The Australian Bankers Association (ABA) says the APRA decision “will increase choice for home loan customers”.

They say:

Today’s announcement of the removal of the 30% benchmark for new interest-only residential mortgages will allow all banks to offer more choice for customers, leading to an increase in competition across the industry, particularly for smaller and regional banks.

The benchmark was introduced by APRA in 2017 to respond to concerns of an oversupply of interest-only loans. The benchmark had a greater effect on banks with smaller home loan lending operations.

CEO of the Australian Banking Association Anna Bligh said that the decision by APRA would not only benefit customers, it also showed that banks were lending prudently with the proportion of interest-only loans more than halving in two years.

“APRA’s announcement today shows that banks have adjusted lending to respond to concerns around an oversupply of interest-only loans, illustrating a prudential system where both banks and regulators can quickly and effectively respond to a changing environment,” Ms Bligh said.

“While banks will continue to lend prudently, today’s decision will mean all banks can offer more choice for customers who are looking to buy a house or apartment.

“Increased competition across the industry will mean customers have more ability to shop around for the best deal for them when looking at an interest-only home loan,” she said.

In terms of banks home loan commitments, the proportion of interest-only loans are now 16.2% much lower than the proportion seen two years ago (37%).

The Australian Prudential Regulation Authority (APRA) has announced that it will remove its supervisory benchmark on interest-only residential mortgage lending by authorised deposit-taking institutions (ADIs).

The benchmark was put in place as a temporary measure in March 2017, as part ofa range of actions over recent years to reinforce sound lending practices. The introduction of the benchmark has led to a marked reduction in the proportion of new interest-only lending, which is now significantly below the 30 per cent threshold.

Earlier this year, APRA announced its intention to remove the supervisory benchmark on investor loan growth subject to ADIs providing certain assurances as to the strength of their lending standards. Most ADIs have now provided those assurances. ADIs that are no longer subject to the investor loan growth benchmark will also no longer be subject to the benchmark on interest-only lending from 1 January 2019. For other ADIs, it will be removed concurrently with the removal of the investor loan growth benchmark.

APRA Chairman Wayne Byres said: “APRA’s lending benchmarks on investor and interest-only lending were always intended to be temporary. Both have now served their purpose of moderating higher risk lending and supporting a gradual strengthening of lending standards across the industry over a number of years.”

Notwithstanding the removal of the interest-only benchmark, ADIs still need to ensure they maintain adequate oversight of the level and type of interest-only lending, consistent with APRA’s Prudential Practice Guide APG223 Residential Mortgage Lending and ASIC’s responsible lending obligations on borrower requirements and objectives.

A welcome move, the shadowy Council Of Financial Regulators has started publishing minutes of its quarterly meetings. However, group think, and self-interest is all over it. Specifically the comments about tighter credit, and the need to continue to lend (to keep the debt bomb ticking a bit longer! Also how does independence of the RBA work in this context?

They noted that non-ADI lending for housing has been growing significantly faster than ADI housing lending and there is some evidence that non-ADI lending for property development is also increasing quickly.

As part of its commitment to transparency, the Council of Financial Regulators (the Council) has decided to publish a statement following each of its regular quarterly meetings. This is the first such statement.

The statement will outline the main issues discussed at each meeting. From time to time the

Council discusses confidential issues that relate to an individual entity or to policies still

in formulation. These issues will only be included in the statement where it is appropriate to

do so.

The Council of Financial Regulators (the Council) is the coordinating body for Australia’s

main financial regulatory agencies. There are four members: the Australian Prudential

Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC),

the Australian Treasury and the Reserve Bank of Australia (RBA). The Reserve Bank Governor

chairs the Council and the RBA provides secretariat support. It is a non-statutory body,

without regulatory or policy decision-making powers. Those powers reside with its members.

The Council’s objectives are to contribute to the efficiency and effectiveness of financial

regulation, and to promote stability of the Australian financial system. The Council

operates as a forum for cooperation and coordination among member agencies. It meets each

quarter, or more often if required.

At each meeting, the Council discusses the main sources of systemic risk facing the

Australian financial system, as well as regulatory issues and developments relevant to its

members. Topics discussed at its meeting on 10 December 2018 included the following:

Financing conditions. Members discussed the tightening of credit conditions for households

and

small businesses. A tightening of lending standards over recent years has been appropriate

and

has strengthened the resilience of the system. At the same time, members agreed on the

importance of lenders continuing to supply credit to the economy while they adjust their

lending

practices, including in response to the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry. Members discussed how an overly cautious

approach by some lenders to incorporating relevant laws and standards into loan approval

processes may be affecting lending decisions.

Members observed that housing credit growth has moderated since mid-2017, with both demand

and supply factors playing a role. The demand for credit by investors has slowed noticeably,

largely reflecting the change in the dynamics of the housing market. In an environment of

tighter lending standards, the decline in average interest rates for owner-occupier and

principal and interest loans suggests that there is relatively strong competition for

borrowers of low credit risk. Credit to owner-occupiers is continuing to grow at 5 to 6 per

cent.

Non-ADI lending. The Council undertook its annual review of non-bank financial

intermediation. Overall, lending by non-ADIs remains a small share of all lending. However,

non-ADI lending for housing has been growing significantly faster than ADI housing lending

and there is some evidence that non-ADI lending for property development is also increasing

quickly. The Council supported efforts to expand the coverage of data on non-ADI lenders,

drawing on new data collection powers recently granted to APRA.

