ASIC has released a report today on its first survey of various participants in the marketplace lending industry.

Marketplace lending allows investors to invest in loans to consumers and small and medium enterprises (SMEs). It has the potential to provide another avenue of funding for business and consumers.

ASIC conducted the survey on a voluntary basis between November and December 2016 and focused on marketplace lending providers’ business models and activities for the financial year ended 30 June 2016.

Here are the main findings:

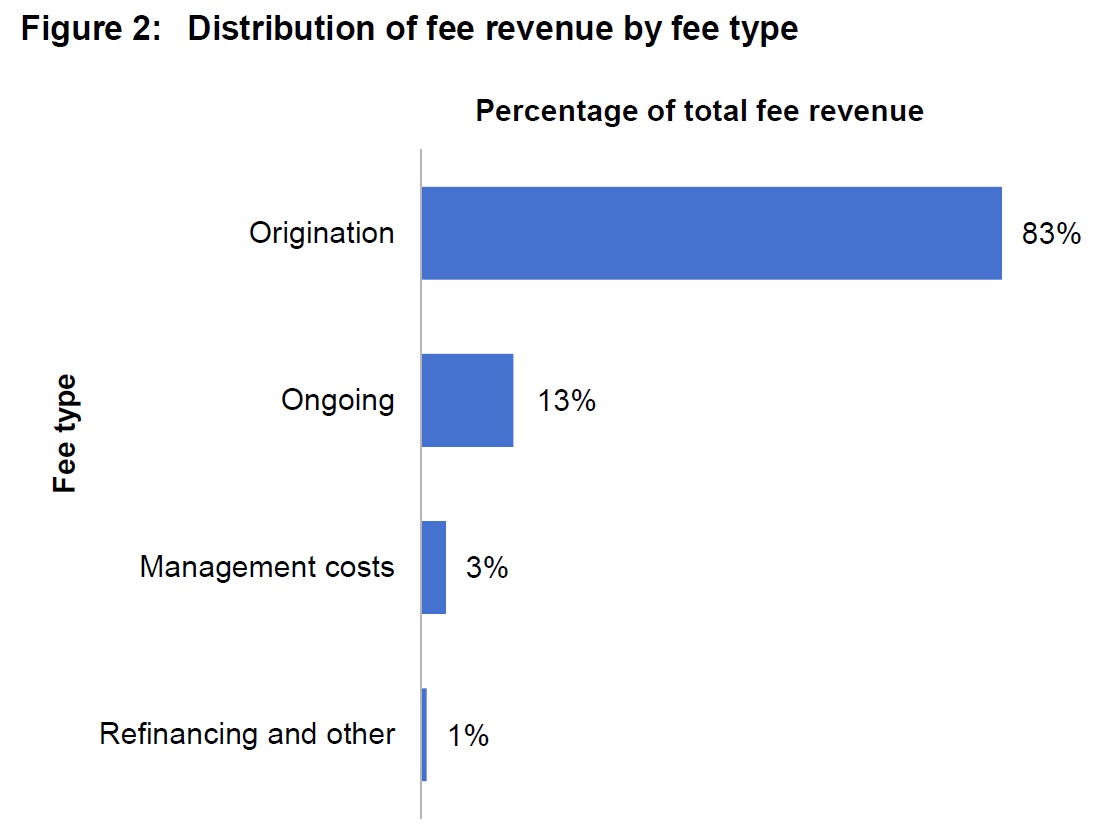

Loan origination fees accounted for approximately 83% of total fee revenue and the remainder of the revenue was almost exclusively generated from investors. The high proportion of origination fees may be partly explained by the fact that most providers have not been operating for a long period of time—any fees collected through interest payments may not be fully realised until future years.

