The Reserve Bank of New Zealand has kept the Official Cash Rate (OCR) at 1.75 percent. They expect to keep the OCR at this level through 2019 and into 2020. Their latest statement on monetary policy was released.

There are both upside and downside risks to our growth and inflation projections. As always, the timing and direction of any future OCR move remains data dependent.

The pick-up in GDP growth in the June quarter was partly due to temporary factors, and business surveys continue to suggest growth will be soft in the near term. Employment is around its maximum sustainable level. However, core consumer price inflation remains below our 2 percent target mid-point, necessitating continued supportive monetary policy.

GDP growth is expected to pick up over 2019. Monetary stimulus and population growth underpin household spending and business investment. Government spending on infrastructure and housing also supports domestic demand. The level of the New Zealand dollar exchange rate will support export earnings.

As capacity pressures build, core consumer price inflation is expected to rise to around the mid-point of our target range at 2 percent.

Downside risks to the growth outlook remain. Weak business sentiment could weigh on growth for longer. Trade tensions remain in some major economies, raising the risk that trade barriers increase and undermine global growth.

Upside risks to the inflation outlook also exist. Higher fuel prices are boosting near-term headline inflation. We will look through this volatility as appropriate. Our projection assumes firms have limited pass through of higher costs into generalised consumer prices, and that longer-term inflation expectations remain anchored at our target.

We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.

Finance Brokers Association of Australia (FBAA) has lodged its response to the royal commission’s interim report, arguing that brokers should not be “forced into even more documentary disclosure” regarding commissions and reiterating its support of the current remuneration structure, via The Adviser.

The interim report from the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry was released at the end of September, raising a swathe of questions regarding the mortgage broking industry.

In the report, the commission questioned some aspects of broker remuneration (including the perceived conflicts of upfront and trail commissions based on loan value and the now largely defunct volume-based commissions), outlined that there was “no simple legal answer” for explaining whom an intermediary (such as a broker) acts for, and questioned the need for a new duty on brokers.

“[I]t will be important to consider whether value and volume-based remuneration of intermediaries should be forbidden,” the commissioner wrote in his report, outlining findings from ASIC’s remuneration review that found that broker loans are marginally larger and have slightly higher loan-to-value ratios (LVRs).

While the full responses to the financial services royal commission have not yet been officially released, the Finance Brokers Association of Australia (FBAA) has revealed that it has tabled a “substantive submission” focusing on disclosure obligations, remuneration structures, compliance with existing laws, and the commission’s call for greater regulation.

Speaking of the association’s submission, FBAA managing director Peter White warned of any wholesale changes to the current broker remuneration model, arguing that major change may be detrimental to the industry.

“We are concerned that a change to the existing structure without fully understanding the impact of any proposed model may simply disrupt a stable and important profession with no corresponding improvement,” Mr White said.

“The majority of misconduct has been due to market participants failing to follow existing laws. This shows that further reforms should not be contemplated until there is compliance with current laws.”

The FBAA also said that its submission disputes claims that lenders paying value-based upfront and trail commissions could be a possible breach of the National Consumer Credit Protection Act (NCCP).

“The relevant section does not prohibit conflicts of interest, only those causing disadvantage, yet the term disadvantage is imperfect and can’t be relied on. It’s our submission that the laws already in place strike an appropriate balance,” Mr White said.

Touching on remuneration disclosure to brokers, the FBAA emphasised that brokers already provide “lengthy disclosure documents”, while the NCCP Act ensures that clients are well informed about the costs and commissions.

“We don’t want brokers to be forced into even more documentary disclosure and that view accords with ASIC’s findings that consumers can disengage because of information overload,” Mr White said.

The managing director of the FBAA concluded that that while the association agrees with the commission’s interim report that improvements could be made, he “agreed” that new laws or regulations are not necessarily the answer.

“Some of the responses to the royal commission have verged on emotional or value proposition statements, and while most have merit, we have deliberately taken a strong legal approach to our language to ensure our messages are clearly understood by the commissioner, a High Court Judge,” Mr White said.

The seventh round of hearings for the final round of the financial services royal commission will be held at the Lionel Bowen Building in Sydney from 19 to 23 November and at the Commonwealth Law Courts Building in Melbourne from 26 to 30 November.

The hearings will focus on “causes of misconduct and conduct falling below community standards and expectations by financial services entities (including culture, governance, remuneration and risk management practices), and on possible responses, including regulatory reform”.

It is expected that the seventh round will be the final round of the financial services royal commission, unless Commissioner Hayne requests, and is granted, an extension.

Commissioner Kenneth Hayne is expected to release his final report, which will include the topics of the fifth, sixth and seventh rounds of hearings (focusing on superannuation, insurance and “policy questions arising from the first six rounds”, respectively) by 1 February 2019.

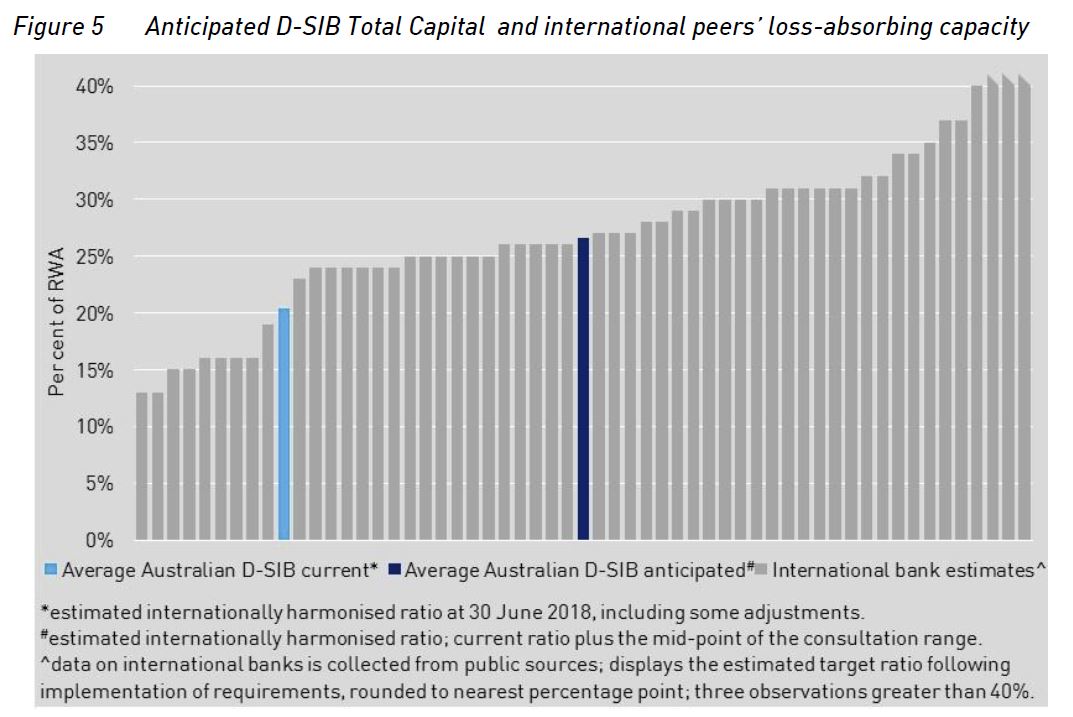

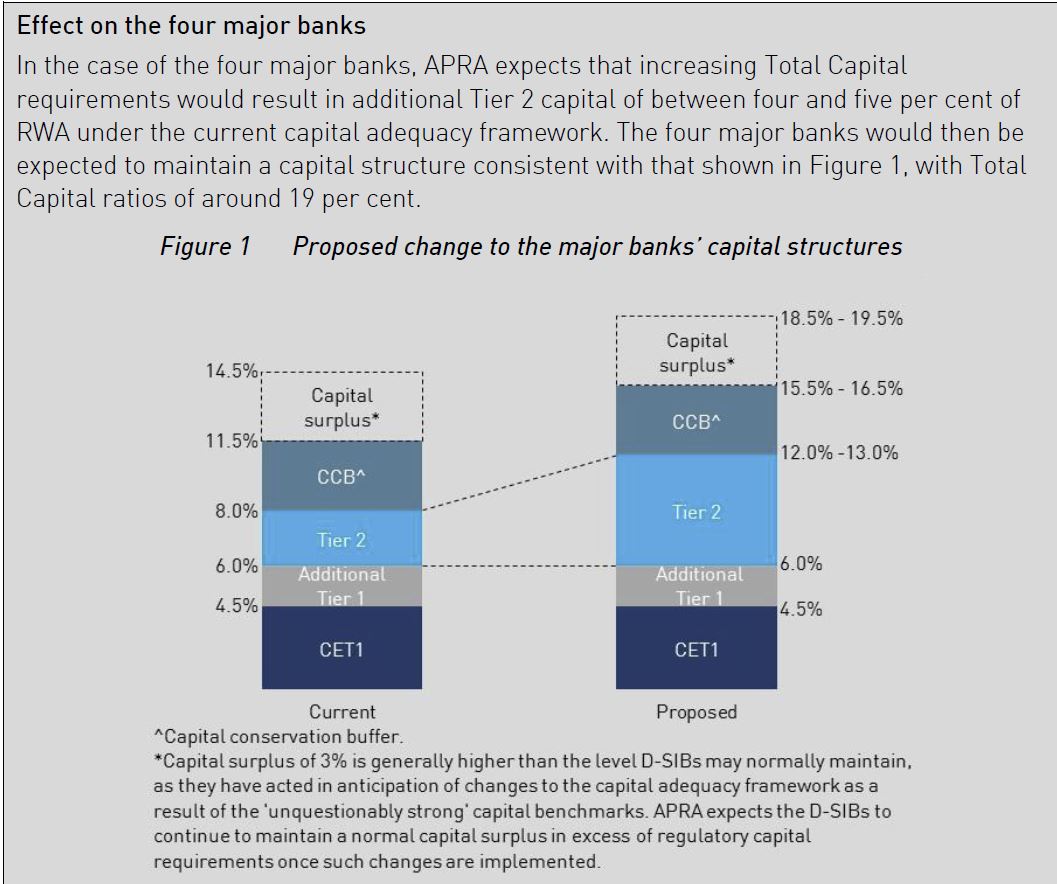

It shows that currently major Australian banks are at the lower end of Total Capital compared with international peers. As a result of proposed changes, major banks (Domestic systemically important banks in Australia, D-SIBs) will see their funding costs rise – incrementally over four years – by up to five basis points based on current pricing. This is intended to build in more financial resilience by lifting the capital requirements, centred on tier 2. Other banks may also be impacted to an extent.

If the D-SIBs were to maintain an additional four to five percentage points of Total Capital they would have ratios more in line with their international peers. But not in the top 25%, and the banks overseas are also lifting capital higher… so some tail chasing here! Is this “unquestionably strong”?

Under the proposals, each D-SIB would be required to maintain additional loss absorbency of between four and five percentage points of RWA. It is anticipated that each D-SIB’s Total Capital requirement would be adjusted by the same amount.

By way of background, the Australian Government’s 2014 Financial System Inquiry (FSI) recommended APRA implement a framework for loss absorbing and recapitalisation capacity in line with emerging international practice, sufficient to facilitate the orderly resolution of Australian ADIs and minimise taxpayer support (FSI Rec 3). The Government supported this recommendation in its response to the FSI.

APRA’s role is not to eliminate failure altogether, but to reduce its probability and impact. This role is set out in APRA’s statutory objectives under the Australian Prudential Regulation Authority Act 1998 and the Banking Act 1959, which require APRA to protect depositors and pursue financial system stability. In performing its functions, APRA will balance those objectives with the need for efficiency, competition, contestability and competitive neutrality in the financial system.

