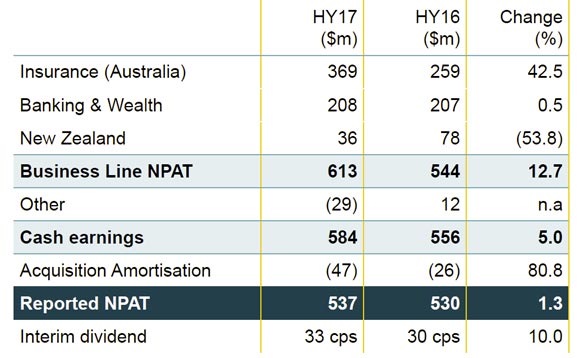

Suncorp today reported net profit after tax (NPAT) of $537 million (HY16: $530 million) for the six months to 31 December 2016. Profit after tax from business lines increased 12.7% to $613 million (HY16: $544 million).

The Group has been working hard to get performance up, and despite pressure on banking margins, and adverse insurance claims from New Zealand, management of the insurance businesses is clearly tighter.

The result included natural hazard claims costs of $350 million (HY16: $362 million), Investment earnings of $79 million (HY16: $133 million), reserve releases of $131 million (HY16: $137 million) and a loss on sale of Autosure of $25 million.

After accounting for the interim dividend, the Suncorp Group’s Common Equity Tier 1 (CET1) is $448 million above the operating targets.

The General Insurance CET1 is 1.23 times the Prescribed Capital Amount and Bank CET1 is 9.20%. The Group has $230 million of franking credits available after the payment of the interim dividend.

The General Insurance CET1 is 1.23 times the Prescribed Capital Amount and Bank CET1 is 9.20%. The Group has $230 million of franking credits available after the payment of the interim dividend.

Shareholders will receive an interim dividend of 33 cents per share fully franked (HY16: 30 cents) representing a payout ratio of 72% of cash earnings.

Insurance (Australia)

Insurance (Australia) NPAT increased 42.5% to $369 million due to top line growth, lower claims costs and disciplined expense management.

Gross Written Premium (GWP) growth of 6.2% was primarily driven by the CTP portfolio. Consumer Insurance benefited from industry stabilisation with Home and Motor GWP increasing 2.4% and 1.6% respectively.The Commercial Insurance market continues to be highly competitive with GWP growth of 0.4% reflecting a prudent approach to pricing and risk selection.

CTP GWP increased 27.3% due to Suncorp’s successful entry into the South Australian market and growth in New South Wales which was supported by improving claims metrics. Insurance (Australia) reserve releases of $149 million reflect the benign inflationary environment and Suncorp’s management of long-tail claims.

Banking & Wealth

The Banking & Wealth business delivered NPAT of $208 million reflecting improved operating expenses and strong credit quality. In response to some unsustainable competitor pricing, the Bank focused on profitable growth through the optimisation of price and volume.

Lending grew 2.5% over the past 12 months.

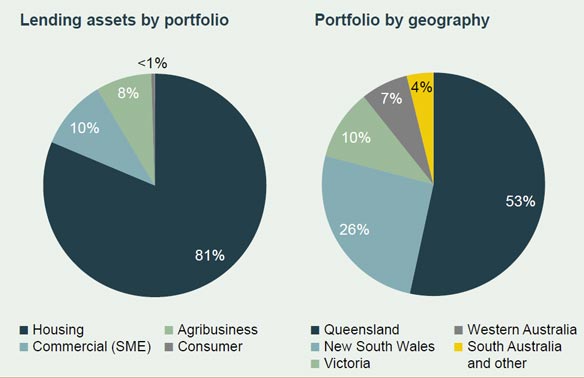

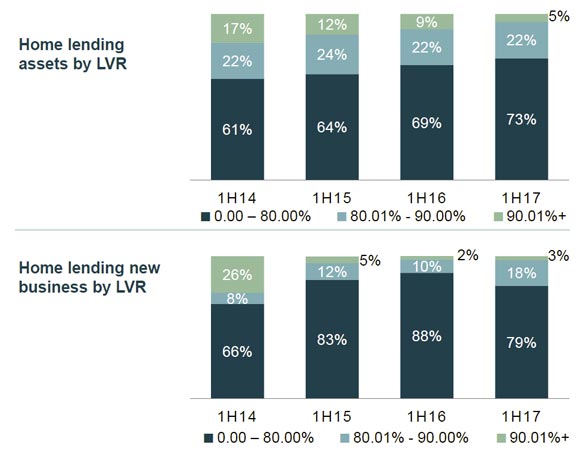

Total assets were $54.2 billion, of which home lending was $44.1 billion, half of which is in QLD. 65% of business came through intermediaries. High LVR loans are down significantly. Overall home lending grew below system. Deposit to loan ratio was 67.2% up a little on a year ago. During the half, the Bank funding mix changed with a 5.5% reduction in retail term deposits and an increase of 6.7% in at call deposits primarily driven by growth in personal transaction accounts.