Housing market. Members discussed recent developments in the housing market.

Conditions have eased, but this follows a period of considerable strength in the market.

Housing prices have been declining in Sydney, Melbourne and Perth, but are stable or rising

in most other locations. The easing in the housing market is occurring in a period of

favourable economic conditions, with low domestic unemployment and interest rates and a

supportive global economy. The Council will continue to closely monitor developments.

Prudential measures. APRA briefed the Council on its latest review of the countercyclical

capital buffer, the results of which will be published in the new year. It also provided an

update on its residential mortgage measures, including the investor lending and

interest-only lending benchmarks. In line with APRA’s announcement in April 2018 that it

would remove the investor lending benchmark subject to assurances of the strength of lending

standards, the benchmark has now been removed for the majority of ADIs. The interest-only

lending benchmark, introduced in 2017, has resulted in a reduction in the share of new

interest-only lending, along with the share of interest-only lending that occurs at high

loan-to-valuation ratios.

Financial sector competition. The Council discussed work by its member agencies in response

to the Productivity Commission’s Final Report of its Inquiry into Competition in the

Australian Financial System. The Council strongly supports improved transparency of mortgage

interest rates and a working group is examining a number of options. The Council also

discussed the Productivity Commission’s recommendations relating to lenders mortgage

insurance and remuneration of mortgage brokers.

Both the Productivity Commission and the Financial System Inquiry recommended a review of the

regulation of payments providers that hold stored value – referred to in legislation as

purchased payment facilities (PPFs). The Council released an issues paper in September and held

an industry roundtable in November. Members considered the feedback received from these

processes and received an update on progress with the review.

Limited recourse borrowing by superannuation funds. Members discussed a report to Government

on leverage and risk in the superannuation system, as requested in the Government’s response to

the Financial System Inquiry. The use of limited recourse borrowing arrangements remains

relatively small, but has risen over time. Leverage by superannuation funds can increase

vulnerabilities in the financial system, though near-term risks have reduced with the shift in

dynamics in the housing market.

International Monetary Fund’s Financial Sector Assessment Program (FSAP). The FSAP review of

Australia was conducted during the course of 2018; preliminary findings were presented to the

Australian authorities in November. The Council held an initial discussion of the main FSAP

recommendations and how they could be addressed. The FSAP will be finalised in early 2019, at

which time summary documents will be published. (Further information on the FSAP review was

published in the Reserve Bank’s October 2018

Financial Stability Review.)

Representatives of the Australian Competition and Consumer Commission and the Australian

Taxation Office attended the meeting for discussions relevant to their responsibilities.

The Australian Prudential Regulation Authority (APRA) has today

released a package of new and enhanced prudential requirements designed

to strengthen the focus of registrable superannuation entity (RSE)

licensees on the delivery of quality outcomes for their members.

A central component of APRA’s new framework is the introduction of an

outcomes assessment that will require RSE licensees to annually

benchmark and evaluate their performance in delivering sound,

value-for-money outcomes to all members – covering both MySuper and

choice products.

APRA deputy chairman Helen Rowell said APRA was committed to lifting

standards across the industry for the long-term benefit of

superannuation members.

“As the prudential regulator, APRA’s primary focus is on the sound

and prudent management of the $1.8 trillion APRA-regulated segment of

the superannuation industry; that includes seeking to ensure that RSE

licensees meet their obligations to put their members’ interests first,”

Mrs Rowell said.

“These changes to the prudential framework set a higher bar for RSE

licensees by requiring a robust assessment of the outcomes delivered for

members to be reflected in their strategic and business planning.”

In addition to the outcomes assessment, APRA’s final package requires

RSE licensees to meet strengthened requirements for strategic and

business planning, including management and oversight of fund

expenditure and reserves. These requirements are set out in new

Prudential Standard SPS 515 Strategic Planning and Member Outcomes.

The Treasury Laws Amendment (Improving Accountability and Member

Outcomes in Superannuation Measures No.1) Bill 2017 (the Bill) that is

before Parliament would, if passed, introduce a legislated outcomes

assessment.

APRA said its proposals are consistent with the outcomes assessment

proposals in the Bill, and are being introduced now to “maintain

industry momentum” towards delivering improved outcomes for members.

APRA will review whether amendments are needed to the prudential

framework requirements if the Bill is passed by Parliament in future.

Mrs Rowell also emphasised APRA’s strong support for the other

reforms contained in the Bill and, in particular, the enhanced

directions powers for APRA, the strengthened MySuper authorisation and

cancellation provisions, and the requirement for APRA to approve changes

of ownership of RSE licensees.

“These new policy proposals address weaknesses in the current

superannuation regulatory framework and would greatly assist APRA in

driving the superannuation industry towards addressing underperformance

and improving member outcomes,” she said.

APRA’s finalised package of measures is the culmination of extensive

industry engagement that commenced in August 2017, and includes

amendments to the original proposals taking into account the feedback

received during consultation.

The commencement date for the new measures has been set as 1 January

2020, to provide industry with sufficient time to meet the new

requirements.