Disorderly failures are inconsistent with APRA’s objectives, as they are highly disruptive to depositors and have an adverse impact on financial system stability. Australia has not experienced a disorderly ADI failure in recent history, though the failure of HIH Insurance Limited (HIH) in 2001 provides an example of the adverse consequences of a disorderly failure of an APRA-regulated institution. In that instance, policyholders were severely affected and essential insurance services to the broader community became unavailable for a period of time.

Conversely, orderly resolution of an ADI would occur when a problem is identified and escalated early enough to allow APRA and other financial regulators to manage and respond in a manner that protects the interests of depositors, stabilises the ADI’s critical functions and promotes financial stability. Achieving an orderly resolution does not necessarily mean a crisis is averted, rather the manner in which an ADI’s failure is managed would result in better outcomes given the circumstances.

APRA’s statutory powers were recently strengthened by the passage of the Financial Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Act 2018.

The effectiveness of resolution planning will be a focus for APRA over the coming years. APRA is in the process of developing a formalised framework for resolution planning and will consult further on this in 2019.

The proposals in this discussion paper focus on the availability of financial resources to support orderly resolution.

These proposals would ensure ADIs have adequate financial resources available to support orderly resolution in the highly unlikely event of failure. This will be achieved by adjusting, where appropriate, an ADI’s Total Capital requirement.

These proposals are distinct from APRA’s work on ensuring ADI capital levels are ‘unquestionably strong’, which relates to the ongoing resilience of institutions and is in response to a separate FSI recommendation (FSI Rec 1).

APRA is proposing an approach on loss-absorbing capacity that is simple, flexible and designed with the distinctive features of the Australian financial system in mind, and has been developed in collaboration with the other members of the Council of Financial Regulators. The key features of the proposals include:

for the four major banks – increasing Total Capital requirements by four to five percentage points of risk-weighted assets

for other ADIs – likely no adjustment, although a small number may be required to maintain additional Total Capital depending on the outcome of resolution planning, which would inform the appropriate amount of additional loss absorbency required to achieve orderly resolution. This assessment would occur on an institution-by-institution basis.

Tier 2 capital instruments are designed to convert to ordinary shares or be written off at the point of non-viability, which means they will be available to absorb losses and can be used to facilitate resolution actions. Tier 2 capital instruments have been a feature of ADI capital structures in various forms since being introduced as part of the 1988 Basel Accord. These instruments have been used as part of resolution actions in other jurisdictions, supporting orderly outcomes.

It is also important that holders of instruments which are intended to be converted or written off in resolution understand the distinctive risks of these investments. In the context of AT1 instruments, APRA has noted that it is inadvisable for investors to view such instruments as higher-yielding fixed-interest investments, without understanding the loss-absorbing role they play in a resolution.15 In the case of the Australian ADIs’ Tier 2 capital instruments, these are mostly issued to institutional investors, who are likely to understand the risks involved.

As ADIs will be able to use any form of capital to meet increased Total Capital requirements, APRA anticipates the bulk of additional capital raised will be in the form of Tier 2 capital. The proposed changes are expected to marginally increase each major bank’s cost of funding – incrementally over four years – by up to five basis points based on current pricing. This is not expected to have an immediate or material effect on lending rates.

APRA proposes that the increased requirements will take full effect from 2023, following relevant ADIs being notified of adjustments to Total Capital requirements from 2019.

In addition to the proposals outlined in this discussion paper, APRA intends to consult on a framework for recovery and resolution in 2019, which will include further details on resolution planning.

APRA Chairman Wayne Byres said one of APRA’s core functions as Australia’s prudential regulator is to plan for, and if required, execute the orderly resolution of the financial institutions it regulates.

“The resilience of the Australian banking system continues to improve, underpinned by the build-up of capital over the last decade.

“However, no matter how resilient financial institutions are, the possibility of failure cannot be entirely removed. Therefore, in addition to strengthening the resilience of the financial system, it is prudent to plan for the unlikely event of failure.

“The events of the global financial crisis demonstrated the impact that failures can have on the broader financial system and the subsequent social and economic consequences.

“The aim of these proposals and resolution planning more broadly is to ensure that the failure of a financial institutions can be resolved in an orderly fashion, which protects the interests of beneficiaries and minimises disruption to the financial system,” Mr Byres said.

The Grattan Institute has rejected the ‘fear factor’ of the financial service industry that encourages Australians to stress about their retirement, via InvestorDaily.

A recently released report by the Grattan Institute, Money in Retirement: More than Enough, reveals that most Australians will be financially comfortable in retirement.

The report shows that retirees are less likely than working-age Australians to suffer financial stress and more likely to have extras like annual holidays.

Grattan Institute chief executive John Daley said that the institute’s models showed that Australians would actually be able to retire in comfort.

“The financial services industry ‘fear factory’ encourages Australians to worry unnecessarily about whether they’ll have enough money in retirement,” he said.

The Institute modelling, even allowing for inflation showed that workers today could expect a retirement income of 91 per cent of their pre-retirement income.

Grattan’s report called on the government to scrap the plan to increase compulsory contributions from 9.5 per cent to 12 per cent as most Australians would be comfortable in retirement.

The report instead called for a 40 per cent increase in the maximum rate of Commonwealth Rent Assistance and for a loosening of the Age Pension assets test which would boost retirement incomes for 70 per cent of future retirees.

The Association of Superannuation Funds of Australia denounced the report calling it an unprecedented attack on the retirement aspirations of ordinary Australians.

ASFA chief executive Dr Martin Fahy said the report was about two Australia’s, one with fully-funded, high-earning retirees and the rest with reliance on the state.

“The Grattan Institute wants to dismantle our world class retirement funding system and replace it with a model that has two thirds of the population relying on the Age Pension,” said Dr Fahy.

Dr Fahy also slammed the reports recommendation that the retirement age be raised to 70 and that the government reviewing the adequacy of Australians’ retirement incomes.

The institute’s report did recommend the government review the adequacy of Australians’ retirement income and called for a new standard.

“The Productivity Commission should establish a new standard for retirement income adequacy and assess how well Australians of different ages and incomes will meet that standard. References to the ASFA comfortable retirement standard should be removed,” the report read.

“The ASFA Retirement Standard provides a detailed account of living expenses in retirement.

“The Grattan analysis in effect wants people in retirement not to have heating in winter, not to take vacations, to get rid of the car, and skimp on prescriptions and other out-of-pocket health care costs,” said Dr Fahy.

The report for its part has said that reform is needed by the government to be able to fund aged care and health in the future.

“Unless governments have the courage to make these reforms, future budgets will not be able to fund aged care and health at the same level as today, which is the real threat to adequate retirement incomes in future,” it said.

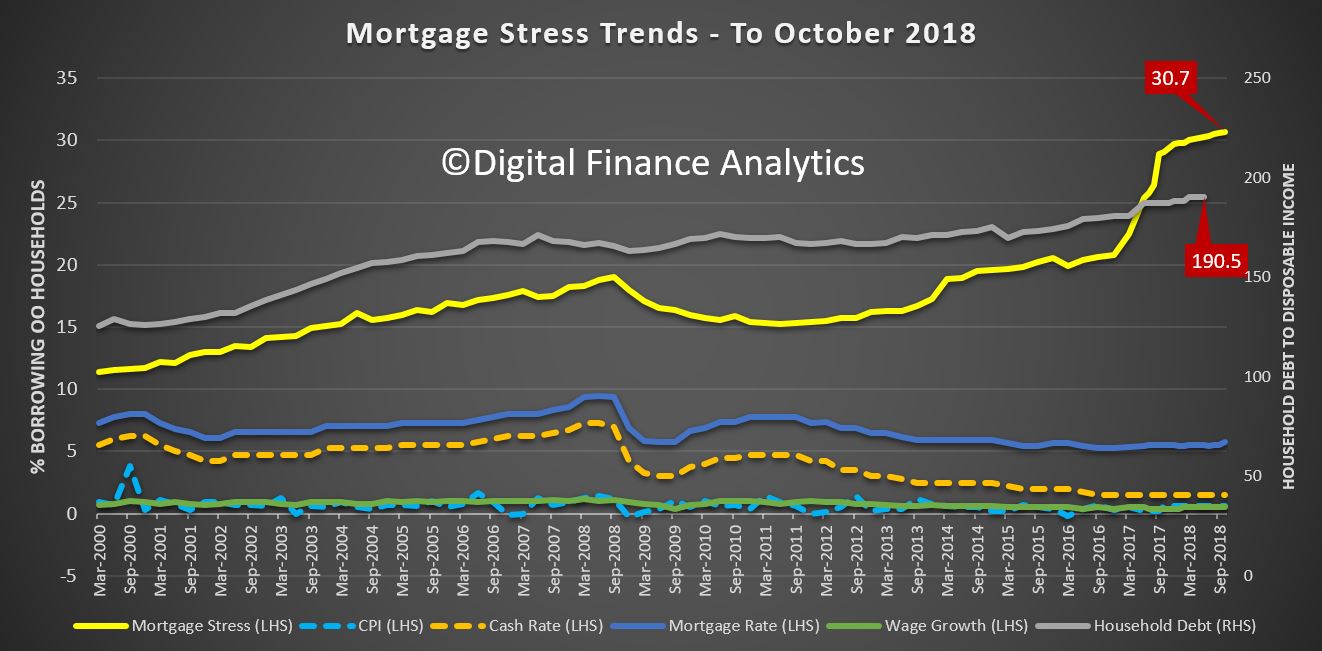

We have completed our October 2018 mortgage stress analysis and today we discuss the results.

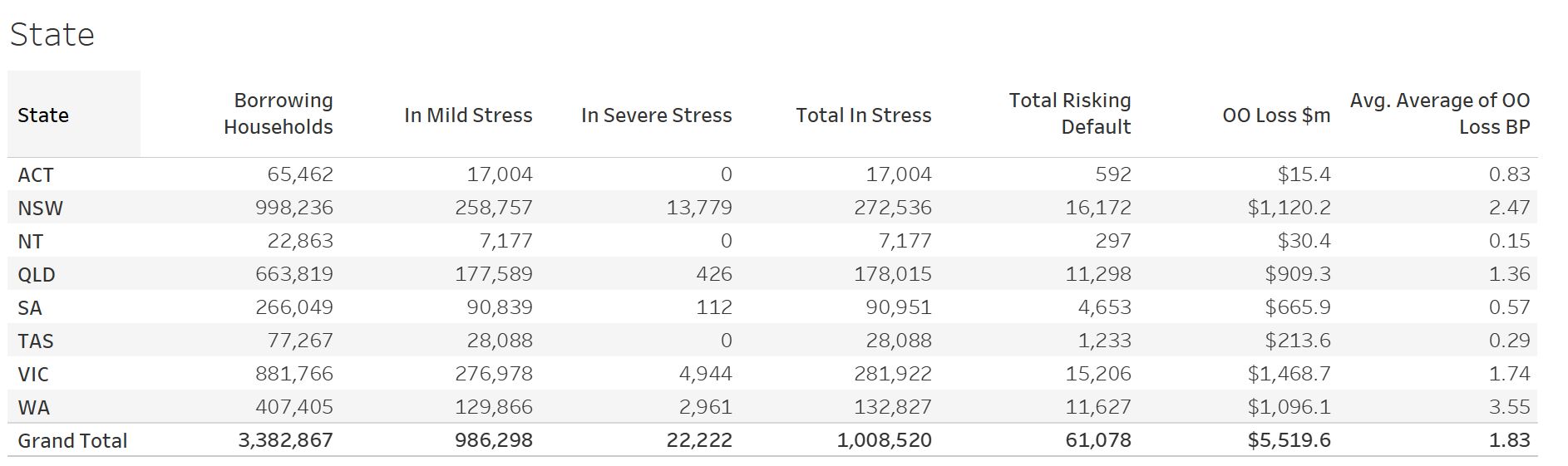

The latest RBA data on household debt to income to June reached a new high of 190.5. This high debt level helps to explain the fact that mortgage stress continues to rise. Having crossed the 1 million Rubicon last month, across Australia, more than 1,008,000 households are estimated to be now in mortgage stress (last month 1,003,000). This equates to 30.7% of owner occupied borrowing households.

