CBA released their latest trading update today, with a rise in profit, and volumes as well as a lift in capital. Expenses were higher reflecting some provisions relating to AUSTRAC, but loan impairments were lower. WA appears to be the most problematic state.

Their unaudited statutory net profit was approximately $2.80bn in the quarter and their unaudited cash earnings was approximately $2.65bn in the quarter, up 6% (on average of two FY17 second half quarters). Both operating income and expense was up 4%.

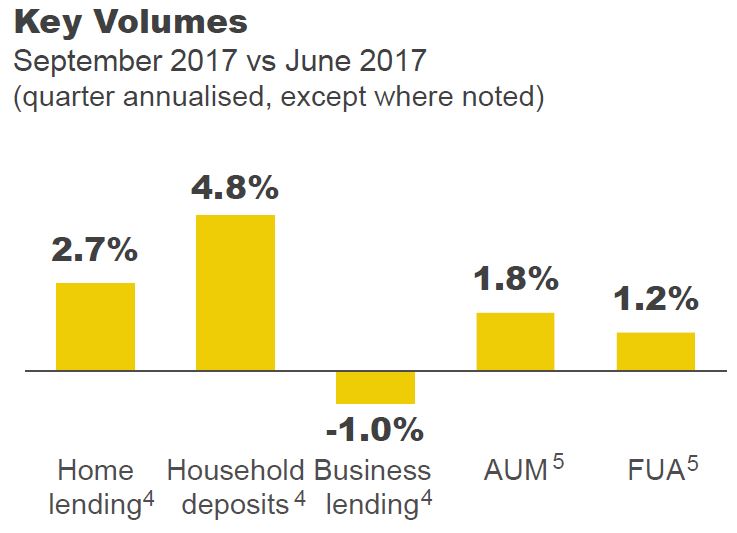

Operating income grew by 4%, with banking income supported by improved margins. Home lending growth was managed within regulatory limits.

Operating income grew by 4%, with banking income supported by improved margins. Home lending growth was managed within regulatory limits.

Trading income was broadly flat. Funds management income decreased slightly, with lower margins partly offset by the benefit of positive investment markets, which contributed to AUM and FUA growth in the quarter.

Insurance income improved reflecting fewer weather events and the non-recurrence of loss recognition.

Group Net Interest Margin was higher in the quarter driven by asset repricing and reduced liquid asset balances, partly offset by the impact of the banking levy, higher funding costs and competition.

Expense growth of 4% includes provisions for their current estimates of future project costs associated with regulatory actions and compliance programs – including those related to the Australian Transaction Reports and Analysis Centre (AUSTRAC) proceedings. On 3 August 2017, AUSTRAC commenced civil penalty proceedings against CBA. CBA is preparing to lodge its defence in response to the allegations in the Statement of Claim and at this time it is not possible to reliably estimate any potential penalties relating to these proceedings. Any such potential penalties are therefore excluded from these provisions.

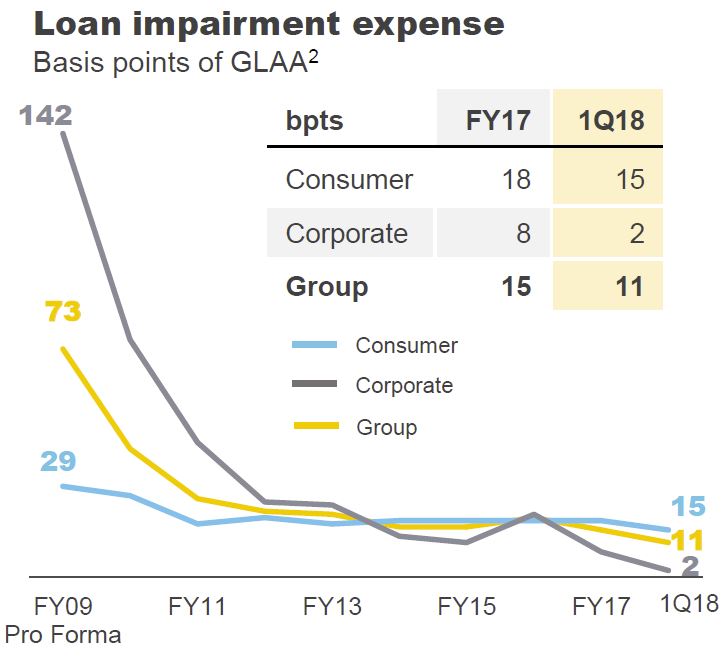

Loan Impairment Expense (LIE) of $198 million in the quarter equated to 11 basis points of Gross Loans and Acceptances, compared to 15 basis points in FY17.