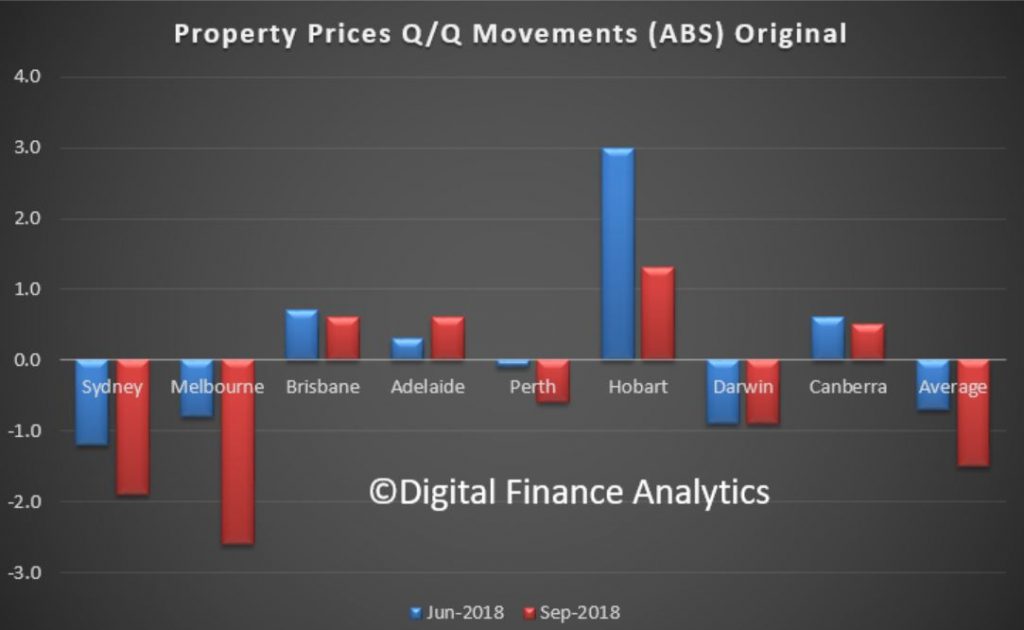

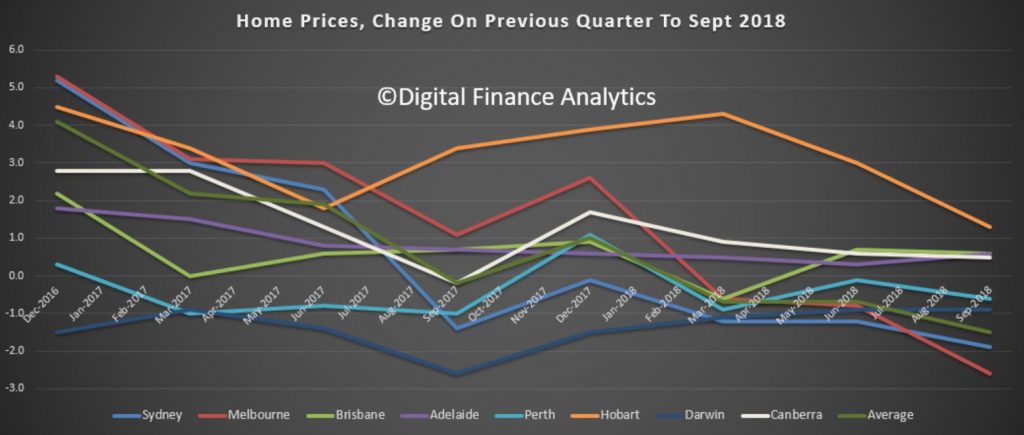

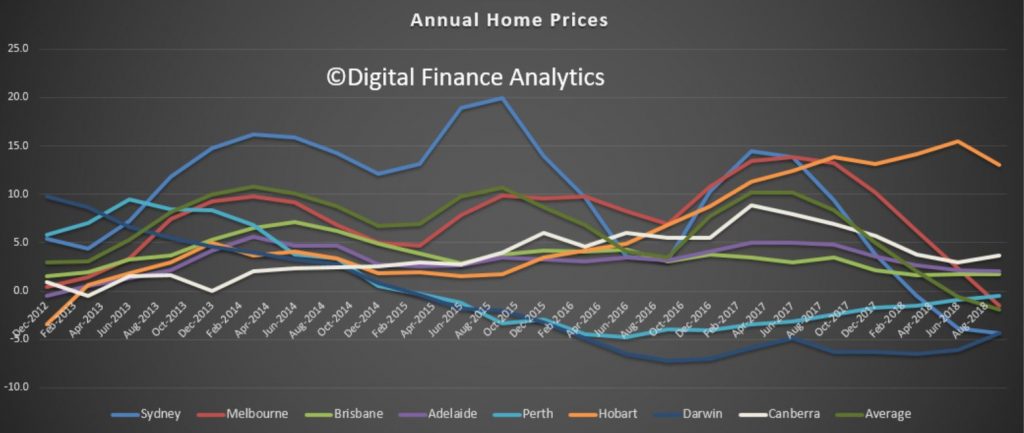

They said that the price index for residential properties for the weighted average of the eight capital cities fell 1.5% in the September quarter 2018. The index fell 1.9% through the year to the September quarter 2018.

The capital city residential property price indexes fell in Melbourne (-2.6%), Sydney (-1.9%), Perth (-0.6%) and Darwin (-0.9%), and rose in Brisbane (+0.6%), Adelaide (+0.6%), Hobart (+1.3%) and Canberra (+0.5%).

Annually, residential property prices fell in Sydney (-4.4%), Darwin (-4.4%), Melbourne (-1.5%), Perth (-0.5%) and rose in Hobart (+13.0%), Canberra (+3.7%), Adelaide (+2.0%) and Brisbane (+1.7%).