In addition, more than 22,000 of these are in severe stress. We estimate that more than 61,000 households risk 30-day default in the next 12 months. We continue to see the impact of flat wages growth, rising living costs and higher real mortgage rates. Bank losses are likely to rise a little ahead.

Our analysis uses the DFA core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to the end of October 2018. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Households are defined as “stressed” when net income (or cash flow) does not cover ongoing costs. They may or may not have access to other available assets, and some have paid ahead, but households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell.

This rise in stress, which has continued for the past 6 years, should be of no surprise at all. “Continued rises in living costs – notably child care, school fees and fuel – whilst real incomes continue to fall and underemployment is causing significant pain. Many are dipping into savings to support their finances.”

Indeed, the fact that significant numbers of households have had their potential borrowing power crimped by lending standards belatedly being tightened, and are therefore mortgage prisoners, is significant. More than 40% of those seeking to refinance are now having difficulty. This is strongly aligned to those who are registering as stressed. These are households urgently trying to reduce their monthly outgoings.

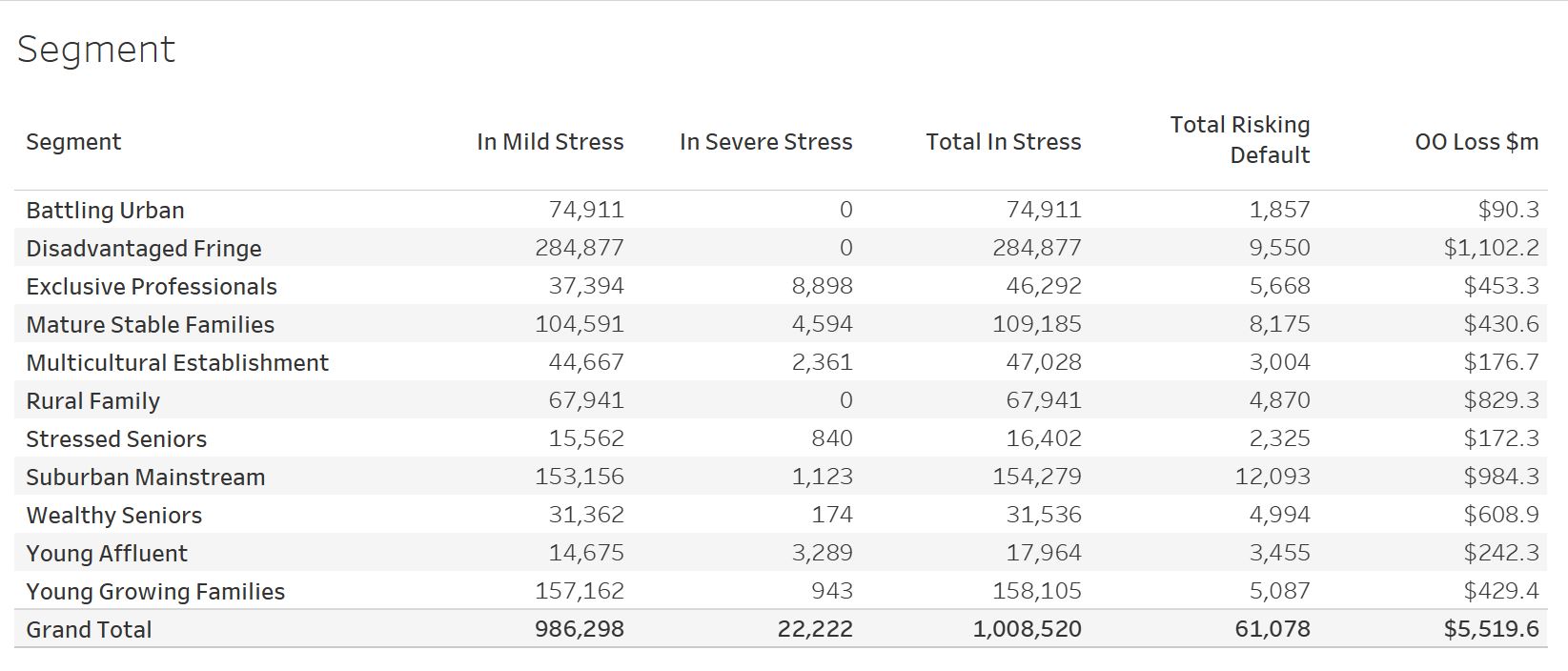

Probability of default extends our mortgage stress analysis by overlaying economic indicators such as employment, future wage growth and cpi changes. Our Core Market Model also examines the potential of portfolio risk of loss in basis point and value terms. Losses are likely to be higher among more affluent households, contrary to the popular belief that affluent households are well protected. This is shown in the segment analysis, with some more wealthy households up against it.

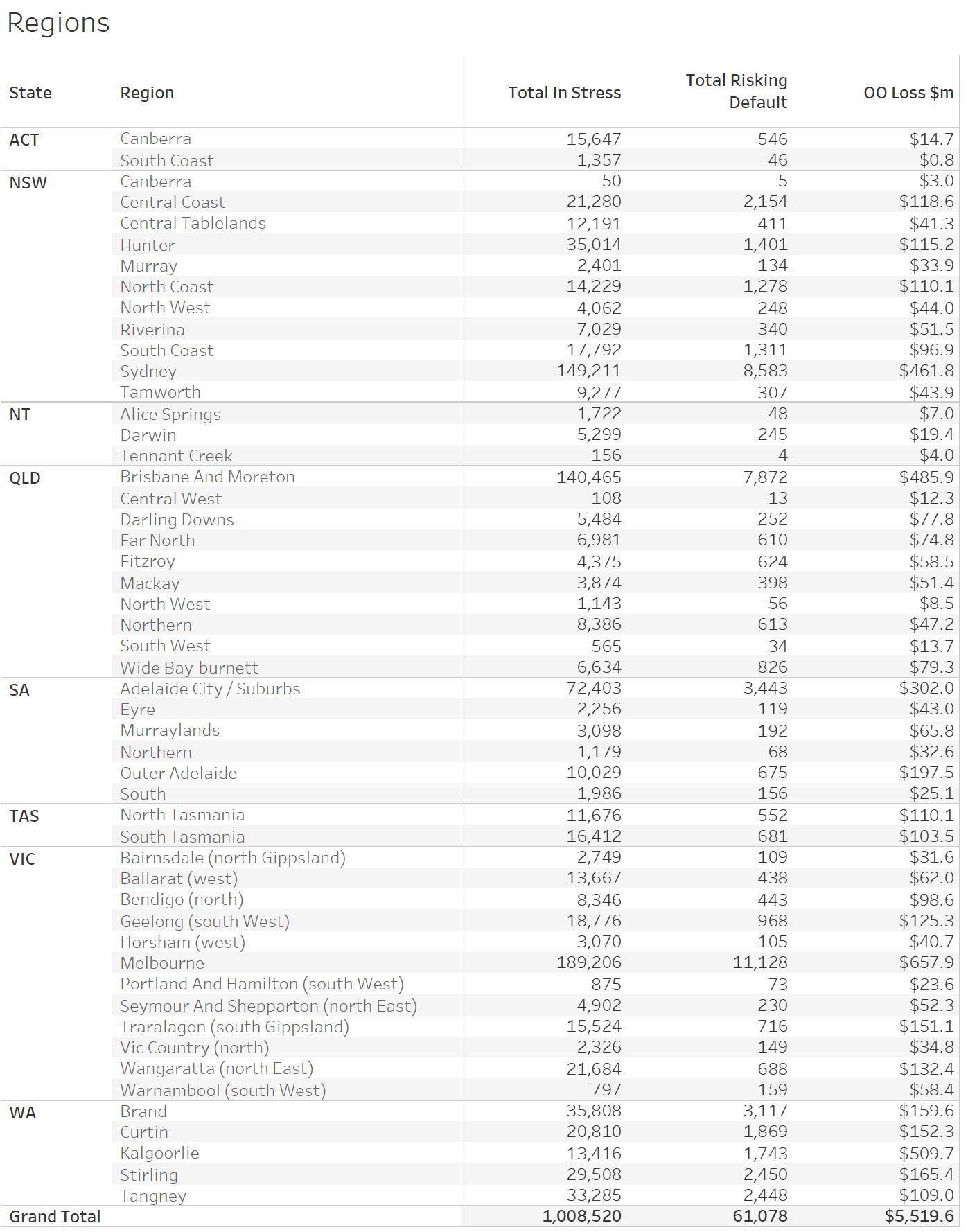

Regional analysis shows that NSW has 272,536 households in stress (276,132 last month), VIC 281,922 (276,926 last month), QLD 178,015 (176,528 last month) and WA has 132,827 (132,700 last month). The probability of default over the next 12 months rose, with around 11,630 in WA, around 11,300 in QLD, 15,200 in VIC and 16,200 in NSW. The largest financial losses relating to bank write-offs reside in NSW ($1.1 billion) from Owner Occupied borrowers) and VIC ($1.74 billion) from Owner Occupied Borrowers, though losses are likely to be highest in WA at 3.6 basis points, which equates to $1,096 million from Owner Occupied borrowers.

Turning to the post codes with the largest counts of households in stress, fifth was Melbourne suburb Berwick and Harkaway, 3806, with 5,267 households in stress and 143 risking default.

In fourth place is Toowoomba and the surrounding area, in Queensland, 4350, with 6,437 households in stress and 256 risking default.

Next in third place is Campbelltown in NSW, 2560, with 6,781 households in stress and 110 risking default.

In second place is Tapping and the surrounding areas in WA, 6065 with 7,409 in stress and 298 risking default

And in first place, the post code with the largest number of households in mortgage stress this month is the area around Chipping Norton and Liverpool, 2170, with 7,732 households in stress and 116 risking default.

As always, it’s worth saying that given flat incomes, and rising costs, and some mortgage rate rises, the pressure will continue, and falling home prices will make things worse. Many people do not keep a cash flow, so they do not know their financial position – drawing one up is the first step and ASIC has some excellent advice on their MoneySmart website. And the other point to make is, if you are in financial distress, you should talk to your lender, they do have an obligation to help in cases of hardship. The worst strategy is simply to ignore the issue and hope it will go away. But in my experience, this is unlikely.

We will update the data again next month.

You can request our media release. Note this will NOT automatically send you our research updates, for that register here.

[contact-form to=’mnorth@digitalfinanceanalytics.com’ subject=’Request The October 2018 Stress Release’][contact-field label=’Name’ type=’name’ required=’1’/][contact-field label=’Email’ type=’email’ required=’1’/][contact-field label=’Email Me The October 2018 Media Release’ type=’radio’ required=’1′ options=’Yes Please’/][contact-field label=”Comment If You Like” type=”textarea”/][/contact-form]

Note that the detailed results from our surveys and analysis are made available to our paying clients.

