Yet another inquiry has been announced into mortgage pricing as the ACCC is tasked to examine the banks failure to pass on in full official interest rate cuts engineered by the central bank. The ACCC’s preliminary report is due by 30 March next year, six months before the final report.

Beyond the crocodile tears, there are important questions here, because as we have highlighted, loyalty is not rewarded as the banks cut rates to attract new customers. In addition, deposit margin compression has reach a floor, and funding costs are under pressure. But nothing has fundamentally changed from recent ACCC and Productivity Commission reports. Yet, having another investigation takes pressure off The Treasurer, conveniently.

Via The Guardian. The treasurer, Josh Frydenberg, has asked the competition watchdog to examine why many mortgage holders are being charged rates well above the cash rate record low of 0.75%.

The higher rates have prompted allegations of price gouging by the banks – Commonwealth Bank,

Westpac, ANZ and National Australia Bank – which have previously cited

funding costs as a reason why not all reductions could be passed on.

“We need information about the cost of the funds of the banks and …

why they’re not passing on these rate cuts in full,” Frydenberg told

ABC television on Monday.

The inquiry, which will also include smaller institutions, comes

after an earlier royal commission into misconduct in the banking sector

uncovered predatory practices and dented market confidence.

But Frydenberg shrugged off suggestions that the new inquiry by the

Australian Competition and Consumer Commission would further affect

confidence in Australia’s banks.

“I actually did call the CEOs of the big four banks yesterday and

told them that this could actually help clear the air,” he said. “But at

the same time, you know, they’re defending their patch and will

continue to do.”

The treasurer said the banks need to explain how they balance the competing needs of shareholders and customers.

The official cash rate is at a record low of 0.75% after the Reserve

Bank of Australia cut interest rates three times this year. But the big

four banks on average passed on only 75% of the total reductions to

their customers.

“There are a number of smaller lenders that have actually wasted no

time in passing on these rate cuts on in full,” Frydenberg said.

“If the big four banks had passed on these 75 basis point rate cuts,

then somebody with a $400,000 mortgage would be more than $500 a year

better off in lower interest payments.”

The ACCC’s preliminary report is due by 30 March next year, six months before the final report.

The ACCC proposes to impose conditions on the Australian Banking

Association’s (ABA) Banking Code of Practice to ensure the revised Code

will benefit low-income consumers and drought-affected farmers.

The ABA, on behalf of its 23 members including the major banks, has

sought authorisation to amend its Banking Code in line with

recommendations of the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry (Hayne Royal Commission).

The proposed amendments aim to improve basic bank accounts and low or

no-fee accounts by prohibiting informal overdrafts unless requested by

the customer, and dishonour fees. The ABA is also proposing that certain

types of basic bank accounts have no minimum deposits, free direct

debit facilities, access to a debit card at no extra cost and free

unlimited domestic transactions.

In addition, the ABA’s changes would prevent default interest being charged on agricultural loans in drought-affected areas.

After considering the ABA’s proposal, the ACCC believes that additional conditions are required to strengthen these changes.

“The proposed changes to the Code should result in public benefits,

by giving customers on low incomes better access to affordable banking,

and to address a source of significant harm to farmers experiencing

drought,” ACCC Deputy Chair Delia Rickard said.

“While the ACCC strongly supports these objectives, we are proposing

to place extra conditions on ABA members to ensure the changes

effectively address the Royal Commission’s recommendations, and in turn

actually deliver these public benefits.”

For example, under the ABA’s proposal, basic bank accounts could

still be overdrawn without the customer’s agreement in some

circumstances, and banks could continue to charge interest, in some

cases at rates approaching 20 per cent, on overdrawn amounts.

“This could lead to low income customers getting into debt from

overdrafts they did not agree to, which is exactly the kind of problem

the Hayne Royal Commission sought to address,” Ms Rickard said.

The proposed conditions of authorisation would not allow interest to

be charged in these cases, or would require any such interest charges to

be repaid to the customer.

The ACCC also shares consumer groups’ concerns that the ABA’s

proposed changes would not require banks to proactively identify

existing customers who would be eligible for the accounts, or even to

continue to offer a basic bank account at all.