Total assets were $54.2 billion, of which home lending was $44.1 billion, half of which is in QLD. 65% of business came through intermediaries. High LVR loans are down significantly. Overall home lending grew below system. Deposit to loan ratio was 67.2% up a little on a year ago. During the half, the Bank funding mix changed with a 5.5% reduction in retail term deposits and an increase of 6.7% in at call deposits primarily driven by growth in personal transaction accounts.

Following a targeted campaign in December, the housing loan portfolio is expected to grow in the second half.

Following a targeted campaign in December, the housing loan portfolio is expected to grow in the second half.

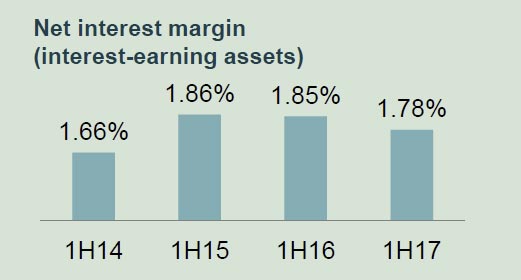

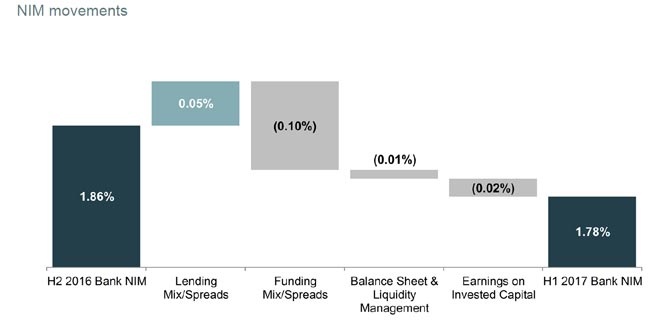

The net interest margin (NIM) of 1.78% was impacted by the lower cash rate and aggressive competition, however it remains within the target range of 1.75% to 1.85%.

Operating expenses improved by 5.8% resulting in a reduction in the cost to income ratio from 53.0% to 51.4%.

Operating expenses improved by 5.8% resulting in a reduction in the cost to income ratio from 53.0% to 51.4%.

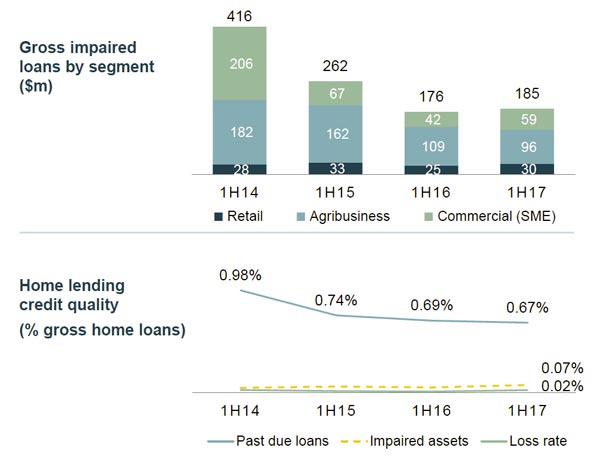

Gross non-performing loans improved by 14.3% over the past six months resulting in impairment losses of $1 million (less than 1bps), well below the target range of 10bps to 20bps of gross loans and advances.

The Bank has a tiered management limit structure for the LCR to ensure that an adequate buffer to the APRA prudential limit of 100% is held. The LCR is managed to market conditions and has been maintained comfortably above the prudential minimum since being introduced in January 2015. The average LCR for the half ending 31 December 2016 was 133%, ending the half at 130%.

The Bank has a tiered management limit structure for the LCR to ensure that an adequate buffer to the APRA prudential limit of 100% is held. The LCR is managed to market conditions and has been maintained comfortably above the prudential minimum since being introduced in January 2015. The average LCR for the half ending 31 December 2016 was 133%, ending the half at 130%.

The Bank is well placed to meet the proposed NSFR requirements, which will be introduced from January 2018. The Bank’s estimated NSFR at the end of the period was 106%.

Discussions continue with the APRA as part of progressing towards Advanced Accreditation. In parallel the Bank has undertaken changes to its processes and retail credit models as part of an industry wide alignment of the treatment of hardship. The Bank expects these changes to have some effect on reporting but no material impact to the risk or loss experience.

New Zealand

New Zealand NPAT of NZ$37 million was impacted by the Kaikoura earthquake and aftershocks (NZ$23 million) and new ‘over-cap’ claims from the 2010/11 Canterbury earthquakes (NZ$18 million) being notified by the Earthquake Commission (EQC).

Net incurred claims (NIC) were $372 million, up 22.8%, driven by the Kaikoura earthquake as well as several large commercial claims and strong unit growth in the consumer portfolios.

GWP growth of 4.8% was delivered primarily from the Home and Motor portfolios.

Included in the result was the New Zealand Life Insurance NPAT of NZ$18 million reflecting a 41.2% increase in underlying profits, and positive claims and lapse experience of NZ$5 million.