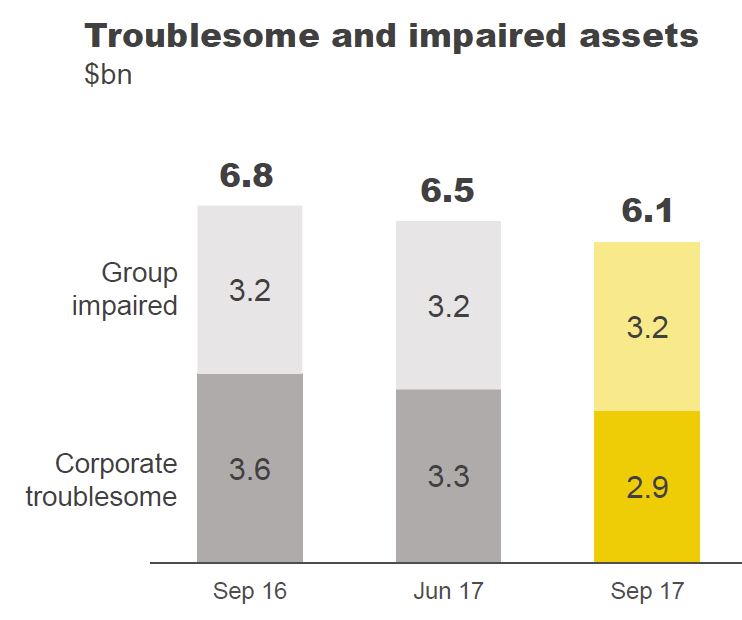

Corporate LIE was substantially lower in the quarter. Troublesome and impaired assets were lower at $6.1 billion, with broadly stable outcomes across most sectors.

Corporate LIE was substantially lower in the quarter. Troublesome and impaired assets were lower at $6.1 billion, with broadly stable outcomes across most sectors.

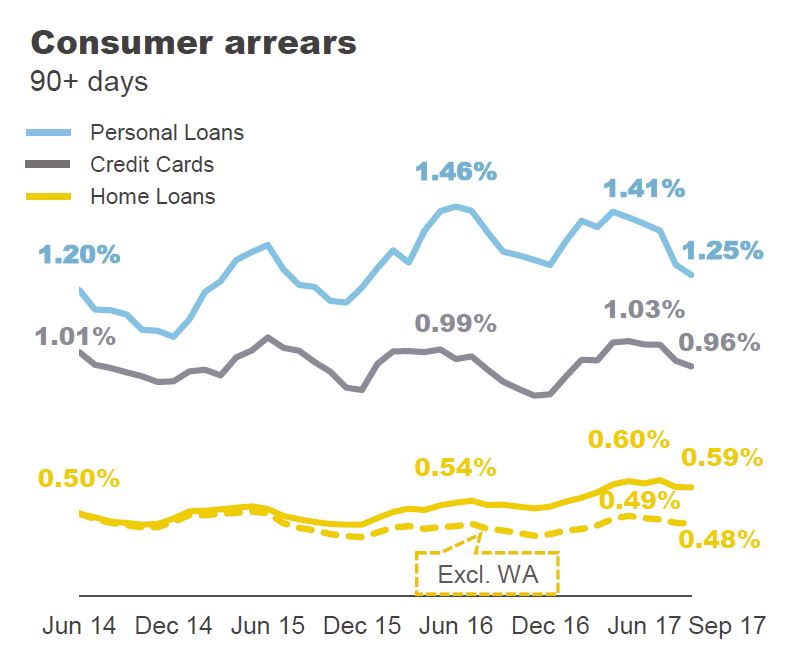

Consumer arrears were seasonally lower but continued to be elevated in Western Australia.