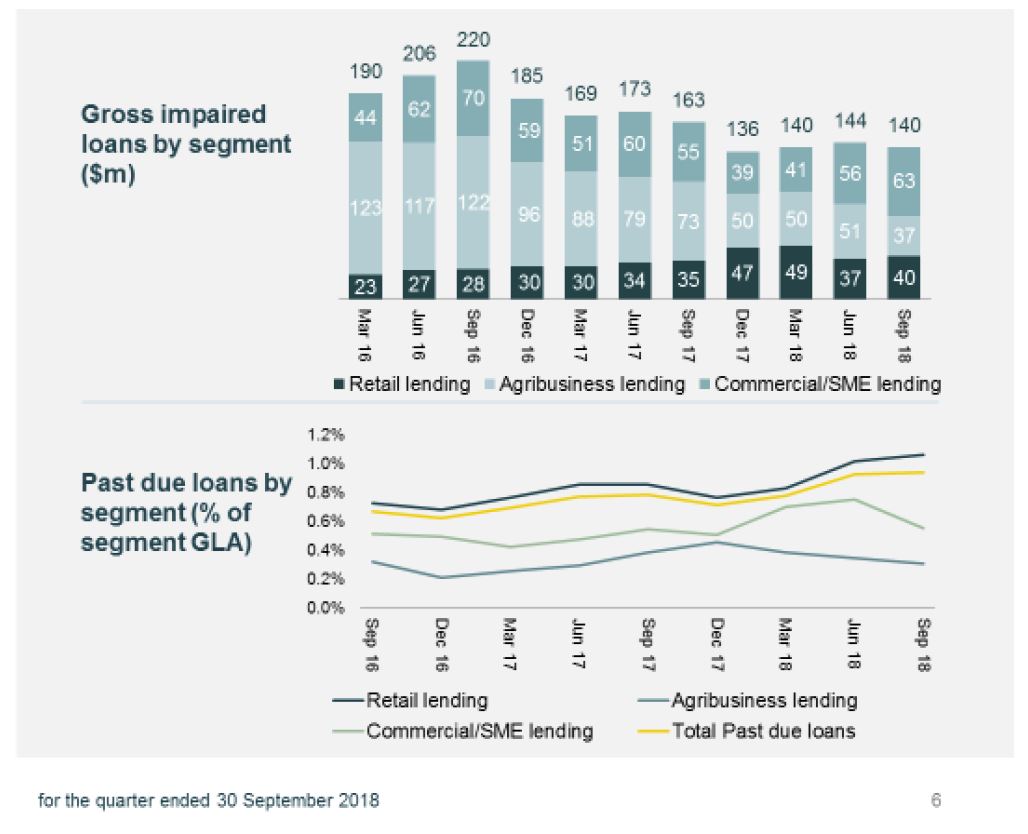

Suncorp released their APS 330 report for the quarter ended September 2018. Like the majors, funding pressure and slow loan growth are impacting the results. There was a rise in 90-day plus past due. They expect the moderation of home lending growth to continue. Sustained pressure from price competition and elevated funding costs is expected to result in a FY19 net interest margin at the low end of the 1.80% to 1.90% target range.

During the September quarter, total lending growth was $265 million or 0.5%. The home lending portfolio grew $361 million, up 0.8% over the quarter, within a competitive and slowing mortgage market. The home lending portfolio remains comfortably within macroprudential limit settings as Suncorp continues to be selective in its target markets. The business lending portfolio contracted $90m or 0.8% over the quarter, with moderate growth in the commercial and small business portfolios offset by a reduction in agribusiness lending following customers repayment of debt.

The transition to AASB 9 Financial Instruments (AASB 9) increased the collective provision in the balance sheet by $20 million on 1 July 2018. Following the adoption of AASB 9, provisions are expected to be more variable from period to period reflecting the increased sensitivity of the modelling to changes in economic conditions and the risk profile of Suncorp’s lending portfolio; and the movement of exposures across credit stages.

A net positive movement in impairment losses was driven by a small number of one-off customer recoveries and an improvement in the risk profile of the lending portfolio, as assessed under AASB 9.

Gross impaired assets of $140 million remained broadly stable over the quarter. Past due retail loans grew by 5.2% to $510 million over the quarter, primarily driven by an increase in customer tenure in late stage arrears. Suncorp’s approach to management of arrears is continually reviewed to improve outcomes for all stakeholders.

Wholesale funding costs continue to be impacted by the elevated Bank Bill Swap Rate (BBSW). During the quarter, Suncorp continued to support its sustainable and diversified funding base by issuing a five-year $750m covered bond. Suncorp also achieved a strong increase in at-call deposits, growing 4.7 times system over the quarter. The Net Stable Funding Ratio (NSFR) was 111% as at 30 September 2018. The LCR was 128%.

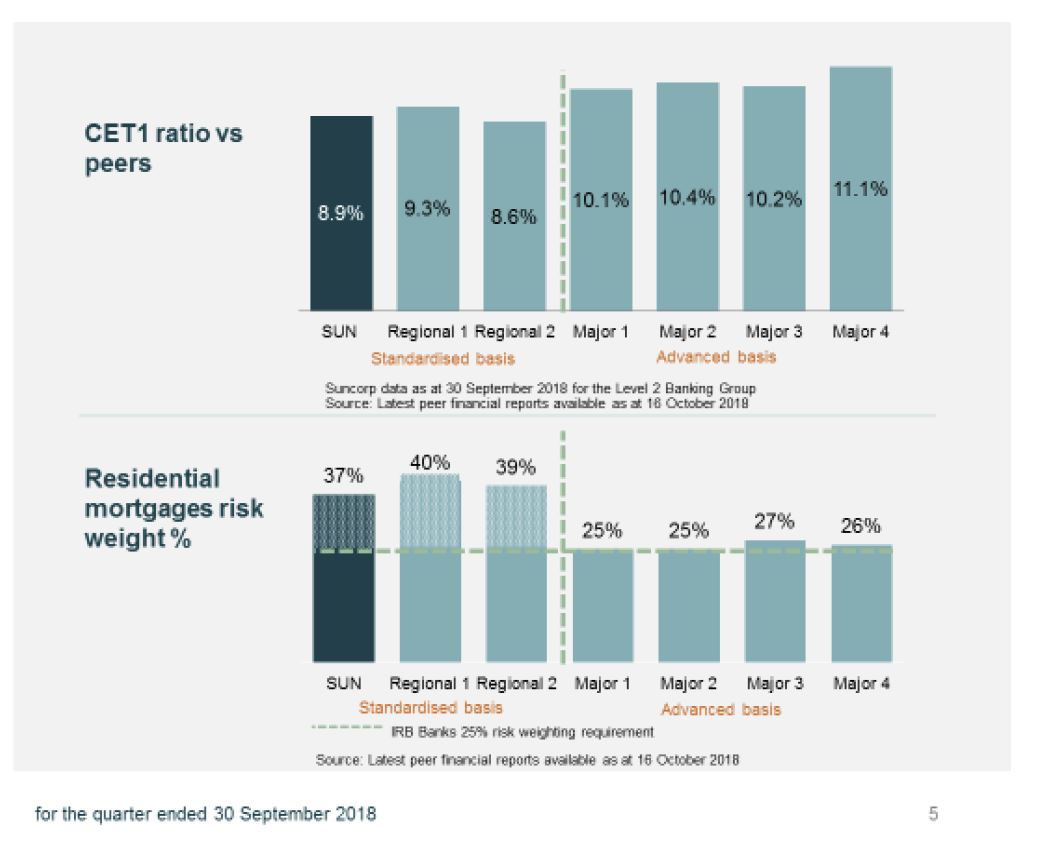

Following payment of the 2018 financial year final dividend to Suncorp Group, Banking’s Common Equity Tier 1 (CET1) ratio of 8.9% reflects a sound capital position towards the upper end of the target operating range of 8.5% to 9.0%.

The moderation of home lending growth is expected to continue, driven by a slowing market and impacts associated with regulatory reforms. Balances of vanilla housing loans dropped by 1.7% compared with the previous quarter, but this was offset by a rise in securitised housing loans and covered bonds, up 16.3%. They grew more in Queensland than outside the state.

They said they will target above system growth in both home lending and business lending for the financial year, provided that pricing and lending criteria remain within the portfolio tolerance settings, noting the impact that ongoing drought conditions may have on the agribusiness portfolio.

Suncorp will continue to maintain a conservative risk appetite, with no material changes in any segment. While impairments could be impacted by economic factors and ongoing drought conditions, they are expected to remain below the bottom end of the through-the-cycle operating range of 10 to 20 basis points of gross loans and advances.

Suncorp continues to target above system growth in at-call customer deposits, leveraging the investments made in enhanced digital and payment capabilities. Sustained pressure from price competition and elevated funding costs is expected to result in a FY19 net interest margin at the low end of the 1.80% to 1.90% target range.

They say the expected impacts of the Basel III reforms and APRA’s roll-out of unquestionably strong benchmarks cannot be confirmed until APRA releases the draft standards, which is assumed to be in early 2019.

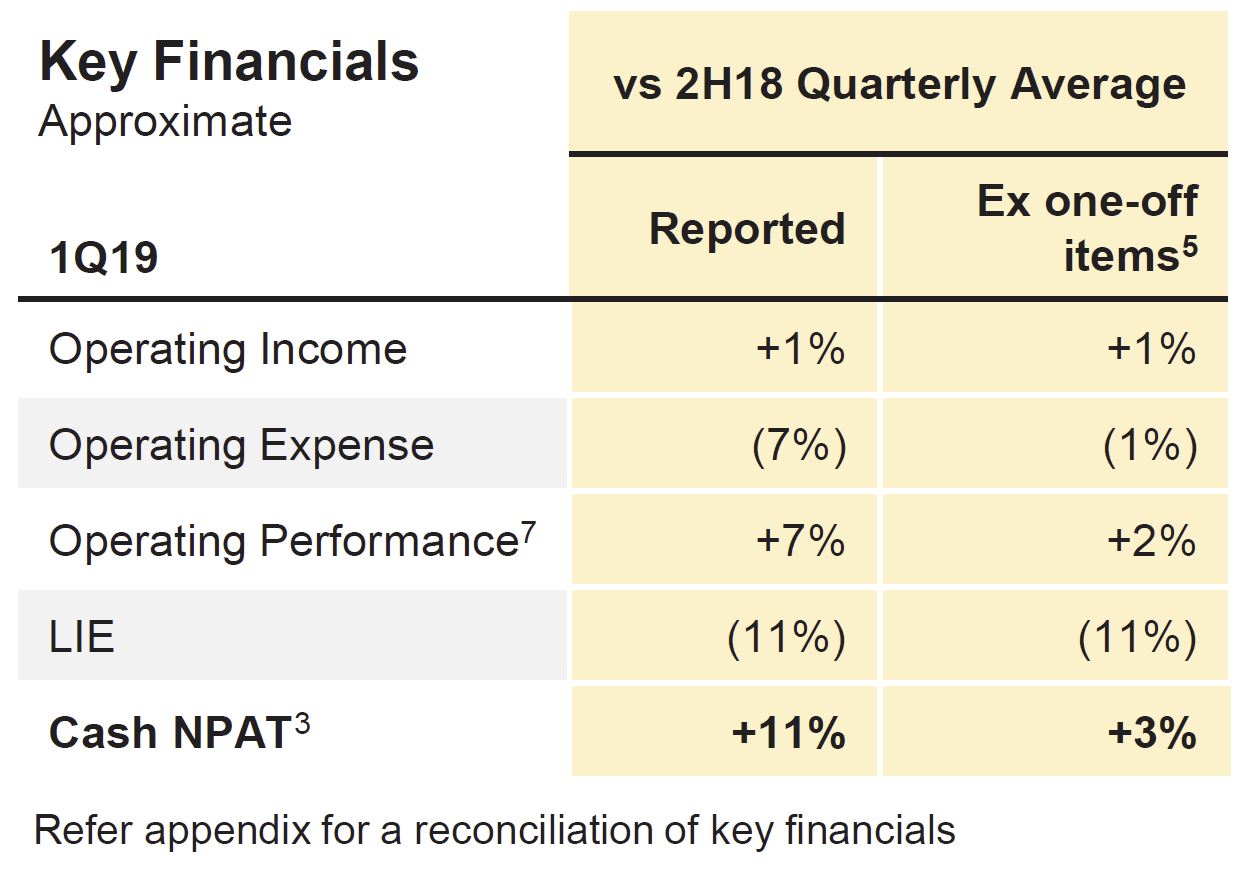

CBA released their 1Q19 trading update today. Their unaudited statutory net profit was approximately $2.45bn in the quarter and unaudited cash net profit was approximately $2.50bn in the quarter, both rounded to the nearest $50 million. The cash basis is used by management to present a clear view of the Group’s operating results. CBA did not include any further customer remediation charges in the quarter.

