Suncorp provided their quarterly statutory update today, as at 30

September 2016. Once again we see the pressure on regional players. Some relief may emerge when they move formally to advanced accreditation with APRA. Risks include a rise in bad debts, and the possibility of higher insurance claims though the summer storm period.

Suncorp’s lending assets remained broadly flat over the quarter at $54.1 billion, as the Bank actively managed volume and margin in a price driven market. Home lending was down 0.7% in the quarter, whilst business lending rose 1.5%. They have a 66% deposit to loan ratio.

Credit quality remained strong with gross non-performing loans decreasing 4.8% over the quarter to $581 million. Impairment losses of $10 million for the quarter represent an annualised 7 basis points of gross loans and advances, below the Bank’s 10 to 20 basis points expected operating range.

Gross impaired assets increased by $14 million to $220 million during the quarter, representing 0.41% of gross loans and advances. Whilst there is evidence the slowdown in the resource sector has had downstream impacts in some regional centres in Queensland, the impact is limited to a small number of exposures. The increase in the September quarter was driven by one mid-sized Commercial/SME loan with an indirect exposure to the downturn in the Queensland resources sector.

Gross impaired assets increased by $14 million to $220 million during the quarter, representing 0.41% of gross loans and advances. Whilst there is evidence the slowdown in the resource sector has had downstream impacts in some regional centres in Queensland, the impact is limited to a small number of exposures. The increase in the September quarter was driven by one mid-sized Commercial/SME loan with an indirect exposure to the downturn in the Queensland resources sector.

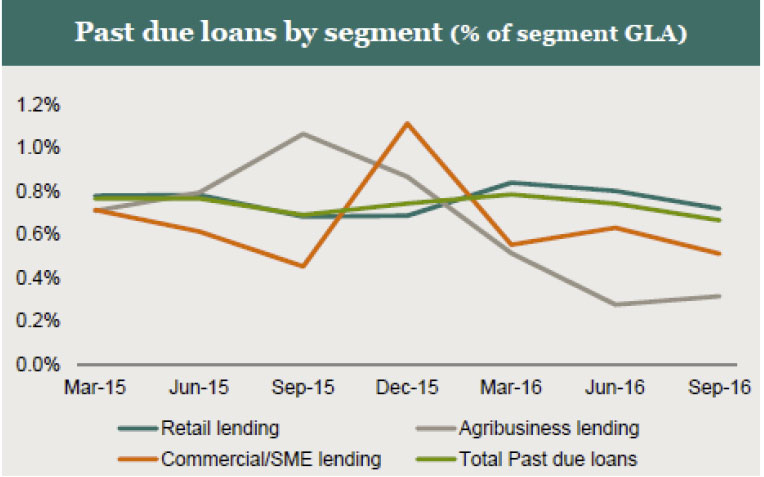

The balance of past due loans that are not impaired decreased by 10.6% to $361 million as at 30 September 2016. Retail past due loans decreased by $39 million to $319 million over the quarter. The favourable movement follows the embedding of enhancements to the collections system and processes that were disclosed with previous financial results.

The balance of past due loans that are not impaired decreased by 10.6% to $361 million as at 30 September 2016. Retail past due loans decreased by $39 million to $319 million over the quarter. The favourable movement follows the embedding of enhancements to the collections system and processes that were disclosed with previous financial results.

Suncorp Banking & Wealth CEO David Carter said the Bank remained committed to driving sustainable growth, while prudently managing risk, liquidity and the funding mix. The Net Stable Funding Ratio (NSFR) was 111% at 30 September.

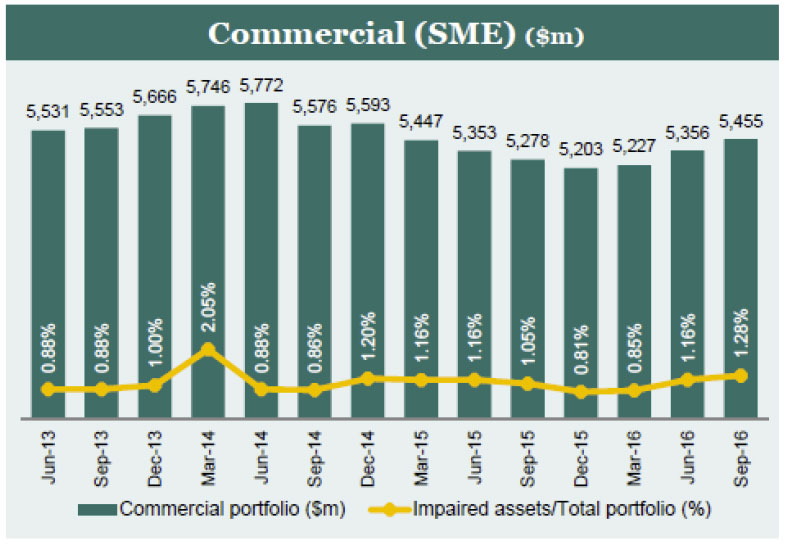

Modest growth in business lending continued during the quarter, with the commercial portfolio increasing 1.8% to $5.5 billion and agribusiness growing 1.1% to $4.4 billion. They are $480m in development finance across units, townhouses and other residential.

The home lending portfolio contracted marginally to $43.9 billion, as the Bank remained focused on sustainable and profitable lending. Since last year it has grown at 2.3%, well below the ~6.5% system rate. The quality of the lending portfolio remained favourable across a range of measures including quantitative serviceability parameters, credit quality and loan to value ratio (LVR), with 80% of new loans having a LVR of 80% or less.

Consistent with others in the market the Bank saw a sharp increase in term deposit funding costs following the May RBA rate cut. Whilst some of that pressure has recently abated, average funding costs will be higher than originally expected this half.

Consistent with others in the market the Bank saw a sharp increase in term deposit funding costs following the May RBA rate cut. Whilst some of that pressure has recently abated, average funding costs will be higher than originally expected this half.

The capital position of the Bank is robust with a Common Equity Tier 1 (CET1) ratio of 8.92% as at 30 September 2016, at the upper end of the 8.5% to 9% target.

They continue discussions with APRA towards achieving Advanced Accreditation. Meantime, they are operating as an Advanced Bank, with strong risk management and advanced models in use across the business.