Consumer arrears were seasonally lower but continued to be elevated in Western Australia.

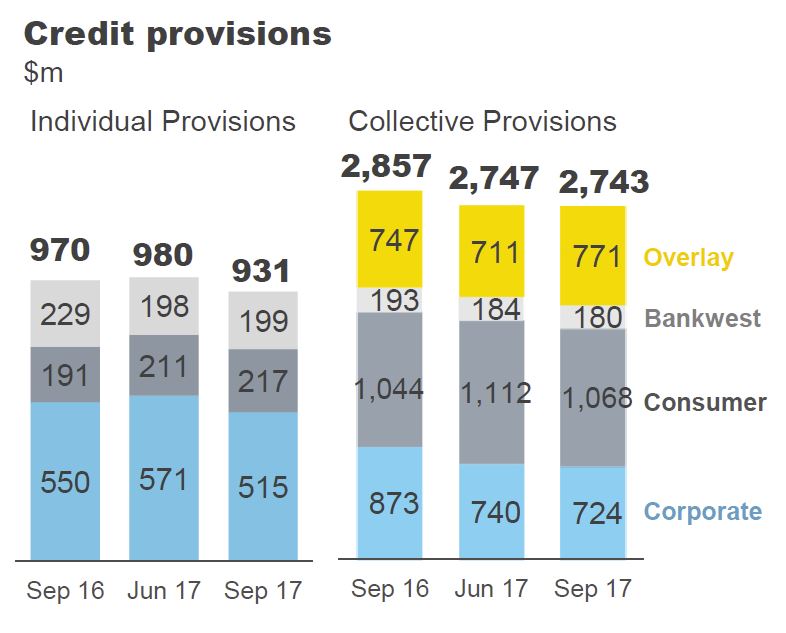

Prudent levels of credit provisioning were maintained, with Total Provisions at approximately $3.7 billion.

Prudent levels of credit provisioning were maintained, with Total Provisions at approximately $3.7 billion.

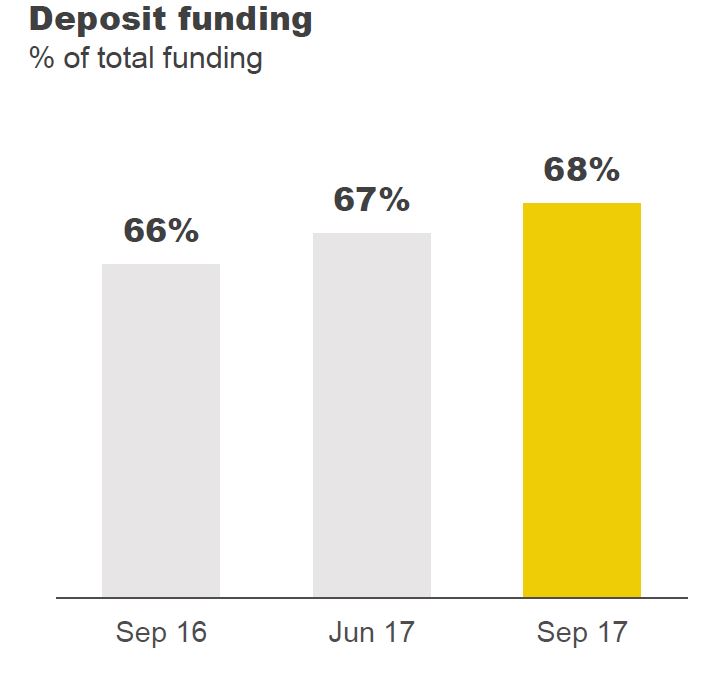

68% of their balance sheet is funded from deposits.

68% of their balance sheet is funded from deposits.