To address this, the ACCC’s proposed conditions would require banks

to proactively identify eligible customers, including through data

analysis; inform these customers of their eligibility, and for the ABA

to report to the ACCC on measures taken to offer them fee-free bank

accounts, and report how many customers have taken them up.

The ACCC will also require members of the ABA who currently offer a

basic banking product to continue to do so for the period of

authorisation.

Feedback is invited on these issues and the proposed conditions by 14

October 2019. The ACCC’s final determination is due in November 2019.

The draft determination and more information about the application for authorisation is available at The Australian Banking Association.

Australia’s customer owned

banking sector welcomes reports that the Australian Competition and Consumer

Commission (ACCC) is requesting to conduct an inquiry into the banking

industry’s competitiveness.

Customer Owned Banking Association CEO Michael Lawrence

says the request from the ACCC and the comments from Tim Wilson MP were

encouraging for credit unions, building societies and mutual banks who have

been leading the charge for a more competitive retail banking market.

“The enduring solution to concerns about the banking

market is action to promote competition.

“We don’t have sustainable banking competition at

the moment. A lack of competition can contribute to inappropriate conduct

by firms, and insufficient choice, limited access and poor-quality products for

consumers.

“We strongly support the ACCC’s calls for an

inquiry to examine the banking industry’s competitiveness. It’s encouraging to

see that the ACCC and Tim Wilson MP share our sector’s concerns about

competition and what an uncompetitive banking market means for consumers.

“Last year’s Productivity Commission’s report on

competition in banking sent strong messages to regulators and policymakers that

regulation is hurting competition and consumers are paying the price.

“The regulatory framework over time has

entrenched the dominant position of the largest banks.

“The PC report shone a light on a problem that is not

well enough recognised – that more and more regulation can be harmful to

consumers because it weakens competition.

“The Productivity Commission found that competition

drives innovation and overall value for customers.

“The Financial Services Royal Commission

looked into misconduct, now is the time to look into competition.”

Australian

consumers are paying too much for foreign currency conversion (FX)

services because of confusing pricing and a lack of robust competition, a

new ACCC report has found.

The final report of the ACCC’s Foreign Currency Conversion Services Inquiry

highlights important competition and consumer issues affecting

individuals and small businesses who use international money transfers

(IMTs), foreign cash, travel cards, and credit cards or debit cards for

transactions in foreign currencies.

The ACCC found that it can be challenging for consumers to shop

around and make informed decisions about FX services. As a result, many

consumers continue to use the big four banks for FX services despite the

availability of much cheaper alternatives.

It is difficult for consumers to compare prices because some

suppliers do not disclose their total price up front. In addition,

consumers pay unexpected fees for some services. Finally, complex prices

can deter consumers from shopping around because of the time and effort

required to do so.

During 2017-18, individual consumers who used the big four banks to

send IMTs in US dollars and British pounds could have collectively saved

about AUD150 million if they had instead used a lower priced IMT

supplier.

“Shopping around could save Australian consumers hundreds of millions of dollars each year,” ACCC Chair Rod Sims said.

“Consumers and small businesses tend to default to their usual bank

to send money overseas, but this may not be the cheapest option. This is

another example where consumers may end up paying more for their

loyalty.”

Guidance for consumers using FX services

The ACCC has released a guide to

help consumers shop around. For example, the guide gives tips on

sending money overseas and avoiding fees when making overseas purchases

online.

“The guide will help consumers to shop around, carefully select where

and how they pay for their purchases and to identify fees so they can

get the best deal,” Mr Sims said.

“For example, the guide explains how foreign exchange services with low or no fees are not always the best value for money.”

“We have also tried to clear up a few misconceptions, such as the

assumption that paying in Australian dollars when shopping overseas is

always best, when that is not the case.”

The final report warns that travellers can pay a high price for

leaving their purchase of foreign cash to the last minute and buying at

the airport.

Consumers should also consider whether their existing credit or debit

card may be cheaper than using foreign cash or a travel money card for

overseas purchases. Some credit and debit providers offer cards with no

international transaction fees which can be a much cheaper option than

many other products.

