FY18.

The bank’s overall mortgage portfolio now totals $451 billion, with the share of broker-originated loans slipping from 46 per cent in FY17 to 45 per cent in FY18.

In its presentation notes, CBA made specific reference to the bank’s focus on its “core market” of owner-occupied lending through its propriety channel, with the number of loans settled through its direct channel rising from 57 per cent to 59 per cent in FY18, and the share of new owner-occupied mortgages also growing from 67 per cent to 70 per cent.

The share of investor loans settled by CBA over FY18 declined from 33 per cent to 29 per cent, now making up 32 per cent of the major bank’s mortgage portfolio.

Interest-only lending fell sharply over FY18, falling by 18 per cent from 41 per cent of new loans settled in FY17 to 23 per cent in FY18.

The proportion of new loans settled with variable rates increased in FY18, from 85 per cent to 86 per cent (81 per cent of CBA’s portfolio).

CBA CEO Matt Comyn attributed the fall in the bank’s home lending to risk and pricing adjustments introduced by the lender over the financial year.

“[We] have been prepared to make some choices from both a risk and pricing perspective, which has seen us grow below system in home lending,” the CEO said.

“We will continue to make the right choices from volume and margin as we think about our home lending business. But overall, the core franchise of the retail bank has continued to perform well.”

Mr Comyn also claimed that despite slowing credit and housing conditions, he expects the bank to generate 4 per cent credit growth in FY19 and noted that CBA would not be looking to make any further changes to its lending policy.

“Consistent with the remarks from the chair of APRA, we see that the majority of the tightening work has been done, certainly at the margin, and there’s certainly some potential in the application of those policy changes,” the CEO continued.

“[We] certainly don’t see any big policy adjustments on the horizon. We feel like that 4 per cent credit growth, given what we’re seeing at the moment in the system, is about right, and of course, it’ll be a function of our performance against that system.”