The total value of residential dwellings in Australia was $6,847,057.2m at the end of the September quarter 2018, falling $70,148.6m over the quarter.

The mean price of residential dwellings fell $9,700 to $675,000 and the number of residential dwellings rose by 40,900 to 10,143,700 in the September quarter 2018.

Of course these averages do not tell the true picture, because the movements are not uniform across a state. In some post codes now we are seeing falls of more than 20% from the previous peak, elsewhere prices are holding more steadily. However, given credit availability drives home prices, and credit is harder to come by, we should expect more falls ahead. Then the question becomes, is a soft landing feasible? I have to say that all the cycles I have examined never ended softly, so it would be a first, if it did happen.

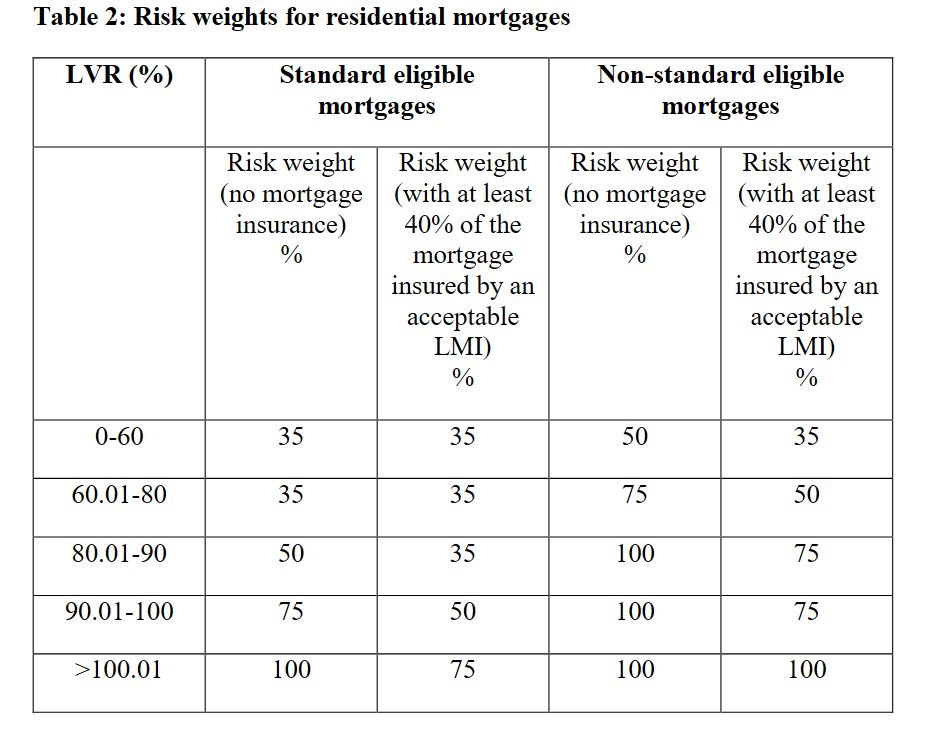

But there is another point to consider. Major banks use internal risk models to calculate the amount of capital they hold against mortgage loans. Other banks use more standard approaches.

The calculation is driven by a range of factors, but LVR is one element. Here is the APRA risk weights table. The point is a loan with an LVR at 80% has a risk weight of 50%, but the same loan at 90% LVR requires 75%, and 100% LVR 100% weighting. In other words, the capital doubles between 80 and 100% LVR!

At some point quite soon now banks will need to re-baseline their mortgage books. When property prices were rising, they would do this quite regularly to reduce the capital requirement. The reverse is also true.

The governing APRA document says “The ADI must also revalue any property offered as security for such loans when it becomes aware of a material change in the market value of property in an area or region”. Have banks started to revalue their portfolios and up their risk weights in the light of these falls? This is also, by the way, why economists attached to the major banks have an interest in playing down potential home price falls.

APRA says “the valuation may be based on the valuation at origination or, where relevant, on a subsequent formal revaluation by an independent accredited valuer. The determination of the appropriate risk weight is also dependent upon mortgage insurance provided by an acceptable lenders mortgage insurer (LMI)”. Of course many lenders now have access to Automated Valuation Models from players such as CoreLogic.

So now the question becomes, how much more capital will the banks have to put aside to take account of falling prices, who will bear the cost, and will APRA back down on its capital requirements which insist the banks hold more capital ahead? I expect more weakness in bank share prices as the impact of this hits home. As home prices fall further the impact will be magnified.

The board of IOOF Holdings has today announced that IOOF managing director, Christopher Kelaher and chairman, George Venardos, have agreed to step aside from their respective positions effective immediately, pending resolution of proceedings brought by the Australian Prudential Regulation Authority (APRA) and announced last Friday, 7 December.

Mr Renato Mota, currently group general manager – wealth management,

has been appointed acting chief executive officer and Mr Allan

Griffiths, a current non-executive director of IFL, is acting chairman.

Both Mr Kelaher and Mr Venardos will be on leave while they focus on

defending the actions brought against them by APRA.

Chief financial officer David Coulter, company secretary Paul Vine

and general counsel Gary Riordan will remain in their positions, however

will have no responsibilities in relation to the management of the IOOF

trustee companies and will have no engagement at all with APRA during

this period, including in relation to the matters the subject of APRA’s

announcement of Friday 7 December.