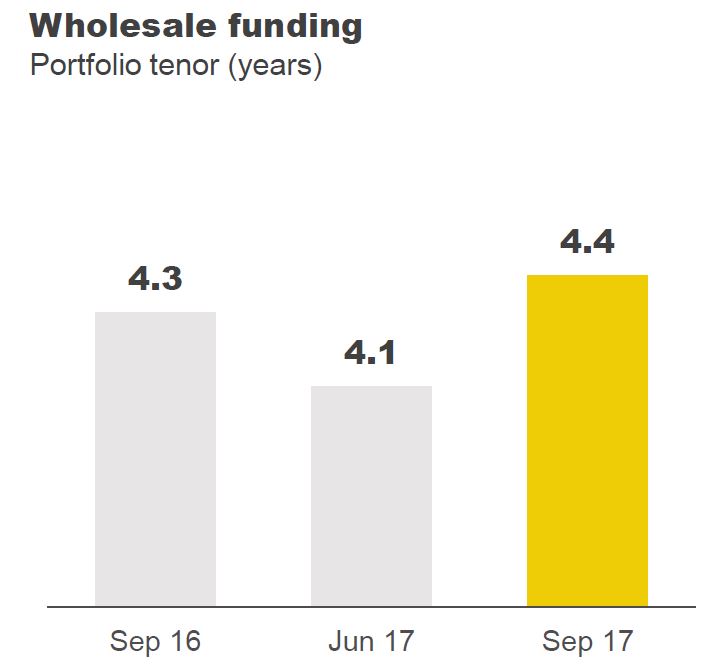

The average tenor of wholesale funding extended a little. The Group issued $9.5 billion of long term funding in the quarter, including a 30 year US$1.5bn issue –a first for an Australian major bank.

The average tenor of wholesale funding extended a little. The Group issued $9.5 billion of long term funding in the quarter, including a 30 year US$1.5bn issue –a first for an Australian major bank.

The Net Stable Funding Ratio (NSFR) was 107% at September 2017.

The Net Stable Funding Ratio (NSFR) was 107% at September 2017.

The Liquidity Coverage Ratio (LCR) was 131% as at September 2017, with liquid asset balances and net cash outflows moving by similar amounts in the quarter. Liquid assets totalled $132 billion as at September 2017.

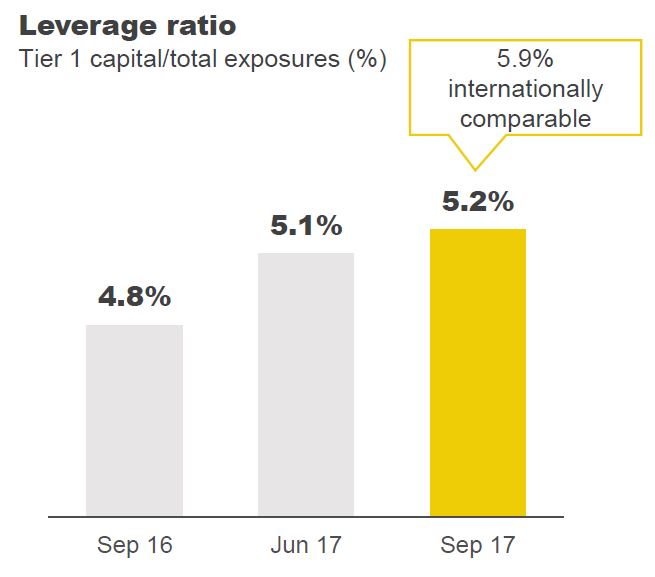

The Group’s Leverage Ratio was 5.2% on an APRA basis and 5.9% on an internationally comparable basis, an increase under both measures of 10 basis points on June 17.