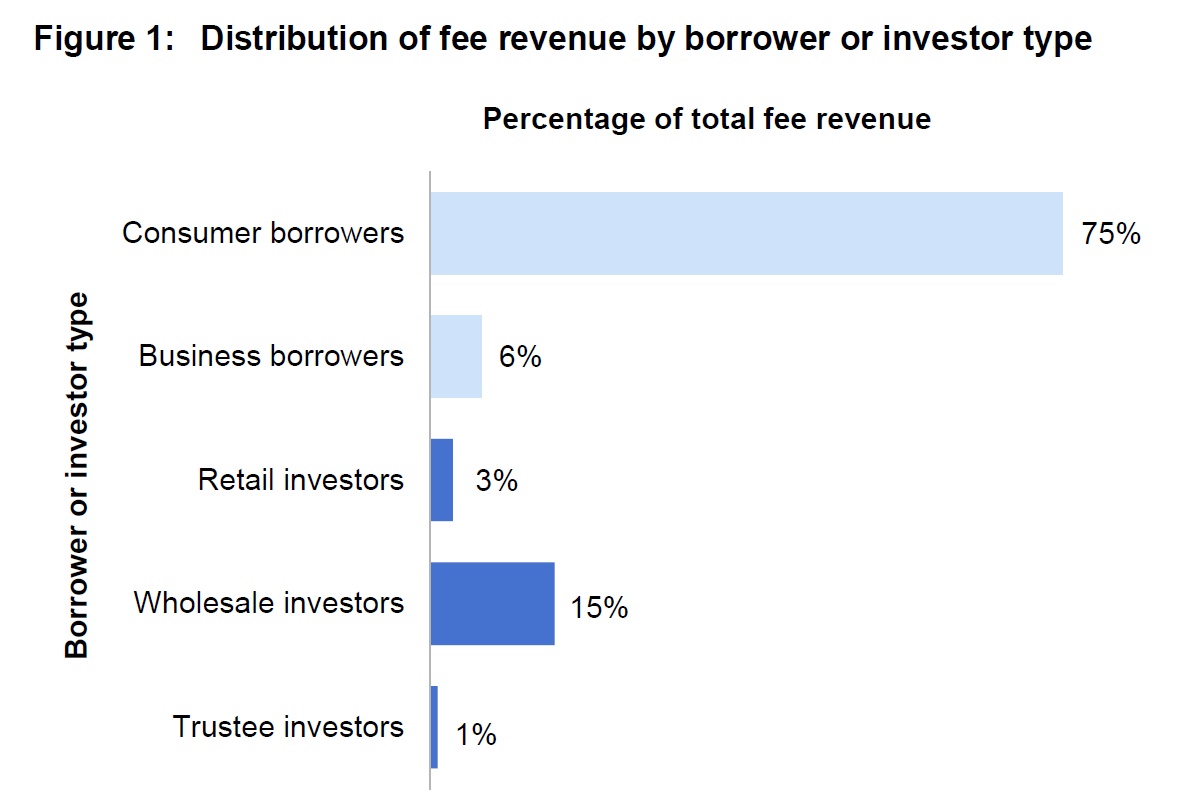

Respondents promoted their product to a range of different borrowers, which fell broadly under the category of consumers (i.e. individuals) or non-consumer/business borrowers, such as SMEs, self-managed superannuation funds (SMSFs) and agribusiness.

Respondents promoted their product to a range of different borrowers, which fell broadly under the category of consumers (i.e. individuals) or non-consumer/business borrowers, such as SMEs, self-managed superannuation funds (SMSFs) and agribusiness.

As at June 2016, the eight entities who responded to the second part of the survey reported a total of 7,448 borrowers, consisting of 7,415 consumer borrowers and 33 business borrowers.

As at June 2016, the eight entities who responded to the second part of the survey reported a total of 7,448 borrowers, consisting of 7,415 consumer borrowers and 33 business borrowers.