“We maintain our position that the allegations made by APRA are

misconceived, and will be vigorously defended. The Board believes that,

in the interests of good governance, it is appropriate that Chris and

George step aside from their positions. The Board will also commence a

search for an additional non-executive Director,” Acting chairman, Allan

Griffiths said

“We acknowledge the seriousness of these allegations. We have a

responsibility to our superannuation members, shareholders, advisers,

employees and the wider community, to take decisive action.

“We are entirely focused on addressing the governance issues in the

interests of all stakeholders and will do so in an orderly manner.

“I will personally lead our review of the situation and, alongside

acting CEO Renato Mota, will work cooperatively with APRA to continue to

implement previously agreed initiatives. Many of these actions are

already complete.”

IOOF posted an underlying net profit after tax result in financial

year 2018 of $191.4 million, up 13 per cent on the financial year 2017

result.

“These results have been delivered by our unwavering commitment to

our clients, driven by our talented people and a recognition of the

importance of advice. We remain committed to the ANZ transaction and we

are working cooperatively with ANZ as they consider their position,” Mr

Griffiths said.

The prudential regulator is seeking to impose additional licence

conditions and issue directions to APRA-regulated entities in the IOOF

group.

The proceedings in the Federal Court seek to disqualify five

individuals that were responsible persons at IOOF Investment Management

Limited (IIML) and Questor Financial Services.

The proceedings are also seeking a court declaration that IIML and Questor breached the SIS Act.

The announcement drove ANZ to rethink the sale of its wealth business

to IOOF. ANZ released an update on its sale following APRA’s move to

disqualify IOOF individuals and its move to apply licence restrictions

on the group.

ANZs deputy chief executive Alexis George said ANZ would reassess the

sale of its OnePath Pensions and Investments business to IOOF.

“Given the significance of APRA’s action, we will assess the various

options available to us while we seek urgent information from both IOOF

and APRA.

“The work to separate Pensions and Investments from our Life

Insurance business continues. There is a framework available to complete

the Zurich transaction that does not involve IOOF,” he said.

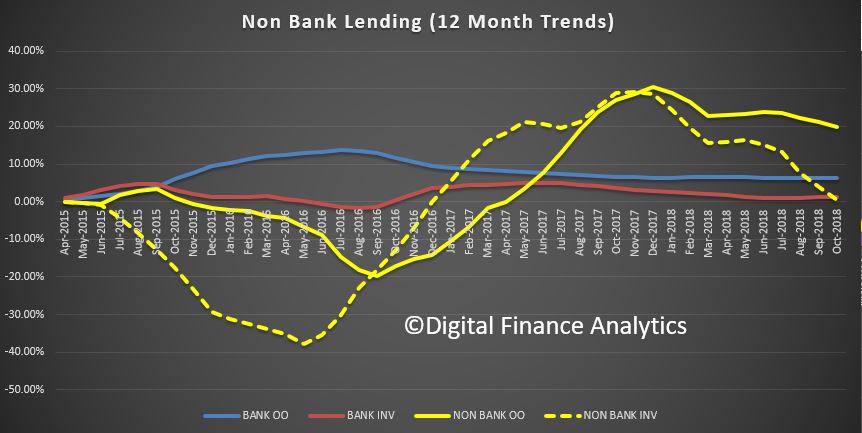

The analysis of the monthly banking stats out last week gives us the opportunity to look across the non-bank sector, relative to the banking sector by comparing the APRA data with the Reserve Bank data series.

We have plotting the rolling 12 month trends, and this chart shows the results.

The striking observation is the relatively stronger growth rate relative to the banks supervised more directly by APRA. Granted APRA does have some responsibilities for the non-bank sector, but appear not to be their main focus.

All lenders have the same obligation with regards to responsible lending, but non-banks are generally more flush with cash, and less constrained by the capital requirements which crimp ADI’s.

Thus we can expect the growth on non-ADI mortgage lending to continue at a faster pace than the bank sector. As a result, we think more risks are building in the financial system.

The Australian Prudential Regulation Authority (APRA) has announced a number of actions against IOOF entities, directors and executives for failing to act in the best interests of superannuation members.

APRA has commenced disqualification proceedings and is seeking to impose additional licence conditions and issue directions to APRA-regulated entities in the IOOF group.

APRA has issued a show cause notice setting out APRA’s intention to direct IOOF Investment Management Limited (IIML) to comply with its Registrable Superannuation Entity (RSE) Licence and impose additional conditions on the licenses of IIML, Australian Executor Trustees Limited (AET) and IOOF Ltd (IL). These entities have 14 days to respond to this notice.

The proposed conditions and directions to comply with conditions seek to achieve significant changes to the identification and management of conflicts of interest by IIML, AET and IL and facilitate APRA’s ability to take further enforcement action should this not occur. The proposed additional conditions on the licences of IIML, AET and IL are based on issues and concerns raised by APRA since 2015 relating to the entities’ organisational structure, governance and conflicts management frameworks, and require the entities to address these within specified timeframes. The proposed directions for IIML relate to an independent report issued by Ernst & Young, the findings of which provide a reasonable basis to conclude that IIML has breached section 52 of the Superannuation Industry (Supervision) Act 1993 (SIS Act), Prudential Standard SPS 520: Fit and Proper and Prudential Standard SPS 521: Conflicts of Interest.

APRA has also commenced proceedings in the Federal Court of Australia to seek the disqualification of five individuals that, at relevant times, were responsible persons of IIML and Questor Financial Services Limited (Questor). The proceedings also seek a court declaration that IIML and Questor (which at the material times were RSE Licensees owned by IOOF Holdings Limited) breached the SIS Act.

