In the RBA’s latest Statement on Monetary Policy, they explore the impact of off-set accounts on the total household debt outstanding.

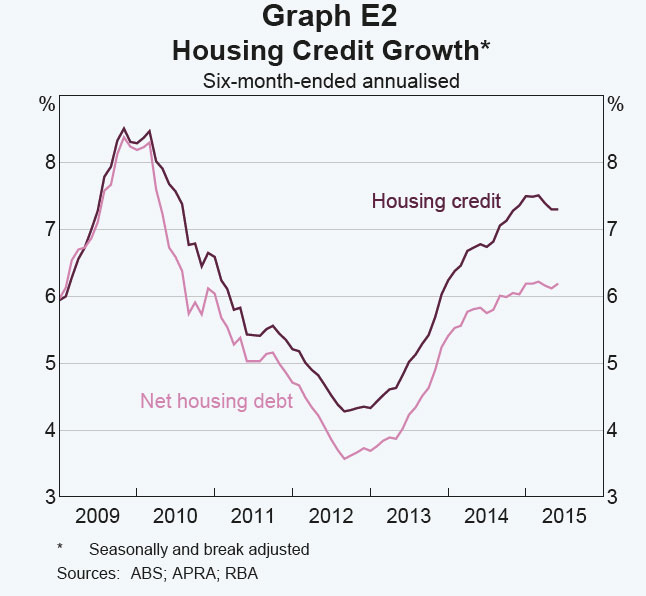

The increase in housing credit growth over recent years has been accompanied by rapid growth in loan products that provide borrowers with access to offset accounts. Offset accounts are a type of deposit account that are directly linked to a loan, such as a mortgage. Funds deposited into offset accounts effectively reduce the borrower’s net debt position and the interest payable on the loan. Offset account balances currently amount to around $90 billion, equivalent to over 6 per cent of housing loans outstanding. Since offset account balances have been growing by around 30 per cent annually over recent years, annual growth in net housing debt, which takes into account offset accounts, is about 6 per cent. This compares with annual growth in housing credit of around 7 per cent.

The RBA compiles monthly statistics that measure the stock of outstanding credit. Changes in the stock of credit reflect various flows during the month. In the case of housing credit, for example, borrowers are required to make scheduled repayments and often also have the option of making additional repayments, which are referred to here as mortgage prepayments. Mortgage prepayments include those for loans with redraw facilities, which give the borrower the option of withdrawing accumulated

prepaid funds in the future. All mortgage payments, whether scheduled or prepaid, reduce the stock of outstanding credit, thereby reducing the rate of growth of credit. When households choose to pay back their mortgage faster than scheduled by making prepayments, this lowers credit growth.

Offset accounts are an alternative form of mortgage prepayment that are not treated as such when measuring housing credit. An offset account typically acts like an at-call deposit account, with funds in the account netted against the borrower’s outstanding mortgage balance for the purposes of calculating interest on the loan. Because it acts like an at-call deposit account, any accumulated funds are easily available for withdrawal or for purchasing goods and services. As mentioned above, balances in offset accounts have been increasing rapidly, with growth over recent years around 30 per cent. This growth has the potential to continue as older loans that are less likely to have offset accounts are replaced with new loans, where it is more common to have an offset account. Available redraw balances, at around $120 billion, are larger than offset account balances, but have grown at a pace closer to 10 per cent over recent years.

For a household with a mortgage, mortgage prepayments made using a redraw facility or a deposit into an offset account have a similar economic effect. In both cases, a household’s net housing debt and interest payable are reduced. Thus, while the effect on household balance sheets differs – loans and deposits are higher than they otherwise would be if offset accounts are used – net housing debt is the same. Since offset account balances have been growing much more rapidly than housing credit, net housing debt is growing more slowly than housing credit; over the six months to June, annualised net housing debt growth was around 6 per cent, compared to 7 per cent for housing credit growth (Graph E2).  The effect is slightly larger for credit extended to investors than to owner-occupiers, reflecting the fact that investor offset account balances have grown more quickly than balances for owner-occupiers. Offset account balances have also been making a significant contribution to household deposit growth; excluding offset account balances reduces growth in household deposits by around 1 percentage point to 71/2 per cent.

The effect is slightly larger for credit extended to investors than to owner-occupiers, reflecting the fact that investor offset account balances have grown more quickly than balances for owner-occupiers. Offset account balances have also been making a significant contribution to household deposit growth; excluding offset account balances reduces growth in household deposits by around 1 percentage point to 71/2 per cent.

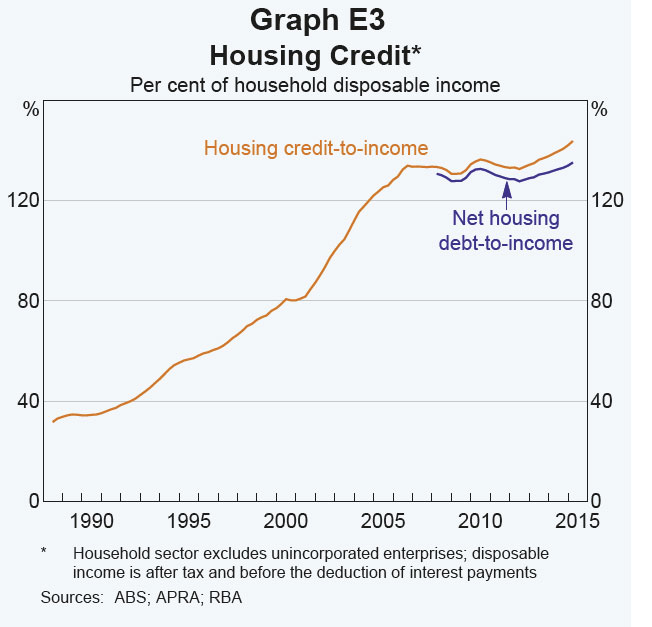

The treatment of offset account balances also has implications for measuring the household debt-to-income ratio. Housing credit is the major component of household debt. Without adjusting the stock of outstanding housing credit for offset account balances, housing debt as a share of household disposable income has been increasing since mid 2012 to be at a historical high of 144 per cent (Graph E3). Adjusting for offset account balances suggests that this ratio has been rising at a slower pace, and has only just surpassed its most recent peak in late 2010.