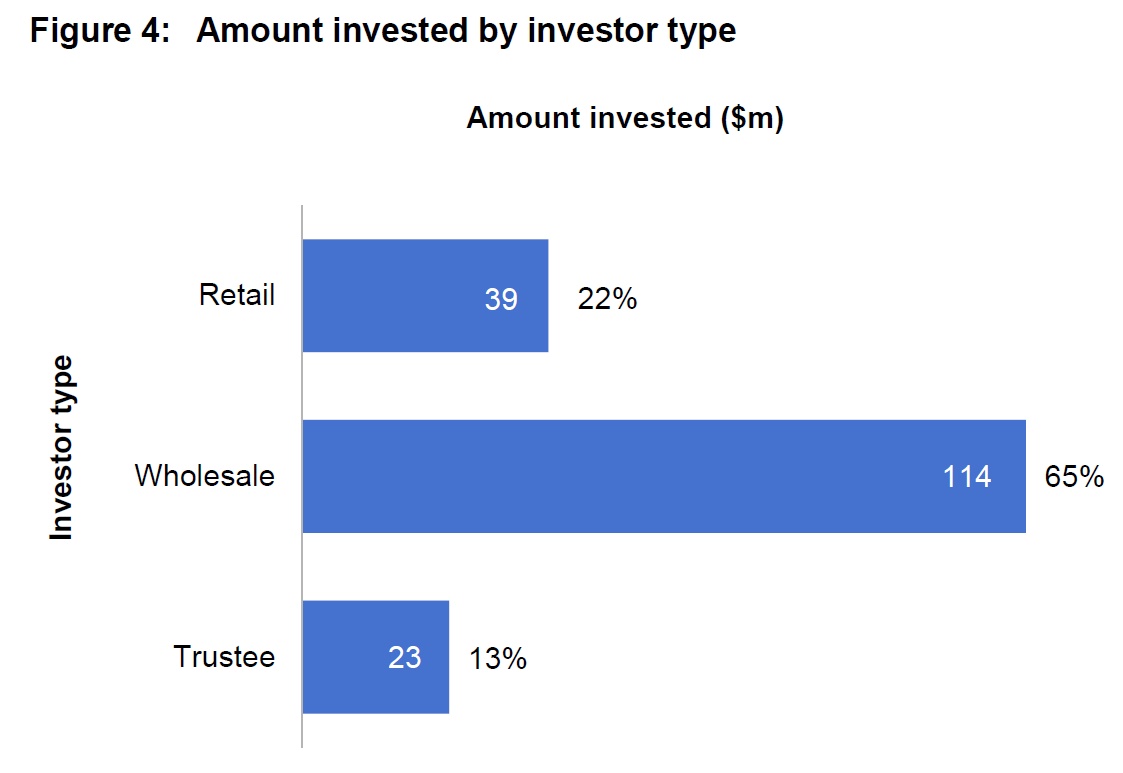

The survey results indicate that the industry is predominantly comprised of investors that are wholesale clients. However, some respondents that are currently wholesale-only providers have indicated that they intend to broaden their marketplace lending product offering to retail client investors in the future. The fact that many providers operate registered schemes seems to suggest that they may have plans to, or may wish to have the option available to, offer their marketplace lending product to retail client investors in the future.

The survey results indicate that the industry is predominantly comprised of investors that are wholesale clients. However, some respondents that are currently wholesale-only providers have indicated that they intend to broaden their marketplace lending product offering to retail client investors in the future. The fact that many providers operate registered schemes seems to suggest that they may have plans to, or may wish to have the option available to, offer their marketplace lending product to retail client investors in the future.

