The September 2017 Bank for International Settlements Quarterly Review says that the combination of a stronger outlook plus low inflation spurs risk-taking. But the quest for the “missing inflation” has become the focus.

Low inflation despite a stronger economic outlook helped push markets up in recent months and reduced the expected pace of tightening of monetary policy in major economies. Signs of increased risk-taking have become apparent in a number of areas, including narrow credit spreads, increased carry trade activity and looser bond covenants.

“All this puts a premium on understanding the ‘missing inflation’, because inflation is the lodestar for central banks,” said Claudio Borio, Head of the Monetary and Economic Department.

The September 2017 issue of the Quarterly Review:

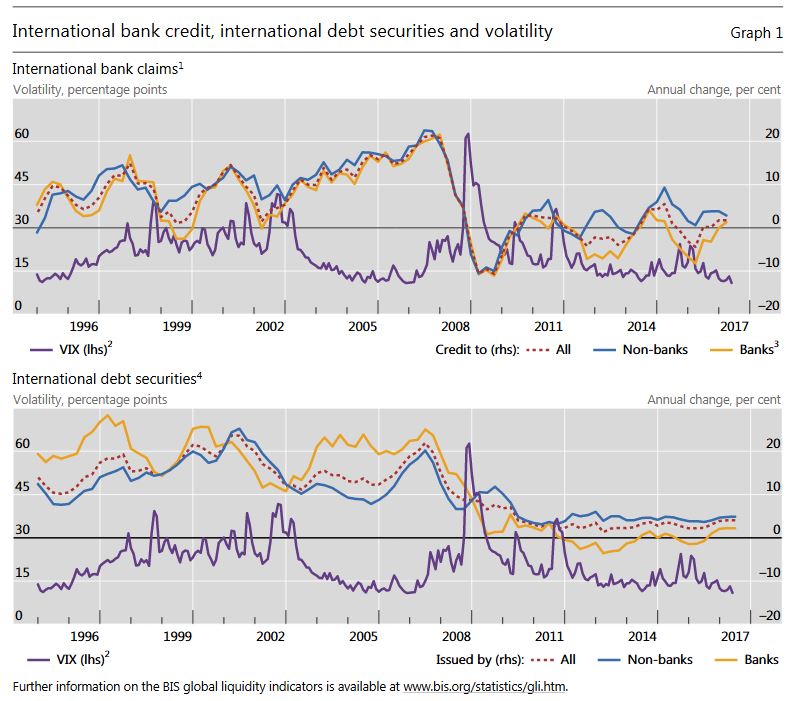

- Shows a pickup in the growth of international debt securities in the first half of 2017, when total stocks rose to $22.7 trillion. The outstanding stock of securities issued by banks grew at its fastest pace in six years.

- Calculates that credit-to-GDP ratios remained well above trend levels for a number of jurisdictions, often coinciding with wide property price gaps. Demand from projects financed by property developers may play a role.

- Reviews the doubling in outstanding government debt of emerging market economies since 2007, to $11.7 trillion at end-2016. Government debt rose from 41% to 51% of GDP over the same period. Emerging market government borrowing is mostly at longer maturities, at fixed rates and in local currencies, and its pattern increasingly resembles that of advanced economies.