Their operating Income up 1%, with higher other banking income offsetting flat net interest income. But the Group Net Interest Margin was lower in the quarter due to higher funding costs (including basis risk which arises from the spread between the 3 month bank bill swap rate and 3 month overnight index swap rate; and replicating portfolio) and home loan price competition.

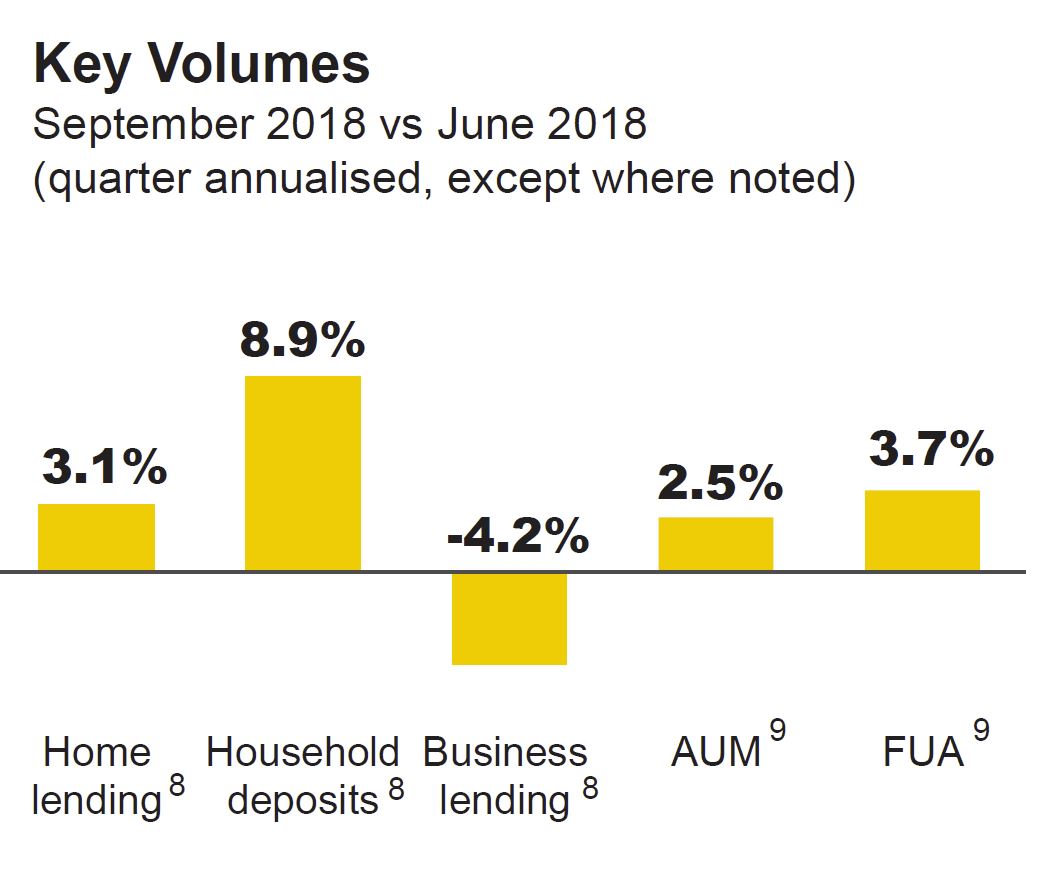

Volume growth included 8.9% quarter annualised growth in household deposits. Home lending growth of 3.1% was below system growth of 3.6% (both quarter annualised). Business lending reflected continued portfolio optimisation in the institutional book.

Operating Expenses ex one-off items were down 1% due to timing of investment spend and software impairments in the comparative period.

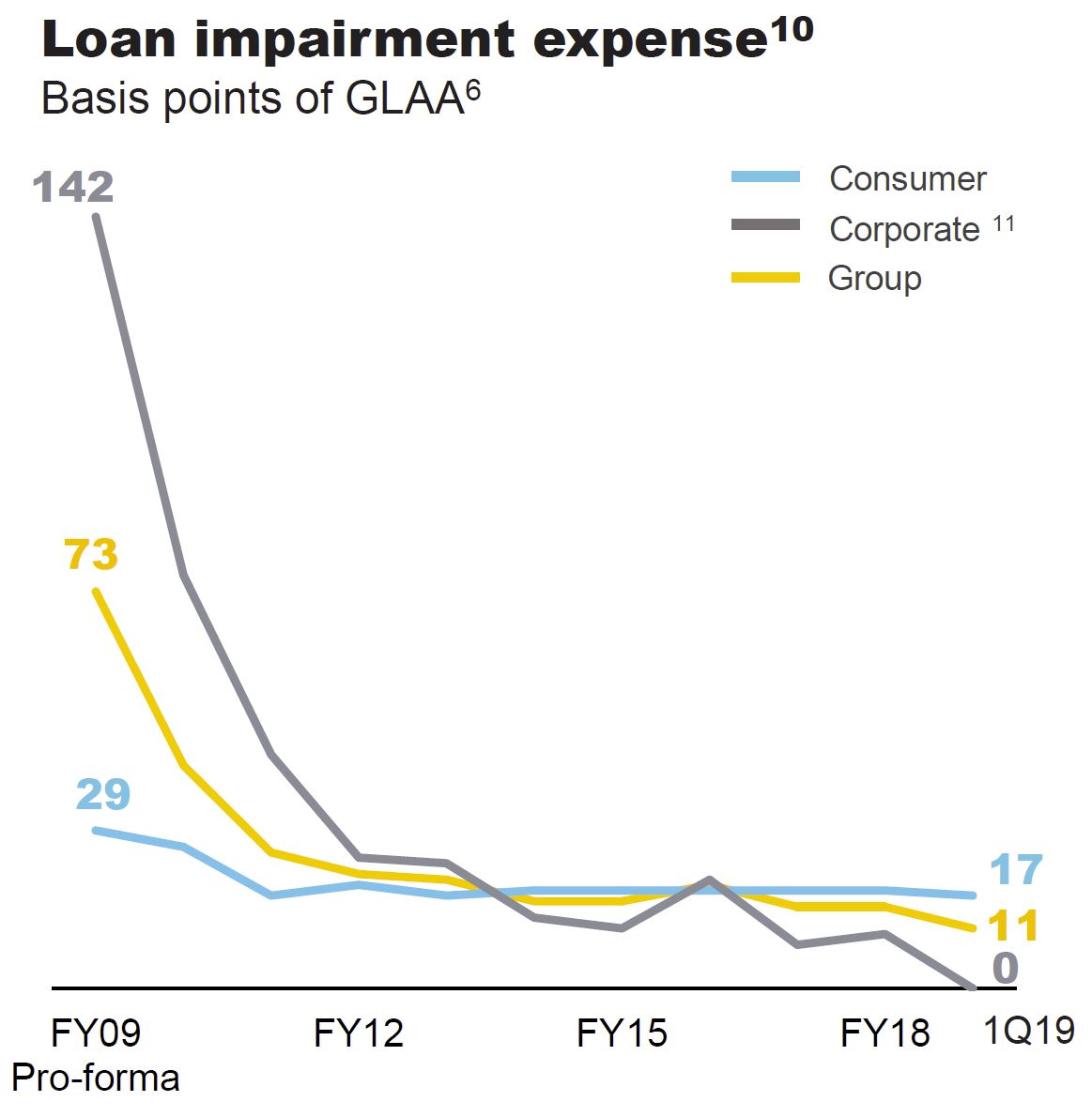

Loan Impairment Expense (LIE) were $216 million in the quarter or 11bpts of GLAA and equated to 11 basis points of Gross Loans and Acceptances, compared to 15 basis points in FY18. Low corporate LIE reflected some single name improvements, sound portfolio credit quality and continued IB&M portfolio optimisation.

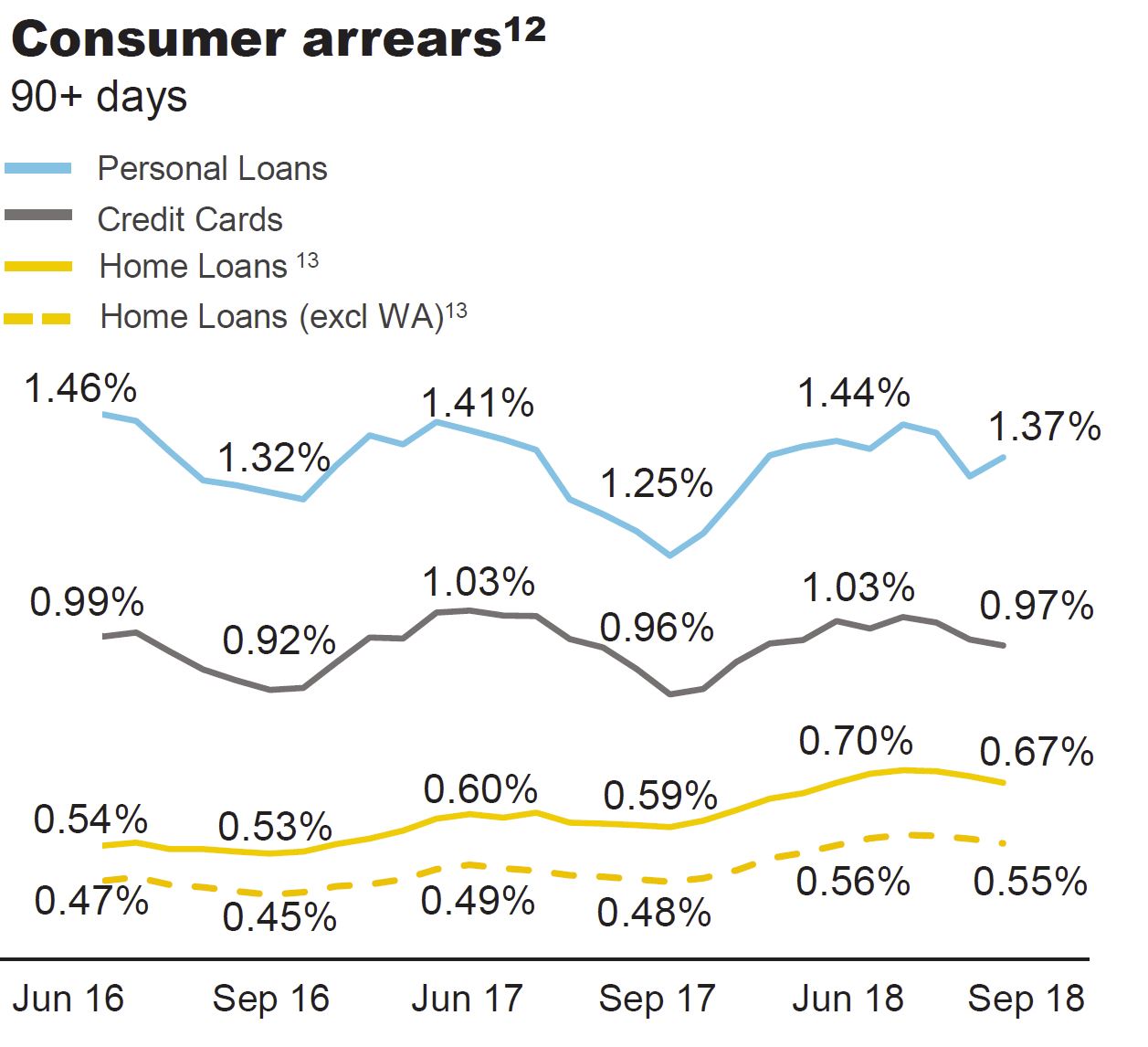

Consumer arrears were seasonally lower in the quarter. Whilst there was a moderate improvement in home loan arrears, some households continued to experience difficulties with rising essential costs and limited income growth.