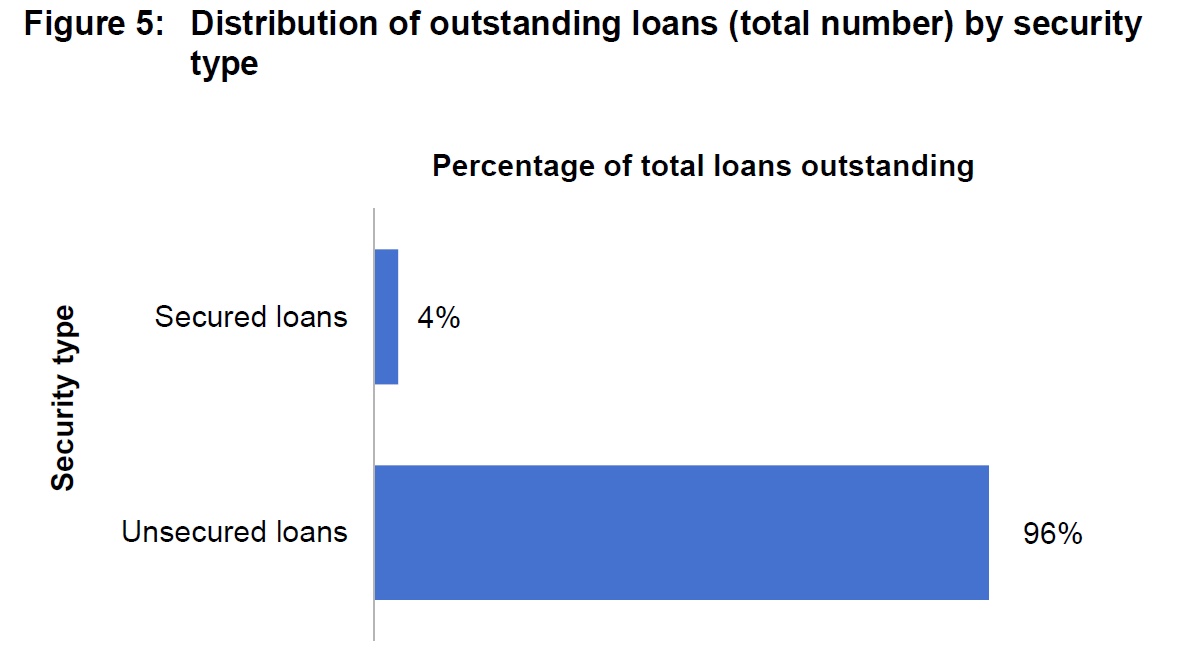

Loans available on marketplace lending platforms may either be secured or unsecured. Two respondents provide loans on an unsecured basis only, while one respondent indicated that all its loans are secured (such as by way of a charge against all the borrowers’ assets or by registered first mortgage). The remaining respondents indicated their loans may either be secured or unsecured. The security is held for the benefit of the investors.

Loans available on marketplace lending platforms may either be secured or unsecured. Two respondents provide loans on an unsecured basis only, while one respondent indicated that all its loans are secured (such as by way of a charge against all the borrowers’ assets or by registered first mortgage). The remaining respondents indicated their loans may either be secured or unsecured. The security is held for the benefit of the investors.

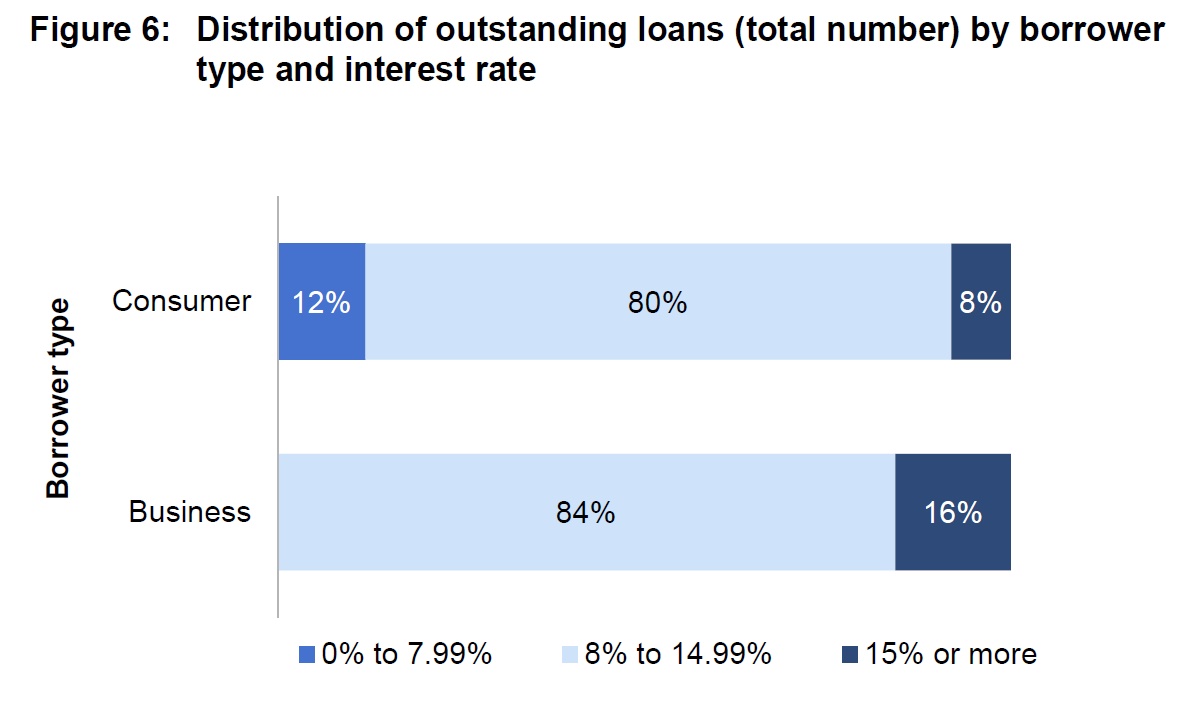

In most cases, requests for loans are assessed and assigned a risk grade and interest rate before they are made available for viewing and selection by investors. Most respondents indicated that interest rates are generally set by the provider and investors do not determine or influence the rate. Investors may choose the loans they wish to invest in based on the interest rate and/or risk grade allocated to the loan.