Consumers should be aware that some commercial comparison sites may

not be independent and that suppliers may pay for their services to be

promoted by these sites. There are, however, two government-funded

comparison websites for international money transfers (IMTs): www.sendmoneypacific.org and www.saverasia.com, which compare prices of IMT services available to a number of South-East Asian and Pacific Island countries.

Savings to be made

The ACCC inquiry found:

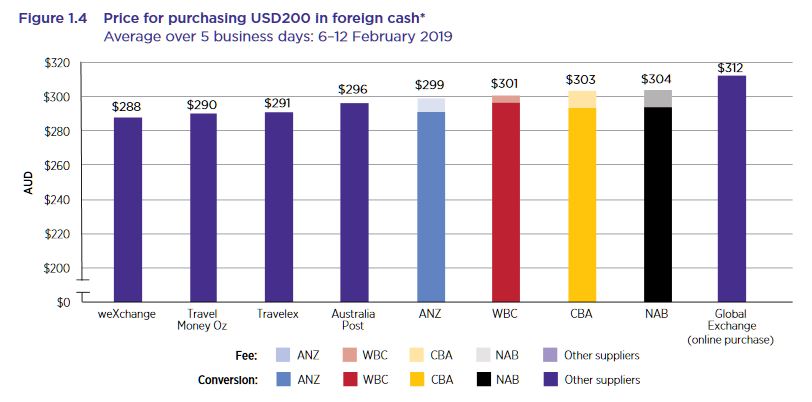

Foreign cash is more expensive at airport locations than at other

locations. When buying USD200 in February 2019, consumers could have

saved AUD40 by purchasing from the cheapest supplier at a non-airport

location, compared with the most expensive supplier at the airport.

Consumers and small businesses who used the most expensive bank to

transfer USD7000 would have paid more than AUD500 more than if they had

used the cheapest supplier.

If customers of the big four banks used a debit or credit card

without international transaction fees instead of a travel money card,

they could save up to AUD13 on a USD200 purchase.

Customers of the big four banks could save up to AUD5 on a USD200

purchase if they used a ‘regular’ debit or credit card instead of a

travel money card.

Guidance for businesses

The report includes best practice guidance for businesses supplying

FX services. It explains how they should disclose prices to consumers.

The guidance focuses on ensuring that businesses clearly disclose the

full price of an FX service to consumers upfront.

“We consider businesses who ignore this best practice guidance may be

at risk of breaching the Australian Consumer Law,” Mr Sims said.

“The ACCC will take action against businesses who do not make appropriate disclosures to consumers.”

New entrants providing lower prices, more advanced services

The ACCC has found that recent competition from newer entrants is

delivering better outcomes for consumers making use of IMTs, including

through lower prices and more advanced services.

These new entrants often rely on obtaining services from banks, their

vertically integrated competitors, to provide IMTs to their customers.

However, the inquiry found that some non-bank IMT suppliers had been

denied access to bank services, such as bank accounts.

“Banks need to comply with Australia’s anti-money laundering and

counter terrorism financing laws, and this is one reason banks have

given for withdrawing banking services to IMT providers,” Mr Sims said.

“The withdrawal of banking services from non-bank IMT suppliers

represents a significant threat to competition that could ultimately

result in less choice and higher prices for consumers.”

To address this issue, the ACCC recommends development of a scheme to

facilitate continued and efficient access to banking services by

non-bank IMT suppliers. This would include addressing the due diligence

requirements of the banks, including in relation to anti-money

laundering and counterterrorism financing requirements.

This scheme should be operational by the end of 2020.

Background

The inquiry was preceded by:

findings by the World Bank

in June 2018 that the cost of sending money overseas from Australia was

approximately 11 per cent higher than the G20 average, 13 per cent

higher than the UK and almost 40 per cent higher than the US

the Productivity Commission’s Report on Competition in the Australian Financial System

which recommended that the ACCC, in consultation with ASIC, investigate

what additional disclosure methods could be used to improve consumer

understanding and comparison of fees for foreign transactions.