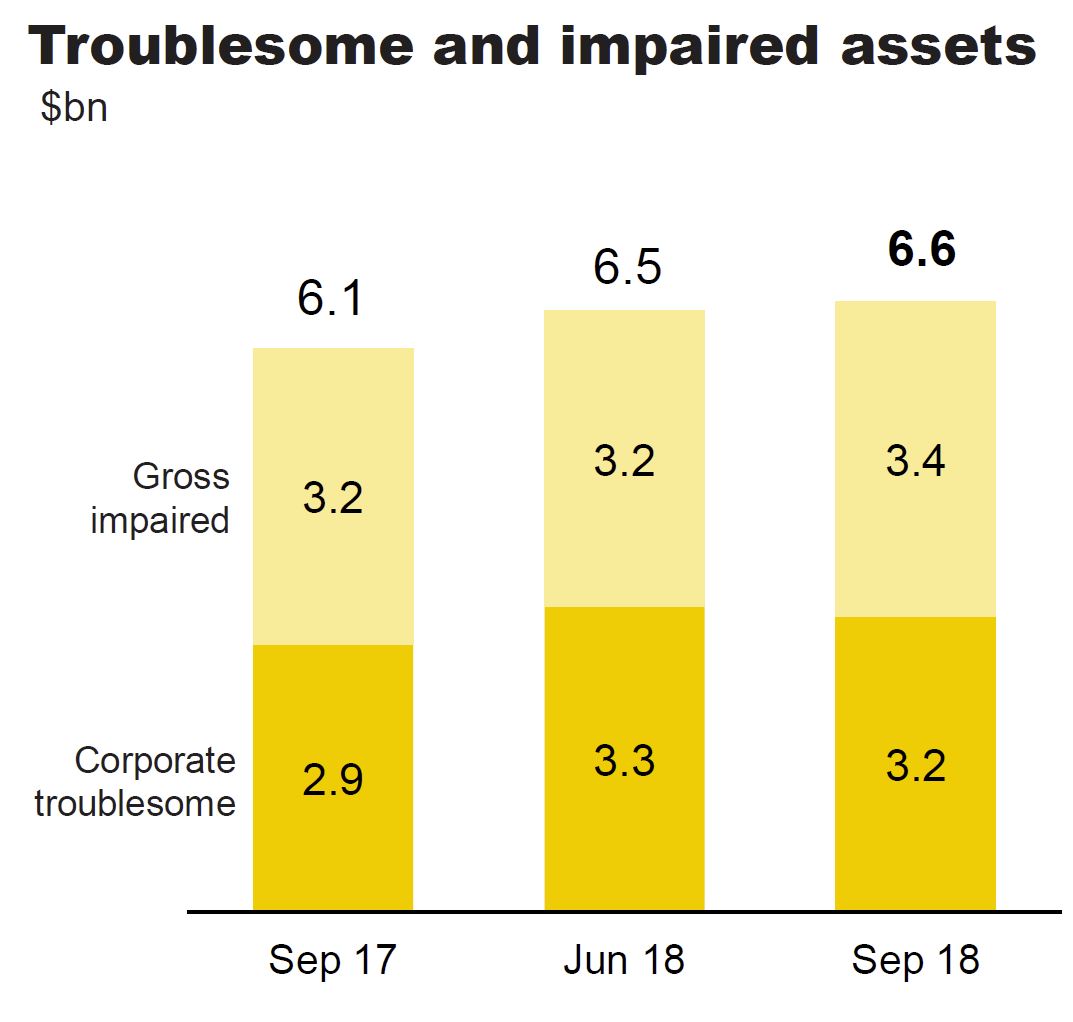

Troublesome and impaired assets increased from $6.5 billion at June 2018 to $6.6 billion in September, driven by an increase in home loan impaired assets and a small number of individual corporate impairments.

Troublesome exposures were broadly stable in the quarter.

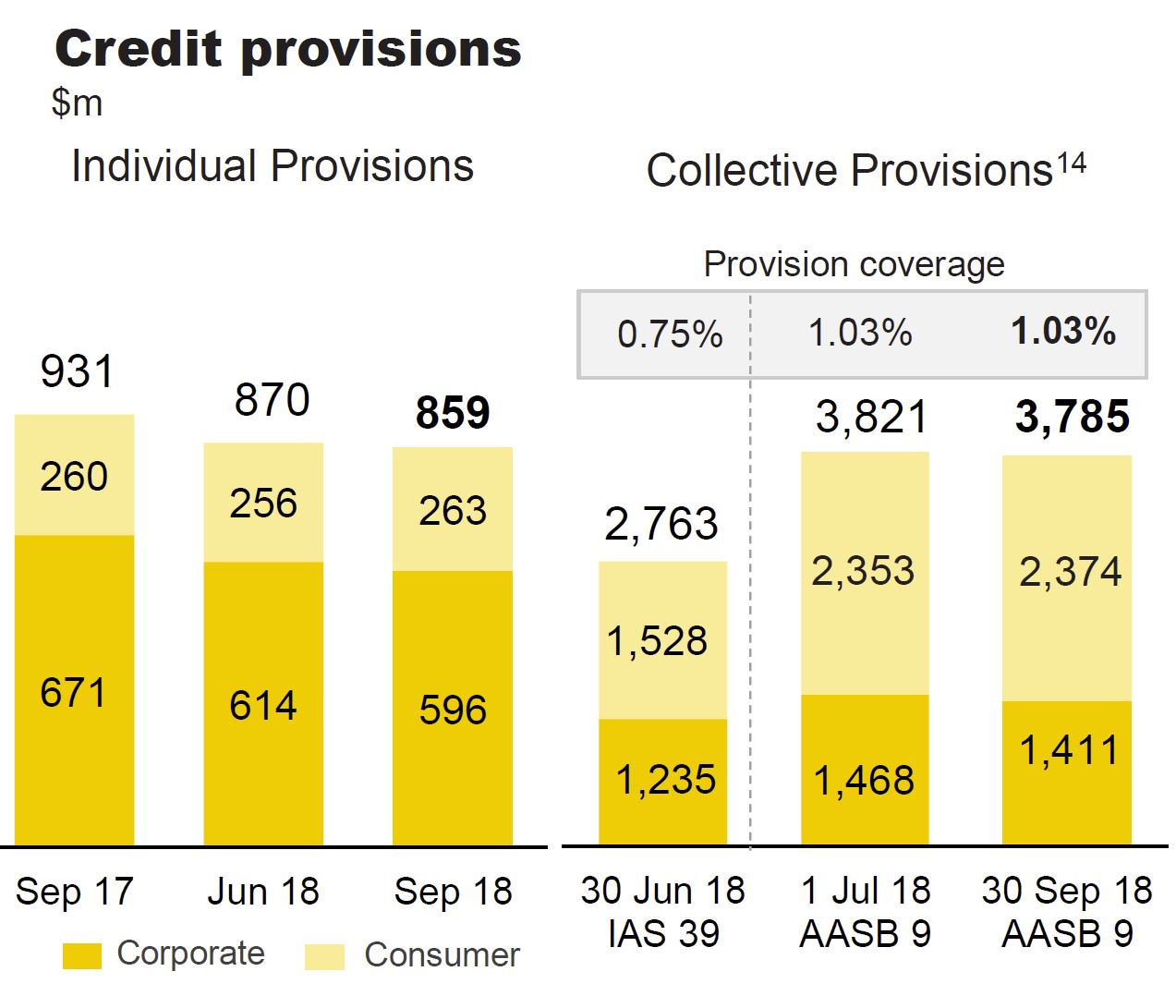

The Group adopted AASB 9 from 1 July 2018 resulting in a $1.06 billion increase to collective provisions and a 28 bpt increase in collective provision coverage to 1.03% (collective provisions to credit risk weighted assets).

Total Provisions were broadly stable in the quarter.

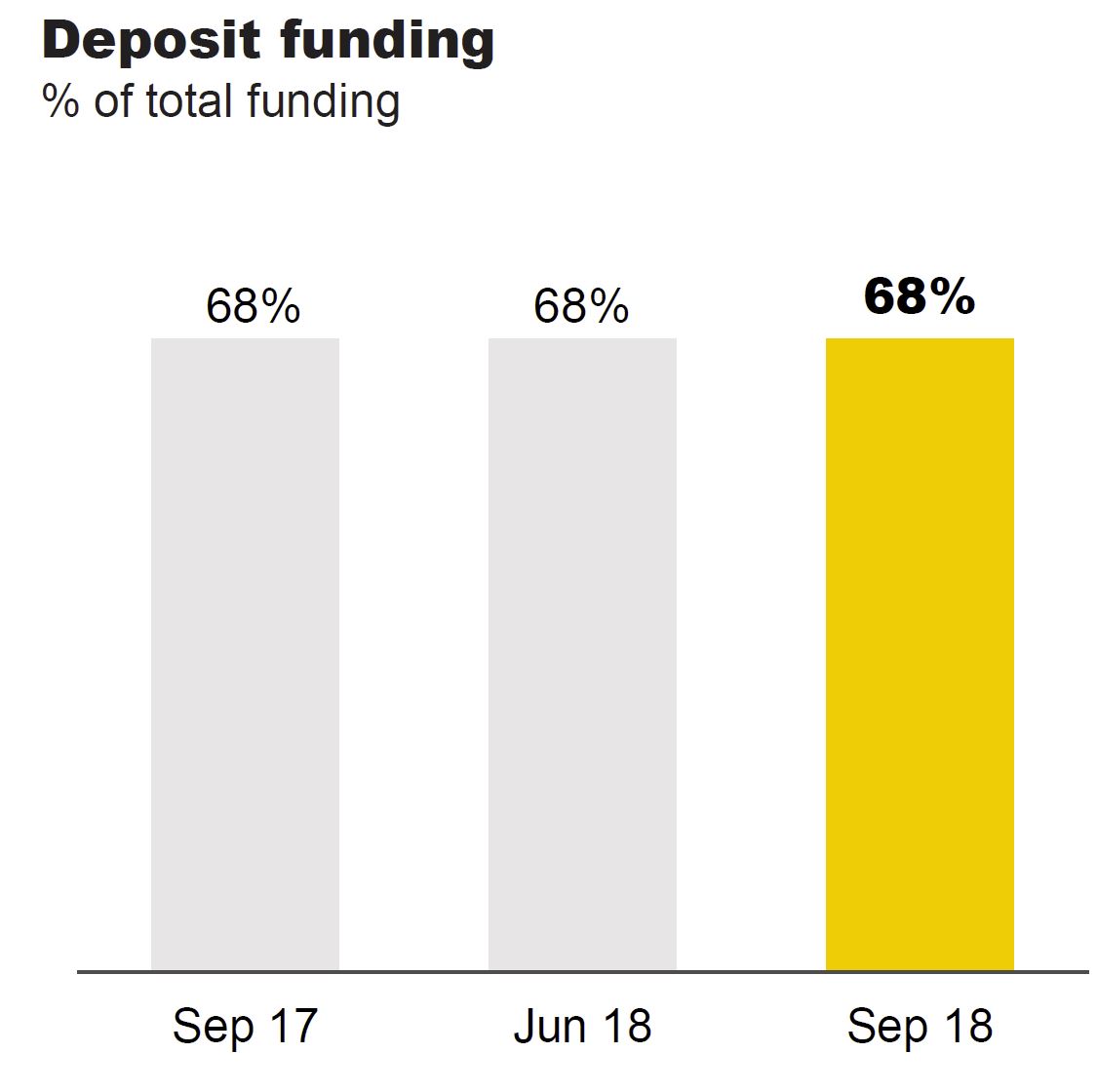

Customer deposit funding remained at 68%.