In most cases, requests for loans are assessed and assigned a risk grade and interest rate before they are made available for viewing and selection by investors. Most respondents indicated that interest rates are generally set by the provider and investors do not determine or influence the rate. Investors may choose the loans they wish to invest in based on the interest rate and/or risk grade allocated to the loan.

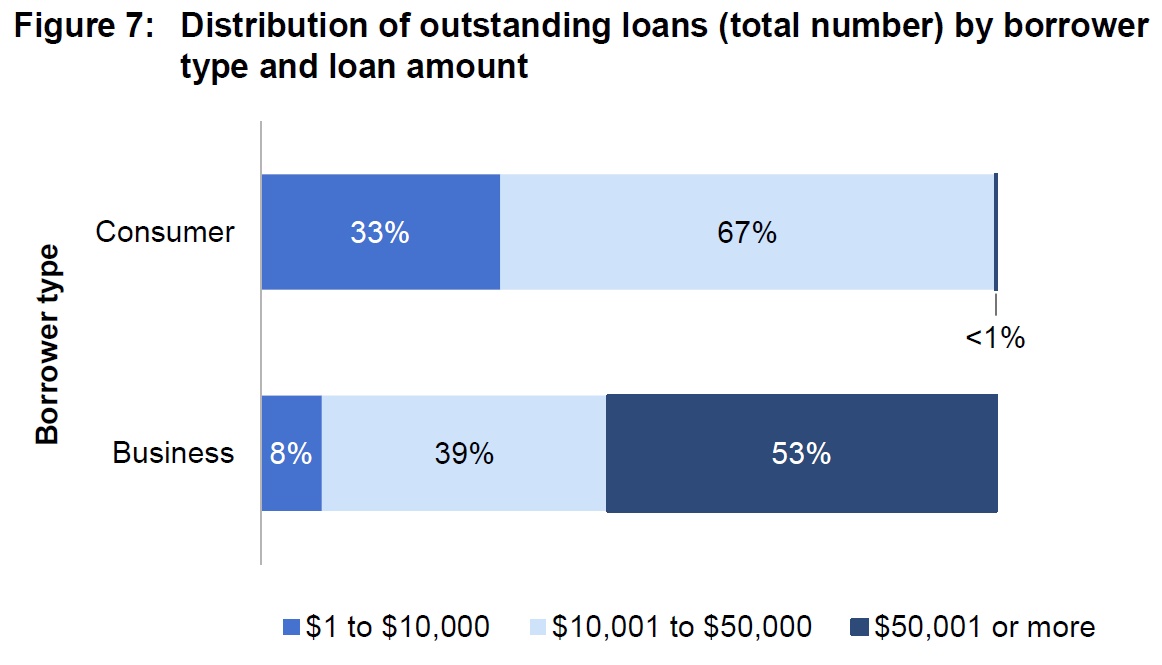

Loan amounts offered to consumer borrowers typically range from $5,000 to $80,000, while for business and other non-consumer borrowers, the amounts range from $2,001 to $3,000,000. None of the respondents provide small amount credit contracts or ‘payday loans’.

Loan amounts offered to consumer borrowers typically range from $5,000 to $80,000, while for business and other non-consumer borrowers, the amounts range from $2,001 to $3,000,000. None of the respondents provide small amount credit contracts or ‘payday loans’.