On 2 October 2018,

the Treasurer approved the ACCC holding an inquiry into the supply of

FX services in Australia. On the same day, the ACCC released an issues

paper for the inquiry. In response, the ACCC received 63 written

submissions from a mix of consumers, FX services suppliers, small

businesses and other stakeholders.

The final report focuses its competition analysis primarily on IMTs. IMTs are significant for a number of reasons including:

prices in Australia are high by global standards and IMTs are a

significant outlay for Australians with an estimated AUD21 billion in

personal IMTs sent from Australia each year

IMTs are regularly used by groups of potentially vulnerable and disadvantaged consumers such as migrants and temporary workers

the average transaction size for IMTs is much larger than the other services considered in the inquiry.

The inquiry is the second inquiry undertaken by the ACCC’s Financial

Services Competition Branch (FSCB). The FSCB proactively monitors and

promotes competition in Australia’s financial services sector by

assessing competition issues and undertaking market studies.

The annual average retail petrol price in 2018–19 was the highest in

real terms (i.e. adjusted for inflation) in four years according to the

ACCC’s latest report on the Australian petroleum market for June quarter 2019.

The report shows that in the five largest cities, Sydney, Melbourne,

Brisbane, Adelaide and Perth, the average annual petrol price in 2018–19

was 141.2 cents per litre (cpl), nearly 7.0 cpl higher than last year.

In nominal terms (i.e. with prices not adjusted for inflation) it was

the highest annual average price in five years.

Annual average retail petrol prices in the five largest cities in nominal and real terms: 2000–01 to 2018–19

“The most significant contributor to this increase was the

depreciation over the year in the AUD-USD exchange rate, which decreased

by USD 0.06 to USD 0.72,” said ACCC Chair Rod Sims.

“This was the lowest annual average AUD-USD exchange rate in the last

15 years. The AUD–USD exchange rate is a significant determinant of

Australia’s retail petrol prices because international refined petrol is

bought and sold in US dollars in global markets.”

A significant development in the petrol industry in the first half of

2019 has been the change in price setter at both Coles Express, to Viva

Energy, and Woolworths, to EG Group, retail sites.

The report found that compared with market average prices, Coles

Express prices were lower in most capital cities after Viva Energy began

setting prices. However, they remained above the market average price

in all eight capital cities. At Woolworths, prices were higher in most

capital cities after EG Group took over the retail sites, although in

the majority of cities, prices were still below the market average

price.

“The ACCC will monitor prices at these retail sites very closely in future,” Mr Sims said.

Mr Sims said it was important for motorists to shop around for cheap

fuel by using the available fuel price websites and apps. For those

motorists in the five largest cities, they can also use information

about petrol price cycles on the ACCC website to time their purchases.

Retail petrol prices in the three smaller capital cities; Canberra,

Hobart and Darwin, are typically higher than prices in the five largest

cities. However, the report noted that, in the first half of 2019, there

were periods when prices in Darwin and Canberra were below prices in

the five largest cities.

Monthly average retail prices in Darwin were lower than in the five

largest cities between February and May 2019, and monthly average retail

prices in Canberra were lower than in the five largest cities in both

April and May 2019.

“This was the first time monthly average prices in Canberra were

below the average price in the five largest cities since April 2012,” Mr

Sims said. “The reduction in prices in the Darwin and Canberra is good

news for motorists in those locations.”

The lower prices in Canberra may have been influenced by the

possibility of greater regulation of the petroleum industry arising from

the current ACT Legislative Assembly petrol inquiry. The situation in

Canberra is similar to that in Darwin in 2015, when the decrease in

petrol prices coincided with increased local scrutiny of petrol prices

by the NT Government.

The report noted that in the June quarter 2019, average retail petrol

prices across the five largest cities were 145.3 cpl, an increase of

15.0 cpl from the March quarter 2019. The principal driver of the

increase was rising international crude oil and refined petrol prices in

the quarter. These continue to be influenced by the agreements made

since late-2016 by the Organisation of Petroleum Exporting Countries

(OPEC) cartel, and some other crude oil producing countries, including

Russia, to cut production.