The individuals included in the disqualification proceedings are Managing Director Chris Kelaher, Chairperson George Venardos, Chief Financial Officer David Coulter, General Manager – Legal, Risk and Compliance and Company Secretary Paul Vine, and General Counsel Gary Riordan.

The Concise Statement seeks disqualification orders and declarations in relation to breaches of sections 52 and 55 of the SIS Act and Prudential Standards, and associated conduct. As outlined in the Concise Statement, APRA considers that IIML, Questor and the relevant individuals did not appropriately acknowledge and address issues concerning conflicts of interest raised by APRA from 2015 to date. In particular, APRA identified that on three separate occasions in 2015, Questor and IIML contravened the SIS Act by deciding to differentially compensate superannuation beneficiaries and other non-superannuation investors for losses caused by Questor, IIML or their service providers, with superannuation beneficiaries being compensated from their own reserve funds rather than the trustees’ own funds or third-party compensation.

If successful, the disqualification proceedings would prohibit the above individuals from being or acting as a responsible person of a trustee of a superannuation entity.

APRA Deputy Chair Helen Rowell said APRA had sought to resolve its concerns with IOOF over several years but considered it was necessary to take stronger action after concluding the company was not making adequate progress, or likely to do so in an acceptable period of time.

“APRA’s efforts to resolve its concerns with IOOF have been frustrated by a disappointing level of acceptance and responsiveness to the issues raised by APRA, which is not the behaviour we expect from an APRA-regulated entity,” Mrs Rowell said.

“The actions we are now taking are aimed at achieving enduring change to ensure that the trustees of the superannuation funds operated by IOOF fully meet their obligation to put the interests of members ahead of all other interests.

“Furthermore, the individuals included in the proceedings have shown a lack of understanding of their personal and trustee obligations under the SIS Act and at law, and a lack of contrition in relation to the breaches of the SIS Act identified by APRA.”

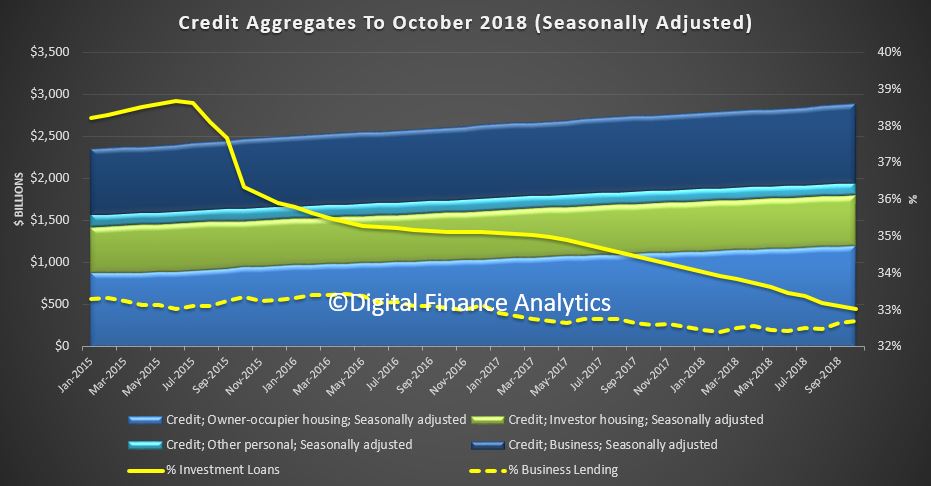

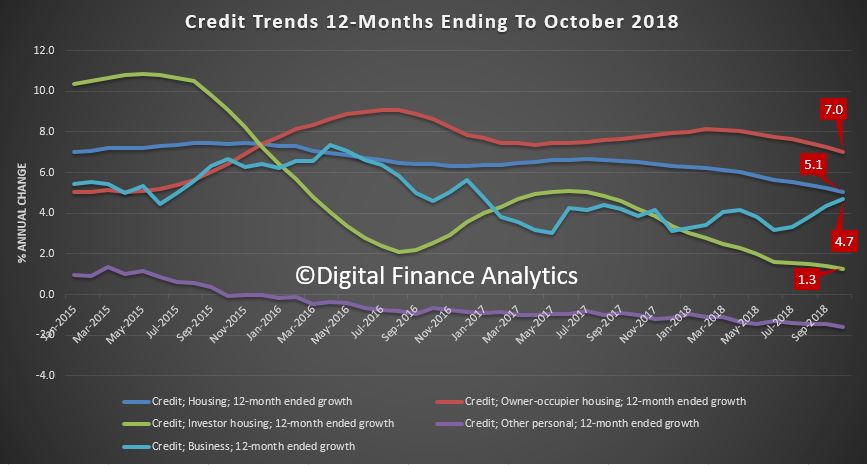

The RBA and APRA both released their statistics today to end of October. The data clearly shows the mortgage flows are easing, which is a key indicator of weaker home prices ahead. Remember it is the RATE of credit growth, or the credit impulse we need to watch. Essentially, for home prices to rise, the rate of credit growth needs to accelerate, and the reverse is also true as can be clearly seen.

The RBA credit aggregates shows that overall credit rose by 0.4% last month, or 4.6% over the past year. Housing credit rose by 0.3% in October, or 5.1% over the past year. Business credit rose 4.7% over the past year and 0.6% in October. Personal credit fell 1.6% over the year, and broad money rose by 1.9%, compared with 6.8% last year – the credit impulse is easing!