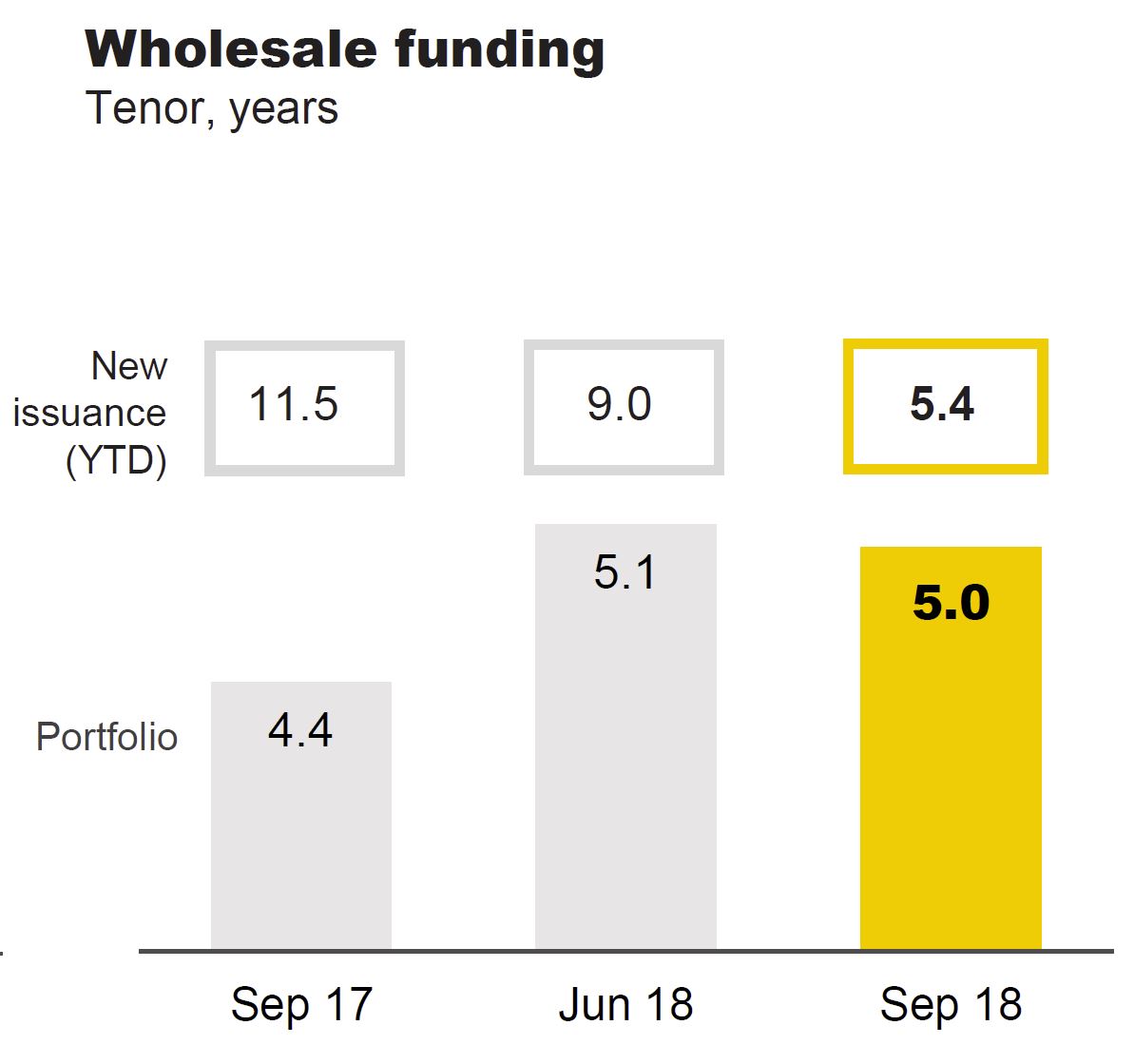

The average tenor of the long term wholesale funding portfolio at 5.0 years.

The Group issued $8.8 billion of long term funding in the quarter.

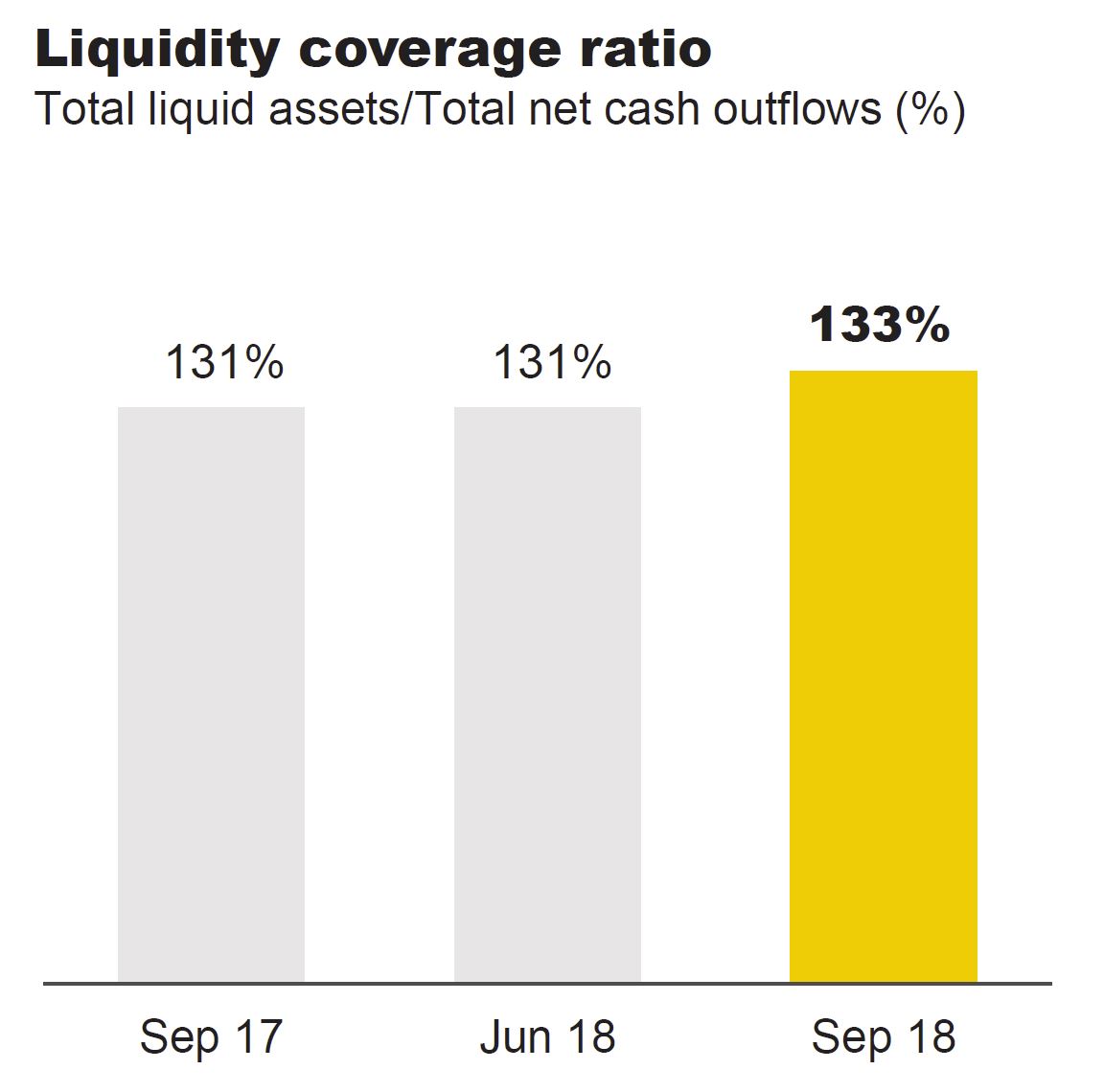

The Liquidity Coverage Ratio (LCR) was 133% at September 2018, up from 131% at June 2018.

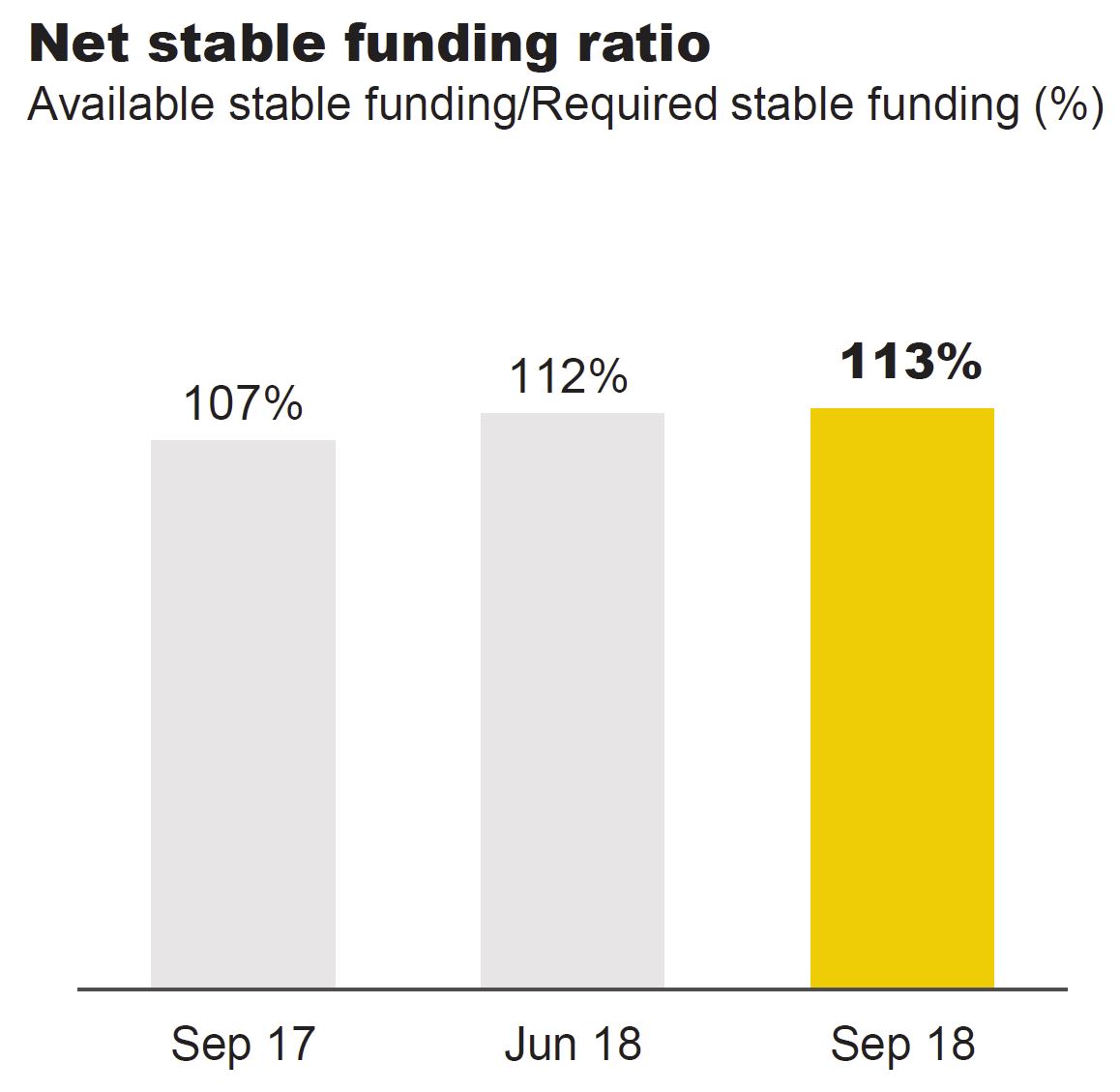

The Net Stable Funding Ratio (NSFR) was 113% at September 2018, up from 112% at June 2018.