Other petrol fast facts:

Brisbane petrol prices were higher than the other large Australian cities.

The city–country petrol price differential decreased in the quarter to 1.5 cpl.

Analysis of NSW’s Coffs Harbour petrol prices shows there are a range of prices available to motorists if they shop around.

Diesel and automotive LPG prices in the five largest cities both increased.

The ACCC says that Australians are set to lose a record amount to scams in 2019, with projections from losses reported to Scamwatch and other government agencies so far expected to exceed $532 million by the end of the year, surpassing half a billion dollars for the first time.

This year’s National Scams Awareness Week

(12-16 August) theme is “too smart to be scammed?” and the ACCC, along

with over 100 campaign partners from government and industry, is urging

consumers to test their scams knowledge and refresh their scam

protection and detection skills.

“Many people are confident they would never fall for a scam but often

it’s this sense of confidence that scammers target,” ACCC Deputy Chair

Delia Rickard said.

“People need to update their idea of what a scam is so that we are

less vulnerable. Scammers are professional businesses dedicated to

ripping us off. They have call centres with convincing scripts, staff

training programs, and corporate performance indicators their

‘employees’ need to meet.”

Investment scams are one of the most sophisticated and convincing

scams and continue to have the highest losses. Nearly half of all

investment scams reported this year resulted in a financial loss.

These scams are prominent on social media, with ‘Facebook lottery’

scams, the ‘Loom’ pyramid scheme, and cryptocurrency scams particularly

common.

Cryptocurrency investment scams have seen record losses, with reports

to the ACCC alone of $14.76 million between January and July 2019. Many

use social media platforms, fake celebrity endorsements or fake online

trading platforms that are made to look legitimate.

Protection advice

“Our advice is to be wary of ads you see on the internet. Don’t be

persuaded by celebrity endorsements or ‘not to be missed’ opportunities.

You never know for certain who you’re dealing with or whether they’re

credible,” Ms Rickard said.

“If you think you’re speaking to a friend on social media, call them,

or find another way to contact them before acting on any advice that

might result in you giving away your personal details or money.”

Scamwatch also suggests that people check ASIC’s list of companies you should not deal with.

If the company that contacted you is on the list – do not deal with

them, and even if they are not listed, continue researching and speak to

a financial advisor before investing.

Be vigilant on social media, when shopping online and when answering

the phone, and never give anyone who has contacted you out of the blue

your personal details, banking details or remote access to your

computer, no matter who they say they are. It’s best to assume scammers

are everywhere, waiting for you to let your guard down.

“Remember, anyone could fall victim and no one is ‘too smart to be

scammed’. Always ask yourself, ‘could this be a scam?’ and if you’re

ever in doubt, decline the contact or hang up the phone – it’s often the

safest option,” Ms Rickard said.

The ACCC has produced a series of videos with tips and tricks on how to spot a scam, and to test people’s awareness of scams. The full series is also available on YouTube.

Australians are losing more money to NBN scams, with reported losses in 2019 already higher than the total of last year’s losses, according to the ACCC.

Consumers lost an average of more than $110,000 each month between

January and May this year, compared with around $38,500 in monthly

average losses throughout 2018 – an increase of nearly 300 per cent.

“People aged over 65 are particularly vulnerable, making the most

reports and losing more than $330,000 this year. That’s more than 60 per

cent of the current losses,” ACCC Acting Chair Delia Rickard said.

“Scammers are increasingly using trusted brands like ‘NBN’ to trick

unsuspecting consumers into parting with their money or personal

information.”

Common types of NBN scams include:

Someone pretending to be from NBN Co or an internet provider calls a

victim and claims there is a problem with their phone or internet

connection, which requires remote access to fix. The scammer can then

install malware or steal valuable personal information, including

banking details.

Scammers pretending to be the NBN attempting to sell NBN services, often at a discount, or equipment to you over the phone.

Scammers may also call or visit people at their homes to sign them

up to the NBN, get them a better deal or test the speed of their

connection. They may ask people to provide personal details such as

their name, address, date of birth, and Medicare number or ask for

payment through gift cards.