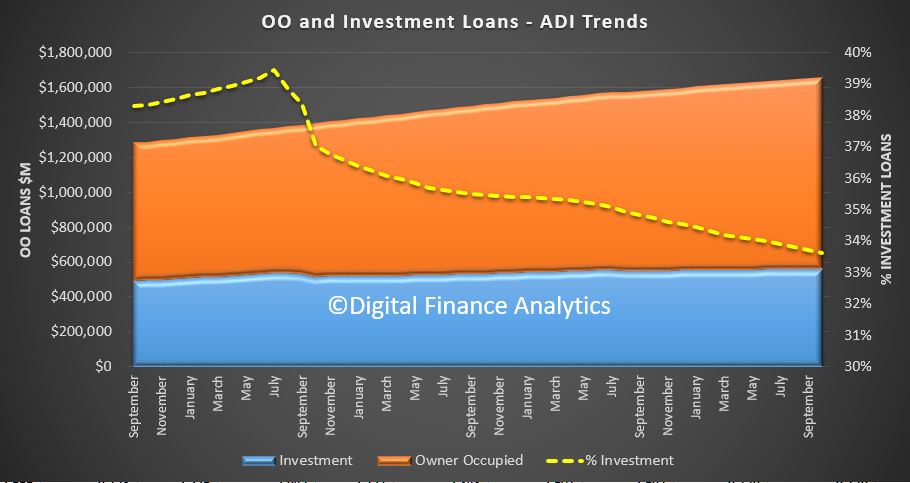

Total housing lending rose by 0.28% to $1.78 trillion. Within that owner occupied lending rose 0.42% or $5 billion to $1.2 trillion while investment lending rose by just 0.1% to $593.6 billion. Investment loans fell to 33% of all loans, down from 38.6% in 2015.

Business lending was 32.7% of all lending, lower than 2015.

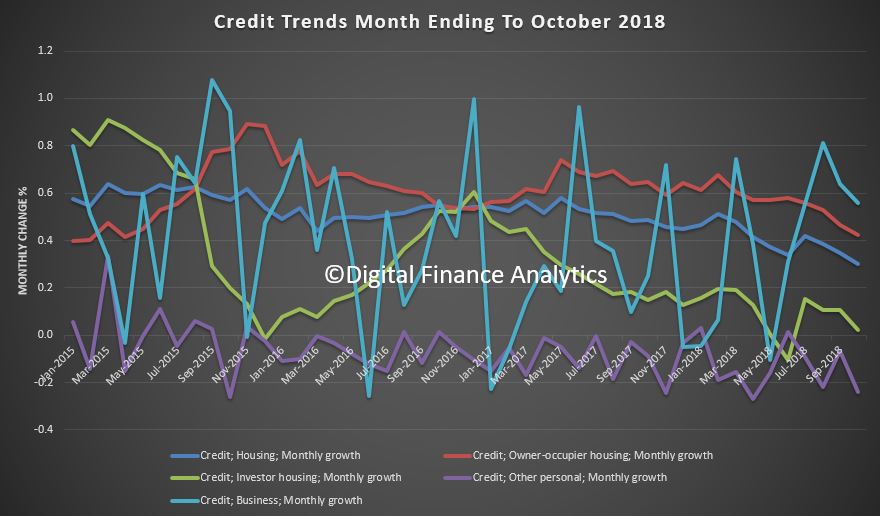

The monthly flows continue to show significant noise…

… but the annualised figures show the fall in housing lending across the board.

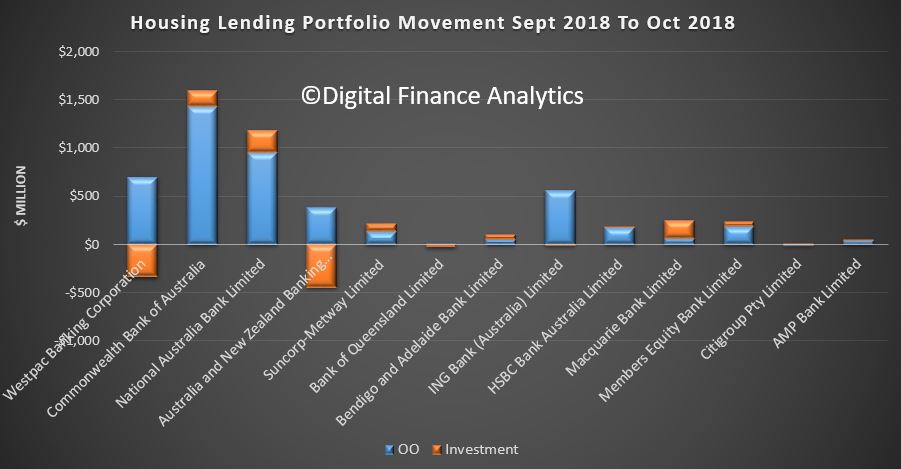

Turning to the APRA banking stats, we can look at individual lender portfolios. We see that Westpac and ANZ both reduced their investor loan portfolios between September and October, while NAB and CBA grew theirs.

Macquarie Bank is still growing its investor pools (well above the now obsolete APRA 10% speed limit).