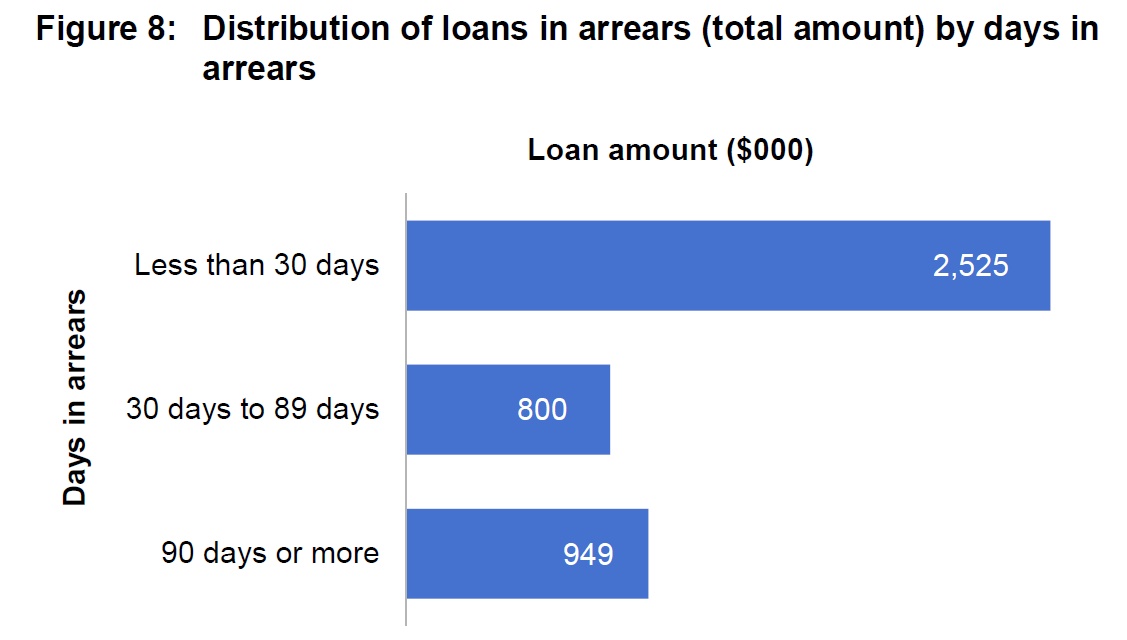

Most respondents indicated that they provide a grace period for borrowers in the event of missed or late repayments. All respondents indicated that reminders and direct engagement with the borrower are undertaken by the platform provider and that a repayment arrangement may be agreed with the borrower. Referrals to external collections agencies would be made if the loan remained delinquent. In one case, it was noted that recovery action would require the consent of the lenders for the particular loan. One respondent noted that problem SME loans require a more tailored process compared to consumer loans. Most respondents indicated they do not stress test their loan book, largely due to the relative newness or small size of current loan books which would not produce any meaningful assessment. However, two respondents do undertake some testing.

Most respondents indicated that they provide a grace period for borrowers in the event of missed or late repayments. All respondents indicated that reminders and direct engagement with the borrower are undertaken by the platform provider and that a repayment arrangement may be agreed with the borrower. Referrals to external collections agencies would be made if the loan remained delinquent. In one case, it was noted that recovery action would require the consent of the lenders for the particular loan. One respondent noted that problem SME loans require a more tailored process compared to consumer loans. Most respondents indicated they do not stress test their loan book, largely due to the relative newness or small size of current loan books which would not produce any meaningful assessment. However, two respondents do undertake some testing.

Commissioner John Price said, ‘As a relatively new industry, it is important for ASIC to engage with and better understand the business models of marketplace lending providers.

‘The survey responses have provided valuable insights into these businesses. We acknowledge and appreciate the participation of survey respondents’, he said.

Report 526 Survey of marketplace lending operators (REP 526) summarises ASIC’s findings from the 2016 Marketplace Lending Industry Survey and outlines ASIC’s role and recent activities in regulating the sector.

The responses to the survey showed that during the 2016 financial year, $156 million in loans were written to consumers and SMEs. Respondents reported a total of 3,201 investors and 7,448 borrowers as at 30 June 2016. Provider revenue was predominately tied to loan origination, and respondents were aware of the conflicts that arose as a result. The number of complaints received by providers was generally low at this stage.

Since the commencement of ASIC’s Innovation Hub in March 2015, ASIC has engaged with 34 marketplace lending providers to assist them to better understand the requirements under Australia’s regulatory framework. This has included specific regulatory guidance and examples of good practice.

ASIC has also granted waivers of some obligations under the law to facilitate six marketplace lending business operations, while maintainingappropriate investor protections.

ASIC will continue to monitor developments in the marketplace lending sector. ASIC is keen to assist marketplace lending providers and engage with new fintech businesses and industry organisations through its Innovation Hub.

Background

In Australia, there is no bespoke regulatory regime for marketplace lending. The regulations that apply to marketplace lending depend on how the business is structured, what financial services and products are being offered and the types of investors and borrowers involved.

In most cases, ASIC has identified that the provision of marketplace lending products involves the operation of a managed investment scheme, which would require the marketplace lending provider to hold an Australian financial services licence. Where the loans made through the platform are consumer loans (i.e. loans to individuals for domestic, personal or household purposes), an Australian credit licence is alsorequired.