The Group’s Leverage Ratio remained relatively stable across the quarter at 5.5% on an APRA basis and 6.2% on an internationally comparable basis.

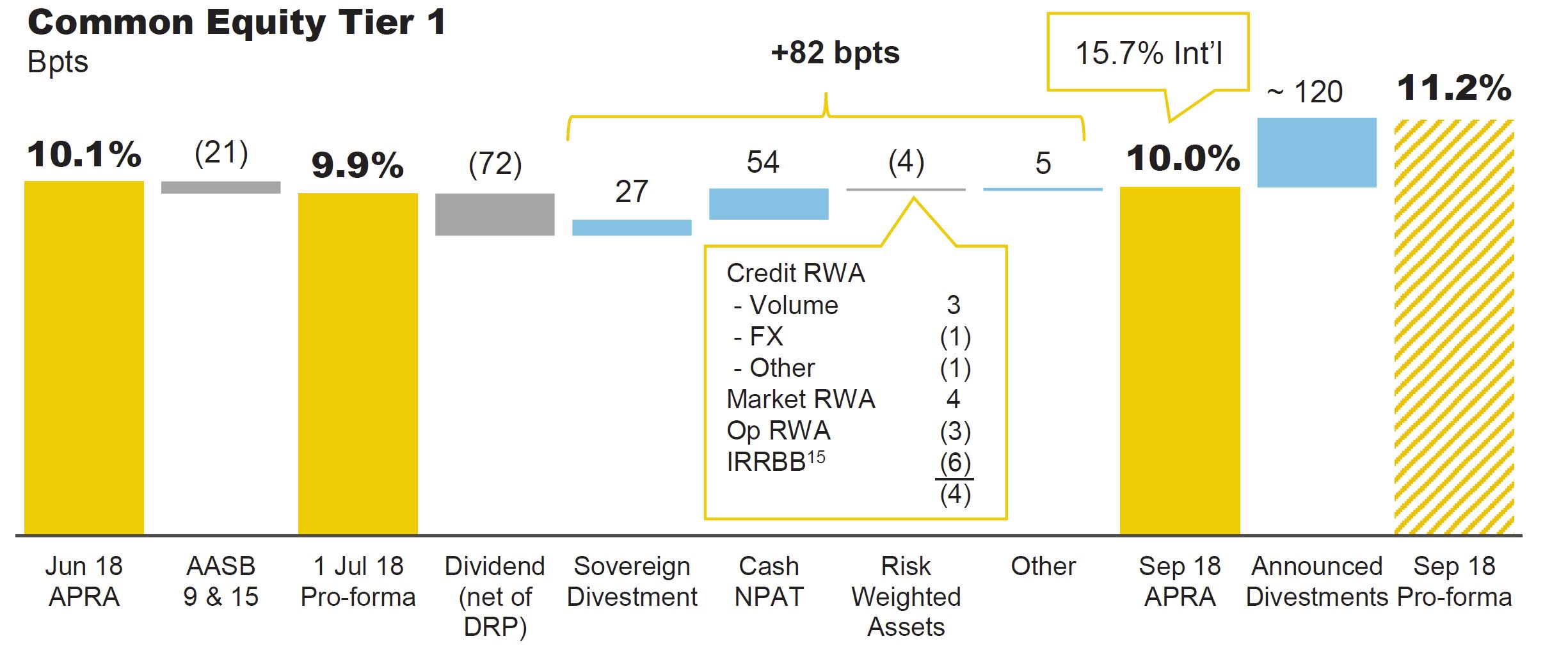

The Common Equity Tier 1 (CET1) APRA ratio was 10.0% as at 30 September 2018. After allowing for the impact of the implementation of AASB 9 and 15 on 1 July 2018, and the 2018 final dividend (which included the issuance of shares in respect of the Dividend Reinvestment Plan), CET1 increased 82 bptsin the quarter. This was driven by a combination of capital generated from earnings and the benefit from the sale of the Group’s New Zealand life insurance operations.

CBA has previously announced the divestment of a number of businesses as part of its strategy to build a simpler, better bank. These divestments are subject to various conditions, regulatory approvals and timings, and include the sale of the bank’s global asset management business, Colonial First State Global Asset Management (CFSGAM, expected completion mid calendar year 2019) and the sales of its Australian life insurance business (“CommInsureLife”), its non-controlling investment in BoCommLife and its 80% interest in the Indonesian life insurance business, PT Commonwealth Life (all expected to complete in the first half of calendar year 2019). Collectively, these divestments will provide an uplift to CET1 of approximately 120 bpts, resulting in a 30 September 2018 pro-forma CET1 ratio of 11.2%.

In June 2018, CBA announced its commitment to the demerger of NewCo, which includes Colonial First State, Count Financial, Financial Wisdom, Aussie Home Loans and CBA’s minority shareholdings in ASX-listed companies CountPlusand Mortgage Choice. The demerger process is expected to be completed by late calendar year 2019, subject to shareholder and regulatory approvals. CFSGAM will no longer form part of NewCo, following the recent announcement of an agreement to sell this business to Mitsubishi UFJ Trust and Banking Corporation.

The end of year analysis by KPMG has shown the need for the major Australian banks to become leaner and simpler to benefit customers, via InvestorDaily.

The KPMG 2018 financial year results analysis showed that in 2018 major banks cash profit after tax decreased by 5.5 per cent to $29.5 billion.

One element that caused loss was the increase in compliance and remediation costs as a result of a challenging and changing operating environment for the majors.

The report found that regulatory, compliance and customer remediation costs had increased the cost to income ratios across the majors from 43.1 per cent to 46.6 per cent.

KPMG predicted that banks would become leaner and simpler in the 2019 financial year as a response to these rise of costs.

KPMG Strategy banking partner Hessel Verbeek said banks needed to simplify their approach as complexity was keeping them from meeting expectations.

“The Australian banking industry is facing a confluence of factors, making simplification vital, but also complex. Without change, incumbent banks will struggle to meet shareholder, customer and regulatory expectations,” he said.

Mr Verbeek said simplifications would be different for each bank depending on its strategic objectives but all of them would have same overall goal.

“The target state for bank simplifications is a ‘connected enterprise’, which is entirely organised around customer needs and is omni-channel, but with a digital focus.

“The bank is streamlined from front-to-back, with every process putting the customer at the core,” he said.

Mr Verbeek gave five steps towards bank simplification:

Clarify the bank’s strategic focus and make clear choice around competitive positioning

Choose a director for the bank’s business architecture

Determine which activities are strategic and provide a competitive advantage, given the bank’s agreed focus in the first step

Assess the simplification options for the bank’s activities, in line with its strategic focus

Develop the simplification roadmap, taking into account various dependencies

Mr Verbeek said there were three potential journeys for banks to follow; one such journey was to operate a full-service bank with a focus on affluent customers and small business.

“The full-service bank in its simplification journey is likely to focus on extending existing centres of excellence, as well as transformation of existing capabilities,” he said.

Another option was for a mainstream bank to be value-focused bank with a focus on efficiency.

“A value-focused bank is more likely to develop-to-replace (including through a neobank) or adopt third-party solutions,” he said.

The final journey said Mr Verbeek would be for a major bank to reposition itself as an embedded finance institution.

“The embedded finance bank will open itself to an eco-system of partners and partnering will be a strategic activity. It is likely to replace rather than transform many of its banking modules,” he said.

Mr Verbeek said that banks needed to plan for simplification immediately as it required management and board focus to achieve.

“It starts with agreeing on the bank’s long-term strategic focus. This could be done concurrently with a maturity assessment of the bank’s existing activities,” he said.

The KPMG end of year analysis found that of the big four banks the worse performer was NAB who came last in the rankings on all but one measure and the top performer was CBA, followed by Westpac with ANZ close behind.

In the 2018 financial year CBA made over $9.2 million in cash profit after tax, while NAB made just over half of that with $5.7 million.

The report said it was clear that the royal commission and the APRA and AUSTRAC inquiries into CBA were felt by all the banks with various compliance and remediation costs all increasing.

The report said that, looking forward, competition was predicted to remain robust as non-bank players and challenger banks were entering the market.

However, business and corporate banking could not expect to pick up all the mortgage market slack and, as a result, total net interest income will be subdued.

The latest minutes from the RBA continues the steady-as-we-go story, once again and so the cash rate remains on hold.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economic expansion is continuing. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. Growth in China has slowed a little, with the authorities easing policy while continuing to pay close attention to the risks in the financial sector. Globally, inflation remains low, although it has increased due to both higher oil prices and some lift in wages growth. A further pick-up in inflation is expected given the tight labour markets and, in the United States, the sizeable fiscal stimulus. One ongoing uncertainty regarding the global outlook stems from the direction of international trade policy in the United States.

Financial conditions in the advanced economies remain expansionary but have tightened somewhat recently. Equity prices have declined and yields on government bonds in some economies have increased, although they remain low. There has also been a broad-based appreciation of the US dollar this year. In Australia, money-market interest rates have declined recently, after increasing earlier in the year. Standard variable mortgage rates are a little higher than a few months ago and the rates charged to new borrowers for housing are generally lower than for outstanding loans.

The Australian economy is performing well. Over the past year, GDP increased by 3.4 per cent and the unemployment rate declined to 5 per cent, the lowest in six years. The forecasts for economic growth in 2018 and 2019 have been revised up a little. The central scenario is for GDP growth to average around 3½ per cent over these two years, before slowing in 2020 due to slower growth in exports of resources. Business conditions are positive and non-mining business investment is expected to increase. Higher levels of public infrastructure investment are also supporting the economy, as is growth in resource exports. One continuing source of uncertainty is the outlook for household consumption. Growth in household income remains low, debt levels are high and some asset prices have declined. The drought has led to difficult conditions in parts of the farm sector.

Australia’s terms of trade have increased over the past couple of years and have been stronger than earlier expected. This has helped boost national income. While the terms of trade are expected to decline over time, they are likely to stay at a relatively high level. The Australian dollar remains within the range that it has been in over the past two years on a trade-weighted basis, although it is currently in the lower part of that range.

The outlook for the labour market remains positive. With the economy growing above trend, a further reduction in the unemployment rate is expected to around 4¾ per cent in 2020. The vacancy rate is high and there are reports of skills shortages in some areas. Wages growth remains low, although it has picked up a little. The improvement in the economy should see some further lift in wages growth over time, although this is still expected to be a gradual process.

Inflation remains low and stable. Over the past year, CPI inflation was 1.9 per cent and, in underlying terms, inflation was 1¾ per cent. These outcomes were in line with the Bank’s expectations and were influenced by declines in some administered prices due to changes in government policies. Inflation is expected to pick up over the next couple of years, with the pick-up likely to be gradual. The central scenario is for inflation to be 2¼ per cent in 2019 and a bit higher in the following year.

Conditions in the Sydney and Melbourne housing markets have continued to ease and nationwide measures of rent inflation remain low. Growth in credit extended to owner-occupiers has eased but remains robust, while demand by investors has slowed noticeably as the dynamics of the housing market have changed. Credit conditions are tighter than they have been for some time, although mortgage rates remain low and there is strong competition for borrowers of high credit quality.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.