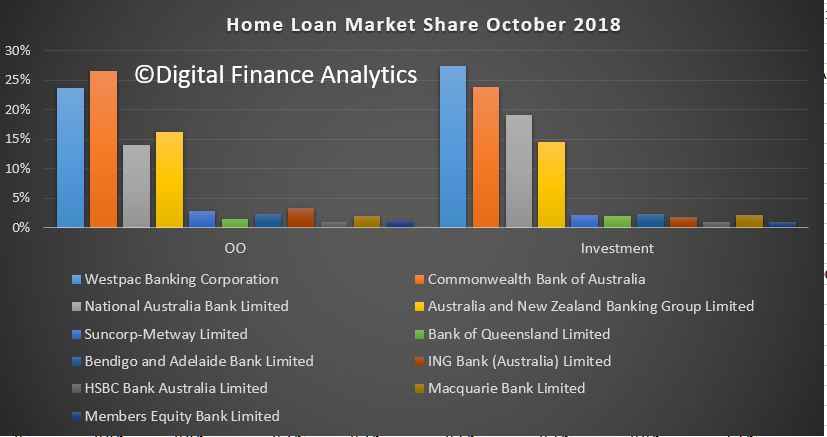

ADI portfolios hardly moved overall with CBA still the largest owner occupied lending, and Westpac the largest investment lender.

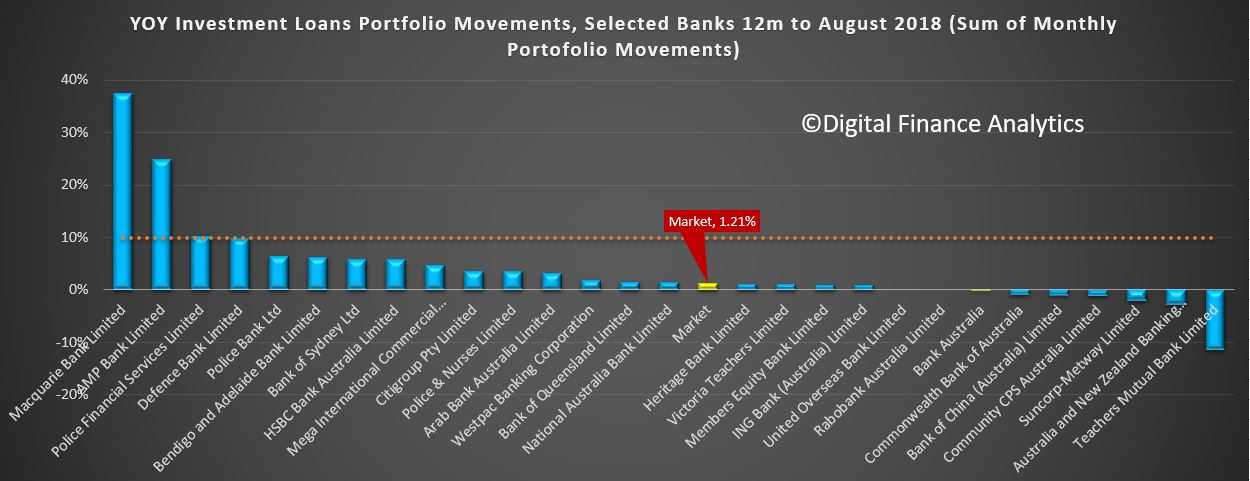

We can still plot the annualised movements of investor loans, and we see a small number of lenders well above the 10% speed limit (which was removed a few months ago). Significantly many lenders are well below that rate.

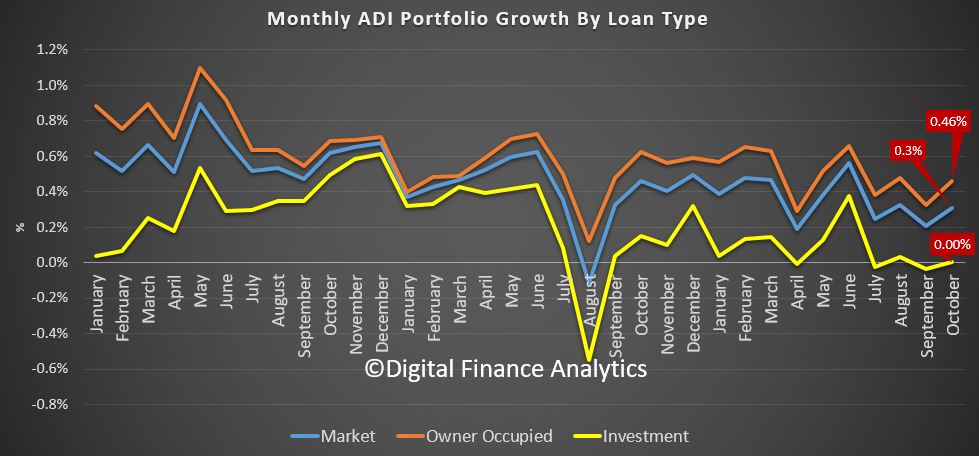

At an aggregate level, lending by ADIs was up 0.3% in the month, with investor loans flat, and owner occupied loans at 0.46%.

The proportion of investor loans fell again in stock terms to 33.6%.

Total ADI lending rose to $1.66 trillion, up 0.3% of $5 billion. Owner occupied loans rose 0.46% to $1.1 trillion and investor loans rose 0.004% to $557.4 billion.

In fact some smaller banks, and non-banks are growing their portfolio faster than the majors, thus the rotation across the sectors continues.

We expect credit to continue to grow more slowly ahead, and this will lead home prices lower.