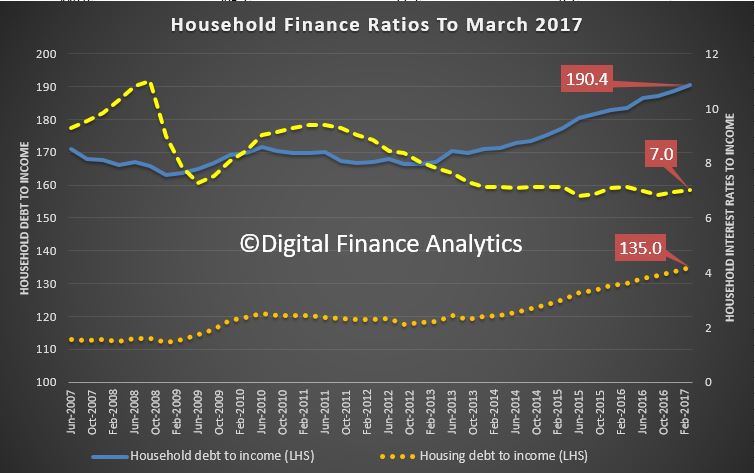

As part of our household survey we had the chance to discuss household debt in our focus group. We had selected participants with large debt burdens, because we wanted to understand better what was driving this behaviour. It was mixed group, with households represented between 20 and 60 years, from multiple locations. The RBA data showing high household debt prompted the research.

In the session, a number of themes emerged. Yes we got the story about incomes not rising, costs going up and big mortgages; as expected. But there was another theme that struck home to the facilitators.

It is this. Around two thirds of the households in the session had a basic assumption that high debt levels were normal. They had often accumulated debts through their education, when they bought a house, and running credit cards. Even more interestingly, their concern from a cash flow perspective was about servicing the debts, not repaying them.

One quote which struck home was “once I am dead, my debts are cancelled”, I just keep borrowing til then.

Wow! Debt, it seems has become part of the furniture, and will remain a spectre at the feast throughout their lifetime. The banks will be happy!

But this got me thinking about the implications of this observation. If households are making debt decisions based on just debt servicing, what does that say about their future cash flow in a low income growth, potentially rising interest rate environment? Is this normal behaviour now? Has financial literacy failed, or is there a new logic in town?

If there is, then I have to ask – am I out of kilter in believing that debt can be useful, but it should be paid down as soon as possible, and that borrowing is the exception, not the rule. Or is the new normal to be saddled with high debt, and live with it? For ever?

The remaining one third, by the way, were more conscious of the need to repay, and were surprised by the majority view in the room.

No wonder households are more highly in debt than ever as the recent RBA data shows. But what I am getting at are the cultural norms which now exist. As a result, lenders will continue to have a field day, but what are the true economic and social costs of this phenomenon?

We hope to do more research on this. Watch this space.

One thought on “Is This Amount of Debt “Normal”?”