Scammers calling you during a blackout offering you the ability to stay connected during a blackout for an extra fee.

It is important to remember NBN Co is a wholesale-only company and does not sell services directly to consumers.

“We will never make unsolicited calls or door knock to sell broadband

services to the public. People need to contact their preferred phone

and internet service provider to make the switch,” NBN Co Chief Security

Officer Darren Kane said.

“We will never request remote access to a resident’s computer and we

will never make unsolicited requests for payment or financial

information.”

“If someone claiming to work ‘for the NBN’ tries to sell you an

internet or phone service and you are unsure, ask for their details,

hang up, and call your service provider to check if they’re legitimate.

Do a Google search or check the phone book to get your service

provider’s number, don’t use contact details provided by the sales

person,” Ms Rickard said.

“Never give an unsolicited caller remote access to your computer, and

never give out your personal, credit card or online account details to

anyone you don’t know – in person or over the phone – unless you made

the contact.”

“It’s also important to know that NBN does not make automated calls

to tell you that you will be disconnected. If you get a call like this

just hang up.”

“If you think a scammer has gained access to your personal

information, such as bank account details, contact your financial

institution immediately.”

The ACCC has established a Financial Services Competition Branch, which it says will provide support for the Commonwealth Director of Public Prosecutions’ prosecution of ANZ, Citigroup, Deutsche Bank and six senior officers, via InvestorDaily.

The unit, enabled by an allocation from the government’s mid-year

budget, falls under the ACCC’s new Compliance and Enforcement Policy and

includes a permanent competition investigation team.

The competition regulator expects its team to complete a number of investigations that could result in court proceedings.

The announcement made by ACCC chair Rod Sims during his address to

the Committee for Economic Development Australia comes on the back of

AMP executives facing potential criminal charges, in a case against ASIC

over charging fees for no service.

“In commenting on regulators, the final report of the financial

services royal commission focused on issues that were of primary concern

to ASIC and APRA,” Mr Sims said.

“However, an underlying theme of the royal commission final report

was that competition is not vigorous among the major banks or in some

parts of the financial sector.”

The watchdog is also writing rules for the Consumer Data Right

system, known as ‘open banking’, which will determine how banks must

operate under the scheme.

The ACCC’s work will also focus on foreign exchange fees remaining high, Mr Sims added.

The ACCC said the finance competition investigation team will

complement a market studies unit that focuses on the financial sector,

which has been in place for a year.

The opaque, discretionary pricing of residential mortgages by banks makes it difficult and time consuming for borrowers to shop around and stifles price competition, a report by the ACCC has found.

The ACCC’s Residential Mortgage Price Inquiry monitored the prices

charged by the five banks affected by the government’s Major Bank Levy

between 9 May 2017 and 30 June 2018.

The ACCC’s final report

found the unnecessarily high search costs or effort required by

borrowers to find better prices reduces their willingness to shop

around, but that many borrowers who negotiate with their bank can get a

much better price.

“Pricing for mortgages is opaque and the big four banks have a lot of

discretion. The banks profit from this and it is against their

interests to make pricing transparent,” ACCC Chair Rod Sims said.

“Borrowers may not be aware they can negotiate with their lender on

price, both before and, particularly, after they have established their

mortgage.”

As at 30 June 2018, an existing borrower with an average-sized

mortgage could initially save up to $850 a year in interest if they

negotiated to pay the same interest rate as the average new borrower at

the five banks under review. For many borrowers the gain will be much

larger.

It appears that media attention on banks from the Banking Royal

Commission, the Productivity Commission’s Inquiry into competition in

the Australian financial system and the ACCC’s inquiry prompted some

borrowers to approach their lender for a better rate.

The ACCC reports that about 11 per cent of borrowers with variable

rate mortgages had the price of their current residential mortgage

reduced by one of the five banks under review in the year to 30 June

2018.

“I encourage more people to ask their lender whether they are getting

the lowest possible interest rates for their residential mortgage and,

as they do so, be ready to threaten to switch to another lender,” Mr

Sims said.

