The Commonwealth Bank (“the Group”) today advised that its unaudited cash earnings for the three months ended 30 September 2016 (“the quarter”) were approximately $2.4 billion. Statutory net profit on an unaudited basis for the same period was also approximately $2.4 billion, with non-cash items treated on a consistent basis to prior periods.

Our take is the CBA ship is running hard under sail, but the seas are far from calm, with funding costs rising, and more capital required to support the mortgage book.

Key outcomes for the quarter are summarised below:

Business Performance:

- Operating income growth was slightly below that of FY16, impacted by the low interest rate environment, a strengthening Australian Dollar (AUD) and higher insurance claims. Banking income growth was solid, supported by strong trading income. Group Net Interest Margin was lower in the quarter due to higher funding costs;

- Expenses were well managed in a lower growth environment, resulting in positive “jaws” in the quarter, notwithstanding ongoing investment in the business;

- Across key markets, volume growth remained either broadly in line with, or ahead of system in home lending, domestic business lending and household deposits. In Wealth Management, Average Assets Under Management (AUM) and Funds Under Administration (FUA) rose by 3 per cent and 2 per cent respectively driven by stronger investment markets and positive net flows. ASB customer advances continued to grow above market in the quarter.

Credit Quality:

- The credit quality of the Group’s lending portfolios remained sound, with consumer arrears decreasing in line with seasonal expectations;

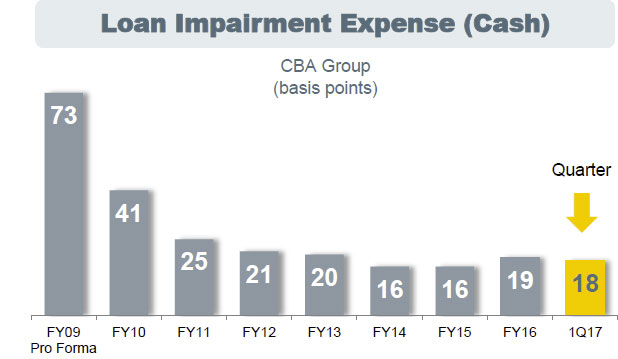

- Loan Impairment Expense (LIE) was $322 million in the quarter, equating to 18 basis points of Gross Loans and Acceptances, compared to 19 basis points in FY16.

- Consumer LIE was higher in the quarter, primarily driven by continued stress in areas of WA and QLD impacted by the mining downturn. Group Troublesome and Impaired Assets were slightly higher at $6.8 billion reflecting ongoing stress in the New Zealand Dairy sector;

Prudent levels of provisioning were maintained, with Total Provisions at $3.8 billion.

Capital, Funding and Liquidity:

Capital, Funding and Liquidity:

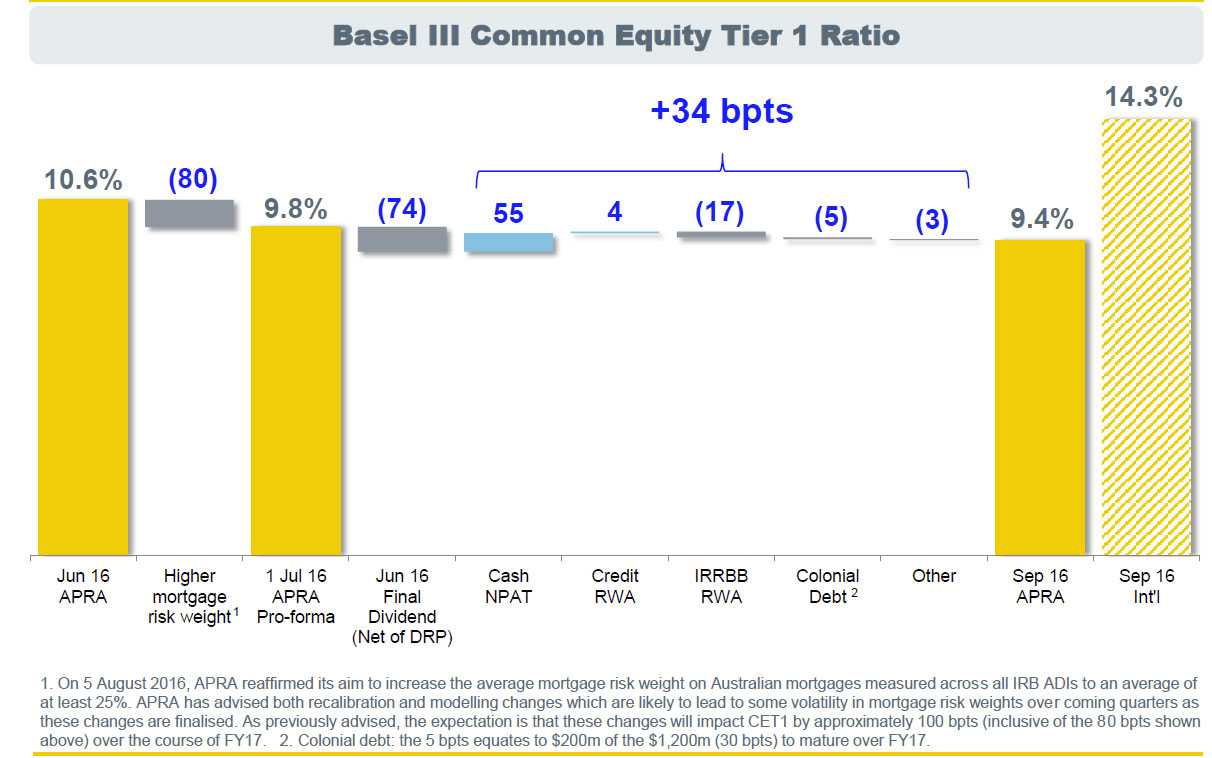

- The Group’s Basel III Common Equity Tier 1 (CET1) APRA ratio was 9.4 per cent as at 30 September 2016. After allowing for the increase in risk weighting for Australian residential mortgages and the impact of the 2016 final dividend (which included the issuance of shares in respect of the Dividend Reinvestment Plan), the CET1 (APRA) ratio increased by 34 basis points in the quarter, primarily driven by capital generated from earnings. The Group’s Basel III Internationally Comparable CET1 ratio as at 30 September 2016 was 14.3 per cent.

- The Group’s Leverage Ratio was 4.8 per cent on an APRA basis and 5.4 per cent on an internationally comparable basis;

- Funding and liquidity positions remained strong, with customer deposit funding at 66 per cent and the average tenor of the wholesale funding portfolio at 4.3 years. Liquid assets totalled $135 billion with the Liquidity Coverage Ratio (LCR) standing at 126 per cent. The Group issued $12.5 billion of long term funding in the quarter.