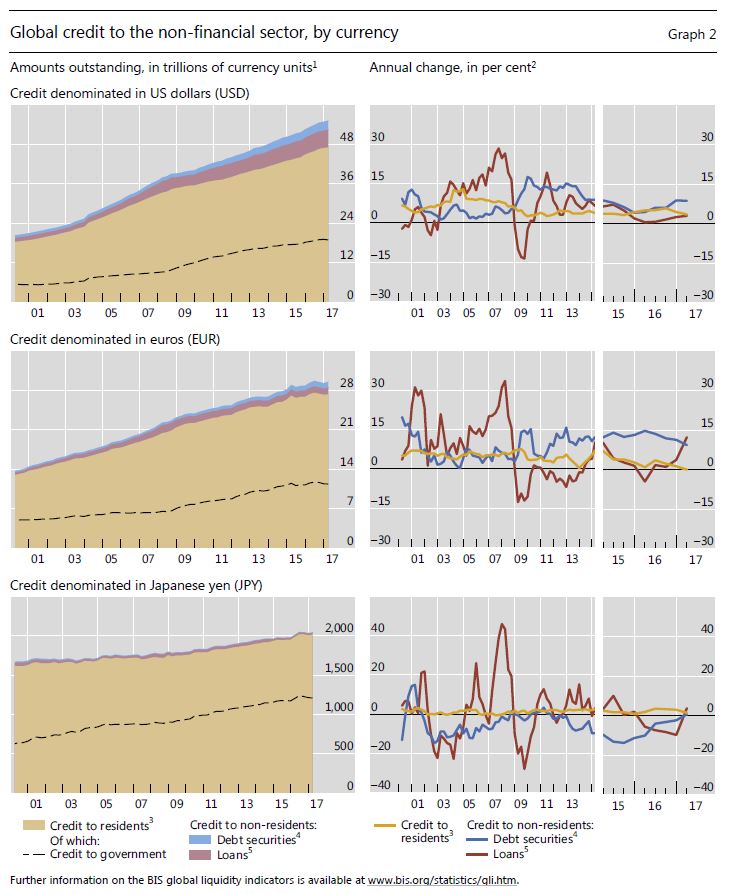

- Reports on new data initiatives aimed at assessing the exposure of economies to foreign currency risk. From now on, the BIS will regularly publish a currency breakdown of cross-border loans and deposits. Bank loans can be added to debt securities to estimate the build-up of total foreign currency debt. Country-level estimates of total US dollar, euro and yen credit provide a better gauge of foreign currency indebtedness of borrowers in a given country and its vulnerability to currency fluctuations. The BIS is also releasing new data series on monetary policy rates and exchange rates.

Special features look at topical issues in global markets and economics:

- Claudio Borio, Robert McCauley and Patrick McGuire (BIS)* analyse the amount of debt incurred by borrowing through FX swaps and forwards, a missing element in assessments of financial stability risk. The authors estimate the size, distribution and use of this missing debt, and assess its implications for financial stability. The off-balance sheet dollars owed by non-banks outside the United States may exceed their $10.7 trillion of on-balance sheet dollar debt (as of Q1 2017). The missing debt is secured with foreign currency, is mostly short-term and is likely to generally serve as a hedge for FX exposures in cash flows and on balance sheets. But rolling over short-term hedges of long-term assets can still spark or amplify funding and liquidity problems during periods of stress.

“This research is the first to put a number on the amount of dollar debt missing from balance sheets and fills in a gap in our understanding of liquidity risk posed by financial firms operating across different currencies,” said Hyun Song Shin, Economic Adviser and Head of Research. - Morten Bech (BIS) and Rodney Garratt (UCSB) outline how central banks might create and use blockchain-based digital currencies. They identify two types of such potential central bank cryptocurrencies, one for consumers and the other for large-value payments, and compare them with existing payment options.

- Codruta Boar, Leonardo Gambacorta, Giovanni Lombardo and Luiz Pereira da Silva (BIS) find that countries which frequently use macroprudential tools have tended to have higher and more stable economic growth rates. On the other hand, ad hoc interventions could hurt growth.

- Torsten Ehlers and Frank Packer (BIS) argue that more consistent standards for green bonds could help develop the market for instruments to finance investments with environmental or climate-related benefits. Although there is some evidence that investors have paid a premium on average at issuance for certified green bonds, the bonds have not generally underperformed conventional ones in the secondary market.

Missing inflation? Well when the BIS banker gets in his BMW with active safety (reduces cost by reducing accidents), stops at a worker less grocery shop (cheaper groceries), gets home and buys something online (cheaper no middle men) and watches Netflix (cheaper no going to the movies) and thinks about getting rid of the BMW and using UBER instead (cheaper-no car ownership), maybe they can reflect on where the “inflation” has gone? Personally just in the entertainment space by joining Netflix and iTune’s music I’m now saving over $100 a month by not buying music or going to the movies. I don’t wonder where inflation’s gone, I wonder when “deflation” will start being accurately reported. Electric trucks are forecast to reduce operating costs by as much as 70% over current trucks, Precision Medicine is forecast to drop medical cost by as much as 60%. The central banks will have to find another way to clear there debts, inflation is not around to do it.