“I am afraid that the threat of switching banks will often be necessary to achieve a competitive mortgage rate.”

When directing the ACCC to conduct this inquiry, the Treasurer

requested the ACCC to report whether it found any evidence of the five

banks passing on the costs associated with the Major Bank Levy to

residential mortgage borrowers.

“The ACCC found no evidence that the five banks changed prices

specifically to recover the cost of the Major Bank Levy, whether in part

or in full, during the price monitoring period,” Mr Sims said.

The ACCC did find that measures announced by APRA in March 2017 to

limit new interest-only residential mortgage lending created an

opportunity for banks to synchronise increases to headline variable

interest rates for interest-only mortgages.

“We were not surprised banks seized the opportunity to increase

prices for interest-only loans. These price rises were enabled by the

oligopoly market structure in which the big four banks collectively have

a market share of about 80 per cent,” Mr Sims said.

ANZ was the first bank to announce increases to these interest-only

rates in June 2017. It did so safe in the knowledge that its move would

put the other banks at risk of breaching the APRA limits.

The other four banks, therefore, announced similar changes in the

same month. Together, the big four banks estimated revenue gains of over

$1.1 billion for their 2018 financial year, primarily as a result of

these rate increases.

“We consider that ANZ increased its rates, clear in its belief that,

given the APRA limits, the other big four banks would follow its lead,

and this expectation proved correct,” Mr Sims said.

The ACCC calculated that the rate increases by the five banks would

have added, in the first year, about $1300 in interest charged to the

average-sized owner-occupier interest-only standard variable mortgage.

“Such is the oligopolistic nature of banking that the banks all took

the opportunity to increase rates on both new and existing interest-only

mortgages, despite APRA’s measures only applying to new lending,” Mr

Sims said.

The ACCC also compared the approach to pricing of a sample of seven

banks that were not subject to the Inquiry. Three of these banks were

particularly focussed on competing on price, and therefore have lower

rates. Some of the banks in our sample rely heavily on brokers and

aggregators to gain market share. The ACCC notes that these banks, and

other lenders in a similar position, are likely to be more vulnerable to

future regulatory changes that affect the use of brokers as a

distribution channel.

In this report the ACCC notes that the new Consumer Data Right will,

among other things make it much easier for consumers to compare

available interest rates.

“The ACCC looks, in particular, to the Consumer Data Right to empower consumers in their dealings with banks,” Mr Sims said.

On 9 May 2017 the Treasurer, the Hon. Scott Morrison MP, issued a

direction to the ACCC to inquire into prices charged or proposed to be

charged by Authorised Deposit-taking Institutions affected by the Major

Bank Levy in relation to the provision of residential mortgage products

in the banking industry in Australia. The Major Bank Levy came into

effect from 1 July 2017.

The five banks affected by the levy are Australia and New Zealand

Banking Group Limited (ANZ), Commonwealth Bank of Australia, Macquarie

Bank Limited, National Australia Bank Limited, and Westpac Banking

Corporation.

The ACCC used its compulsory information gathering powers to obtain

documents and data from the five banks on their pricing of residential

mortgage products. The ACCC supplemented its analysis of the documents

and data supplied by the five banks with data from the Reserve Bank of

Australia (RBA), Australian Prudential Regulation Authority (APRA) and

the Australian Bureau of Statistics (ABS).

This Inquiry was the first task of the ACCC’s Financial Services Unit

(FSU), which was formed as a permanent unit during 2017 following a

commitment of continuing funding by the Australian Government in the

2017-18 Budget. Alongside the ACCC’s role in promoting competition in

financial services through its enforcement, infrastructure regulation,

open banking, and mergers and adjudication work, the FSU will monitor

and promote competition in Australia’s financial services sector by

assessing competition issues, undertaking market studies, and reporting

regularly on emerging issues and trends in the sector.

The FSU is currently examining the pricing of foreign currency

conversion services in Australia to evaluate whether there are

impediments to effective price competition in the sector. An inquiry

report is to be delivered to the Treasurer by 31 May 2019.

Blog")