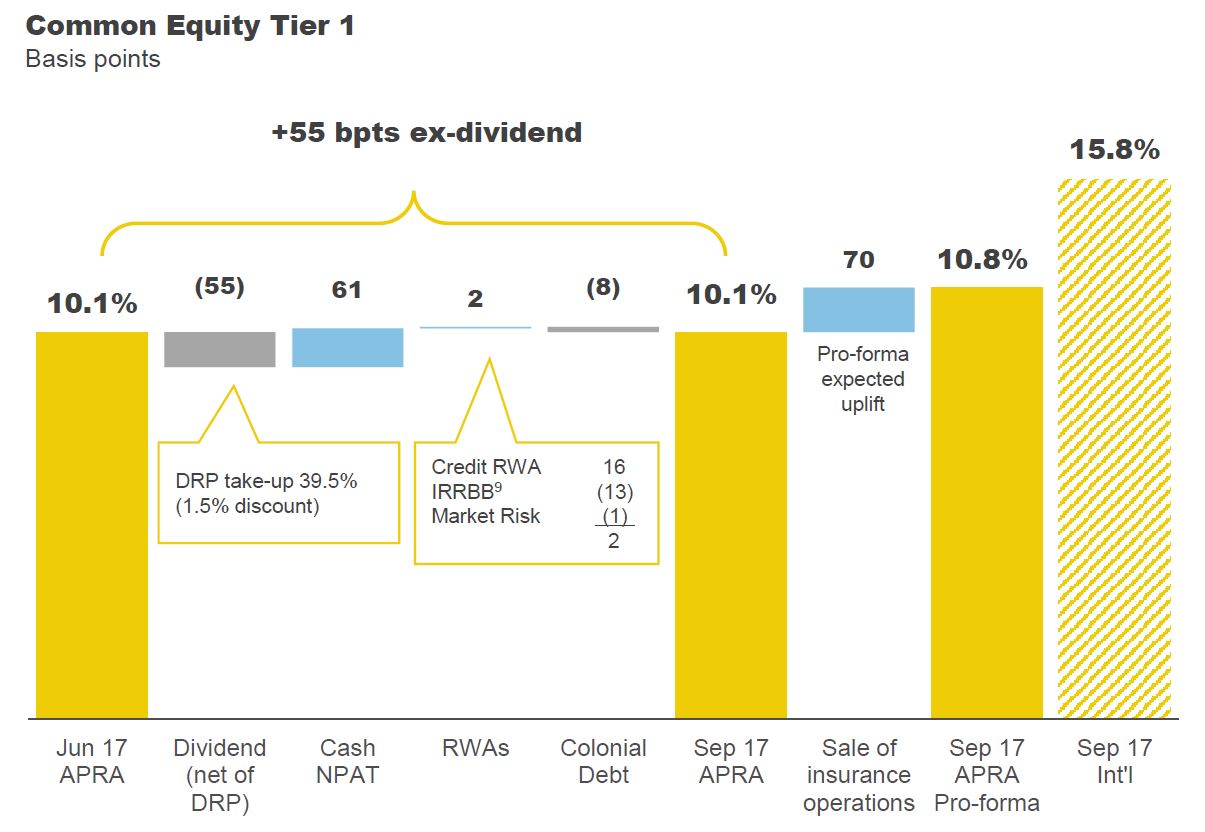

The Group’s Common Equity Tier 1 (CET1) APRA ratio was 10.1% as at 30 September 2017. After allowing for the impact of the 2017 final dividend (which included the issuance of shares in respect of the Dividend Reinvestment Plan), CET1 increased 55 basis points in the quarter.

The Group’s Common Equity Tier 1 (CET1) APRA ratio was 10.1% as at 30 September 2017. After allowing for the impact of the 2017 final dividend (which included the issuance of shares in respect of the Dividend Reinvestment Plan), CET1 increased 55 basis points in the quarter.

Credit Risk Weighted Assets (RWAs) were lower in the quarter, contributing 16 basis points to CET1, partially offset by higher IRRBB9(-13 bpts) driven by interest rate movements and risk management activities.

Credit Risk Weighted Assets (RWAs) were lower in the quarter, contributing 16 basis points to CET1, partially offset by higher IRRBB9(-13 bpts) driven by interest rate movements and risk management activities.

The maturity of a further $350m of Colonial debt compressed CET1 by 8 basis points in the quarter. The final tranche of Colonial debt ($315m) is due to mature in the June 2018 half year, with an estimated CET1 impact of -7 basis points.

In September 2017 the Group announced the sale of its Australian and New Zealand life insurance operations to AIA Group Ltd. The sale is expected to be completed in calendar year 2018 and is expected to result in a pro-forma uplift to the CET1 (APRA) ratio of approximately 70 basis points.